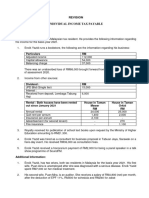

Tutorial 6 Non Business Income Question (202404)

Tutorial 6 Non Business Income Question (202404)

You might also like

- Final Test Fin533 January 2024Document13 pagesFinal Test Fin533 January 20242023607226No ratings yet

- Adjusting Entries Exercises - EditedDocument4 pagesAdjusting Entries Exercises - EditedCINDY LIAN CABILLON100% (2)

- Lessor Discussion U PDFDocument4 pagesLessor Discussion U PDFadmiral spongebobNo ratings yet

- Lease Modules ContinuedDocument8 pagesLease Modules ContinuedKenneth Marcial Ege0% (1)

- Intro To Consulting SlidesDocument34 pagesIntro To Consulting Slidesmanojben100% (2)

- Week 7Document3 pagesWeek 7xinghe666No ratings yet

- Distribute A231 - BKAT3033 - Tutorial 123 - QDocument7 pagesDistribute A231 - BKAT3033 - Tutorial 123 - QallyaNo ratings yet

- Lecture6 - RPGT Class Exercise QDocument4 pagesLecture6 - RPGT Class Exercise QpremsuwaatiiNo ratings yet

- T4 Other Income Q 1-2020-2021Document2 pagesT4 Other Income Q 1-2020-2021Putri Nurin Hasnida HassanNo ratings yet

- Week 8Document3 pagesWeek 8xinghe666No ratings yet

- Prop Tax A RPGT Illustrations (Tracked)Document39 pagesProp Tax A RPGT Illustrations (Tracked)celina kohNo ratings yet

- Abft1024 T8 - LtyDocument2 pagesAbft1024 T8 - Ltylfc778No ratings yet

- Tutorial 9 Year End Adjustments (Q)Document4 pagesTutorial 9 Year End Adjustments (Q)lious lii0% (1)

- Examples & Practice Questions For Income From PropertyDocument8 pagesExamples & Practice Questions For Income From PropertyAbdulAzeemNo ratings yet

- Tutorial 3 - RPGT-2022Document4 pagesTutorial 3 - RPGT-2022Keat 98No ratings yet

- Tutorial 4 QDocument6 pagesTutorial 4 Q謝中豪No ratings yet

- Tutorial Q - Partnership - Feb2024Document2 pagesTutorial Q - Partnership - Feb2024farhanahiszati8No ratings yet

- PR - No.11 To 17 QuestionsDocument5 pagesPR - No.11 To 17 QuestionsSiva SankariNo ratings yet

- Tutorial Questions Week1Document6 pagesTutorial Questions Week1HuiMinHorNo ratings yet

- Tax 3 RevisionDocument10 pagesTax 3 RevisionSoon Mei QiNo ratings yet

- Poa T - 9Document3 pagesPoa T - 9SHEVENA A/P VIJIANNo ratings yet

- Far Project PrefiDocument16 pagesFar Project PrefiMarjorie PagsinuhinNo ratings yet

- 27 (B3 and B4) .IFP (8,9, 10) - 19.06.2023Document1 page27 (B3 and B4) .IFP (8,9, 10) - 19.06.2023jopah81118No ratings yet

- Tutorial - Employment IncomeDocument3 pagesTutorial - Employment IncomeKiyong TanNo ratings yet

- IT AY 23-24 Prob On HPDocument5 pagesIT AY 23-24 Prob On HPrathanreddy2002No ratings yet

- Tutorial 2 - Trust (Q)Document3 pagesTutorial 2 - Trust (Q)Xin RuNo ratings yet

- TQ9 - Year End Adjustments - UPDATEDocument2 pagesTQ9 - Year End Adjustments - UPDATEWEI SZI LIMNo ratings yet

- Quiz 3 Chapter 8: Income From Property 50 Marks Name: SectionDocument4 pagesQuiz 3 Chapter 8: Income From Property 50 Marks Name: SectionHadiNo ratings yet

- Tax317 Quiz Jan 2023 QDocument4 pagesTax317 Quiz Jan 2023 Q2021830296No ratings yet

