ITC January 2024 Paper 3 Question FutureAfrica

ITC January 2024 Paper 3 Question FutureAfrica

You might also like

- Investment PropertyDocument7 pagesInvestment PropertyKate Fernandez50% (4)

- Car Lease Policy MyntraDocument11 pagesCar Lease Policy MyntraertytrythytyNo ratings yet

- CGL - PbasDocument2 pagesCGL - PbasRobbyNo ratings yet

- FAR 1 3rd Mock - ComprehensiveDocument4 pagesFAR 1 3rd Mock - Comprehensiveahsanalipalipoto17No ratings yet

- China Evergrande DISCLOSEABLE TRANSACTION DISPOSAL OF INTERESTS IN PROJECT COMPANYDocument7 pagesChina Evergrande DISCLOSEABLE TRANSACTION DISPOSAL OF INTERESTS IN PROJECT COMPANYchukingfungNo ratings yet

- 10 IFRS 16 Question BankDocument38 pages10 IFRS 16 Question BankthamsanqamanciNo ratings yet

- CFAP 6 AARS Summer 2023Document4 pagesCFAP 6 AARS Summer 2023hassanlatif803No ratings yet

- BCOM - Accounting 3Document6 pagesBCOM - Accounting 3Ntokozo Siphiwo Collin DlaminiNo ratings yet

- FAR2 Assignment EID MUBARAKDocument6 pagesFAR2 Assignment EID MUBARAKAli nawazNo ratings yet

- Review Material - ACCE 411Document5 pagesReview Material - ACCE 411zee abadillaNo ratings yet

- Acro Misr Mohamed GamalDocument35 pagesAcro Misr Mohamed Gamalmoh.gamalaaibNo ratings yet

- IP and PPEDocument3 pagesIP and PPEElaine Joyce GarciaNo ratings yet

- 1 Corporate ReportingDocument6 pages1 Corporate Reportingswarna dasNo ratings yet

- Bacc 233 Assignment 1 Jan-June 2023Document3 pagesBacc 233 Assignment 1 Jan-June 2023emmanuel.mazivireNo ratings yet

- Fitch Egypt Infrastructure Report - 2022-09-27Document53 pagesFitch Egypt Infrastructure Report - 2022-09-27Ziad SaeedNo ratings yet

- Caf-01 Far-I (Mah SS)Document4 pagesCaf-01 Far-I (Mah SS)Abdullah SaberNo ratings yet

- Transfer Pricing Class Practice QuestionDocument4 pagesTransfer Pricing Class Practice QuestionTadiwanashe MaringireNo ratings yet

- FAR 1 Mock 4 - FinalDocument4 pagesFAR 1 Mock 4 - Finalahsanalipalipoto17No ratings yet

- Quiz 1 Far510 MFRS120 123 PDFDocument4 pagesQuiz 1 Far510 MFRS120 123 PDFiirene.ntshNo ratings yet

- AFARicpaDocument23 pagesAFARicpaRegine YbañezNo ratings yet

- Final Exam W MCQDocument12 pagesFinal Exam W MCQPatrick SalvadorNo ratings yet

- Corporate Reporting Paper 3.1 July 2023Document32 pagesCorporate Reporting Paper 3.1 July 2023Prof. OBESENo ratings yet

- True or False: - Write True If The Statement Is Correct. Otherwise, Write FalseDocument3 pagesTrue or False: - Write True If The Statement Is Correct. Otherwise, Write FalseElaine Joyce GarciaNo ratings yet

- Lease Accounting Lecture in Power PointDocument22 pagesLease Accounting Lecture in Power PointEjaz AhmadNo ratings yet

- FAC3764 - Assessment 01Document2 pagesFAC3764 - Assessment 01mandisanomzamo72No ratings yet

- Institute of Business Administration: Diploma in Taxation-Batch 4 Provincial Sales Tax On Services AssignmentDocument3 pagesInstitute of Business Administration: Diploma in Taxation-Batch 4 Provincial Sales Tax On Services AssignmentALI HUSSAINNo ratings yet

- Aafr Ifrs 15 Icap Past Papers With SolutionDocument10 pagesAafr Ifrs 15 Icap Past Papers With SolutionAqib Sheikh0% (1)

- ACC2143ACC2543 Test 1 2023Document9 pagesACC2143ACC2543 Test 1 2023kamichidorahNo ratings yet

