Capital Allowances

Capital Allowances

You might also like

- SAP Group Reporting and ConsolidationDocument21 pagesSAP Group Reporting and ConsolidationA V Srikanth100% (4)

- California PizzaDocument4 pagesCalifornia PizzaMaria Fe Callejas0% (1)

- One Stock CrorepatiDocument27 pagesOne Stock Crorepatigedosi50% (10)

- D8Document11 pagesD8neo14100% (1)

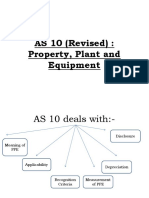

- AS 10 (Revised) : Property, Plant and EquipmentDocument34 pagesAS 10 (Revised) : Property, Plant and EquipmentAkshay PatilNo ratings yet

- CGT SummaryDocument3 pagesCGT Summaryk.c sedibeNo ratings yet

- Pas 16 Property Plant and EquipmentDocument4 pagesPas 16 Property Plant and EquipmentKristalen ArmandoNo ratings yet

- ICAIEKM Material 180116Document57 pagesICAIEKM Material 180116INTER SMARTIANSNo ratings yet

- IFRS CH 4Document6 pagesIFRS CH 4a.adel87No ratings yet

- Capital Allowances SummaryDocument7 pagesCapital Allowances Summarydubembalenhle2003No ratings yet

- Capital Allowances - RevisionDocument2 pagesCapital Allowances - RevisionkauthartaliepNo ratings yet

- Plant AssetsDocument17 pagesPlant AssetsGizaw Belay100% (1)

- AA203 - Cheat Sheet (SB)Document4 pagesAA203 - Cheat Sheet (SB)thooshengbaoNo ratings yet

- Ind AS 16 - RBM (WBS)Document7 pagesInd AS 16 - RBM (WBS)KRISHNENDU JASHNo ratings yet

- Capital AllowancesDocument3 pagesCapital AllowancesNurain Nabilah ZakariyaNo ratings yet

- Chapter 2 Plant Asset PDFDocument20 pagesChapter 2 Plant Asset PDFWonde Biru100% (1)

- Far05. PpeDocument4 pagesFar05. PpeJohn Kenneth BacanNo ratings yet

- Lec - 3Document7 pagesLec - 3Mostafa KaghaNo ratings yet

- Profit & Gain From Business or Profession: Section 145: Taxability As Per Method of Accounting Followed by AssesseeDocument25 pagesProfit & Gain From Business or Profession: Section 145: Taxability As Per Method of Accounting Followed by AssesseeRajesh NangaliaNo ratings yet

- ITC June 2022 Paper 1 Part II Beeprop SolutionDocument5 pagesITC June 2022 Paper 1 Part II Beeprop Solutiondjbongz777No ratings yet

- Ppe Acctng203Document5 pagesPpe Acctng203PgumballNo ratings yet

- FAR 17 - Investment in PropertyDocument2 pagesFAR 17 - Investment in Propertymrsjeon0501No ratings yet

- 1716007983353Document8 pages1716007983353ahmedabso1717No ratings yet

- IAS 16 Property, Plant and EquipmentDocument18 pagesIAS 16 Property, Plant and EquipmentMuhammad Umar IqbalNo ratings yet

- Chapter 03Document2 pagesChapter 03Patrick Kyle AgraviadorNo ratings yet

- Chapter 10 SolutionsDocument70 pagesChapter 10 SolutionsLy VõNo ratings yet

- Cost Accounting QuicknotesDocument8 pagesCost Accounting QuicknotesjuleslovefenNo ratings yet

- Week 1-2 - Investment Property SummaryDocument4 pagesWeek 1-2 - Investment Property Summarykrushi.ntumunNo ratings yet

- Lesson 1 PPEDocument17 pagesLesson 1 PPEBeatriz Jade TicobayNo ratings yet

- To Recognize The Purchase of Investment PropertyDocument3 pagesTo Recognize The Purchase of Investment PropertyShantalNo ratings yet