- School of Business (SBC) : Module's InformationDocument3 pagesSchool of Business (SBC) : Module's InformationEinNo ratings yet

- 5.1 Questions On Income From House PropertyDocument3 pages5.1 Questions On Income From House PropertyAashi GuptaNo ratings yet

- Tutorial 1 - Estate Settlement (Q)Document9 pagesTutorial 1 - Estate Settlement (Q)Xin RuNo ratings yet

- House Property - IllustrationDocument10 pagesHouse Property - IllustrationAnirban ThakurNo ratings yet

- Example RPGTDocument3 pagesExample RPGTRaudhatun Nisa'No ratings yet

- House Property TestDocument4 pagesHouse Property Testbuddybest22No ratings yet

- PTX - Past Year Set ADocument8 pagesPTX - Past Year Set ANUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)No ratings yet

- TAXATION (Preps)Document5 pagesTAXATION (Preps)Navya GulatiNo ratings yet

- House Propery QuestionsDocument6 pagesHouse Propery QuestionsTauseef AzharNo ratings yet

- Accounting For Operating LeaseDocument4 pagesAccounting For Operating LeaseMhico MateoNo ratings yet

- Lease Practical Accounting ProblemsDocument2 pagesLease Practical Accounting ProblemsCamille BonaguaNo ratings yet

- Tutorial 8 - Stamp Duty and Leasing - 2022Document4 pagesTutorial 8 - Stamp Duty and Leasing - 2022Keat 98No ratings yet

- Question Employment IncomeDocument7 pagesQuestion Employment IncomehannaniNo ratings yet

- Questions 34nosDocument21 pagesQuestions 34nosAshish TomsNo ratings yet

- Assignment LLB 2Document1 pageAssignment LLB 2Nitish Kumar NaveenNo ratings yet

- T2Q Rca22020 - EiDocument3 pagesT2Q Rca22020 - EiHaananth SubramaniamNo ratings yet

- PTX - Final ExamDocument7 pagesPTX - Final ExamNUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)No ratings yet

- Personal Taxation QuestionDocument2 pagesPersonal Taxation QuestionNORZAFIRAH BINTI YUSAININo ratings yet

- Tax467 Dec 2019Document13 pagesTax467 Dec 2019Szasza teppeiNo ratings yet

- Assignment 02 Leases-SolutionDocument10 pagesAssignment 02 Leases-SolutionJaziel SestosoNo ratings yet

- 029 Practice Test 08 Taxation Test Solution Subjective Udesh RegularDocument8 pages029 Practice Test 08 Taxation Test Solution Subjective Udesh Regulardeathp006No ratings yet

- Faculty of Management and MuamalahDocument8 pagesFaculty of Management and MuamalahZati TyNo ratings yet

- Lease Modules ContinuedDocument8 pagesLease Modules ContinuedMariz RapadaNo ratings yet

- Revision 1Document4 pagesRevision 1carazamanNo ratings yet

- ACC2054 MTS Tutorial 6 QDocument2 pagesACC2054 MTS Tutorial 6 QTharvind KumarNo ratings yet

- Aa 498 AssignmentDocument2 pagesAa 498 AssignmentMeena SinghNo ratings yet

- Tax Computation Exercise Zafrul Edna QDocument2 pagesTax Computation Exercise Zafrul Edna QU2104037 STUDENTNo ratings yet

- Test 2 - ACC117 - JNAUARY 2024 - QQDocument5 pagesTest 2 - ACC117 - JNAUARY 2024 - QQamymaisarah05No ratings yet

- T3Q RCA22020 Other IncomeDocument2 pagesT3Q RCA22020 Other IncomeHaananth SubramaniamNo ratings yet

- Tutorial 5 (Class)Document3 pagesTutorial 5 (Class)fujinlim98No ratings yet

- Ia2 - Leases by LessorDocument8 pagesIa2 - Leases by LessornishioyukihimeNo ratings yet

- Barangay Health Worker Registration FormDocument1 pageBarangay Health Worker Registration FormJairah Marie100% (2)

- CSR Policy KsfeDocument6 pagesCSR Policy KsfeOhari NikshepamNo ratings yet

- Workbook Answer Key Unit 8 AcbeuDocument1 pageWorkbook Answer Key Unit 8 AcbeuLuisa Mari AlvamoreNo ratings yet

