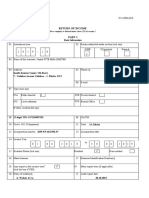

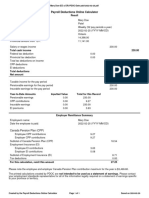

Week 5 Portfolio (kèm ảnh)

Week 5 Portfolio (kèm ảnh)

You might also like

- Kagan MillionDollarWeekend CHP 1Document15 pagesKagan MillionDollarWeekend CHP 1Gideon UsmanNo ratings yet

- Factory Acceptance TestDocument1 pageFactory Acceptance TestMuhammadPurnamaSugiri100% (3)

- Sherrod, Inc., Reported Pretax Accounting Income of $88 Million For 2018Document15 pagesSherrod, Inc., Reported Pretax Accounting Income of $88 Million For 2018laale dijaanNo ratings yet

- Case 06 Financial Detective 2016 F1763XDocument6 pagesCase 06 Financial Detective 2016 F1763XJosie KomiNo ratings yet

- BUMA 20023 - Strategic ManagementDocument104 pagesBUMA 20023 - Strategic ManagementAllyson VillalobosNo ratings yet

- Problems: Problem 12 - 2Document9 pagesProblems: Problem 12 - 2Jein PNo ratings yet

- 06 Taxation - Deferred s20 Final-1Document44 pages06 Taxation - Deferred s20 Final-150902849No ratings yet

- TEST 3 SolutionDocument3 pagesTEST 3 SolutionlusandasithembeloNo ratings yet

- ITC Report and Accounts 2023 185Document1 pageITC Report and Accounts 2023 185Nishith RanjanNo ratings yet

- 16 DT Group: Carrying Amount Tax Base Temporary DifferencesDocument2 pages16 DT Group: Carrying Amount Tax Base Temporary DifferencesJohn WickNo ratings yet

- GQ 6.2 SolDocument1 pageGQ 6.2 SolnessamuchenaNo ratings yet

- Apollo Tyres Ltd.Document3 pagesApollo Tyres Ltd.Nishant HardiyaNo ratings yet

- Test 8 SolutionDocument2 pagesTest 8 SolutionJanie HookeNo ratings yet

- Income Taxes - Crax LTD MemoDocument8 pagesIncome Taxes - Crax LTD Memoandiswa zuluNo ratings yet

- Figure in Lakh Prepared by - Ca. Shivam GuptaDocument11 pagesFigure in Lakh Prepared by - Ca. Shivam GuptaAayush LohanaNo ratings yet

- Sol. Man. - Chapter 9 Income TaxesDocument15 pagesSol. Man. - Chapter 9 Income TaxesMiguel Amihan100% (1)

- Lebanese Association of Certified Public Accountants KEY - IFRS February Exam 2020 - Extra SessionDocument6 pagesLebanese Association of Certified Public Accountants KEY - IFRS February Exam 2020 - Extra Sessionjad NasserNo ratings yet

- Spandana Sporthy Balance SheetDocument1 pageSpandana Sporthy Balance SheetMs VasNo ratings yet

- June 2021Document3 pagesJune 2021akshay kausaleNo ratings yet

- Consolidated Balance Sheet For Hindustan Unilever LTDDocument11 pagesConsolidated Balance Sheet For Hindustan Unilever LTDMohit ChughNo ratings yet

- 02 - Assignment Integration Exercise - SolutionDocument4 pages02 - Assignment Integration Exercise - SolutionAgustín RosalesNo ratings yet

- Sample FS Schedule 3 Tool For CompaniesDocument20 pagesSample FS Schedule 3 Tool For CompaniesGirish HNo ratings yet

- Ratio Analysis SumsDocument8 pagesRatio Analysis Sumshabibi 101No ratings yet

- MMFSL Fin Results Q1 F2019 LODR Clause 33 FianlDocument2 pagesMMFSL Fin Results Q1 F2019 LODR Clause 33 FianlIMAM JAVOORNo ratings yet