- ACC - Chapter 10Document40 pagesACC - Chapter 10Le Pham Khanh Ha (K17 HCM)No ratings yet

- 1, Aset TetapDocument45 pages1, Aset TetapM Syukrihady IrsyadNo ratings yet

- Module 11Document14 pagesModule 11Maria Therese CorderoNo ratings yet

- CIA2001 Lecture Notes Investment PropertyDocument18 pagesCIA2001 Lecture Notes Investment PropertySatthya PeterNo ratings yet

- Capital Gains Tax (Ampongan)Document11 pagesCapital Gains Tax (Ampongan)didit.canonNo ratings yet

- Taxable Fringe BenefitsDocument10 pagesTaxable Fringe BenefitskauthartaliepNo ratings yet

- AS 10 Property, Plant & EquipmentDocument23 pagesAS 10 Property, Plant & EquipmentRENU PALINo ratings yet

- LU6 Capital AllowancesDocument31 pagesLU6 Capital AllowancesabasoomarishaaqNo ratings yet

- 1.2 Far1 Vol II Autumn 2022Document417 pages1.2 Far1 Vol II Autumn 2022rana m harisNo ratings yet

- CH 14 Rental IncomeDocument5 pagesCH 14 Rental IncomeNurin NadhirahNo ratings yet

- Chapter 10 PPTDocument48 pagesChapter 10 PPTkjw 2No ratings yet

- Corporate Tax Planning Unit 3Document17 pagesCorporate Tax Planning Unit 3Abinash PrustyNo ratings yet

- Add Material MFRS116 NotesDocument37 pagesAdd Material MFRS116 NotesDont RushNo ratings yet

- CACC021 IAS 16 - Slides (2024)Document20 pagesCACC021 IAS 16 - Slides (2024)chabalalalesedi254No ratings yet

- Module 6 IAS 40 ADDITIONAL NOTESDocument4 pagesModule 6 IAS 40 ADDITIONAL NOTESsiobhan margaretNo ratings yet

- Financial Accounting: Fixed & Intangible AssetsDocument26 pagesFinancial Accounting: Fixed & Intangible AssetsAstri RirinNo ratings yet

- Chapter 9 - Lecture Notes - DungDocument56 pagesChapter 9 - Lecture Notes - DungThanh UyênNo ratings yet

- Notes - Investment Property BookDocument2 pagesNotes - Investment Property BookJake AustriaNo ratings yet

- Fundamentals of Accounting Ii: Property, Plant and Equipment Are Tangible Items ThatDocument20 pagesFundamentals of Accounting Ii: Property, Plant and Equipment Are Tangible Items ThatYadeno GirmaNo ratings yet

- PGBP - May 2024 & June 2024Document10 pagesPGBP - May 2024 & June 2024shauryaaaaa22kNo ratings yet

- 3 Non-Current Assets TopicDocument43 pages3 Non-Current Assets TopicpesseNo ratings yet

- Contract CostingDocument17 pagesContract CostingHarshit DaveNo ratings yet

- Vol 3 Chapter 6Document5 pagesVol 3 Chapter 6Mary Claudette UnabiaNo ratings yet

- Tax and Accounting 5Document2 pagesTax and Accounting 5Jerrom DuqueNo ratings yet

- Deductions From Gross IncomeDocument6 pagesDeductions From Gross Incomeacuman.irishNo ratings yet

- 01 Ias 16Document9 pages01 Ias 16salman jabbarNo ratings yet

- Lecture Notes On Capital Allowances and RecoupmentsDocument53 pagesLecture Notes On Capital Allowances and RecoupmentsNchafie AsemahleNo ratings yet

- Tax and Accounting 2Document2 pagesTax and Accounting 2Jerrom DuqueNo ratings yet

