Download as docx, pdf, or txt

You might also like

- Tiger Global BrochureDocument27 pagesTiger Global Brochureanandoiyer9100% (2)

- CH13 Balance Sheet 12.31.26Document4 pagesCH13 Balance Sheet 12.31.26Crystal TelaNo ratings yet

- Credit Rating To Customers in Commercial Banks: Rationality and IssuesDocument40 pagesCredit Rating To Customers in Commercial Banks: Rationality and IssuesMaiChi PhamNo ratings yet

- FinQuiz - Smart Summary - Study Session 16 - Reading 56Document7 pagesFinQuiz - Smart Summary - Study Session 16 - Reading 56Rafael100% (1)

- Chapter 6 Valuation and Characteristics of BondsDocument30 pagesChapter 6 Valuation and Characteristics of BondsKiran AishaNo ratings yet

- Introduction To Credit Risk AnalysisDocument39 pagesIntroduction To Credit Risk AnalysisHitesh Kalwani100% (2)

- Distressed Debt PrezDocument32 pagesDistressed Debt Prezmacondo06100% (2)

- Nilu Kumari (490-E)Document10 pagesNilu Kumari (490-E)krinilu802No ratings yet

- Liquidity Risk in BondsDocument3 pagesLiquidity Risk in BondsAanchal MahajanNo ratings yet

- Credit Rating: Submitted By: Group 5 TH Roll No. 6144, 6145, 6136,6141,6104Document26 pagesCredit Rating: Submitted By: Group 5 TH Roll No. 6144, 6145, 6136,6141,6104sukhjeetkaur35No ratings yet

- Credit Rating AgenciesDocument40 pagesCredit Rating AgenciesSmriti DurehaNo ratings yet

- Credit Risk 5Document34 pagesCredit Risk 5tahatalmaccNo ratings yet

- Corporate Governance: By: 1. Kenneth A. Kim John R. Nofsinger and 2. A. C. FernandoDocument28 pagesCorporate Governance: By: 1. Kenneth A. Kim John R. Nofsinger and 2. A. C. FernandoMaryam MalikNo ratings yet

- FI - Reading 44 - Fundamentals of Credit AnalysisDocument42 pagesFI - Reading 44 - Fundamentals of Credit Analysisshaili shahNo ratings yet

- Definition of Credit RiskDocument5 pagesDefinition of Credit RiskraviNo ratings yet

- CFA Level 1 FundamentalsDocument5 pagesCFA Level 1 Fundamentalskazimeister1No ratings yet

- Credit RatingDocument50 pagesCredit Ratingmaruf_tanmimNo ratings yet

- Module 5 - Credit Rating and Securitization of Debts2Document15 pagesModule 5 - Credit Rating and Securitization of Debts2welcome2jungleNo ratings yet

- AnalysisDocument12 pagesAnalysisShaik NisarNo ratings yet

- Chapter 6 - Fundamentals of Credit AnalysisDocument86 pagesChapter 6 - Fundamentals of Credit Analysisybpdwjg5brNo ratings yet

- General Principal of Credit Rating-1Document35 pagesGeneral Principal of Credit Rating-1Nazir Ahmed ZihadNo ratings yet

- Credit RiskDocument37 pagesCredit RiskWakas KhalidNo ratings yet

- Summary - Financial Markets and InstitutionsDocument20 pagesSummary - Financial Markets and Institutionswzq0308chnNo ratings yet

- General Principal of Credit Rating-1 - AaDocument23 pagesGeneral Principal of Credit Rating-1 - AaNazir Ahmed ZihadNo ratings yet

- Lecture 7 Topic 4 Credit Market Failures - BbslidesDocument50 pagesLecture 7 Topic 4 Credit Market Failures - Bbslidessamyyamalik1701No ratings yet

- 2021 Level I SS15-Fundamentals of Credit AnalysisDocument12 pages2021 Level I SS15-Fundamentals of Credit AnalysisRyan DiedricksNo ratings yet

- Credit RiskDocument18 pagesCredit Riskyoshiharu.harano1726No ratings yet

- Management of Risk-1Document22 pagesManagement of Risk-1Abhishek sonkarNo ratings yet

- Credit Rating Finance AssignmentDocument6 pagesCredit Rating Finance Assignmentrashikhsitesholder4607No ratings yet

