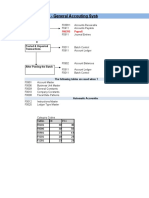

Balance Sheet Explanation

Balance Sheet Explanation

You might also like

- Answer Key - Chapter 6 - ACCOUNTINGDocument92 pagesAnswer Key - Chapter 6 - ACCOUNTINGIL MareNo ratings yet

- Fundamentals of Accountancy, Business, and Management 2: ExpectationDocument131 pagesFundamentals of Accountancy, Business, and Management 2: ExpectationAngela Garcia100% (1)

- Chapter-2 Accounting CycleDocument18 pagesChapter-2 Accounting CycleTsegaye BelayNo ratings yet

- Chapter 2Document24 pagesChapter 2Lleiram Bulotano Bolanio25% (4)

- MGMT 026 Connect Chapter 3 Homework HQ PDFDocument28 pagesMGMT 026 Connect Chapter 3 Homework HQ PDFKailash KumarNo ratings yet

- Introduction To Balance SheetDocument10 pagesIntroduction To Balance SheetJodie Ann PajacNo ratings yet

- Apoyo 1.. - InglesDocument5 pagesApoyo 1.. - InglesWilder ManceraNo ratings yet

- Since A Long Time AgoDocument5 pagesSince A Long Time AgoPatrisia CibisovNo ratings yet

- Fundamentals Ofabm2: Gerlie D. BorneaDocument53 pagesFundamentals Ofabm2: Gerlie D. BorneaGerlie BorneaNo ratings yet

- Unit 3 Cost Estimation and Annual ReportsDocument35 pagesUnit 3 Cost Estimation and Annual ReportsRamakrishna ReddyNo ratings yet

- Chapter 2Document21 pagesChapter 2Kibrom EmbzaNo ratings yet

- Name: Giovanni Oliveria. Opog 12-VenusDocument7 pagesName: Giovanni Oliveria. Opog 12-VenusbannieopogNo ratings yet

- Accounting Elements in The Statement of Financial PositionDocument4 pagesAccounting Elements in The Statement of Financial PositionBianca Jane GaayonNo ratings yet

- Csec Poa Handout 3Document32 pagesCsec Poa Handout 3Taariq Abdul-MajeedNo ratings yet

- Accounting Notes - 1Document55 pagesAccounting Notes - 1Rahim MashaalNo ratings yet

- What Is The Difference Between Rent Receivable and Rent PayableDocument3 pagesWhat Is The Difference Between Rent Receivable and Rent PayableMa. Angela GarciaNo ratings yet

- Accounting Notes: Double Entry BookkeepingDocument19 pagesAccounting Notes: Double Entry Bookkeepingkashmala HussainNo ratings yet

- Accounting BasicsDocument13 pagesAccounting BasicskameshpatilNo ratings yet

- Static 1Document16 pagesStatic 1Anurag SinghNo ratings yet

- Balance Sheet Dimasaka & JaranillaDocument56 pagesBalance Sheet Dimasaka & JaranillaShaneBattierNo ratings yet

- Rules of Debits and CreditsDocument6 pagesRules of Debits and CreditsJubelle Tacusalme Punzalan100% (1)

- 5.2. Specific ArrangementsDocument51 pages5.2. Specific ArrangementsPranjal pandeyNo ratings yet

- Module 4 - Financial Statement Analysis Lecture S23Document25 pagesModule 4 - Financial Statement Analysis Lecture S23Prachi YadavNo ratings yet

- Engineering EconomicsDocument12 pagesEngineering EconomicsAwais SiddiqueNo ratings yet

- Chapter 3 - Accounting Cycle For Service EnterpriseDocument22 pagesChapter 3 - Accounting Cycle For Service EnterpriseAnimaw YayehNo ratings yet

- Chapter Two: Accounting Cycle For Service-Giving BusinessDocument35 pagesChapter Two: Accounting Cycle For Service-Giving BusinessMathewos Woldemariam Birru100% (2)

- Financial Accounting NotesDocument14 pagesFinancial Accounting NotesLex XuNo ratings yet

- Introduction to Balance Sheet: Fulfilled: student of the AБ-71-8a group V.V. Radko Checked: Z. A. OleksichDocument14 pagesIntroduction to Balance Sheet: Fulfilled: student of the AБ-71-8a group V.V. Radko Checked: Z. A. OleksichРадько Вікторія ВікторівнаNo ratings yet