- Ias 16 PpeDocument40 pagesIas 16 PpeziyuNo ratings yet

- TENDER OF PLANT BUILDING & EQUIPMENT INSTALLATION - HitungDocument51 pagesTENDER OF PLANT BUILDING & EQUIPMENT INSTALLATION - HitungRini AdelinaNo ratings yet

- P&R AnalysisDocument29 pagesP&R Analysiscontact.xinanneNo ratings yet

- Video Case CH 15Document3 pagesVideo Case CH 15Panji Yudha SanjayaNo ratings yet

- Module 3 InvestmentDocument12 pagesModule 3 InvestmentKim JisooNo ratings yet

- Chapter 24 - Teachers Manual - Aa Part 2 PDFDocument13 pagesChapter 24 - Teachers Manual - Aa Part 2 PDFSheed ChiuNo ratings yet

- Reading Stock Market PDFDocument3 pagesReading Stock Market PDFfiorella lillian tito cerronNo ratings yet

- BII 2023 Global Outlook Latam EditionDocument18 pagesBII 2023 Global Outlook Latam EditionContacto Ex-Ante100% (1)

- Business Unit 3 NotesDocument45 pagesBusiness Unit 3 Notesamir dargahiNo ratings yet

- Break Even Analysis and Ratio AnalysisDocument63 pagesBreak Even Analysis and Ratio AnalysisJaywanti Akshra Gurbani100% (1)

- Weak Balance Sheet Drags Profitability: Q3FY18 Result HighlightsDocument8 pagesWeak Balance Sheet Drags Profitability: Q3FY18 Result Highlightsrishab agarwalNo ratings yet

- April StatementDocument9 pagesApril Statementyv4pfn8xhhNo ratings yet

- Requirements For Increase of Capital StocksDocument3 pagesRequirements For Increase of Capital StocksNarciso Reyes Jr.0% (1)

- CV ContohDocument1 pageCV ContohFikriNo ratings yet

- BE Threatbar-KLHGRB - RB - RB - 16x360 - 2023Document7 pagesBE Threatbar-KLHGRB - RB - RB - 16x360 - 2023ANDRI MULYADINo ratings yet

- Conceptual Framework: & Accounting StandardsDocument45 pagesConceptual Framework: & Accounting StandardsAmie Jane MirandaNo ratings yet

- CHAPTER 1 Trial - ACC101Document9 pagesCHAPTER 1 Trial - ACC101An nguyên Trương ĐỗNo ratings yet

- ACCA104 - Investment in AssociatesDocument6 pagesACCA104 - Investment in AssociatesAnaluz Cristine B. CeaNo ratings yet

- 1 - Financial DecisionsDocument9 pages1 - Financial DecisionsByamaka ObedNo ratings yet

- Chapter 5Document46 pagesChapter 5vaman kambleNo ratings yet

- Investment Vs FinancingDocument6 pagesInvestment Vs FinancingSolomon, Heren Mae M.No ratings yet

- Project Evaluation QuestionsDocument5 pagesProject Evaluation Questionsanon_615698823No ratings yet

- 2022-11-10 19 30 51 Morning-NoteDocument8 pages2022-11-10 19 30 51 Morning-Notevikalp123123No ratings yet

- Mutual FundsDocument35 pagesMutual FundsDovilė Purickaitė - Koncienė100% (1)

- When Value Failed - But Quantum Succeeded - The Honest Truth by Ajit Dayal PDFDocument7 pagesWhen Value Failed - But Quantum Succeeded - The Honest Truth by Ajit Dayal PDFdeepakc598No ratings yet

- Customer CentricityDocument2 pagesCustomer CentricityHarinie SutharsonNo ratings yet

- 2) Short Notes: A) Forms of DividendDocument2 pages2) Short Notes: A) Forms of DividendTarunvir KukrejaNo ratings yet

- A Study of Foreign Exchange Exposure in The Indian IT SectorDocument14 pagesA Study of Foreign Exchange Exposure in The Indian IT SectorAnish AnishNo ratings yet