- ACCT 302 TS - Fin InstDocument4 pagesACCT 302 TS - Fin InstbismarkkwadzokpoNo ratings yet

- Prac 1 Final PreboardDocument10 pagesPrac 1 Final Preboardbobo kaNo ratings yet

- Audit Mid Spring 24 (V-2)Document3 pagesAudit Mid Spring 24 (V-2)Nouman ShamasNo ratings yet

- Comprehensive Financial Reporting QuestionDocument18 pagesComprehensive Financial Reporting QuestionBrain MangoroNo ratings yet

- Assessment 3 RemovedDocument6 pagesAssessment 3 RemovedTariro ManyikaNo ratings yet

- Topic 4 - Borrowing Cost - MFRS 123Document21 pagesTopic 4 - Borrowing Cost - MFRS 1232023105069No ratings yet

- A Project Report On Technical Analysis of Automobile Sector at Geojit PNB ParibasDocument62 pagesA Project Report On Technical Analysis of Automobile Sector at Geojit PNB ParibasBabasab Patil (Karrisatte)No ratings yet

- Borrowing CostsDocument4 pagesBorrowing CostsAila Mae SuarezNo ratings yet

- Final Mock by TSB CFAP6 S2020Document5 pagesFinal Mock by TSB CFAP6 S2020Umar FarooqNo ratings yet

- Test 4 Revision Class Question - 2023Document3 pagesTest 4 Revision Class Question - 2023Given RefilweNo ratings yet

- Assignment 1Document2 pagesAssignment 1chrislupinjrNo ratings yet

- VR CF Proj Group 5Document9 pagesVR CF Proj Group 5sandeep singhNo ratings yet

- Ac413 Supp Feb20Document5 pagesAc413 Supp Feb20AnishahNo ratings yet

- Naqdown Final Round 2013Document8 pagesNaqdown Final Round 2013MJ YaconNo ratings yet

- CA Final Paper 2Document32 pagesCA Final Paper 2MM_AKSINo ratings yet

- Godo - 22!12!14 TOR For Business ConsultingDocument16 pagesGodo - 22!12!14 TOR For Business ConsultingRisaa TubeNo ratings yet

- Group 1 - 7 (110722)Document8 pagesGroup 1 - 7 (110722)JACOB MAZHANGANo ratings yet

- Fa May June - 2019Document5 pagesFa May June - 2019xodic49847No ratings yet

- Bravado June 2009Document3 pagesBravado June 2009Tian YinNo ratings yet

- Foreign Direct Investments: by Prof. Augustin AmaladasDocument33 pagesForeign Direct Investments: by Prof. Augustin AmaladasPooja MehraNo ratings yet

- Msa 1Document132 pagesMsa 1ehteshamanwar444No ratings yet

- Sino CasoniDocument35 pagesSino CasoniYetnayet ZerfuNo ratings yet

- 7 Af 301 FaDocument4 pages7 Af 301 FaAleenaSheikhNo ratings yet

- Bacc 236 Ass 2 Semester 1 of 2024 (MU TIPLE CHOICE)Document8 pagesBacc 236 Ass 2 Semester 1 of 2024 (MU TIPLE CHOICE)TarusengaNo ratings yet

- Accounting StandardDocument33 pagesAccounting StandardPooja BaghelNo ratings yet

- IntAcc 2 For Prac. SolvingDocument2 pagesIntAcc 2 For Prac. Solvingrachel banana hammockNo ratings yet

- ACCT 302 Tutorial Set 7 and AnswersDocument10 pagesACCT 302 Tutorial Set 7 and AnswersPrince AgyeiNo ratings yet

- FR RTP May 22Document32 pagesFR RTP May 22Utkarsh SharmaNo ratings yet

- RTO Programme Pitchbook 20191213Document7 pagesRTO Programme Pitchbook 20191213Kung FooNo ratings yet

- 2021 Revision QuestionsDocument10 pages2021 Revision QuestionsTawanda Tatenda HerbertNo ratings yet

- Financial Reporting and Auditing in Sovereign Operations: Technical Guidance NoteFrom EverandFinancial Reporting and Auditing in Sovereign Operations: Technical Guidance NoteNo ratings yet

- Utkarsh 2023 For PromotionDocument167 pagesUtkarsh 2023 For PromotionAmit GagraniNo ratings yet