- Statement of Financial Position (SFP) : Lesson 1Document29 pagesStatement of Financial Position (SFP) : Lesson 1Dianne Saragena100% (1)

- Account PaperDocument12 pagesAccount PaperVinit RanaNo ratings yet

- Accounting For Managers: Basics of Business Accounting (Learner Friendly Approach)Document45 pagesAccounting For Managers: Basics of Business Accounting (Learner Friendly Approach)Sasi Kesanasetty KiranNo ratings yet

- ACC - ACF1200 Topic 3 SOLUTIONS To Questions For Self-StudyDocument3 pagesACC - ACF1200 Topic 3 SOLUTIONS To Questions For Self-StudyChuangjia MaNo ratings yet

- Financial Accounting & AnalysisDocument7 pagesFinancial Accounting & Analysisneha bakshiNo ratings yet

- Balance Sheets: Assets: Assets Are Subdivided Into Current and Long-TermDocument6 pagesBalance Sheets: Assets: Assets Are Subdivided Into Current and Long-TermPhướcHàNo ratings yet

- The Balance SheetDocument7 pagesThe Balance Sheetsevirous valeriaNo ratings yet

- Balance Sheet: PositionDocument4 pagesBalance Sheet: PositionRavi SunNo ratings yet

- 1 LectureDocument42 pages1 LectureVall HallaNo ratings yet

- Fundamentals of AccountingDocument29 pagesFundamentals of AccountingManoj BhogaleNo ratings yet

- Unit 3-Recording of TransactionDocument20 pagesUnit 3-Recording of Transactionanamikarajendran441998No ratings yet

- Unit 2 Financial Statement AnalysisDocument17 pagesUnit 2 Financial Statement AnalysisalemayehuNo ratings yet

- Accounting Principles: (Cheat Sheet)Document4 pagesAccounting Principles: (Cheat Sheet)Bony ThomasNo ratings yet

- Statement of Financial PositionDocument8 pagesStatement of Financial PositionKaye LiwagNo ratings yet

- Bookkeeping ConceptsDocument6 pagesBookkeeping ConceptsJagiNo ratings yet

- Financial Accounting 2Document31 pagesFinancial Accounting 2Umurbey GençNo ratings yet

- Lec 6 AFM Fin Statement AnalDocument44 pagesLec 6 AFM Fin Statement AnalHaroon Rashid100% (1)

- Chap 1 Principle AccountingDocument33 pagesChap 1 Principle Accountingnajkoz yaruNo ratings yet

- Sample of Asset-Office Land, Equiptment, Cash, MachinesDocument29 pagesSample of Asset-Office Land, Equiptment, Cash, MachinesMaria Cludet NayveNo ratings yet

- Questions and Answers RatiosDocument14 pagesQuestions and Answers RatiosBalujagadishNo ratings yet

- Topic Two: Recording Business Transactions: Case One: Owner Supplying All The ResourcesDocument15 pagesTopic Two: Recording Business Transactions: Case One: Owner Supplying All The ResourcesZAKAYO NJONYNo ratings yet

- FIN 201 Chapter 02Document27 pagesFIN 201 Chapter 02ImraanHossainAyaanNo ratings yet

- Chapter 2Document31 pagesChapter 2abenezer nardiyasNo ratings yet

- Chaptertwo Hand OutDocument28 pagesChaptertwo Hand OutAnteneh YitbarekNo ratings yet

- Balance SheetDocument6 pagesBalance Sheetddoc.mimiNo ratings yet

- FINANCIAL ACCOUNTING - AsbDocument9 pagesFINANCIAL ACCOUNTING - AsbMuskaanNo ratings yet

- Adjusting Entries PDFDocument6 pagesAdjusting Entries PDFJan ryanNo ratings yet

- GuidetoBookkeepingConcepts PDFDocument18 pagesGuidetoBookkeepingConcepts PDFSarah HlordjiNo ratings yet

- Business Accounting: Muhammad TariqDocument24 pagesBusiness Accounting: Muhammad Tariqsameed mateenNo ratings yet

- An Overview On Financial Statements and Ratio AnalysisDocument10 pagesAn Overview On Financial Statements and Ratio AnalysissachinoilNo ratings yet

