Download as pdf or txt

You might also like

- Final Grading Exam - Key AnswersDocument35 pagesFinal Grading Exam - Key AnswersJEFFERSON CUTE97% (32)

- IA ReviewerDocument8 pagesIA ReviewerKaren Clarisse Alimot0% (2)

- 11 Picks From Warren Buffett's BookshelfDocument4 pages11 Picks From Warren Buffett's Bookshelfgrh04No ratings yet

- Audit of Long Term Liabilities 2Document5 pagesAudit of Long Term Liabilities 2Cesar EsguerraNo ratings yet

- Noncurrent Liabilities - PROBLEMS: B. A DiscountDocument12 pagesNoncurrent Liabilities - PROBLEMS: B. A DiscountIra Grace De Castro67% (3)

- 2018 Level II Mock Exam PMDocument26 pages2018 Level II Mock Exam PMHui GuoNo ratings yet

- Bonds Problem With Solutions 2Document4 pagesBonds Problem With Solutions 2reviewrecord.rr2No ratings yet

- Quiz 2 BP With Answers PDFDocument4 pagesQuiz 2 BP With Answers PDFspur iousNo ratings yet

- Quiz 2 BP With AnswersDocument4 pagesQuiz 2 BP With Answersspur iousNo ratings yet

- Quiz 2 BPDocument4 pagesQuiz 2 BPspur iousNo ratings yet

- AP-LIABS-3 (With Answers)Document4 pagesAP-LIABS-3 (With Answers)Kendrew SujideNo ratings yet

- Audprob Bonds Problem With SolutionsDocument4 pagesAudprob Bonds Problem With Solutionsreviewrecord.rr2No ratings yet

- 9TH Bonds Payable Part IIDocument8 pages9TH Bonds Payable Part IIAnthony DyNo ratings yet

- Compound Financial InstrumentDocument2 pagesCompound Financial Instrumenthae1234No ratings yet

- Chapter 20 - Effective Interest Method (Amortized Cost, FVOCI, FVPL)Document66 pagesChapter 20 - Effective Interest Method (Amortized Cost, FVOCI, FVPL)Never Letting GoNo ratings yet

- January 1, 2020 P5,388,835 December 31, 2020 P550,000 P484,995 P65,005Document7 pagesJanuary 1, 2020 P5,388,835 December 31, 2020 P550,000 P484,995 P65,005gazer beamNo ratings yet

- Module - IA Chapter 6Document10 pagesModule - IA Chapter 6Kathleen EbuenNo ratings yet

- Nfjpia Cup - Auditing Problems SGV & Co. Easy Question #1: Answer: P126,816Document18 pagesNfjpia Cup - Auditing Problems SGV & Co. Easy Question #1: Answer: P126,816Merliza Jusayan100% (1)

- Effective Interest MethodDocument31 pagesEffective Interest MethodMikaela LacabaNo ratings yet

- Bonds Payable Bond - Is A Formal Unconditional Promise, Made Under Seal, To Pay A Specified Sum of Money at ADocument8 pagesBonds Payable Bond - Is A Formal Unconditional Promise, Made Under Seal, To Pay A Specified Sum of Money at ACamille BacaresNo ratings yet

- Accounting 1Document10 pagesAccounting 1Jay EbuenNo ratings yet

- Chapter 3 Problem 6 LenzierDocument25 pagesChapter 3 Problem 6 LenzierJohn Lenzier TurtorNo ratings yet

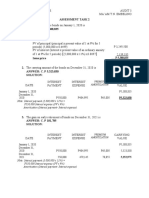

- Assessment Task 3Document5 pagesAssessment Task 3Christian N MagsinoNo ratings yet

- Chapter 3 Problem 6 LenzierDocument25 pagesChapter 3 Problem 6 LenzierJohn Lenzier TurtorNo ratings yet

- Ia2 Final Exam A Test Bank - CompressDocument32 pagesIa2 Final Exam A Test Bank - CompressFiona MiralpesNo ratings yet

- Name: Michelle J. Sabit Section Code: B6 Date: 02/24/2024Document3 pagesName: Michelle J. Sabit Section Code: B6 Date: 02/24/2024sabit.michelle0903No ratings yet