- Vasilia 1Document25 pagesVasilia 1Feline FrevrNo ratings yet

- Facility AgreementDocument52 pagesFacility AgreementIlyes JerbiNo ratings yet

- NEW Defintion of Withholding Tax Keys (PER-53-2009) Old Definition of Withholding Tax KeysDocument2 pagesNEW Defintion of Withholding Tax Keys (PER-53-2009) Old Definition of Withholding Tax KeysKauam SantosNo ratings yet

- Barrons 06 09 2021Document80 pagesBarrons 06 09 2021glauber silvaNo ratings yet

- Mortgage Refi Script 101Document4 pagesMortgage Refi Script 101bluewhaleoutsourcingNo ratings yet

- Cancellation FormDocument2 pagesCancellation FormAnuradha AmjuriNo ratings yet

- CA Final SFM Chalisa Book by CA Aaditya Jain For Nov 2021 ExamDocument48 pagesCA Final SFM Chalisa Book by CA Aaditya Jain For Nov 2021 ExamKapil MeenaNo ratings yet

- Single AmountDocument26 pagesSingle AmountYejiNo ratings yet

- Topic 3 - Internal Control System - Part 2-StudentDocument9 pagesTopic 3 - Internal Control System - Part 2-StudentThinh NguyenNo ratings yet

- Financial Accounting and Reporting - QUIZ 7Document4 pagesFinancial Accounting and Reporting - QUIZ 7JINGLE FULGENCIONo ratings yet

- Project Finance Performance of SBIDocument39 pagesProject Finance Performance of SBIManmohan SahuNo ratings yet

- Marine Insurance: Free of Capture and SeizureDocument2 pagesMarine Insurance: Free of Capture and SeizurevinxoxNo ratings yet

- Final AccountsDocument9 pagesFinal AccountsRositaNo ratings yet

- Banks and Banking 1: What Kind of Services Do Banks Offer?Document4 pagesBanks and Banking 1: What Kind of Services Do Banks Offer?Karima MammeriNo ratings yet

- Principles of Accounting (ACC-1101)Document4 pagesPrinciples of Accounting (ACC-1101)hojegaNo ratings yet

- Table B7: Bank-Wise and Bank Group-Wise Gross Non-Performing Assets, Gross Advances, and Gross NPA Ratio of Scheduled Commercial Banks - 2012Document5 pagesTable B7: Bank-Wise and Bank Group-Wise Gross Non-Performing Assets, Gross Advances, and Gross NPA Ratio of Scheduled Commercial Banks - 2012shipra1305No ratings yet

- 2nd Year Reviewer Midterms (Compatibility)Document11 pages2nd Year Reviewer Midterms (Compatibility)Louie De La Torre0% (1)

- FA3 - Article - Phillips Et Al. (2003) - Earnings Management New Evidence Based On Deferred Tax ExpenseDocument32 pagesFA3 - Article - Phillips Et Al. (2003) - Earnings Management New Evidence Based On Deferred Tax Expense吕沁珂No ratings yet

- Liabilities: Chart of Accounts AssetsDocument39 pagesLiabilities: Chart of Accounts AssetsDiana Rose OrlinaNo ratings yet

- ACC 102 Chapter 16 Review QuestionsDocument3 pagesACC 102 Chapter 16 Review QuestionsKaitlyn MakiNo ratings yet

- BankmedDocument6 pagesBankmedJoele shNo ratings yet

- AtmDocument127 pagesAtmPuja Ghosh100% (3)

- Keys VaultsDocument37 pagesKeys VaultsAsfar Khan100% (1)

- Xii Mcqs CH - 15 Ratio AnalysisDocument6 pagesXii Mcqs CH - 15 Ratio AnalysisJoanna GarciaNo ratings yet

- Short Questions-Central BankDocument6 pagesShort Questions-Central BanksadNo ratings yet

- Maybank Islamic Mastercard Ikhwan Card-I Agreement: Humanising Financial ServicesDocument25 pagesMaybank Islamic Mastercard Ikhwan Card-I Agreement: Humanising Financial ServicesEjang GutNo ratings yet

- Insurance Code Reviewer 2014Document31 pagesInsurance Code Reviewer 2014Samantha ReyesNo ratings yet

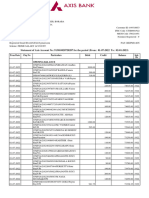

- Statement of Axis Account No:913010028728287 For The Period (From: 01-07-2022 To: 02-01-2023)Document41 pagesStatement of Axis Account No:913010028728287 For The Period (From: 01-07-2022 To: 02-01-2023)Shreshtha Suffix Financial ServicesNo ratings yet