- Accounting: Ankon Gopal BanikDocument9 pagesAccounting: Ankon Gopal BanikAnkon Gopal BanikNo ratings yet

- Keeping ConceptsDocument5 pagesKeeping ConceptsJagiNo ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Lecture 5Document49 pagesLecture 5premsuwaatiiNo ratings yet

- Fin Stat Ilustrasi, PT Indonesia 2016Document173 pagesFin Stat Ilustrasi, PT Indonesia 2016CorneliusNo ratings yet

- Teknosa 4 QengDocument15 pagesTeknosa 4 QengFaIIen0nENo ratings yet

- 04 Ias 38 PDFDocument40 pages04 Ias 38 PDFnida younasNo ratings yet

- Week 4 Practice Questions 1Document17 pagesWeek 4 Practice Questions 1Gabriel Abdillah100% (1)

- T8 Homework Solutions-1Document15 pagesT8 Homework Solutions-1Anathi AnathiNo ratings yet

- Accountancy 2023-24 MSDocument11 pagesAccountancy 2023-24 MSirfanoushad15No ratings yet

- An Overview of Financial Management: LessonDocument6 pagesAn Overview of Financial Management: LessonKliennt TorrejosNo ratings yet

- Finance Process Flow in JDEDocument35 pagesFinance Process Flow in JDERamesh KumarNo ratings yet

- Sessions 8 - 9 - BS - SentDocument11 pagesSessions 8 - 9 - BS - SentAjay DesaleNo ratings yet

- FAR Final Preboard QuestionaireDocument18 pagesFAR Final Preboard Questionaireyzhlansang.studentNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument12 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionErwin Labayog MedinaNo ratings yet

- Initiating Coverage Report - TVS Motor Company LTDDocument14 pagesInitiating Coverage Report - TVS Motor Company LTDshreya2626No ratings yet

- SGV Cup Level 2Document6 pagesSGV Cup Level 2Nicolette DonovanNo ratings yet

- Period Close Exceptions Report 310323Document49 pagesPeriod Close Exceptions Report 310323mshadabalamNo ratings yet

- Chapter 07 - Intercompany Inventory TransactionsDocument38 pagesChapter 07 - Intercompany Inventory Transactions_casals100% (8)

- Excel - PPT Big 3 Performance Q2'23 - 31 July 2023Document18 pagesExcel - PPT Big 3 Performance Q2'23 - 31 July 2023Roby SatriyaNo ratings yet

- Practical ExerciseDocument9 pagesPractical Exercisesharini subramaniamNo ratings yet

- Annual Report PTCLDocument4 pagesAnnual Report PTCLuzair212No ratings yet

- Test Bank For Financial Accounting Reporting Analysis and Decision Making 6th Edition Shirley Carlon Rosina Mcalpine Chrisann Lee Lorena Mitrione Ngaire Kirk Lily WongDocument36 pagesTest Bank For Financial Accounting Reporting Analysis and Decision Making 6th Edition Shirley Carlon Rosina Mcalpine Chrisann Lee Lorena Mitrione Ngaire Kirk Lily Wongtiffanybuckdtoexpmnbz100% (23)

- Financial Accounts Assingnment 3Document5 pagesFinancial Accounts Assingnment 3Zakarya KhanNo ratings yet

- Factsheet AMRT 2023 01Document4 pagesFactsheet AMRT 2023 01arsyil1453No ratings yet

- Analysis of Financial StatementsDocument16 pagesAnalysis of Financial StatementsAlok ThakurNo ratings yet

- Chapter 15: Single Entry Characteristics of Single EntryDocument12 pagesChapter 15: Single Entry Characteristics of Single EntryPaula Bautista100% (2)

- Key Uni 1 Activities Lessons 2 3Document20 pagesKey Uni 1 Activities Lessons 2 3Leslie Mae Vargas ZafeNo ratings yet

- Practice Test: Career AvenuesDocument10 pagesPractice Test: Career AvenuesEthan GomesNo ratings yet

- Peanut Butter Fantasies Exhibit DataDocument25 pagesPeanut Butter Fantasies Exhibit DataGonz�lez Alonzo Juan ManuelNo ratings yet