- Fin Man HW1Document3 pagesFin Man HW1KingkongNo ratings yet

Download as pdf or txt

You might also like

- SAP Group Reporting and ConsolidationDocument21 pagesSAP Group Reporting and ConsolidationA V Srikanth100% (4)

- California PizzaDocument4 pagesCalifornia PizzaMaria Fe Callejas0% (1)

- One Stock CrorepatiDocument27 pagesOne Stock Crorepatigedosi50% (10)

- D8Document11 pagesD8neo14100% (1)

- AS 10 (Revised) : Property, Plant and EquipmentDocument34 pagesAS 10 (Revised) : Property, Plant and EquipmentAkshay PatilNo ratings yet

- CGT SummaryDocument3 pagesCGT Summaryk.c sedibeNo ratings yet

- Pas 16 Property Plant and EquipmentDocument4 pagesPas 16 Property Plant and EquipmentKristalen ArmandoNo ratings yet

- ICAIEKM Material 180116Document57 pagesICAIEKM Material 180116INTER SMARTIANSNo ratings yet

- IFRS CH 4Document6 pagesIFRS CH 4a.adel87No ratings yet

- Capital Allowances SummaryDocument7 pagesCapital Allowances Summarydubembalenhle2003No ratings yet

- Capital Allowances - RevisionDocument2 pagesCapital Allowances - RevisionkauthartaliepNo ratings yet

- Plant AssetsDocument17 pagesPlant AssetsGizaw Belay100% (1)

- AA203 - Cheat Sheet (SB)Document4 pagesAA203 - Cheat Sheet (SB)thooshengbaoNo ratings yet

- Ind AS 16 - RBM (WBS)Document7 pagesInd AS 16 - RBM (WBS)KRISHNENDU JASHNo ratings yet

- Capital AllowancesDocument3 pagesCapital AllowancesNurain Nabilah ZakariyaNo ratings yet

- Chapter 2 Plant Asset PDFDocument20 pagesChapter 2 Plant Asset PDFWonde Biru100% (1)

- Far05. PpeDocument4 pagesFar05. PpeJohn Kenneth BacanNo ratings yet

- Lec - 3Document7 pagesLec - 3Mostafa KaghaNo ratings yet

- Profit & Gain From Business or Profession: Section 145: Taxability As Per Method of Accounting Followed by AssesseeDocument25 pagesProfit & Gain From Business or Profession: Section 145: Taxability As Per Method of Accounting Followed by AssesseeRajesh NangaliaNo ratings yet

- ITC June 2022 Paper 1 Part II Beeprop SolutionDocument5 pagesITC June 2022 Paper 1 Part II Beeprop Solutiondjbongz777No ratings yet

- Ppe Acctng203Document5 pagesPpe Acctng203PgumballNo ratings yet

- FAR 17 - Investment in PropertyDocument2 pagesFAR 17 - Investment in Propertymrsjeon0501No ratings yet

- 1716007983353Document8 pages1716007983353ahmedabso1717No ratings yet

- IAS 16 Property, Plant and EquipmentDocument18 pagesIAS 16 Property, Plant and EquipmentMuhammad Umar IqbalNo ratings yet

- Chapter 03Document2 pagesChapter 03Patrick Kyle AgraviadorNo ratings yet

- Chapter 10 SolutionsDocument70 pagesChapter 10 SolutionsLy VõNo ratings yet

- Cost Accounting QuicknotesDocument8 pagesCost Accounting QuicknotesjuleslovefenNo ratings yet

- Week 1-2 - Investment Property SummaryDocument4 pagesWeek 1-2 - Investment Property Summarykrushi.ntumunNo ratings yet

- Lesson 1 PPEDocument17 pagesLesson 1 PPEBeatriz Jade TicobayNo ratings yet

- To Recognize The Purchase of Investment PropertyDocument3 pagesTo Recognize The Purchase of Investment PropertyShantalNo ratings yet