Download as pdf or txt

You might also like

- Investment PropertyDocument7 pagesInvestment PropertyKate Fernandez50% (4)

- Car Lease Policy MyntraDocument11 pagesCar Lease Policy MyntraertytrythytyNo ratings yet

- CGL - PbasDocument2 pagesCGL - PbasRobbyNo ratings yet

- FAR 1 3rd Mock - ComprehensiveDocument4 pagesFAR 1 3rd Mock - Comprehensiveahsanalipalipoto17No ratings yet

- China Evergrande DISCLOSEABLE TRANSACTION DISPOSAL OF INTERESTS IN PROJECT COMPANYDocument7 pagesChina Evergrande DISCLOSEABLE TRANSACTION DISPOSAL OF INTERESTS IN PROJECT COMPANYchukingfungNo ratings yet

- 10 IFRS 16 Question BankDocument38 pages10 IFRS 16 Question BankthamsanqamanciNo ratings yet

- CFAP 6 AARS Summer 2023Document4 pagesCFAP 6 AARS Summer 2023hassanlatif803No ratings yet

- BCOM - Accounting 3Document6 pagesBCOM - Accounting 3Ntokozo Siphiwo Collin DlaminiNo ratings yet

- FAR2 Assignment EID MUBARAKDocument6 pagesFAR2 Assignment EID MUBARAKAli nawazNo ratings yet

- Review Material - ACCE 411Document5 pagesReview Material - ACCE 411zee abadillaNo ratings yet

- Acro Misr Mohamed GamalDocument35 pagesAcro Misr Mohamed Gamalmoh.gamalaaibNo ratings yet

- IP and PPEDocument3 pagesIP and PPEElaine Joyce GarciaNo ratings yet

- 1 Corporate ReportingDocument6 pages1 Corporate Reportingswarna dasNo ratings yet

- Bacc 233 Assignment 1 Jan-June 2023Document3 pagesBacc 233 Assignment 1 Jan-June 2023emmanuel.mazivireNo ratings yet

- Fitch Egypt Infrastructure Report - 2022-09-27Document53 pagesFitch Egypt Infrastructure Report - 2022-09-27Ziad SaeedNo ratings yet

- Caf-01 Far-I (Mah SS)Document4 pagesCaf-01 Far-I (Mah SS)Abdullah SaberNo ratings yet

- Transfer Pricing Class Practice QuestionDocument4 pagesTransfer Pricing Class Practice QuestionTadiwanashe MaringireNo ratings yet

- FAR 1 Mock 4 - FinalDocument4 pagesFAR 1 Mock 4 - Finalahsanalipalipoto17No ratings yet

- Quiz 1 Far510 MFRS120 123 PDFDocument4 pagesQuiz 1 Far510 MFRS120 123 PDFiirene.ntshNo ratings yet

- AFARicpaDocument23 pagesAFARicpaRegine YbañezNo ratings yet

- Final Exam W MCQDocument12 pagesFinal Exam W MCQPatrick SalvadorNo ratings yet

- Corporate Reporting Paper 3.1 July 2023Document32 pagesCorporate Reporting Paper 3.1 July 2023Prof. OBESENo ratings yet

- True or False: - Write True If The Statement Is Correct. Otherwise, Write FalseDocument3 pagesTrue or False: - Write True If The Statement Is Correct. Otherwise, Write FalseElaine Joyce GarciaNo ratings yet

- Lease Accounting Lecture in Power PointDocument22 pagesLease Accounting Lecture in Power PointEjaz AhmadNo ratings yet

- FAC3764 - Assessment 01Document2 pagesFAC3764 - Assessment 01mandisanomzamo72No ratings yet

- Institute of Business Administration: Diploma in Taxation-Batch 4 Provincial Sales Tax On Services AssignmentDocument3 pagesInstitute of Business Administration: Diploma in Taxation-Batch 4 Provincial Sales Tax On Services AssignmentALI HUSSAINNo ratings yet

- Aafr Ifrs 15 Icap Past Papers With SolutionDocument10 pagesAafr Ifrs 15 Icap Past Papers With SolutionAqib Sheikh0% (1)

- ACC2143ACC2543 Test 1 2023Document9 pagesACC2143ACC2543 Test 1 2023kamichidorahNo ratings yet