- Chapter 3 The Accounting CycleDocument68 pagesChapter 3 The Accounting CycleChala EnkossaNo ratings yet

Download as pdf or txt

You might also like

- Answer Key - Chapter 6 - ACCOUNTINGDocument92 pagesAnswer Key - Chapter 6 - ACCOUNTINGIL MareNo ratings yet

- Fundamentals of Accountancy, Business, and Management 2: ExpectationDocument131 pagesFundamentals of Accountancy, Business, and Management 2: ExpectationAngela Garcia100% (1)

- Chapter-2 Accounting CycleDocument18 pagesChapter-2 Accounting CycleTsegaye BelayNo ratings yet

- Chapter 2Document24 pagesChapter 2Lleiram Bulotano Bolanio25% (4)

- MGMT 026 Connect Chapter 3 Homework HQ PDFDocument28 pagesMGMT 026 Connect Chapter 3 Homework HQ PDFKailash KumarNo ratings yet

- Introduction To Balance SheetDocument10 pagesIntroduction To Balance SheetJodie Ann PajacNo ratings yet

- Apoyo 1.. - InglesDocument5 pagesApoyo 1.. - InglesWilder ManceraNo ratings yet

- Since A Long Time AgoDocument5 pagesSince A Long Time AgoPatrisia CibisovNo ratings yet

- Fundamentals Ofabm2: Gerlie D. BorneaDocument53 pagesFundamentals Ofabm2: Gerlie D. BorneaGerlie BorneaNo ratings yet

- Unit 3 Cost Estimation and Annual ReportsDocument35 pagesUnit 3 Cost Estimation and Annual ReportsRamakrishna ReddyNo ratings yet

- Chapter 2Document21 pagesChapter 2Kibrom EmbzaNo ratings yet

- Name: Giovanni Oliveria. Opog 12-VenusDocument7 pagesName: Giovanni Oliveria. Opog 12-VenusbannieopogNo ratings yet

- Accounting Elements in The Statement of Financial PositionDocument4 pagesAccounting Elements in The Statement of Financial PositionBianca Jane GaayonNo ratings yet

- Csec Poa Handout 3Document32 pagesCsec Poa Handout 3Taariq Abdul-MajeedNo ratings yet

- Accounting Notes - 1Document55 pagesAccounting Notes - 1Rahim MashaalNo ratings yet

- What Is The Difference Between Rent Receivable and Rent PayableDocument3 pagesWhat Is The Difference Between Rent Receivable and Rent PayableMa. Angela GarciaNo ratings yet

- Accounting Notes: Double Entry BookkeepingDocument19 pagesAccounting Notes: Double Entry Bookkeepingkashmala HussainNo ratings yet

- Accounting BasicsDocument13 pagesAccounting BasicskameshpatilNo ratings yet

- Static 1Document16 pagesStatic 1Anurag SinghNo ratings yet

- Balance Sheet Dimasaka & JaranillaDocument56 pagesBalance Sheet Dimasaka & JaranillaShaneBattierNo ratings yet

- Rules of Debits and CreditsDocument6 pagesRules of Debits and CreditsJubelle Tacusalme Punzalan100% (1)

- 5.2. Specific ArrangementsDocument51 pages5.2. Specific ArrangementsPranjal pandeyNo ratings yet

- Module 4 - Financial Statement Analysis Lecture S23Document25 pagesModule 4 - Financial Statement Analysis Lecture S23Prachi YadavNo ratings yet

- Engineering EconomicsDocument12 pagesEngineering EconomicsAwais SiddiqueNo ratings yet

- Chapter 3 - Accounting Cycle For Service EnterpriseDocument22 pagesChapter 3 - Accounting Cycle For Service EnterpriseAnimaw YayehNo ratings yet

- Chapter Two: Accounting Cycle For Service-Giving BusinessDocument35 pagesChapter Two: Accounting Cycle For Service-Giving BusinessMathewos Woldemariam Birru100% (2)

- Financial Accounting NotesDocument14 pagesFinancial Accounting NotesLex XuNo ratings yet

- Introduction to Balance Sheet: Fulfilled: student of the AБ-71-8a group V.V. Radko Checked: Z. A. OleksichDocument14 pagesIntroduction to Balance Sheet: Fulfilled: student of the AБ-71-8a group V.V. Radko Checked: Z. A. OleksichРадько Вікторія ВікторівнаNo ratings yet