- Chapter 01 - Introduction To EaDocument18 pagesChapter 01 - Introduction To EaMrz RostanNo ratings yet

- Operationalize The County Policing AuthorityDocument2 pagesOperationalize The County Policing AuthorityOmbayo JuniourNo ratings yet

- XdealSkin Vitamins Tiktok ProposalDocument4 pagesXdealSkin Vitamins Tiktok ProposalElixia KiteNo ratings yet

- Oil and Gas ExplorationDocument87 pagesOil and Gas ExplorationVanix DesuasidoNo ratings yet

- Correction Level 5Document9 pagesCorrection Level 5nika wikaNo ratings yet

- LAZUDAN ZEKRELLAH I. BSMT 2 BD WATCH 1 Semi Final Exam 1Document8 pagesLAZUDAN ZEKRELLAH I. BSMT 2 BD WATCH 1 Semi Final Exam 1Macxie Baldonado QuibuyenNo ratings yet

- ANT332 Answer Key 6Document3 pagesANT332 Answer Key 6mariefmuntheNo ratings yet

- Cheatsheet Gimp-Letter PDFDocument1 pageCheatsheet Gimp-Letter PDFRox DiazNo ratings yet

- Web Bill: Noor Muhammad S/O Muhammad Pinjri Pur Haveli NTN: 00000000000Document1 pageWeb Bill: Noor Muhammad S/O Muhammad Pinjri Pur Haveli NTN: 00000000000Syed Waqar ShahNo ratings yet

- Caterpillar D6Document3 pagesCaterpillar D6RasoolKhadibi100% (1)

- South Bend SB1002 Lathe Owners ManualDocument84 pagesSouth Bend SB1002 Lathe Owners ManualRendab100% (2)

- MDC Monthly Proposal Dec 2019Document2 pagesMDC Monthly Proposal Dec 2019Tushar Prakash ChaudhariNo ratings yet

- 003.ladders - Rev. 0Document25 pages003.ladders - Rev. 0narasimhamurthy414No ratings yet

- Road Safety FundamentalsDocument122 pagesRoad Safety Fundamentalssmanoj354100% (3)

- Mint OilDocument4 pagesMint OilPreeti SinghNo ratings yet

- TDS - Emaco R907 PlusDocument2 pagesTDS - Emaco R907 PlusVenkata RaoNo ratings yet

- Fire Protection Valves: Effective March 18, 2013 - Supercedes FPP-0312 of March 26, 2012Document8 pagesFire Protection Valves: Effective March 18, 2013 - Supercedes FPP-0312 of March 26, 2012Jorge Alberto Martinez OrtizNo ratings yet

- Case FerreroDocument22 pagesCase FerreroGlyka K. RigaNo ratings yet

- Mock Test - 98 (17 Jan 2023) Rotational DynamicsDocument1 pageMock Test - 98 (17 Jan 2023) Rotational DynamicsparamNo ratings yet

- Carnot Cycle - Working Principle & Processes With (PV - Ts Diagram)Document8 pagesCarnot Cycle - Working Principle & Processes With (PV - Ts Diagram)Sharif Muhammad HossainNo ratings yet

- Lesson 7 Protection For Estaurieas and Intertidal ZoneDocument15 pagesLesson 7 Protection For Estaurieas and Intertidal ZoneTeacher JoanNo ratings yet

- 22 Passage 2 - Western Immigration of Canada Q14-26Document6 pages22 Passage 2 - Western Immigration of Canada Q14-26Cương Nguyễn DuyNo ratings yet

- Kopi-O: Seating ProductsDocument8 pagesKopi-O: Seating Productsishanj1991No ratings yet

- 2.1.c.ii. Theory of Liming and UnhairingDocument5 pages2.1.c.ii. Theory of Liming and UnhairingAnanthNo ratings yet

- Banco de Oro Savings and Mortgage Bank vs. Equitable Banking CorporationDocument15 pagesBanco de Oro Savings and Mortgage Bank vs. Equitable Banking CorporationFD Balita0% (1)