- ACCT 302 TS - Fin InstDocument4 pagesACCT 302 TS - Fin InstbismarkkwadzokpoNo ratings yet

- Prac 1 Final PreboardDocument10 pagesPrac 1 Final Preboardbobo kaNo ratings yet

- Audit Mid Spring 24 (V-2)Document3 pagesAudit Mid Spring 24 (V-2)Nouman ShamasNo ratings yet

- Comprehensive Financial Reporting QuestionDocument18 pagesComprehensive Financial Reporting QuestionBrain MangoroNo ratings yet

- Assessment 3 RemovedDocument6 pagesAssessment 3 RemovedTariro ManyikaNo ratings yet

- Topic 4 - Borrowing Cost - MFRS 123Document21 pagesTopic 4 - Borrowing Cost - MFRS 1232023105069No ratings yet

- A Project Report On Technical Analysis of Automobile Sector at Geojit PNB ParibasDocument62 pagesA Project Report On Technical Analysis of Automobile Sector at Geojit PNB ParibasBabasab Patil (Karrisatte)No ratings yet

- Borrowing CostsDocument4 pagesBorrowing CostsAila Mae SuarezNo ratings yet

- Final Mock by TSB CFAP6 S2020Document5 pagesFinal Mock by TSB CFAP6 S2020Umar FarooqNo ratings yet

- Test 4 Revision Class Question - 2023Document3 pagesTest 4 Revision Class Question - 2023Given RefilweNo ratings yet

- Assignment 1Document2 pagesAssignment 1chrislupinjrNo ratings yet

- VR CF Proj Group 5Document9 pagesVR CF Proj Group 5sandeep singhNo ratings yet

- Ac413 Supp Feb20Document5 pagesAc413 Supp Feb20AnishahNo ratings yet

- Naqdown Final Round 2013Document8 pagesNaqdown Final Round 2013MJ YaconNo ratings yet

- CA Final Paper 2Document32 pagesCA Final Paper 2MM_AKSINo ratings yet

- Godo - 22!12!14 TOR For Business ConsultingDocument16 pagesGodo - 22!12!14 TOR For Business ConsultingRisaa TubeNo ratings yet

- Group 1 - 7 (110722)Document8 pagesGroup 1 - 7 (110722)JACOB MAZHANGANo ratings yet

- Fa May June - 2019Document5 pagesFa May June - 2019xodic49847No ratings yet

- Bravado June 2009Document3 pagesBravado June 2009Tian YinNo ratings yet

- Foreign Direct Investments: by Prof. Augustin AmaladasDocument33 pagesForeign Direct Investments: by Prof. Augustin AmaladasPooja MehraNo ratings yet

- Msa 1Document132 pagesMsa 1ehteshamanwar444No ratings yet

- Sino CasoniDocument35 pagesSino CasoniYetnayet ZerfuNo ratings yet

- 7 Af 301 FaDocument4 pages7 Af 301 FaAleenaSheikhNo ratings yet

- Bacc 236 Ass 2 Semester 1 of 2024 (MU TIPLE CHOICE)Document8 pagesBacc 236 Ass 2 Semester 1 of 2024 (MU TIPLE CHOICE)TarusengaNo ratings yet

- Accounting StandardDocument33 pagesAccounting StandardPooja BaghelNo ratings yet

- IntAcc 2 For Prac. SolvingDocument2 pagesIntAcc 2 For Prac. Solvingrachel banana hammockNo ratings yet

- ACCT 302 Tutorial Set 7 and AnswersDocument10 pagesACCT 302 Tutorial Set 7 and AnswersPrince AgyeiNo ratings yet

- FR RTP May 22Document32 pagesFR RTP May 22Utkarsh SharmaNo ratings yet

- RTO Programme Pitchbook 20191213Document7 pagesRTO Programme Pitchbook 20191213Kung FooNo ratings yet

- 2021 Revision QuestionsDocument10 pages2021 Revision QuestionsTawanda Tatenda HerbertNo ratings yet

- Financial Reporting and Auditing in Sovereign Operations: Technical Guidance NoteFrom EverandFinancial Reporting and Auditing in Sovereign Operations: Technical Guidance NoteNo ratings yet

- Utkarsh 2023 For PromotionDocument167 pagesUtkarsh 2023 For PromotionAmit GagraniNo ratings yet

