Download as doc, pdf, or txt

You might also like

- Financial Managerial Accounting 3Rd Edition Horngren Solutions Manual Full Chapter PDFDocument31 pagesFinancial Managerial Accounting 3Rd Edition Horngren Solutions Manual Full Chapter PDFMeganPrestonceim100% (17)

- Journey To Series A e BookDocument57 pagesJourney To Series A e BookDare LawansonNo ratings yet

- Solution Manual For Finance For Non Financial Managers Fourth Canadian EditionDocument20 pagesSolution Manual For Finance For Non Financial Managers Fourth Canadian EditionEdna Steward100% (38)

- RETADocument37 pagesRETAJoshua ChavezNo ratings yet

- Invoice 1535361450 PDFDocument2 pagesInvoice 1535361450 PDFHappy Stay Service Apartments ChennaiNo ratings yet

- The Statement of Cash Flows-TheoryDocument3 pagesThe Statement of Cash Flows-TheoryApryl TaiNo ratings yet

- SOLUTI~2Document39 pagesSOLUTI~2kevinkariuki227No ratings yet

- Bsbfia401 Amit ChhetriDocument20 pagesBsbfia401 Amit Chhetriamitchettri419No ratings yet

- Accounting Principles, Liabilities & Payroll System in An Ethiopian ContextDocument15 pagesAccounting Principles, Liabilities & Payroll System in An Ethiopian ContextAbdu AliNo ratings yet

- Cash Flow StatementDocument37 pagesCash Flow Statementg28720081No ratings yet

- Midterm Chapter1 2 3Document3 pagesMidterm Chapter1 2 3Mae Ann AvenidoNo ratings yet

- Acctg11e - SM - CH03 For 25 - 29 Sept 2017Document114 pagesAcctg11e - SM - CH03 For 25 - 29 Sept 2017Dylan Rabin Pereira100% (1)

- How To Be An Investment Banker - Q&A PDFDocument30 pagesHow To Be An Investment Banker - Q&A PDFEric LukasNo ratings yet

- Vinayak 22251 Accounts 1Document5 pagesVinayak 22251 Accounts 1vinayakNo ratings yet

- ACCA NoteDocument21 pagesACCA NoteTanbir Ahsan RubelNo ratings yet

- Dwnload Full Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions Manual PDFDocument36 pagesDwnload Full Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions Manual PDFjayden77evans100% (18)

- Full Download Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions ManualDocument36 pagesFull Download Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions Manualcolagiovannibeckah100% (33)

- Prepare The Statement of Cash Flows Using The Indirect MethodDocument4 pagesPrepare The Statement of Cash Flows Using The Indirect MethodcindywNo ratings yet

- 11 Accountany II Goalias BlogspotDocument296 pages11 Accountany II Goalias BlogspotRanbir Singh JamwalNo ratings yet

- Receivables ChecklistDocument6 pagesReceivables ChecklistAngeliNo ratings yet

- Audit QNS-1Document4 pagesAudit QNS-1kiddyhimsselfNo ratings yet

- PayrollDocument3 pagesPayrolllakhman100% (1)

- Accountancy Class XIDocument296 pagesAccountancy Class XIkarthikmk90100% (1)

- 2009 Study Questions - MelvilleDocument7 pages2009 Study Questions - MelvillebollenNo ratings yet

- Payroll Accounting 2015 Bieg 25th Edition Solutions ManualDocument31 pagesPayroll Accounting 2015 Bieg 25th Edition Solutions ManualBrittanyMorrismxgo100% (51)

- List The Country Specific Payroll InfotypesDocument15 pagesList The Country Specific Payroll InfotypesPradeep KumarNo ratings yet

- What Is GAAPDocument13 pagesWhat Is GAAPmshashi5No ratings yet

- BSBFIM601 Manage Finances Task 1Document16 pagesBSBFIM601 Manage Finances Task 1Kathleen RamientoNo ratings yet

- Financial Managerial Accounting 3rd Edition Horngren Solutions ManualDocument10 pagesFinancial Managerial Accounting 3rd Edition Horngren Solutions Manualexsect.drizzlezu95% (21)

