Download as pdf or txt

You might also like

- Company's Ability To Produce Chips That Meet Specifications? The Elements That TheDocument4 pagesCompany's Ability To Produce Chips That Meet Specifications? The Elements That TheMikey MadRatNo ratings yet

- Guth and Ginsberg 1990Document12 pagesGuth and Ginsberg 1990Fazrul Azry100% (1)

- Ex 1B PG 17Document2 pagesEx 1B PG 17Darlene BellesiaNo ratings yet

- Responsible Restructuring: Creative and Profitable Alternatives to LayoffsFrom EverandResponsible Restructuring: Creative and Profitable Alternatives to LayoffsNo ratings yet

- Ambidextrous Strategies and Innovation PDFDocument9 pagesAmbidextrous Strategies and Innovation PDFLeidy SánchezNo ratings yet

- Ch7 Sampling Distribution - Suggested Problems SolutionsDocument8 pagesCh7 Sampling Distribution - Suggested Problems Solutionsmaxentiuss100% (1)

- Design of Packed Bed Reactor Catalyst Based On Shape Size PDFDocument14 pagesDesign of Packed Bed Reactor Catalyst Based On Shape Size PDFArbaz AKNo ratings yet

- Chapter 08 Sampling Distributions and Estimation: Multiple Choice QuestionsDocument302 pagesChapter 08 Sampling Distributions and Estimation: Multiple Choice QuestionsTruc NguyenNo ratings yet

- Decision MakingDocument72 pagesDecision Makingmuwowo1100% (1)

- Budgetary SlackDocument19 pagesBudgetary SlackwinarsNo ratings yet

- Peteraf (1993) Tipos de Renta (20.05)Document14 pagesPeteraf (1993) Tipos de Renta (20.05)Angie ZuritaNo ratings yet

- SynergyDocument3 pagesSynergyJunior VeigaNo ratings yet

- Slack Resources and The Performance of Privately Held Firms: Gerard George University of Wisconsin-MadisonDocument17 pagesSlack Resources and The Performance of Privately Held Firms: Gerard George University of Wisconsin-MadisonWesley S. LourençoNo ratings yet

- Critical Competitive Strategies Every Entrepreneur Should ConsiderDocument11 pagesCritical Competitive Strategies Every Entrepreneur Should ConsiderrasanavaneethanNo ratings yet

- Deregulation, Misallocation, and Size Evidence From IndiaDocument50 pagesDeregulation, Misallocation, and Size Evidence From IndiaLarry BNo ratings yet

- Organizational Restructuring and Economic Performance in Leveraged Buyouts: An Ex Post StudyDocument37 pagesOrganizational Restructuring and Economic Performance in Leveraged Buyouts: An Ex Post StudyPriyanka SinghNo ratings yet

- Summary Corporate DiversificationDocument3 pagesSummary Corporate DiversificationVoip Kredisi0% (1)

- Worker Redeployment in Multi-Business FirmsDocument62 pagesWorker Redeployment in Multi-Business FirmsMarcosNo ratings yet

- Marketing The New VentureDocument2 pagesMarketing The New VentureSahira DamianoNo ratings yet

- The Dynamics of Diversification: Shayne GaryDocument20 pagesThe Dynamics of Diversification: Shayne GaryindrabudhiNo ratings yet

- Concepts of Synergy - Towards A Clarification: Working Paper For The DRUID-seminar January 1997Document12 pagesConcepts of Synergy - Towards A Clarification: Working Paper For The DRUID-seminar January 1997ChawkiTrabelsi100% (1)

- UWI, Mona: Densil A. WilliamsDocument18 pagesUWI, Mona: Densil A. WilliamsKolleen SerranoNo ratings yet

- Combined Influence of Absorptive Capacity and CorpDocument26 pagesCombined Influence of Absorptive Capacity and CorpFlorante De LeonNo ratings yet