- Vasilia 1Document25 pagesVasilia 1Feline FrevrNo ratings yet

- Facility AgreementDocument52 pagesFacility AgreementIlyes JerbiNo ratings yet

- NEW Defintion of Withholding Tax Keys (PER-53-2009) Old Definition of Withholding Tax KeysDocument2 pagesNEW Defintion of Withholding Tax Keys (PER-53-2009) Old Definition of Withholding Tax KeysKauam SantosNo ratings yet

- Barrons 06 09 2021Document80 pagesBarrons 06 09 2021glauber silvaNo ratings yet

- Mortgage Refi Script 101Document4 pagesMortgage Refi Script 101bluewhaleoutsourcingNo ratings yet

- Cancellation FormDocument2 pagesCancellation FormAnuradha AmjuriNo ratings yet

- CA Final SFM Chalisa Book by CA Aaditya Jain For Nov 2021 ExamDocument48 pagesCA Final SFM Chalisa Book by CA Aaditya Jain For Nov 2021 ExamKapil MeenaNo ratings yet

- Single AmountDocument26 pagesSingle AmountYejiNo ratings yet

- Topic 3 - Internal Control System - Part 2-StudentDocument9 pagesTopic 3 - Internal Control System - Part 2-StudentThinh NguyenNo ratings yet

- Financial Accounting and Reporting - QUIZ 7Document4 pagesFinancial Accounting and Reporting - QUIZ 7JINGLE FULGENCIONo ratings yet

- Project Finance Performance of SBIDocument39 pagesProject Finance Performance of SBIManmohan SahuNo ratings yet

- Marine Insurance: Free of Capture and SeizureDocument2 pagesMarine Insurance: Free of Capture and SeizurevinxoxNo ratings yet

- Final AccountsDocument9 pagesFinal AccountsRositaNo ratings yet

- Banks and Banking 1: What Kind of Services Do Banks Offer?Document4 pagesBanks and Banking 1: What Kind of Services Do Banks Offer?Karima MammeriNo ratings yet

- Principles of Accounting (ACC-1101)Document4 pagesPrinciples of Accounting (ACC-1101)hojegaNo ratings yet

- Table B7: Bank-Wise and Bank Group-Wise Gross Non-Performing Assets, Gross Advances, and Gross NPA Ratio of Scheduled Commercial Banks - 2012Document5 pagesTable B7: Bank-Wise and Bank Group-Wise Gross Non-Performing Assets, Gross Advances, and Gross NPA Ratio of Scheduled Commercial Banks - 2012shipra1305No ratings yet

- 2nd Year Reviewer Midterms (Compatibility)Document11 pages2nd Year Reviewer Midterms (Compatibility)Louie De La Torre0% (1)

- FA3 - Article - Phillips Et Al. (2003) - Earnings Management New Evidence Based On Deferred Tax ExpenseDocument32 pagesFA3 - Article - Phillips Et Al. (2003) - Earnings Management New Evidence Based On Deferred Tax Expense吕沁珂No ratings yet

- Liabilities: Chart of Accounts AssetsDocument39 pagesLiabilities: Chart of Accounts AssetsDiana Rose OrlinaNo ratings yet

- ACC 102 Chapter 16 Review QuestionsDocument3 pagesACC 102 Chapter 16 Review QuestionsKaitlyn MakiNo ratings yet

- BankmedDocument6 pagesBankmedJoele shNo ratings yet

- AtmDocument127 pagesAtmPuja Ghosh100% (3)

- Keys VaultsDocument37 pagesKeys VaultsAsfar Khan100% (1)

- Xii Mcqs CH - 15 Ratio AnalysisDocument6 pagesXii Mcqs CH - 15 Ratio AnalysisJoanna GarciaNo ratings yet

- Short Questions-Central BankDocument6 pagesShort Questions-Central BanksadNo ratings yet

- Maybank Islamic Mastercard Ikhwan Card-I Agreement: Humanising Financial ServicesDocument25 pagesMaybank Islamic Mastercard Ikhwan Card-I Agreement: Humanising Financial ServicesEjang GutNo ratings yet

- Insurance Code Reviewer 2014Document31 pagesInsurance Code Reviewer 2014Samantha ReyesNo ratings yet

- Statement of Axis Account No:913010028728287 For The Period (From: 01-07-2022 To: 02-01-2023)Document41 pagesStatement of Axis Account No:913010028728287 For The Period (From: 01-07-2022 To: 02-01-2023)Shreshtha Suffix Financial ServicesNo ratings yet