- ACC - Chapter 10Document40 pagesACC - Chapter 10Le Pham Khanh Ha (K17 HCM)No ratings yet

- 1, Aset TetapDocument45 pages1, Aset TetapM Syukrihady IrsyadNo ratings yet

- Module 11Document14 pagesModule 11Maria Therese CorderoNo ratings yet

- CIA2001 Lecture Notes Investment PropertyDocument18 pagesCIA2001 Lecture Notes Investment PropertySatthya PeterNo ratings yet

- Capital Gains Tax (Ampongan)Document11 pagesCapital Gains Tax (Ampongan)didit.canonNo ratings yet

- Taxable Fringe BenefitsDocument10 pagesTaxable Fringe BenefitskauthartaliepNo ratings yet

- AS 10 Property, Plant & EquipmentDocument23 pagesAS 10 Property, Plant & EquipmentRENU PALINo ratings yet

- LU6 Capital AllowancesDocument31 pagesLU6 Capital AllowancesabasoomarishaaqNo ratings yet

- 1.2 Far1 Vol II Autumn 2022Document417 pages1.2 Far1 Vol II Autumn 2022rana m harisNo ratings yet

- CH 14 Rental IncomeDocument5 pagesCH 14 Rental IncomeNurin NadhirahNo ratings yet

- Chapter 10 PPTDocument48 pagesChapter 10 PPTkjw 2No ratings yet

- Corporate Tax Planning Unit 3Document17 pagesCorporate Tax Planning Unit 3Abinash PrustyNo ratings yet

- Add Material MFRS116 NotesDocument37 pagesAdd Material MFRS116 NotesDont RushNo ratings yet

- CACC021 IAS 16 - Slides (2024)Document20 pagesCACC021 IAS 16 - Slides (2024)chabalalalesedi254No ratings yet

- Module 6 IAS 40 ADDITIONAL NOTESDocument4 pagesModule 6 IAS 40 ADDITIONAL NOTESsiobhan margaretNo ratings yet

- Financial Accounting: Fixed & Intangible AssetsDocument26 pagesFinancial Accounting: Fixed & Intangible AssetsAstri RirinNo ratings yet

- Chapter 9 - Lecture Notes - DungDocument56 pagesChapter 9 - Lecture Notes - DungThanh UyênNo ratings yet

- Notes - Investment Property BookDocument2 pagesNotes - Investment Property BookJake AustriaNo ratings yet

- Fundamentals of Accounting Ii: Property, Plant and Equipment Are Tangible Items ThatDocument20 pagesFundamentals of Accounting Ii: Property, Plant and Equipment Are Tangible Items ThatYadeno GirmaNo ratings yet

- PGBP - May 2024 & June 2024Document10 pagesPGBP - May 2024 & June 2024shauryaaaaa22kNo ratings yet

- 3 Non-Current Assets TopicDocument43 pages3 Non-Current Assets TopicpesseNo ratings yet

- Contract CostingDocument17 pagesContract CostingHarshit DaveNo ratings yet

- Vol 3 Chapter 6Document5 pagesVol 3 Chapter 6Mary Claudette UnabiaNo ratings yet

- Tax and Accounting 5Document2 pagesTax and Accounting 5Jerrom DuqueNo ratings yet

- Deductions From Gross IncomeDocument6 pagesDeductions From Gross Incomeacuman.irishNo ratings yet

- 01 Ias 16Document9 pages01 Ias 16salman jabbarNo ratings yet

- Lecture Notes On Capital Allowances and RecoupmentsDocument53 pagesLecture Notes On Capital Allowances and RecoupmentsNchafie AsemahleNo ratings yet

- Tax and Accounting 2Document2 pagesTax and Accounting 2Jerrom DuqueNo ratings yet

- Ias 16 PpeDocument40 pagesIas 16 PpeziyuNo ratings yet

- TENDER OF PLANT BUILDING & EQUIPMENT INSTALLATION - HitungDocument51 pagesTENDER OF PLANT BUILDING & EQUIPMENT INSTALLATION - HitungRini AdelinaNo ratings yet