- Fidelity Engineering Reported Pretax Accounting IncomeDocument2 pagesFidelity Engineering Reported Pretax Accounting IncomeJalaj GuptaNo ratings yet

- Case Study 2 - Example (Handout 1)Document3 pagesCase Study 2 - Example (Handout 1)Nikoleta TrudovNo ratings yet

- T8 Tutorial SolutionsDocument4 pagesT8 Tutorial SolutionsAnathi AnathiNo ratings yet

- Projected P&L and BSDocument9 pagesProjected P&L and BSbipin kumarNo ratings yet

- Cma & DSCRDocument10 pagesCma & DSCRSaranNo ratings yet

- Statement of Profit and Loss: For The Year Ended 31st March, 2021Document2 pagesStatement of Profit and Loss: For The Year Ended 31st March, 2021Only For StudyNo ratings yet

- 9 Cash Flow Navneet EnterpriseDocument5 pages9 Cash Flow Navneet EnterpriseChanchal MisraNo ratings yet

- Return of Income: Basic InformationDocument11 pagesReturn of Income: Basic InformationShuvro PaulNo ratings yet

- 2 Case1 1bFinPlannNEWFashionSHOPS2022 23SolutionTemplateDocument8 pages2 Case1 1bFinPlannNEWFashionSHOPS2022 23SolutionTemplatesantiagoNo ratings yet

- Mock Answers Far-1 Autumn 2022Document13 pagesMock Answers Far-1 Autumn 2022rana m harisNo ratings yet

- Draft ReportDocument8 pagesDraft Report0264192238No ratings yet

- 06 Taxation - Deferred s22Document38 pages06 Taxation - Deferred s22Odzulaho DemanaNo ratings yet

- Case Study 2 - Example Solution (Handout 2)Document4 pagesCase Study 2 - Example Solution (Handout 2)Nikoleta TrudovNo ratings yet

- Compilation Pyq - Far570Document109 pagesCompilation Pyq - Far570Nur SyafiqahNo ratings yet

- Mary Doe - (EE & ER) - PDOC-Date Paid-2022-02-25Document1 pageMary Doe - (EE & ER) - PDOC-Date Paid-2022-02-25rahul_ransureNo ratings yet

- T01 - Income Tax QuestionsDocument7 pagesT01 - Income Tax QuestionsLijing CheNo ratings yet

- Examination: Subject SA3 - General Insurance Specialist ApplicationsDocument13 pagesExamination: Subject SA3 - General Insurance Specialist Applicationsdickson phiriNo ratings yet

- Act370 Tax Form SowasifDocument16 pagesAct370 Tax Form SowasifAbuboker MahadyNo ratings yet

- Standalone Result Mar23Document9 pagesStandalone Result Mar23Amit KumarNo ratings yet

- Group Activity 2 Answer KeyDocument4 pagesGroup Activity 2 Answer Keykrisha milloNo ratings yet

- Chapter 6 Deferred TaxDocument109 pagesChapter 6 Deferred Taxlindokuhlentuli75No ratings yet

- Fs Credo Ye 2017Document38 pagesFs Credo Ye 2017AzerNo ratings yet

- FM16 Ch27 Tool KitDocument5 pagesFM16 Ch27 Tool KitAdamNo ratings yet

- Pricilla AssignmentDocument3 pagesPricilla AssignmentjasonnumahnalkelNo ratings yet

- Problem 3 Accounts ReceivableDocument11 pagesProblem 3 Accounts ReceivableAngelie Bocala CatalanNo ratings yet

- CAF 5 Autumn 2023Document7 pagesCAF 5 Autumn 2023Hammad ShahidNo ratings yet

- PA - Group Assignment T1.2023Document6 pagesPA - Group Assignment T1.2023kkNo ratings yet