- Wa0019.Document96 pagesWa0019.Ali KingNo ratings yet

- BACCTG1Document4 pagesBACCTG1Athena MillerNo ratings yet

- Payroll Accounting 2015 25th Edition Bieg Solutions ManualDocument31 pagesPayroll Accounting 2015 25th Edition Bieg Solutions Manualhofulchondrin6migjb100% (35)

- Midterm 112Document3 pagesMidterm 112Mae Ann AvenidoNo ratings yet

- Cash Flows ExercicesDocument96 pagesCash Flows ExercicesAbdelmajid JamaneNo ratings yet

- Alaya-Ay, Regine MDocument3 pagesAlaya-Ay, Regine MMae Ann AvenidoNo ratings yet

- Acc Ans CP1Document48 pagesAcc Ans CP1wingssNo ratings yet

- Foreignlanguage InbusinessDocument5 pagesForeignlanguage InbusinessChirilenco ValeaNo ratings yet

- Accounting Chap 1 DiscussionDocument7 pagesAccounting Chap 1 DiscussionVicky Le100% (2)

- DC Tacn Ki IiDocument6 pagesDC Tacn Ki IiHà Phương TrầnNo ratings yet

- Accounting BasicsDocument10 pagesAccounting BasicsBhandare KautikNo ratings yet

- Fundamentals of Financial Accounting Canadian 4th Edition by Phillips Libby and Mackintosh ISBN Solution ManualDocument49 pagesFundamentals of Financial Accounting Canadian 4th Edition by Phillips Libby and Mackintosh ISBN Solution Manualnadia100% (34)

- Chapter 1: Business Decisions and Financial AccountingDocument36 pagesChapter 1: Business Decisions and Financial Accountingnancy.rodriguez985100% (12)

- Before Course Exam SBSDocument17 pagesBefore Course Exam SBSGia LâmNo ratings yet

- Accrued Liabilities and Deferred RevenueDocument2 pagesAccrued Liabilities and Deferred RevenueanonymousjoeyNo ratings yet

- Discussion Question: Nama: Putu Febri Berliana Irawan ABSEN /NIM: 23 / 18106053 Kelas: Mah B 5Document1 pageDiscussion Question: Nama: Putu Febri Berliana Irawan ABSEN /NIM: 23 / 18106053 Kelas: Mah B 5FEBRI IRAWANNo ratings yet

- Questions Chap2Document2 pagesQuestions Chap2Ghassan EidNo ratings yet

- Reviewer For Quali CFASDocument12 pagesReviewer For Quali CFASJethro DonascoNo ratings yet

- Financial Statements and AnalysisDocument5 pagesFinancial Statements and AnalysisLeyla SuleymanliNo ratings yet

- ACCT 221 Chapter 1Document26 pagesACCT 221 Chapter 1Shane Hundley100% (1)

- Chapter 1-SolutionsDocument55 pagesChapter 1-Solutionstongthanhthao265No ratings yet

- Chapter 1Document42 pagesChapter 1aluatNo ratings yet

- CH 10Document6 pagesCH 10Cris LuNo ratings yet

- Establish Maintain A Payroll SystemDocument17 pagesEstablish Maintain A Payroll SystemReta TolesaNo ratings yet

- Cash Flow StatementDocument4 pagesCash Flow StatementSs KkNo ratings yet

- Midterm ExamDocument3 pagesMidterm ExamMae Ann AvenidoNo ratings yet

- Financial Accounting Libby 7th Edition Solutions Manual download pdf full chapterDocument29 pagesFinancial Accounting Libby 7th Edition Solutions Manual download pdf full chapterunkoazamo100% (8)

- Full download Financial Accounting Libby 7th Edition Solutions Manual file pdf free all chapterDocument29 pagesFull download Financial Accounting Libby 7th Edition Solutions Manual file pdf free all chapterblisscomms100% (1)

- Survey of Accounting Homework Written AssignmentDocument22 pagesSurvey of Accounting Homework Written AssignmentEMZy ChannelNo ratings yet