- P&R AnalysisDocument29 pagesP&R Analysiscontact.xinanneNo ratings yet

- Video Case CH 15Document3 pagesVideo Case CH 15Panji Yudha SanjayaNo ratings yet

- Module 3 InvestmentDocument12 pagesModule 3 InvestmentKim JisooNo ratings yet

- Chapter 24 - Teachers Manual - Aa Part 2 PDFDocument13 pagesChapter 24 - Teachers Manual - Aa Part 2 PDFSheed ChiuNo ratings yet

- Reading Stock Market PDFDocument3 pagesReading Stock Market PDFfiorella lillian tito cerronNo ratings yet

- BII 2023 Global Outlook Latam EditionDocument18 pagesBII 2023 Global Outlook Latam EditionContacto Ex-Ante100% (1)

- Business Unit 3 NotesDocument45 pagesBusiness Unit 3 Notesamir dargahiNo ratings yet

- Break Even Analysis and Ratio AnalysisDocument63 pagesBreak Even Analysis and Ratio AnalysisJaywanti Akshra Gurbani100% (1)

- Weak Balance Sheet Drags Profitability: Q3FY18 Result HighlightsDocument8 pagesWeak Balance Sheet Drags Profitability: Q3FY18 Result Highlightsrishab agarwalNo ratings yet

- April StatementDocument9 pagesApril Statementyv4pfn8xhhNo ratings yet

- Requirements For Increase of Capital StocksDocument3 pagesRequirements For Increase of Capital StocksNarciso Reyes Jr.0% (1)

- CV ContohDocument1 pageCV ContohFikriNo ratings yet

- BE Threatbar-KLHGRB - RB - RB - 16x360 - 2023Document7 pagesBE Threatbar-KLHGRB - RB - RB - 16x360 - 2023ANDRI MULYADINo ratings yet

- Conceptual Framework: & Accounting StandardsDocument45 pagesConceptual Framework: & Accounting StandardsAmie Jane MirandaNo ratings yet

- CHAPTER 1 Trial - ACC101Document9 pagesCHAPTER 1 Trial - ACC101An nguyên Trương ĐỗNo ratings yet

- ACCA104 - Investment in AssociatesDocument6 pagesACCA104 - Investment in AssociatesAnaluz Cristine B. CeaNo ratings yet

- 1 - Financial DecisionsDocument9 pages1 - Financial DecisionsByamaka ObedNo ratings yet

- Chapter 5Document46 pagesChapter 5vaman kambleNo ratings yet

- Investment Vs FinancingDocument6 pagesInvestment Vs FinancingSolomon, Heren Mae M.No ratings yet

- Project Evaluation QuestionsDocument5 pagesProject Evaluation Questionsanon_615698823No ratings yet

- 2022-11-10 19 30 51 Morning-NoteDocument8 pages2022-11-10 19 30 51 Morning-Notevikalp123123No ratings yet

- Mutual FundsDocument35 pagesMutual FundsDovilė Purickaitė - Koncienė100% (1)

- When Value Failed - But Quantum Succeeded - The Honest Truth by Ajit Dayal PDFDocument7 pagesWhen Value Failed - But Quantum Succeeded - The Honest Truth by Ajit Dayal PDFdeepakc598No ratings yet

- Customer CentricityDocument2 pagesCustomer CentricityHarinie SutharsonNo ratings yet

- 2) Short Notes: A) Forms of DividendDocument2 pages2) Short Notes: A) Forms of DividendTarunvir KukrejaNo ratings yet

- A Study of Foreign Exchange Exposure in The Indian IT SectorDocument14 pagesA Study of Foreign Exchange Exposure in The Indian IT SectorAnish AnishNo ratings yet

- Fin Man HW1Document3 pagesFin Man HW1KingkongNo ratings yet