- Asian Paints Annual Report 2016-17Document2 pagesAsian Paints Annual Report 2016-17Amit Pandey0% (1)

- Indiabulls Housing Finance Limited (CIN: L65922DL2005PLC136029)Document9 pagesIndiabulls Housing Finance Limited (CIN: L65922DL2005PLC136029)hemant goyalNo ratings yet

- Cae05-Chapter 10 Income Tax Problem DiscussionDocument37 pagesCae05-Chapter 10 Income Tax Problem Discussioncris tellaNo ratings yet

- Final CMADocument6 pagesFinal CMAManjari AgrawalNo ratings yet

- QUESTION 6 Financial Reporting May 2021 KOLIDocument6 pagesQUESTION 6 Financial Reporting May 2021 KOLILaud ListowellNo ratings yet

- Cash Flow Explanatory SheetDocument4 pagesCash Flow Explanatory SheetTony DarwishNo ratings yet

- ASX Release: 23 August 2021Document40 pagesASX Release: 23 August 2021Peper12345No ratings yet

- SPS Chit Funds Private Limited Profit-Loss Fy2021-22Document1 pageSPS Chit Funds Private Limited Profit-Loss Fy2021-22Basker BillaNo ratings yet

- Taxation Solution 2017 SeptemberDocument11 pagesTaxation Solution 2017 Septemberzezu zazaNo ratings yet

- Example 1 - Over and Under Provision of Current TaxDocument14 pagesExample 1 - Over and Under Provision of Current TaxPui YanNo ratings yet

- Work Sheet AnalysisDocument7 pagesWork Sheet AnalysisMUHAMMAD ARIF BASHIRNo ratings yet

- Apology Letter For Late Delivery of OrderDocument1 pageApology Letter For Late Delivery of OrderSumaiyaLimi0% (1)

- Management Flashcards - QuizletDocument3 pagesManagement Flashcards - Quizletanis athirahNo ratings yet

- Business Economics Objective Type Questions Chapter - 1 Choose The Correct AnswerDocument11 pagesBusiness Economics Objective Type Questions Chapter - 1 Choose The Correct AnswerPraveen Perumal PNo ratings yet

- Power of AttorneyDocument3 pagesPower of Attorneyumair aqibNo ratings yet

- 19 - Attachment File 19 Hazard Analaysis and Risk AssesmentDocument10 pages19 - Attachment File 19 Hazard Analaysis and Risk AssesmentSana IdreesNo ratings yet

- Oblicon - BPI Vs CA, REYESDocument1 pageOblicon - BPI Vs CA, REYESChi KoyNo ratings yet

- Lesson 1 Introduction To PRDocument21 pagesLesson 1 Introduction To PRNorhayati Hj BasriNo ratings yet

- Labour Licence ChittorDocument3 pagesLabour Licence ChittorGaurav SinghNo ratings yet

- IT211 PPT Research PaperDocument10 pagesIT211 PPT Research Paperb88f5wbdbvNo ratings yet

- Digital Platforms Contribution To Improvement of Service Provision To Citizens in NampulaDocument13 pagesDigital Platforms Contribution To Improvement of Service Provision To Citizens in NampulaIJAERS JOURNALNo ratings yet

- Walmart Case StudyDocument28 pagesWalmart Case StudychandanNo ratings yet

- Notes (LA 12B) 28-02-2018 - AcceptanceDocument3 pagesNotes (LA 12B) 28-02-2018 - AcceptanceBrian PetersNo ratings yet

- Week 1 - 11Document35 pagesWeek 1 - 11asdasdNo ratings yet

- Building ComponentsDocument41 pagesBuilding ComponentsKainaz ChothiaNo ratings yet

- Origin of Clause AaaaDocument2 pagesOrigin of Clause AaaaRizky NugrohoNo ratings yet

- IEC Name of ExporterDocument20 pagesIEC Name of ExporterUday kumarNo ratings yet