- Musician VC YGO IV 2021Document1 pageMusician VC YGO IV 2021Ari J PalawiNo ratings yet

Download as pdf or txt

You might also like

- Final Test Fin533 January 2024Document13 pagesFinal Test Fin533 January 20242023607226No ratings yet

- Adjusting Entries Exercises - EditedDocument4 pagesAdjusting Entries Exercises - EditedCINDY LIAN CABILLON100% (2)

- Lessor Discussion U PDFDocument4 pagesLessor Discussion U PDFadmiral spongebobNo ratings yet

- Lease Modules ContinuedDocument8 pagesLease Modules ContinuedKenneth Marcial Ege0% (1)

- Intro To Consulting SlidesDocument34 pagesIntro To Consulting Slidesmanojben100% (2)

- Week 7Document3 pagesWeek 7xinghe666No ratings yet

- Distribute A231 - BKAT3033 - Tutorial 123 - QDocument7 pagesDistribute A231 - BKAT3033 - Tutorial 123 - QallyaNo ratings yet

- Lecture6 - RPGT Class Exercise QDocument4 pagesLecture6 - RPGT Class Exercise QpremsuwaatiiNo ratings yet

- T4 Other Income Q 1-2020-2021Document2 pagesT4 Other Income Q 1-2020-2021Putri Nurin Hasnida HassanNo ratings yet

- Week 8Document3 pagesWeek 8xinghe666No ratings yet

- Prop Tax A RPGT Illustrations (Tracked)Document39 pagesProp Tax A RPGT Illustrations (Tracked)celina kohNo ratings yet

- Abft1024 T8 - LtyDocument2 pagesAbft1024 T8 - Ltylfc778No ratings yet

- Tutorial 9 Year End Adjustments (Q)Document4 pagesTutorial 9 Year End Adjustments (Q)lious lii0% (1)

- Examples & Practice Questions For Income From PropertyDocument8 pagesExamples & Practice Questions For Income From PropertyAbdulAzeemNo ratings yet

- Tutorial 3 - RPGT-2022Document4 pagesTutorial 3 - RPGT-2022Keat 98No ratings yet

- Tutorial 4 QDocument6 pagesTutorial 4 Q謝中豪No ratings yet

- Tutorial Q - Partnership - Feb2024Document2 pagesTutorial Q - Partnership - Feb2024farhanahiszati8No ratings yet

- PR - No.11 To 17 QuestionsDocument5 pagesPR - No.11 To 17 QuestionsSiva SankariNo ratings yet

- Tutorial Questions Week1Document6 pagesTutorial Questions Week1HuiMinHorNo ratings yet

- Tax 3 RevisionDocument10 pagesTax 3 RevisionSoon Mei QiNo ratings yet

- Poa T - 9Document3 pagesPoa T - 9SHEVENA A/P VIJIANNo ratings yet

- Far Project PrefiDocument16 pagesFar Project PrefiMarjorie PagsinuhinNo ratings yet

- 27 (B3 and B4) .IFP (8,9, 10) - 19.06.2023Document1 page27 (B3 and B4) .IFP (8,9, 10) - 19.06.2023jopah81118No ratings yet

- Tutorial - Employment IncomeDocument3 pagesTutorial - Employment IncomeKiyong TanNo ratings yet

- IT AY 23-24 Prob On HPDocument5 pagesIT AY 23-24 Prob On HPrathanreddy2002No ratings yet

- Tutorial 2 - Trust (Q)Document3 pagesTutorial 2 - Trust (Q)Xin RuNo ratings yet

- TQ9 - Year End Adjustments - UPDATEDocument2 pagesTQ9 - Year End Adjustments - UPDATEWEI SZI LIMNo ratings yet

- Quiz 3 Chapter 8: Income From Property 50 Marks Name: SectionDocument4 pagesQuiz 3 Chapter 8: Income From Property 50 Marks Name: SectionHadiNo ratings yet

- Tax317 Quiz Jan 2023 QDocument4 pagesTax317 Quiz Jan 2023 Q2021830296No ratings yet

- School of Business (SBC) : Module's InformationDocument3 pagesSchool of Business (SBC) : Module's InformationEinNo ratings yet