- Credit Rating: Made By: Megha Aggarwal Diksha Mantry Kunal GoyalDocument21 pagesCredit Rating: Made By: Megha Aggarwal Diksha Mantry Kunal GoyalKafonyi JohnNo ratings yet

- Credit Rating IBDocument10 pagesCredit Rating IBKIng KumarNo ratings yet

- The Features of Long Term DebtsDocument56 pagesThe Features of Long Term DebtsMicah Ramayka100% (3)

- Credit Ratings 1Document296 pagesCredit Ratings 1Harsh KhatriNo ratings yet

- 10 Risk Management Credit Rating Agencies PDFDocument7 pages10 Risk Management Credit Rating Agencies PDFEmanuela Alexandra SavinNo ratings yet

- Credit RatingDocument48 pagesCredit RatingChinmayee ChoudhuryNo ratings yet

- A Study On What Is A Good Credit Rate.: ObjectivesDocument4 pagesA Study On What Is A Good Credit Rate.: ObjectivesSandeep GuptaNo ratings yet

- Guide To Credit Rating Essentials DigitalDocument16 pagesGuide To Credit Rating Essentials DigitalJerico ConsultoriaNo ratings yet

- Credit RatingDocument4 pagesCredit RatingAbhisek ShawNo ratings yet

- Credit Risk ManagementDocument5 pagesCredit Risk Managementzaheer shahzadNo ratings yet

- AFM Notes 2.2Document9 pagesAFM Notes 2.2ubaid.officialNo ratings yet

- What Is A Credit RatingDocument16 pagesWhat Is A Credit RatingashiqstrongNo ratings yet

- Credit Rating: Fees Structure FEE Structure Initial Rating FeesDocument6 pagesCredit Rating: Fees Structure FEE Structure Initial Rating FeesWindowFashionNo ratings yet

- Procedures For AppraisalDocument8 pagesProcedures For AppraisalsairamNo ratings yet

- Benefits of Credit RatingDocument4 pagesBenefits of Credit RatingJohn WickNo ratings yet

- Chapter - 12 Credit Rating AgenciesDocument13 pagesChapter - 12 Credit Rating AgenciesMehak 731No ratings yet

- Ufi M 5Document25 pagesUfi M 5sresthapatel28No ratings yet

- What Is Credit Analysis?: Credit Risk Default Risk Bonds Stocks Loans Credit Analyst CertificationDocument6 pagesWhat Is Credit Analysis?: Credit Risk Default Risk Bonds Stocks Loans Credit Analyst CertificationselvarajsathiyaNo ratings yet

- Debt V/s Equity FinancingDocument5 pagesDebt V/s Equity FinancingArjit KumarNo ratings yet

- Bond RatingsDocument2 pagesBond RatingscciesaadNo ratings yet

- Credit Rating: Need, Process and LimitationsDocument24 pagesCredit Rating: Need, Process and LimitationsRupam Aryan BorahNo ratings yet

- Lesson 1 CREDIT - Credit and CollectionDocument4 pagesLesson 1 CREDIT - Credit and CollectionAngela MagtibayNo ratings yet

- Chapter 1Document4 pagesChapter 1sinchanaNo ratings yet

- Definition, Types and Scales of Credit RatingDocument8 pagesDefinition, Types and Scales of Credit Ratingjannatul ferthousNo ratings yet

- Bond Rating ProcessDocument15 pagesBond Rating ProcessKapil SharmaNo ratings yet

- Topic 3 - Credit RiskDocument51 pagesTopic 3 - Credit RiskSandra YebyoNo ratings yet

- 1.5 Provisions BasicsDocument5 pages1.5 Provisions Basicskik leeNo ratings yet

- Credit RatingDocument8 pagesCredit Ratingpatelchhotupatel8No ratings yet

- Credit Rating: Need, Process and LimitationsDocument24 pagesCredit Rating: Need, Process and LimitationsRupam Aryan BorahNo ratings yet

- Presented By: Rajesh Sandhya Santhosh Abhishek DamyantiDocument11 pagesPresented By: Rajesh Sandhya Santhosh Abhishek DamyantiDamyanti ShawNo ratings yet

- Monetery Policy and BankingDocument8 pagesMonetery Policy and Banking17FB049 Mokter HasanNo ratings yet

- Credit Rating ServicesDocument5 pagesCredit Rating ServicesNithi NithiNo ratings yet