- Growth Vs ScalingDocument3 pagesGrowth Vs Scalingmichelle dizonNo ratings yet

- Amazon's Alexa Spaghetti StrategyDocument10 pagesAmazon's Alexa Spaghetti StrategyShubham SinghNo ratings yet

- ANURAG R KANOJIYA PROJECT - Anurag KanojiyaDocument44 pagesANURAG R KANOJIYA PROJECT - Anurag Kanojiyadipak tighareNo ratings yet

- Competition and Efficiency in Banking. Behavioural Evidence From GhanaDocument27 pagesCompetition and Efficiency in Banking. Behavioural Evidence From GhanaKingston Nkansah Kwadwo EmmanuelNo ratings yet

- Tax - Cargill Philippines Inc Vs CIR DigestDocument2 pagesTax - Cargill Philippines Inc Vs CIR DigestDyannah Alexa Marie RamachoNo ratings yet

- Peningkatan Dan Pengembangan Produk Olahan Kopi Di Desa BrunosariDocument13 pagesPeningkatan Dan Pengembangan Produk Olahan Kopi Di Desa BrunosariRendy StarsNo ratings yet

- Customer Relationship Management - Chapter 1Document40 pagesCustomer Relationship Management - Chapter 1leni th100% (1)

- Holy Angel University: School of Business and Accountancy Holy Angel University Angeles City ACADEMIC YEAR 2021-2022Document10 pagesHoly Angel University: School of Business and Accountancy Holy Angel University Angeles City ACADEMIC YEAR 2021-2022Mae Justine Joy TajoneraNo ratings yet

- Financial DerivativesDocument23 pagesFinancial DerivativesKriti MarwahNo ratings yet

- Lt234.Tvp (Il-II) Question Cma May-2023 Exam.Document7 pagesLt234.Tvp (Il-II) Question Cma May-2023 Exam.Arif HossainNo ratings yet

- Wise Transaction Invoice Transfer 503629724 589929159 enDocument3 pagesWise Transaction Invoice Transfer 503629724 589929159 enHanna PyzhovaNo ratings yet

Download as docx, pdf, or txt

You might also like

- Kagan MillionDollarWeekend CHP 1Document15 pagesKagan MillionDollarWeekend CHP 1Gideon UsmanNo ratings yet

- Factory Acceptance TestDocument1 pageFactory Acceptance TestMuhammadPurnamaSugiri100% (3)

- Sherrod, Inc., Reported Pretax Accounting Income of $88 Million For 2018Document15 pagesSherrod, Inc., Reported Pretax Accounting Income of $88 Million For 2018laale dijaanNo ratings yet

- Case 06 Financial Detective 2016 F1763XDocument6 pagesCase 06 Financial Detective 2016 F1763XJosie KomiNo ratings yet

- BUMA 20023 - Strategic ManagementDocument104 pagesBUMA 20023 - Strategic ManagementAllyson VillalobosNo ratings yet

- Problems: Problem 12 - 2Document9 pagesProblems: Problem 12 - 2Jein PNo ratings yet

- 06 Taxation - Deferred s20 Final-1Document44 pages06 Taxation - Deferred s20 Final-150902849No ratings yet

- TEST 3 SolutionDocument3 pagesTEST 3 SolutionlusandasithembeloNo ratings yet

- ITC Report and Accounts 2023 185Document1 pageITC Report and Accounts 2023 185Nishith RanjanNo ratings yet

- 16 DT Group: Carrying Amount Tax Base Temporary DifferencesDocument2 pages16 DT Group: Carrying Amount Tax Base Temporary DifferencesJohn WickNo ratings yet