- Note Payable Irrevocably Designated As at Fair Value Through Profit or LossDocument4 pagesNote Payable Irrevocably Designated As at Fair Value Through Profit or Lossnot funny didn't laughNo ratings yet

- Notes ReceivableDocument47 pagesNotes ReceivableAlexandria Ann FloresNo ratings yet

- DocumentDocument3 pagesDocumentsabit.michelle0903No ratings yet

- Pa4-Chapter-3.Garcia J John Vincent DDocument5 pagesPa4-Chapter-3.Garcia J John Vincent DJohn Vincent GarciaNo ratings yet

- Intermediate Accounting 2Document4 pagesIntermediate Accounting 2MARRIETTE JOY ABADNo ratings yet

- 2020 Spring Midterm II A AnsKey PDFDocument12 pages2020 Spring Midterm II A AnsKey PDFEunice GuoNo ratings yet

- Me AnswersDocument9 pagesMe Answersgabprems11No ratings yet

- Ia PPT 6Document20 pagesIa PPT 6lorriejaneNo ratings yet

- Prob.2 Classroom Discussion BP OCDocument4 pagesProb.2 Classroom Discussion BP OCWenjunNo ratings yet

- Investments in Debt SecuritiesDocument34 pagesInvestments in Debt SecuritiesNobu NobuNo ratings yet

- Sol. Man. - Chapter 3 Bonds Payable & Other ConceptsDocument23 pagesSol. Man. - Chapter 3 Bonds Payable & Other ConceptsMiguel Amihan100% (1)

- T5 - Qs and SolutionDocument15 pagesT5 - Qs and SolutionCalvin MaNo ratings yet

- Homework 4 - 5th EdDocument4 pagesHomework 4 - 5th EdNandini GoyalNo ratings yet

- Sol. Man. - Chapter 3 Bonds Payable Other ConceptsDocument21 pagesSol. Man. - Chapter 3 Bonds Payable Other ConceptsJasmine Nouvel Soriaga Cruz86% (7)

- Assignment 1 - SolutionsDocument8 pagesAssignment 1 - SolutionsSiying GuNo ratings yet

- AFM RevisionDocument8 pagesAFM RevisionSomabhizinisi MazibukoNo ratings yet

- Anathi LukweDocument10 pagesAnathi Lukwetivanani baloyiNo ratings yet

- Problem 6: For Classroom Discussion: Requirement (A)Document6 pagesProblem 6: For Classroom Discussion: Requirement (A)Nikky Bless LeonarNo ratings yet

- Inter AccDocument6 pagesInter AccshaylieeeNo ratings yet

- CH 14: Long Term Liabilities: The Timelines of The Bonds Will Be As FollowsDocument9 pagesCH 14: Long Term Liabilities: The Timelines of The Bonds Will Be As Followschesca marie penarandaNo ratings yet

- Tutorial 13 14 Answer MFRS9Document4 pagesTutorial 13 14 Answer MFRS9NavaneetaNo ratings yet

- 7 Loan ReceivableDocument10 pages7 Loan ReceivableAYEZZA SAMSONNo ratings yet

- Debt Financing SolutionsDocument3 pagesDebt Financing SolutionsSleepy marshmallowNo ratings yet

- TOPIC 1 Accounting For Financial LiabilitiesDocument45 pagesTOPIC 1 Accounting For Financial LiabilitiesZe KhaiNo ratings yet

- Chapter 3 Bonds Payable Other ConceptsDocument20 pagesChapter 3 Bonds Payable Other ConceptsThalia Rhine AberteNo ratings yet

- Psa Financial Reporting AssignmentDocument8 pagesPsa Financial Reporting AssignmentNyara MakurumidzeNo ratings yet

- Acquisition & Interest Date Interest Earned (NR X Face) A Interest Income (ER X BV) B Discount Amortization A-B Book Value 07/01/14 12/31/14 12/31/15Document3 pagesAcquisition & Interest Date Interest Earned (NR X Face) A Interest Income (ER X BV) B Discount Amortization A-B Book Value 07/01/14 12/31/14 12/31/15Gray JavierNo ratings yet

- IA2 Chapter3 ExercisesDocument4 pagesIA2 Chapter3 Exercisesmarriette joy abadNo ratings yet

- Acctg34 Franchise Pret. Remaining Items AkeyDocument6 pagesAcctg34 Franchise Pret. Remaining Items AkeyDonna Mae SingsonNo ratings yet