- Statement of Financial Position (SFP) : Lesson 1Document29 pagesStatement of Financial Position (SFP) : Lesson 1Dianne Saragena100% (1)

- Account PaperDocument12 pagesAccount PaperVinit RanaNo ratings yet

- Accounting For Managers: Basics of Business Accounting (Learner Friendly Approach)Document45 pagesAccounting For Managers: Basics of Business Accounting (Learner Friendly Approach)Sasi Kesanasetty KiranNo ratings yet

- ACC - ACF1200 Topic 3 SOLUTIONS To Questions For Self-StudyDocument3 pagesACC - ACF1200 Topic 3 SOLUTIONS To Questions For Self-StudyChuangjia MaNo ratings yet

- Financial Accounting & AnalysisDocument7 pagesFinancial Accounting & Analysisneha bakshiNo ratings yet

- Balance Sheets: Assets: Assets Are Subdivided Into Current and Long-TermDocument6 pagesBalance Sheets: Assets: Assets Are Subdivided Into Current and Long-TermPhướcHàNo ratings yet

- The Balance SheetDocument7 pagesThe Balance Sheetsevirous valeriaNo ratings yet

- Balance Sheet: PositionDocument4 pagesBalance Sheet: PositionRavi SunNo ratings yet

- 1 LectureDocument42 pages1 LectureVall HallaNo ratings yet

- Fundamentals of AccountingDocument29 pagesFundamentals of AccountingManoj BhogaleNo ratings yet

- Unit 3-Recording of TransactionDocument20 pagesUnit 3-Recording of Transactionanamikarajendran441998No ratings yet

- Unit 2 Financial Statement AnalysisDocument17 pagesUnit 2 Financial Statement AnalysisalemayehuNo ratings yet

- Accounting Principles: (Cheat Sheet)Document4 pagesAccounting Principles: (Cheat Sheet)Bony ThomasNo ratings yet

- Statement of Financial PositionDocument8 pagesStatement of Financial PositionKaye LiwagNo ratings yet

- Bookkeeping ConceptsDocument6 pagesBookkeeping ConceptsJagiNo ratings yet

- Financial Accounting 2Document31 pagesFinancial Accounting 2Umurbey GençNo ratings yet

- Lec 6 AFM Fin Statement AnalDocument44 pagesLec 6 AFM Fin Statement AnalHaroon Rashid100% (1)

- Chap 1 Principle AccountingDocument33 pagesChap 1 Principle Accountingnajkoz yaruNo ratings yet

- Sample of Asset-Office Land, Equiptment, Cash, MachinesDocument29 pagesSample of Asset-Office Land, Equiptment, Cash, MachinesMaria Cludet NayveNo ratings yet

- Questions and Answers RatiosDocument14 pagesQuestions and Answers RatiosBalujagadishNo ratings yet

- Topic Two: Recording Business Transactions: Case One: Owner Supplying All The ResourcesDocument15 pagesTopic Two: Recording Business Transactions: Case One: Owner Supplying All The ResourcesZAKAYO NJONYNo ratings yet

- FIN 201 Chapter 02Document27 pagesFIN 201 Chapter 02ImraanHossainAyaanNo ratings yet

- Chapter 2Document31 pagesChapter 2abenezer nardiyasNo ratings yet

- Chaptertwo Hand OutDocument28 pagesChaptertwo Hand OutAnteneh YitbarekNo ratings yet

- Balance SheetDocument6 pagesBalance Sheetddoc.mimiNo ratings yet

- FINANCIAL ACCOUNTING - AsbDocument9 pagesFINANCIAL ACCOUNTING - AsbMuskaanNo ratings yet

- Adjusting Entries PDFDocument6 pagesAdjusting Entries PDFJan ryanNo ratings yet

- GuidetoBookkeepingConcepts PDFDocument18 pagesGuidetoBookkeepingConcepts PDFSarah HlordjiNo ratings yet

- Business Accounting: Muhammad TariqDocument24 pagesBusiness Accounting: Muhammad Tariqsameed mateenNo ratings yet

- An Overview On Financial Statements and Ratio AnalysisDocument10 pagesAn Overview On Financial Statements and Ratio AnalysissachinoilNo ratings yet