- GQ 6.2 SolDocument1 pageGQ 6.2 SolnessamuchenaNo ratings yet

- Apollo Tyres Ltd.Document3 pagesApollo Tyres Ltd.Nishant HardiyaNo ratings yet

- Test 8 SolutionDocument2 pagesTest 8 SolutionJanie HookeNo ratings yet

- Income Taxes - Crax LTD MemoDocument8 pagesIncome Taxes - Crax LTD Memoandiswa zuluNo ratings yet

- Figure in Lakh Prepared by - Ca. Shivam GuptaDocument11 pagesFigure in Lakh Prepared by - Ca. Shivam GuptaAayush LohanaNo ratings yet

- Sol. Man. - Chapter 9 Income TaxesDocument15 pagesSol. Man. - Chapter 9 Income TaxesMiguel Amihan100% (1)

- Lebanese Association of Certified Public Accountants KEY - IFRS February Exam 2020 - Extra SessionDocument6 pagesLebanese Association of Certified Public Accountants KEY - IFRS February Exam 2020 - Extra Sessionjad NasserNo ratings yet

- Spandana Sporthy Balance SheetDocument1 pageSpandana Sporthy Balance SheetMs VasNo ratings yet

- June 2021Document3 pagesJune 2021akshay kausaleNo ratings yet

- Consolidated Balance Sheet For Hindustan Unilever LTDDocument11 pagesConsolidated Balance Sheet For Hindustan Unilever LTDMohit ChughNo ratings yet

- 02 - Assignment Integration Exercise - SolutionDocument4 pages02 - Assignment Integration Exercise - SolutionAgustín RosalesNo ratings yet

- Sample FS Schedule 3 Tool For CompaniesDocument20 pagesSample FS Schedule 3 Tool For CompaniesGirish HNo ratings yet

- Ratio Analysis SumsDocument8 pagesRatio Analysis Sumshabibi 101No ratings yet

- MMFSL Fin Results Q1 F2019 LODR Clause 33 FianlDocument2 pagesMMFSL Fin Results Q1 F2019 LODR Clause 33 FianlIMAM JAVOORNo ratings yet

- Fidelity Engineering Reported Pretax Accounting IncomeDocument2 pagesFidelity Engineering Reported Pretax Accounting IncomeJalaj GuptaNo ratings yet

- Case Study 2 - Example (Handout 1)Document3 pagesCase Study 2 - Example (Handout 1)Nikoleta TrudovNo ratings yet

- T8 Tutorial SolutionsDocument4 pagesT8 Tutorial SolutionsAnathi AnathiNo ratings yet

- Projected P&L and BSDocument9 pagesProjected P&L and BSbipin kumarNo ratings yet

- Cma & DSCRDocument10 pagesCma & DSCRSaranNo ratings yet

- Statement of Profit and Loss: For The Year Ended 31st March, 2021Document2 pagesStatement of Profit and Loss: For The Year Ended 31st March, 2021Only For StudyNo ratings yet

- 9 Cash Flow Navneet EnterpriseDocument5 pages9 Cash Flow Navneet EnterpriseChanchal MisraNo ratings yet

- Return of Income: Basic InformationDocument11 pagesReturn of Income: Basic InformationShuvro PaulNo ratings yet

- 2 Case1 1bFinPlannNEWFashionSHOPS2022 23SolutionTemplateDocument8 pages2 Case1 1bFinPlannNEWFashionSHOPS2022 23SolutionTemplatesantiagoNo ratings yet

- Mock Answers Far-1 Autumn 2022Document13 pagesMock Answers Far-1 Autumn 2022rana m harisNo ratings yet

- Draft ReportDocument8 pagesDraft Report0264192238No ratings yet

- 06 Taxation - Deferred s22Document38 pages06 Taxation - Deferred s22Odzulaho DemanaNo ratings yet

- Case Study 2 - Example Solution (Handout 2)Document4 pagesCase Study 2 - Example Solution (Handout 2)Nikoleta TrudovNo ratings yet

- Compilation Pyq - Far570Document109 pagesCompilation Pyq - Far570Nur SyafiqahNo ratings yet