- Effect of Best Management Practices On The Performance and Productivity of Small FirmsDocument17 pagesEffect of Best Management Practices On The Performance and Productivity of Small FirmsSaúl RojasNo ratings yet

- Quarterly Journal of EconomicsDocument53 pagesQuarterly Journal of EconomicsIAmDeivNo ratings yet

- Corporate Restructuring and Its Effect On Employee Morale and PerformanceDocument9 pagesCorporate Restructuring and Its Effect On Employee Morale and PerformanceAbhishek GuptaNo ratings yet

- Isitbettertobe Aggressiveor Conservativein Managing WCDocument12 pagesIsitbettertobe Aggressiveor Conservativein Managing WCMargarette LumaynoNo ratings yet

- Hart 15 YearsDocument16 pagesHart 15 YearsNguyen Thu Huong KDQTNo ratings yet

- Reviews by Macro EditorsDocument12 pagesReviews by Macro EditorsKchiey SshiNo ratings yet

- BEJ-10 Vol2010Document9 pagesBEJ-10 Vol2010Agung WicaksonoNo ratings yet

- Miles and Snow HR Strtegic ModelDocument3 pagesMiles and Snow HR Strtegic ModeltanyaNo ratings yet

- Benefits and Drawbacks of Innovation and Imitation: James M. BloodgoodDocument16 pagesBenefits and Drawbacks of Innovation and Imitation: James M. BloodgoodankNo ratings yet

- UC Berkeley Previously Published WorksDocument56 pagesUC Berkeley Previously Published WorksBhushi ShushiNo ratings yet

- Victoria University of Bangladesh: Anstotheqno-1Document12 pagesVictoria University of Bangladesh: Anstotheqno-1Md Shadat HossainNo ratings yet

- 06 The Emergence of World-Class Companies in ChileDocument8 pages06 The Emergence of World-Class Companies in ChileAnonymous vGOtuxeNo ratings yet

- Organisational AmbidexterityDocument9 pagesOrganisational AmbidexterityElena LostaunauNo ratings yet

- El Mehdi Dan Seboui (2011) Corporate - Diversification - and - Earnings - Management PDFDocument21 pagesEl Mehdi Dan Seboui (2011) Corporate - Diversification - and - Earnings - Management PDFrikky adiwijayaNo ratings yet

- Gschwantner - Hiebl (JoMaC, 2016) - Management Control Systems and Organizational AmbidexterityDocument35 pagesGschwantner - Hiebl (JoMaC, 2016) - Management Control Systems and Organizational AmbidexterityHemi Fradilla TariganNo ratings yet

- Eo BF Configurational JBVDocument21 pagesEo BF Configurational JBVrmyan0304No ratings yet

- Neil NagyDocument32 pagesNeil Nagymasyuki1979No ratings yet

- Downsizing in Indian Organisation Case Study On Boeing CompanyDocument25 pagesDownsizing in Indian Organisation Case Study On Boeing CompanyReHopNo ratings yet

- The Balancing of EmpowermentDocument15 pagesThe Balancing of EmpowermentRamon NarcizoNo ratings yet

- A Panel Data Analysis of Working Capital Management PoliciesDocument15 pagesA Panel Data Analysis of Working Capital Management PoliciesGizachewNo ratings yet

- Ntroduction: HY DO Mergers OR Acquisitions Take PlaceDocument8 pagesNtroduction: HY DO Mergers OR Acquisitions Take PlaceDechenDolkerNo ratings yet

- Economic and Social Significance of BudgetsDocument16 pagesEconomic and Social Significance of BudgetsAysel SalahovaNo ratings yet

- Sample Ques-Ans: (Short Answers) Ans A. Entrepreneur vs. InventorDocument31 pagesSample Ques-Ans: (Short Answers) Ans A. Entrepreneur vs. InventorSayantan BhattacharyaNo ratings yet