- PQ3 BondsDocument2 pagesPQ3 BondsElla Mae MagbatoNo ratings yet

- AP 5902 Liability Supporting NotesDocument6 pagesAP 5902 Liability Supporting NotesMeojh Imissu100% (1)

- IA2Document9 pagesIA2Claire BarbaNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Quiz 2 Answers SolutionsDocument29 pagesQuiz 2 Answers SolutionsMarcus Monocay100% (2)

- Sol DissolutionDocument40 pagesSol DissolutionBlastik FalconNo ratings yet

- Wa0002.Document4 pagesWa0002.arviii63No ratings yet

- Pert 12 Intercorporate Investments Chapter15Document34 pagesPert 12 Intercorporate Investments Chapter15Chevalier ChevalierNo ratings yet

- Chapter 3 Economic Study MethodsDocument62 pagesChapter 3 Economic Study MethodsJohn Fretz AbelardeNo ratings yet

- Spice House Business PlanDocument9 pagesSpice House Business Plananon_22054856No ratings yet

- Emperical ResearchDocument63 pagesEmperical ResearchJatin BansalNo ratings yet

- Reading 31 Valuation of Contingent Claims - Answers.Document48 pagesReading 31 Valuation of Contingent Claims - Answers.NeerajNo ratings yet

- Primarry and Secondary MarketDocument7 pagesPrimarry and Secondary MarketDiyaNo ratings yet

- Finacial Analysis - PDF MRFDocument9 pagesFinacial Analysis - PDF MRFharshNo ratings yet

- BDHCH 13Document40 pagesBDHCH 13tzsyxxwhtNo ratings yet

- Acct Cheat SheetDocument3 pagesAcct Cheat SheetAllen LiouNo ratings yet

- JE vs. Memo Method IllustrationDocument2 pagesJE vs. Memo Method IllustrationccanapizingaboNo ratings yet

- 126105601chutuburu Jamshedpur 18Document3 pages126105601chutuburu Jamshedpur 18Sanjay KumarNo ratings yet

- Audit and Assuranc1Document5 pagesAudit and Assuranc1shaazNo ratings yet

- High Quality Dividend Investing Guide EbookDocument17 pagesHigh Quality Dividend Investing Guide EbookDelwitt CampeloNo ratings yet

- Pas 28 Investment in Associates and Joint VenturesDocument14 pagesPas 28 Investment in Associates and Joint VenturesGenivy SalidoNo ratings yet

- Martin J Rosenburgh CVDocument2 pagesMartin J Rosenburgh CVMartin RosenburghNo ratings yet

- Intermediate Accounting I - Investment Part 1Document3 pagesIntermediate Accounting I - Investment Part 1Joovs Joovho0% (3)

- FN2191 Commentary 2022Document27 pagesFN2191 Commentary 2022slimshadyNo ratings yet

- Tutorial - Depreciation 19 PDFDocument2 pagesTutorial - Depreciation 19 PDFSetsuna TeruNo ratings yet

- Restructuring at Neiman Marcus Group (A)Document33 pagesRestructuring at Neiman Marcus Group (A)Shaikh Saifullah KhalidNo ratings yet

- Day Count ConventionDocument11 pagesDay Count Conventiontimothy454No ratings yet

- Asset Turnover Ratio Definition - InvestopediaDocument4 pagesAsset Turnover Ratio Definition - InvestopediaBob KaneNo ratings yet

- U74999HR2017PTC066978 OTRE 143398915 Form-PAS-3-20012020 SignedDocument5 pagesU74999HR2017PTC066978 OTRE 143398915 Form-PAS-3-20012020 Signedakshay bhartiyaNo ratings yet

- RentechDocument31 pagesRentechjimNo ratings yet

- The Count - Rem - 3Document33 pagesThe Count - Rem - 3Scott BoogemansNo ratings yet

- Accept Less - Reject Greater: IRR Is The Interest Rate That Makes The NPV 0: 0 +$200 - $2501+IRR Solving For IRRDocument10 pagesAccept Less - Reject Greater: IRR Is The Interest Rate That Makes The NPV 0: 0 +$200 - $2501+IRR Solving For IRRAtheer Al-AnsariNo ratings yet