- Mary Doe - (EE & ER) - PDOC-Date Paid-2022-02-25Document1 pageMary Doe - (EE & ER) - PDOC-Date Paid-2022-02-25rahul_ransureNo ratings yet

- T01 - Income Tax QuestionsDocument7 pagesT01 - Income Tax QuestionsLijing CheNo ratings yet

- Examination: Subject SA3 - General Insurance Specialist ApplicationsDocument13 pagesExamination: Subject SA3 - General Insurance Specialist Applicationsdickson phiriNo ratings yet

- Act370 Tax Form SowasifDocument16 pagesAct370 Tax Form SowasifAbuboker MahadyNo ratings yet

- Standalone Result Mar23Document9 pagesStandalone Result Mar23Amit KumarNo ratings yet

- Group Activity 2 Answer KeyDocument4 pagesGroup Activity 2 Answer Keykrisha milloNo ratings yet

- Chapter 6 Deferred TaxDocument109 pagesChapter 6 Deferred Taxlindokuhlentuli75No ratings yet

- Fs Credo Ye 2017Document38 pagesFs Credo Ye 2017AzerNo ratings yet

- FM16 Ch27 Tool KitDocument5 pagesFM16 Ch27 Tool KitAdamNo ratings yet

- Pricilla AssignmentDocument3 pagesPricilla AssignmentjasonnumahnalkelNo ratings yet

- Problem 3 Accounts ReceivableDocument11 pagesProblem 3 Accounts ReceivableAngelie Bocala CatalanNo ratings yet

- CAF 5 Autumn 2023Document7 pagesCAF 5 Autumn 2023Hammad ShahidNo ratings yet

- PA - Group Assignment T1.2023Document6 pagesPA - Group Assignment T1.2023kkNo ratings yet

- Asian Paints Annual Report 2016-17Document2 pagesAsian Paints Annual Report 2016-17Amit Pandey0% (1)

- Indiabulls Housing Finance Limited (CIN: L65922DL2005PLC136029)Document9 pagesIndiabulls Housing Finance Limited (CIN: L65922DL2005PLC136029)hemant goyalNo ratings yet

- Cae05-Chapter 10 Income Tax Problem DiscussionDocument37 pagesCae05-Chapter 10 Income Tax Problem Discussioncris tellaNo ratings yet

- Final CMADocument6 pagesFinal CMAManjari AgrawalNo ratings yet

- QUESTION 6 Financial Reporting May 2021 KOLIDocument6 pagesQUESTION 6 Financial Reporting May 2021 KOLILaud ListowellNo ratings yet

- Cash Flow Explanatory SheetDocument4 pagesCash Flow Explanatory SheetTony DarwishNo ratings yet

- ASX Release: 23 August 2021Document40 pagesASX Release: 23 August 2021Peper12345No ratings yet

- SPS Chit Funds Private Limited Profit-Loss Fy2021-22Document1 pageSPS Chit Funds Private Limited Profit-Loss Fy2021-22Basker BillaNo ratings yet

- Taxation Solution 2017 SeptemberDocument11 pagesTaxation Solution 2017 Septemberzezu zazaNo ratings yet

- Example 1 - Over and Under Provision of Current TaxDocument14 pagesExample 1 - Over and Under Provision of Current TaxPui YanNo ratings yet

- Work Sheet AnalysisDocument7 pagesWork Sheet AnalysisMUHAMMAD ARIF BASHIRNo ratings yet

- Apology Letter For Late Delivery of OrderDocument1 pageApology Letter For Late Delivery of OrderSumaiyaLimi0% (1)

- Management Flashcards - QuizletDocument3 pagesManagement Flashcards - Quizletanis athirahNo ratings yet

- Business Economics Objective Type Questions Chapter - 1 Choose The Correct AnswerDocument11 pagesBusiness Economics Objective Type Questions Chapter - 1 Choose The Correct AnswerPraveen Perumal PNo ratings yet