- 5.1 Questions On Income From House PropertyDocument3 pages5.1 Questions On Income From House PropertyAashi GuptaNo ratings yet

- Tutorial 1 - Estate Settlement (Q)Document9 pagesTutorial 1 - Estate Settlement (Q)Xin RuNo ratings yet

- House Property - IllustrationDocument10 pagesHouse Property - IllustrationAnirban ThakurNo ratings yet

- Example RPGTDocument3 pagesExample RPGTRaudhatun Nisa'No ratings yet

- House Property TestDocument4 pagesHouse Property Testbuddybest22No ratings yet

- PTX - Past Year Set ADocument8 pagesPTX - Past Year Set ANUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)No ratings yet

- TAXATION (Preps)Document5 pagesTAXATION (Preps)Navya GulatiNo ratings yet

- House Propery QuestionsDocument6 pagesHouse Propery QuestionsTauseef AzharNo ratings yet

- Accounting For Operating LeaseDocument4 pagesAccounting For Operating LeaseMhico MateoNo ratings yet

- Lease Practical Accounting ProblemsDocument2 pagesLease Practical Accounting ProblemsCamille BonaguaNo ratings yet

- Tutorial 8 - Stamp Duty and Leasing - 2022Document4 pagesTutorial 8 - Stamp Duty and Leasing - 2022Keat 98No ratings yet

- Question Employment IncomeDocument7 pagesQuestion Employment IncomehannaniNo ratings yet

- Questions 34nosDocument21 pagesQuestions 34nosAshish TomsNo ratings yet

- Assignment LLB 2Document1 pageAssignment LLB 2Nitish Kumar NaveenNo ratings yet

- T2Q Rca22020 - EiDocument3 pagesT2Q Rca22020 - EiHaananth SubramaniamNo ratings yet

- PTX - Final ExamDocument7 pagesPTX - Final ExamNUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)No ratings yet

- Personal Taxation QuestionDocument2 pagesPersonal Taxation QuestionNORZAFIRAH BINTI YUSAININo ratings yet

- Tax467 Dec 2019Document13 pagesTax467 Dec 2019Szasza teppeiNo ratings yet

- Assignment 02 Leases-SolutionDocument10 pagesAssignment 02 Leases-SolutionJaziel SestosoNo ratings yet

- 029 Practice Test 08 Taxation Test Solution Subjective Udesh RegularDocument8 pages029 Practice Test 08 Taxation Test Solution Subjective Udesh Regulardeathp006No ratings yet

- Faculty of Management and MuamalahDocument8 pagesFaculty of Management and MuamalahZati TyNo ratings yet

- Lease Modules ContinuedDocument8 pagesLease Modules ContinuedMariz RapadaNo ratings yet

- Revision 1Document4 pagesRevision 1carazamanNo ratings yet

- ACC2054 MTS Tutorial 6 QDocument2 pagesACC2054 MTS Tutorial 6 QTharvind KumarNo ratings yet

- Aa 498 AssignmentDocument2 pagesAa 498 AssignmentMeena SinghNo ratings yet

- Tax Computation Exercise Zafrul Edna QDocument2 pagesTax Computation Exercise Zafrul Edna QU2104037 STUDENTNo ratings yet

- Test 2 - ACC117 - JNAUARY 2024 - QQDocument5 pagesTest 2 - ACC117 - JNAUARY 2024 - QQamymaisarah05No ratings yet

- T3Q RCA22020 Other IncomeDocument2 pagesT3Q RCA22020 Other IncomeHaananth SubramaniamNo ratings yet

- Tutorial 5 (Class)Document3 pagesTutorial 5 (Class)fujinlim98No ratings yet

- Ia2 - Leases by LessorDocument8 pagesIa2 - Leases by LessornishioyukihimeNo ratings yet

- Barangay Health Worker Registration FormDocument1 pageBarangay Health Worker Registration FormJairah Marie100% (2)

- CSR Policy KsfeDocument6 pagesCSR Policy KsfeOhari NikshepamNo ratings yet

- Workbook Answer Key Unit 8 AcbeuDocument1 pageWorkbook Answer Key Unit 8 AcbeuLuisa Mari AlvamoreNo ratings yet