- The Relationship Between Working Capital Managementand Profitability Article PublishedDocument10 pagesThe Relationship Between Working Capital Managementand Profitability Article PublishedmannyNo ratings yet

- Andries Et Al 2013 - Simultaneous Experimentation As A Learning Strategy Business Model Development Under Uncertainty PDFDocument23 pagesAndries Et Al 2013 - Simultaneous Experimentation As A Learning Strategy Business Model Development Under Uncertainty PDFIZAZ NAHANo ratings yet

- Eat or Be EatenDocument85 pagesEat or Be EatenMarieta VanceaNo ratings yet

- 2014 03 3020141847wernerfelt - 1984Document11 pages2014 03 3020141847wernerfelt - 1984Miriam Olivares TorresNo ratings yet

- Employment ContractsDocument19 pagesEmployment ContractssujitsekharmoharanaigitNo ratings yet

- Final Project Rashid AliDocument72 pagesFinal Project Rashid AliSyed Zaheer Abbas KazmiNo ratings yet

- AppendixDocument4 pagesAppendixJayanga JayathungaNo ratings yet

- Contingent Pay PlanDocument4 pagesContingent Pay Plantallalbasahel100% (1)

- IntroductionDocument3 pagesIntroductionhaya.noor11200No ratings yet

- Read: Article - Consider This Article Written in The 1980s With Your Knowledge and Experience ofDocument5 pagesRead: Article - Consider This Article Written in The 1980s With Your Knowledge and Experience ofJude LarteyNo ratings yet

- 10 1109@itmc 2013 7352658Document14 pages10 1109@itmc 2013 7352658Wilson SCKUDLAREKNo ratings yet

- Why Do Firms Change?: RIDE/IMIT Working Paper No. 84426-015Document49 pagesWhy Do Firms Change?: RIDE/IMIT Working Paper No. 84426-015Uzair MayaNo ratings yet

- Khan & Naemullah FixDocument4 pagesKhan & Naemullah FixBudi ProNo ratings yet

- EIBA2023 - Track 2 - Competitive - The Controlled Morphing Process DCDocument12 pagesEIBA2023 - Track 2 - Competitive - The Controlled Morphing Process DCAlex MeraNo ratings yet

- Demsetz & Lehn 1985Document24 pagesDemsetz & Lehn 1985nicodimoana100% (1)

- Strategic Resource Management Is Explored Further by Cassia andDocument5 pagesStrategic Resource Management Is Explored Further by Cassia andKimberly JohnsonNo ratings yet

- BB31403Document4 pagesBB31403nadiaNo ratings yet

- BPM and PerformanceDocument12 pagesBPM and PerformanceGaribaldiNo ratings yet

- Competitive Analysis: Submitted To: Submitted By: Pooja Seth (UB2784596)Document12 pagesCompetitive Analysis: Submitted To: Submitted By: Pooja Seth (UB2784596)aaservices100% (1)

- Summary: Equity: Review and Analysis of Rosen, Case and Staubus' BookFrom EverandSummary: Equity: Review and Analysis of Rosen, Case and Staubus' BookNo ratings yet

- Chapter-5-slicing-dicing-ex-ante-Eden-LundDean-VaalerDocument9 pagesChapter-5-slicing-dicing-ex-ante-Eden-LundDean-VaalerRanjan DasguptaNo ratings yet

- Jet Airways 2015, ImprovementDocument1 pageJet Airways 2015, ImprovementRanjan DasguptaNo ratings yet

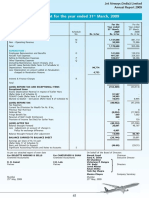

- Profit and Loss Account For The Year Ended 31 March, 2009: ST STDocument2 pagesProfit and Loss Account For The Year Ended 31 March, 2009: ST STRanjan DasguptaNo ratings yet

- Indas 2Document28 pagesIndas 2Ranjan DasguptaNo ratings yet

- Balance Sheet: As at March 31, 2017Document2 pagesBalance Sheet: As at March 31, 2017Ranjan DasguptaNo ratings yet