- Power of AttorneyDocument3 pagesPower of Attorneyumair aqibNo ratings yet

- 19 - Attachment File 19 Hazard Analaysis and Risk AssesmentDocument10 pages19 - Attachment File 19 Hazard Analaysis and Risk AssesmentSana IdreesNo ratings yet

- Oblicon - BPI Vs CA, REYESDocument1 pageOblicon - BPI Vs CA, REYESChi KoyNo ratings yet

- Lesson 1 Introduction To PRDocument21 pagesLesson 1 Introduction To PRNorhayati Hj BasriNo ratings yet

- Labour Licence ChittorDocument3 pagesLabour Licence ChittorGaurav SinghNo ratings yet

- IT211 PPT Research PaperDocument10 pagesIT211 PPT Research Paperb88f5wbdbvNo ratings yet

- Digital Platforms Contribution To Improvement of Service Provision To Citizens in NampulaDocument13 pagesDigital Platforms Contribution To Improvement of Service Provision To Citizens in NampulaIJAERS JOURNALNo ratings yet

- Walmart Case StudyDocument28 pagesWalmart Case StudychandanNo ratings yet

- Notes (LA 12B) 28-02-2018 - AcceptanceDocument3 pagesNotes (LA 12B) 28-02-2018 - AcceptanceBrian PetersNo ratings yet

- Week 1 - 11Document35 pagesWeek 1 - 11asdasdNo ratings yet

- Building ComponentsDocument41 pagesBuilding ComponentsKainaz ChothiaNo ratings yet

- Origin of Clause AaaaDocument2 pagesOrigin of Clause AaaaRizky NugrohoNo ratings yet

- IEC Name of ExporterDocument20 pagesIEC Name of ExporterUday kumarNo ratings yet

- Growth Vs ScalingDocument3 pagesGrowth Vs Scalingmichelle dizonNo ratings yet

- Amazon's Alexa Spaghetti StrategyDocument10 pagesAmazon's Alexa Spaghetti StrategyShubham SinghNo ratings yet

- ANURAG R KANOJIYA PROJECT - Anurag KanojiyaDocument44 pagesANURAG R KANOJIYA PROJECT - Anurag Kanojiyadipak tighareNo ratings yet

- Competition and Efficiency in Banking. Behavioural Evidence From GhanaDocument27 pagesCompetition and Efficiency in Banking. Behavioural Evidence From GhanaKingston Nkansah Kwadwo EmmanuelNo ratings yet

- Tax - Cargill Philippines Inc Vs CIR DigestDocument2 pagesTax - Cargill Philippines Inc Vs CIR DigestDyannah Alexa Marie RamachoNo ratings yet

- Peningkatan Dan Pengembangan Produk Olahan Kopi Di Desa BrunosariDocument13 pagesPeningkatan Dan Pengembangan Produk Olahan Kopi Di Desa BrunosariRendy StarsNo ratings yet

- Customer Relationship Management - Chapter 1Document40 pagesCustomer Relationship Management - Chapter 1leni th100% (1)

- Holy Angel University: School of Business and Accountancy Holy Angel University Angeles City ACADEMIC YEAR 2021-2022Document10 pagesHoly Angel University: School of Business and Accountancy Holy Angel University Angeles City ACADEMIC YEAR 2021-2022Mae Justine Joy TajoneraNo ratings yet

- Financial DerivativesDocument23 pagesFinancial DerivativesKriti MarwahNo ratings yet

- Lt234.Tvp (Il-II) Question Cma May-2023 Exam.Document7 pagesLt234.Tvp (Il-II) Question Cma May-2023 Exam.Arif HossainNo ratings yet

- Wise Transaction Invoice Transfer 503629724 589929159 enDocument3 pagesWise Transaction Invoice Transfer 503629724 589929159 enHanna PyzhovaNo ratings yet