- Chapter 01 - Introduction To EaDocument18 pagesChapter 01 - Introduction To EaMrz RostanNo ratings yet

- Operationalize The County Policing AuthorityDocument2 pagesOperationalize The County Policing AuthorityOmbayo JuniourNo ratings yet

- XdealSkin Vitamins Tiktok ProposalDocument4 pagesXdealSkin Vitamins Tiktok ProposalElixia KiteNo ratings yet

- Oil and Gas ExplorationDocument87 pagesOil and Gas ExplorationVanix DesuasidoNo ratings yet

- Correction Level 5Document9 pagesCorrection Level 5nika wikaNo ratings yet

- LAZUDAN ZEKRELLAH I. BSMT 2 BD WATCH 1 Semi Final Exam 1Document8 pagesLAZUDAN ZEKRELLAH I. BSMT 2 BD WATCH 1 Semi Final Exam 1Macxie Baldonado QuibuyenNo ratings yet

- ANT332 Answer Key 6Document3 pagesANT332 Answer Key 6mariefmuntheNo ratings yet

- Cheatsheet Gimp-Letter PDFDocument1 pageCheatsheet Gimp-Letter PDFRox DiazNo ratings yet

- Web Bill: Noor Muhammad S/O Muhammad Pinjri Pur Haveli NTN: 00000000000Document1 pageWeb Bill: Noor Muhammad S/O Muhammad Pinjri Pur Haveli NTN: 00000000000Syed Waqar ShahNo ratings yet

- Caterpillar D6Document3 pagesCaterpillar D6RasoolKhadibi100% (1)

- South Bend SB1002 Lathe Owners ManualDocument84 pagesSouth Bend SB1002 Lathe Owners ManualRendab100% (2)

- MDC Monthly Proposal Dec 2019Document2 pagesMDC Monthly Proposal Dec 2019Tushar Prakash ChaudhariNo ratings yet

- 003.ladders - Rev. 0Document25 pages003.ladders - Rev. 0narasimhamurthy414No ratings yet

- Road Safety FundamentalsDocument122 pagesRoad Safety Fundamentalssmanoj354100% (3)

- Mint OilDocument4 pagesMint OilPreeti SinghNo ratings yet

- TDS - Emaco R907 PlusDocument2 pagesTDS - Emaco R907 PlusVenkata RaoNo ratings yet

- Fire Protection Valves: Effective March 18, 2013 - Supercedes FPP-0312 of March 26, 2012Document8 pagesFire Protection Valves: Effective March 18, 2013 - Supercedes FPP-0312 of March 26, 2012Jorge Alberto Martinez OrtizNo ratings yet

- Case FerreroDocument22 pagesCase FerreroGlyka K. RigaNo ratings yet

- Mock Test - 98 (17 Jan 2023) Rotational DynamicsDocument1 pageMock Test - 98 (17 Jan 2023) Rotational DynamicsparamNo ratings yet

- Carnot Cycle - Working Principle & Processes With (PV - Ts Diagram)Document8 pagesCarnot Cycle - Working Principle & Processes With (PV - Ts Diagram)Sharif Muhammad HossainNo ratings yet

- Lesson 7 Protection For Estaurieas and Intertidal ZoneDocument15 pagesLesson 7 Protection For Estaurieas and Intertidal ZoneTeacher JoanNo ratings yet

- 22 Passage 2 - Western Immigration of Canada Q14-26Document6 pages22 Passage 2 - Western Immigration of Canada Q14-26Cương Nguyễn DuyNo ratings yet

- Kopi-O: Seating ProductsDocument8 pagesKopi-O: Seating Productsishanj1991No ratings yet

- 2.1.c.ii. Theory of Liming and UnhairingDocument5 pages2.1.c.ii. Theory of Liming and UnhairingAnanthNo ratings yet

- Banco de Oro Savings and Mortgage Bank vs. Equitable Banking CorporationDocument15 pagesBanco de Oro Savings and Mortgage Bank vs. Equitable Banking CorporationFD Balita0% (1)

- Musician VC YGO IV 2021Document1 pageMusician VC YGO IV 2021Ari J PalawiNo ratings yet