- Accounting: Ankon Gopal BanikDocument9 pagesAccounting: Ankon Gopal BanikAnkon Gopal BanikNo ratings yet

- Keeping ConceptsDocument5 pagesKeeping ConceptsJagiNo ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Lecture 5Document49 pagesLecture 5premsuwaatiiNo ratings yet

- Fin Stat Ilustrasi, PT Indonesia 2016Document173 pagesFin Stat Ilustrasi, PT Indonesia 2016CorneliusNo ratings yet

- Teknosa 4 QengDocument15 pagesTeknosa 4 QengFaIIen0nENo ratings yet

- 04 Ias 38 PDFDocument40 pages04 Ias 38 PDFnida younasNo ratings yet

- Week 4 Practice Questions 1Document17 pagesWeek 4 Practice Questions 1Gabriel Abdillah100% (1)

- T8 Homework Solutions-1Document15 pagesT8 Homework Solutions-1Anathi AnathiNo ratings yet

- Accountancy 2023-24 MSDocument11 pagesAccountancy 2023-24 MSirfanoushad15No ratings yet

- An Overview of Financial Management: LessonDocument6 pagesAn Overview of Financial Management: LessonKliennt TorrejosNo ratings yet

- Finance Process Flow in JDEDocument35 pagesFinance Process Flow in JDERamesh KumarNo ratings yet

- Sessions 8 - 9 - BS - SentDocument11 pagesSessions 8 - 9 - BS - SentAjay DesaleNo ratings yet

- FAR Final Preboard QuestionaireDocument18 pagesFAR Final Preboard Questionaireyzhlansang.studentNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument12 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionErwin Labayog MedinaNo ratings yet

- Initiating Coverage Report - TVS Motor Company LTDDocument14 pagesInitiating Coverage Report - TVS Motor Company LTDshreya2626No ratings yet

- SGV Cup Level 2Document6 pagesSGV Cup Level 2Nicolette DonovanNo ratings yet

- Period Close Exceptions Report 310323Document49 pagesPeriod Close Exceptions Report 310323mshadabalamNo ratings yet

- Chapter 07 - Intercompany Inventory TransactionsDocument38 pagesChapter 07 - Intercompany Inventory Transactions_casals100% (8)

- Excel - PPT Big 3 Performance Q2'23 - 31 July 2023Document18 pagesExcel - PPT Big 3 Performance Q2'23 - 31 July 2023Roby SatriyaNo ratings yet

- Practical ExerciseDocument9 pagesPractical Exercisesharini subramaniamNo ratings yet

- Annual Report PTCLDocument4 pagesAnnual Report PTCLuzair212No ratings yet

- Test Bank For Financial Accounting Reporting Analysis and Decision Making 6th Edition Shirley Carlon Rosina Mcalpine Chrisann Lee Lorena Mitrione Ngaire Kirk Lily WongDocument36 pagesTest Bank For Financial Accounting Reporting Analysis and Decision Making 6th Edition Shirley Carlon Rosina Mcalpine Chrisann Lee Lorena Mitrione Ngaire Kirk Lily Wongtiffanybuckdtoexpmnbz100% (23)

- Financial Accounts Assingnment 3Document5 pagesFinancial Accounts Assingnment 3Zakarya KhanNo ratings yet

- Factsheet AMRT 2023 01Document4 pagesFactsheet AMRT 2023 01arsyil1453No ratings yet

- Analysis of Financial StatementsDocument16 pagesAnalysis of Financial StatementsAlok ThakurNo ratings yet

- Chapter 15: Single Entry Characteristics of Single EntryDocument12 pagesChapter 15: Single Entry Characteristics of Single EntryPaula Bautista100% (2)

- Key Uni 1 Activities Lessons 2 3Document20 pagesKey Uni 1 Activities Lessons 2 3Leslie Mae Vargas ZafeNo ratings yet

- Practice Test: Career AvenuesDocument10 pagesPractice Test: Career AvenuesEthan GomesNo ratings yet

- Peanut Butter Fantasies Exhibit DataDocument25 pagesPeanut Butter Fantasies Exhibit DataGonz�lez Alonzo Juan ManuelNo ratings yet

- Chapter 3 The Accounting CycleDocument68 pagesChapter 3 The Accounting CycleChala EnkossaNo ratings yet