- Application Module 4 Lesson 3Document2 pagesApplication Module 4 Lesson 3Crysvenne Perez BisligNo ratings yet

- Mathematics: Engineering ©©©©©© Medical Work ©©©©©©©© Law ©© Science ©Document8 pagesMathematics: Engineering ©©©©©© Medical Work ©©©©©©©© Law ©© Science ©Jheanelle Andrea GodoyNo ratings yet

- Full Download Introduction To Statistics An Active Learning Approach 2nd Edition Carlson Test BankDocument35 pagesFull Download Introduction To Statistics An Active Learning Approach 2nd Edition Carlson Test Banklukec8kne100% (41)

- Anna University Applied Maths Question PaperDocument3 pagesAnna University Applied Maths Question Papernarayanan07No ratings yet

- 11 Appliedmaths SP 04Document15 pages11 Appliedmaths SP 04sagar JunejaNo ratings yet

- CHM 421 - ToPIC 3 - StatisticsDocument58 pagesCHM 421 - ToPIC 3 - StatisticsthemfyNo ratings yet

- Ed 203 - Stat (Cluster B) - Suguitan, J.L. Exercise #1Document4 pagesEd 203 - Stat (Cluster B) - Suguitan, J.L. Exercise #1John Lewis SuguitanNo ratings yet

- Capitulo 9 QC With R PDFDocument33 pagesCapitulo 9 QC With R PDFMartin VidalonNo ratings yet

- labVIEW y ExcelDocument5 pageslabVIEW y Exceloferamal9562No ratings yet

- Remis (Real Estate Management System)Document73 pagesRemis (Real Estate Management System)Ogankpolor Kelly Uyi100% (1)

- Measures of Central Tendency and DispersionDocument13 pagesMeasures of Central Tendency and DispersionArlan Joseph LopezNo ratings yet

- ES031 M1 DataCollection&PresentationDocument64 pagesES031 M1 DataCollection&PresentationGwyneth Marie DayaganNo ratings yet

- Pranav Sir - Statistics Theory Notes Dec 2022Document15 pagesPranav Sir - Statistics Theory Notes Dec 2022HarshNo ratings yet

- Multiple Indicator Kriging Models in MineSight 3DDocument5 pagesMultiple Indicator Kriging Models in MineSight 3D11804No ratings yet

- Quiz Test of First and Third ChapterDocument2 pagesQuiz Test of First and Third ChapterHaFizSNKNo ratings yet

- Machines 05 00021 v3 PDFDocument28 pagesMachines 05 00021 v3 PDFAuditio MandhanyNo ratings yet

- Q3 Statistics and Probability 11 Module 2Document22 pagesQ3 Statistics and Probability 11 Module 2leonelyn.leceraNo ratings yet

- MLife Theory PDFDocument12 pagesMLife Theory PDFOsmanKatliNo ratings yet

- مستوى الوعي بأخلاقيات البحث التربوي لدى طلبة الدراساتDocument46 pagesمستوى الوعي بأخلاقيات البحث التربوي لدى طلبة الدراساتadnan53No ratings yet

- Flow Measurement Uncertainty and Data Reconciliation-EssenceDocument29 pagesFlow Measurement Uncertainty and Data Reconciliation-EssenceWen Wu100% (1)

- Activity-4-1 Salosagcol, Leobert Yancy GDocument2 pagesActivity-4-1 Salosagcol, Leobert Yancy GLeobert Yancy SalosagcolNo ratings yet

- Chap 016Document137 pagesChap 016Virender SinghNo ratings yet

- SIR CLEO - Statistics-ExamDocument11 pagesSIR CLEO - Statistics-ExamOrly AbrenicaNo ratings yet

- MATH Test Only TNR 10Document8 pagesMATH Test Only TNR 10Elaine ManalansanNo ratings yet