- Finnancial AccountingDocument10 pagesFinnancial AccountingNaveenNo ratings yet

- Chapter 4Document56 pagesChapter 4Crystal Brown100% (1)

- Accounting ConceptsDocument11 pagesAccounting ConceptssyedasadaligardeziNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- HDFC Bank: CMP: INR537 TP: INR600 NeutralDocument12 pagesHDFC Bank: CMP: INR537 TP: INR600 NeutralDarshan RavalNo ratings yet

- Maroof Black BookDocument61 pagesMaroof Black Bookharshgudhka55No ratings yet

- Financial Statements With Adjustments (Accounts)Document13 pagesFinancial Statements With Adjustments (Accounts)ChiragNo ratings yet

- Answer - Final ExamsDocument5 pagesAnswer - Final Examsyen claveNo ratings yet

- CM 6549 20220528025414Document7 pagesCM 6549 20220528025414AT100% (1)

- Time Value of Money - ProblemsDocument10 pagesTime Value of Money - Problemsjav3d762No ratings yet

- Chapter 13Document30 pagesChapter 13REEMA BNo ratings yet

- Secondary MarketDocument20 pagesSecondary Marketoureducation.inNo ratings yet

- HPG Finance Statement 1Document25 pagesHPG Finance Statement 1Hoàng Ngọc OanhNo ratings yet

- Finallllllllll Report BBA MCB ADocument55 pagesFinallllllllll Report BBA MCB AMahrukh WaheedNo ratings yet

- Chapter 5Document65 pagesChapter 5Sena KahramanNo ratings yet

- Finance Final Project DetailsDocument2 pagesFinance Final Project DetailswajeehNo ratings yet

- RA 7653 (Sec. 96-102)Document2 pagesRA 7653 (Sec. 96-102)Toki BatumbakalNo ratings yet

- Test #1 Chapters 1-4 Review: Personal Finance For Fiscal Wellness Dan W. Royer, Ed.D., CpaDocument33 pagesTest #1 Chapters 1-4 Review: Personal Finance For Fiscal Wellness Dan W. Royer, Ed.D., CpaMichael EvansNo ratings yet

- Liu NguyenDocument33 pagesLiu NguyenYulianita AdrimaNo ratings yet

- Non-Funded Credit (Bank Guarantee)Document17 pagesNon-Funded Credit (Bank Guarantee)vrmistry6No ratings yet

- Activity 11: ExplanationDocument11 pagesActivity 11: ExplanationDonabelle Marimon0% (1)

- Interpreting Financial DataDocument3 pagesInterpreting Financial Dataapi-693298996No ratings yet

- (MCOF19M028) CF AssignmentDocument5 pages(MCOF19M028) CF AssignmentFaaiz YousafNo ratings yet

- 04 .All About Int Rates, Zero RatesDocument87 pages04 .All About Int Rates, Zero RatesHarshit DwivediNo ratings yet

- Monte Carlo Fashions Ltd. Forecast - UPDATEDDocument26 pagesMonte Carlo Fashions Ltd. Forecast - UPDATEDsanket patilNo ratings yet

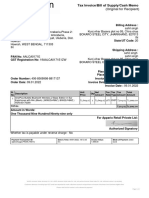

- InvoiceDocument1 pageInvoiceNikhil SinghNo ratings yet

- Malavika Nair Daniel Sutter Blockchain Cooperation PaperDocument23 pagesMalavika Nair Daniel Sutter Blockchain Cooperation PaperJ CastroNo ratings yet

- Canara - Epassbook - 2023-11-02 200708.530629Document95 pagesCanara - Epassbook - 2023-11-02 200708.530629manojsailor855No ratings yet

- Accounting HomeworkDocument3 pagesAccounting HomeworkChris Tian FlorendoNo ratings yet

- Iamp 7Document30 pagesIamp 7Tshepang MatebesiNo ratings yet

- 3rd Periodical Summative Test - FABM2Document3 pages3rd Periodical Summative Test - FABM2eddahamorlagosNo ratings yet

- Parcial L Ingles Tecnico UBPDocument6 pagesParcial L Ingles Tecnico UBPGiovannaNo ratings yet