- Credit MGT TraineesDocument20 pagesCredit MGT TraineesTewodros2014No ratings yet

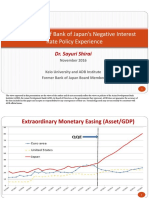

- An Overview of Bank of Japan Negative Interest Rate Policy ExperienceDocument12 pagesAn Overview of Bank of Japan Negative Interest Rate Policy ExperienceADBI Events100% (1)

- Chapter - 01 Introduction of BankDocument37 pagesChapter - 01 Introduction of BankJeeva JeevaNo ratings yet

- StrategyNote 20180209 WhatHappened XIV SVXYDocument4 pagesStrategyNote 20180209 WhatHappened XIV SVXYchris mbaNo ratings yet

- Framework of Islamic Financial SystemDocument31 pagesFramework of Islamic Financial SystemMahyuddin KhalidNo ratings yet

- Bank Reconcilation Knowledge Aptitude TestDocument4 pagesBank Reconcilation Knowledge Aptitude TestBirender SinghNo ratings yet

- Anexo 3 - C4. Economista Carlos MarxDocument4 pagesAnexo 3 - C4. Economista Carlos MarxDario CarrilloNo ratings yet

- Interest RatesDocument207 pagesInterest RatesBenjamin RogersNo ratings yet

- Practical Finance Guide: By: NicholasDocument38 pagesPractical Finance Guide: By: NicholasFx Rafael NicholasNo ratings yet

- Question Bank (Accounting Problems)Document11 pagesQuestion Bank (Accounting Problems)Abhishek MohantyNo ratings yet

- Lesson 8 Trading ProcessDocument20 pagesLesson 8 Trading ProcessRica joy TahumNo ratings yet

- Ogdcl PDFDocument2 pagesOgdcl PDFnomi9818No ratings yet

- Table Showing Current Ratio: List of TablesDocument37 pagesTable Showing Current Ratio: List of TablesMano ManiNo ratings yet

- Accounting Principles, 9th Edition OUTLINESDocument7 pagesAccounting Principles, 9th Edition OUTLINESAsghar AliNo ratings yet

- Account - Statement - 011022 - 311022Document17 pagesAccount - Statement - 011022 - 311022Rohit KumarNo ratings yet

- 05 GL Head ReportSultanpur Lodhi PADB19082019021855PMDocument15 pages05 GL Head ReportSultanpur Lodhi PADB19082019021855PMsandeepNo ratings yet

- Chapter - Working CapitalDocument35 pagesChapter - Working CapitalchandoraNo ratings yet

- Lecture 1 - 2Document70 pagesLecture 1 - 2premsuwaatiiNo ratings yet

- Chapter 16 Cash FlowsDocument4 pagesChapter 16 Cash Flowsjou20220354No ratings yet

- About Return: What Is Return in Finance?Document10 pagesAbout Return: What Is Return in Finance?Mudit GuptaNo ratings yet

- Investment Management & Trading Courses - Canadian Securities InstituteDocument2 pagesInvestment Management & Trading Courses - Canadian Securities InstituteRamsinghNo ratings yet

- Kelayakan Investasi (Invesment Feasibility) Pembangunan Pasar Tradisional Rukoh Barona Kota Banda AcehDocument7 pagesKelayakan Investasi (Invesment Feasibility) Pembangunan Pasar Tradisional Rukoh Barona Kota Banda AcehBianNo ratings yet

- "Financial Analysis of HDFC Bank": Symbiosis Centre For Distance Learning, PuneDocument69 pages"Financial Analysis of HDFC Bank": Symbiosis Centre For Distance Learning, PuneBheeshm Singh100% (1)

- FDNACCT - Quiz #2 - Problem Solving - Solutions-2Document4 pagesFDNACCT - Quiz #2 - Problem Solving - Solutions-2Ichi HasukiNo ratings yet

- CitibankDocument11 pagesCitibankAdab MediaNo ratings yet

- Investment in Stock Market NotesDocument11 pagesInvestment in Stock Market Notesappuzzz2000zzzzNo ratings yet

- 2468 - EstimDocument2 pages2468 - EstimTariq MahmoodNo ratings yet

- GetNotice AspxDocument2 pagesGetNotice Aspxmaria matundaNo ratings yet