Download as pdf or txt

You might also like

- Lufthansa - Your Booking InformationDocument3 pagesLufthansa - Your Booking InformationMedia PilleNo ratings yet

- Managing Personal FinanceDocument7 pagesManaging Personal FinanceCarl Joseph BalajadiaNo ratings yet

- Michael Tonry - Punishing Race - A Continuing American Dilemma (2011, Oxford University Press)Document221 pagesMichael Tonry - Punishing Race - A Continuing American Dilemma (2011, Oxford University Press)Par PoundzNo ratings yet

- Personal Financial PlanningDocument8 pagesPersonal Financial PlanningAkanksha SrivastavaNo ratings yet

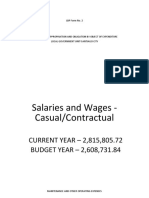

- LBP Form No. 4Document8 pagesLBP Form No. 4Shie La Ma RieNo ratings yet

- PayU - Sales DeckDocument27 pagesPayU - Sales DeckaNANTNo ratings yet

- Bachelor Degree TimetableDocument20 pagesBachelor Degree Timetablebite meNo ratings yet

- An Assignment On Fund ManagementDocument10 pagesAn Assignment On Fund Managementarvind singhalNo ratings yet

- BrijeshDocument120 pagesBrijeshAakash147No ratings yet

- RM - J229 - Research PaperDocument10 pagesRM - J229 - Research PaperRishikaNo ratings yet

- Black Book (Pradnya More)Document74 pagesBlack Book (Pradnya More)ahmedsirajkhan147No ratings yet

- Comparative Analysis of Various Financial Institution in The Market 2011Document120 pagesComparative Analysis of Various Financial Institution in The Market 2011Binay TiwariNo ratings yet

- Report of Financial Capability of Street Vendors Reference With Kolar and Bangalore 22-4-2019 Updated - For MergeDocument56 pagesReport of Financial Capability of Street Vendors Reference With Kolar and Bangalore 22-4-2019 Updated - For MergeNandish gowdaNo ratings yet

- Wealth Management and Alternate Investments: Term Project Phase-1Document13 pagesWealth Management and Alternate Investments: Term Project Phase-1priti GuptaNo ratings yet

- Financial Planning of Individual Synosis.....Document14 pagesFinancial Planning of Individual Synosis.....Ronak SethiaNo ratings yet

- Research On Financial PlanningDocument9 pagesResearch On Financial PlanningvaradNo ratings yet

- Fundamentals of Finance and Financial ManagementDocument4 pagesFundamentals of Finance and Financial ManagementCrisha Diane GalvezNo ratings yet

- Financial Planning & Tax Management PDFDocument16 pagesFinancial Planning & Tax Management PDFRanjeet singhNo ratings yet

- Term Paper Topics For Investment ManagementDocument8 pagesTerm Paper Topics For Investment Managementaflskkcez100% (1)

- BF 4QW3Document48 pagesBF 4QW3Ian Bethelmar UmaliNo ratings yet

- Management Technology 2150: Book ReportDocument6 pagesManagement Technology 2150: Book ReportFloyd SeremNo ratings yet

- Q3 4 Personal Finance EditedDocument11 pagesQ3 4 Personal Finance Editedbeavivo1No ratings yet

- Personal Budget As A List of All of My Expenses Such As Tuition Fees School SuppliesDocument10 pagesPersonal Budget As A List of All of My Expenses Such As Tuition Fees School SuppliesJanine IgdalinoNo ratings yet

- FamilybudgetingDocument30 pagesFamilybudgetingNeethu VincentNo ratings yet

- FINAL MahantheshDocument138 pagesFINAL MahantheshKapil DevNo ratings yet

- Financial ManagmentDocument25 pagesFinancial ManagmentSHASHANK TOMER 21211781No ratings yet

- Wealth Management and Alternate Investments: End Term Project ReportDocument36 pagesWealth Management and Alternate Investments: End Term Project ReportSakshee SinghNo ratings yet

- Pursue Lesson 1Document14 pagesPursue Lesson 1Kent Andojar MarianitoNo ratings yet

- Financail Management 2 NotesDocument86 pagesFinancail Management 2 NotesRalph MindaroNo ratings yet

- ProjectDocument29 pagesProjectSanket PatilNo ratings yet

- Personal Finance Is The Financial Management Which An Individual or A Family Unit Performs To BudgetDocument5 pagesPersonal Finance Is The Financial Management Which An Individual or A Family Unit Performs To Budgetdhwani100% (1)

- 8 Financial Literacy Lesson1Document6 pages8 Financial Literacy Lesson1hlmd.blogNo ratings yet

- Maryam DocsDocument28 pagesMaryam DocstalhahammadmNo ratings yet

- Personal Finance Chapter 1Document6 pagesPersonal Finance Chapter 1SUMAYYAH MANALAONo ratings yet

- Financial PlanningDocument4 pagesFinancial Planningਸਰਦਾਰ ਦੀਪ ਗਿੱਲNo ratings yet

- Business FinanceDocument49 pagesBusiness FinanceFrancis GeboneNo ratings yet

- Familybudgeting 140117071008 Phpapp01 141004043430 Conversion Gate01 PDFDocument30 pagesFamilybudgeting 140117071008 Phpapp01 141004043430 Conversion Gate01 PDFjhenilyn ramosNo ratings yet

- For A Rich Future: Owning A Car, A HouseDocument11 pagesFor A Rich Future: Owning A Car, A Housedbsmba2015No ratings yet

- Finance Thesis Topics 2013 in PakistanDocument7 pagesFinance Thesis Topics 2013 in Pakistanhod1beh0dik3100% (2)

- Project Finance Dissertation PDFDocument5 pagesProject Finance Dissertation PDFPayToDoMyPaperDurham100% (1)

- Financial Management Thesis DownloadDocument4 pagesFinancial Management Thesis Downloadpwqlnolkd100% (2)

- Principle 1: Personal Financial ManagementDocument12 pagesPrinciple 1: Personal Financial Managementapi-315024834No ratings yet

- MBA Project TopicsDocument15 pagesMBA Project TopicsAvinash BilagiNo ratings yet

- Finance Is The Lifeline of Any BusinessDocument22 pagesFinance Is The Lifeline of Any BusinessmeseretNo ratings yet

- Savings BehaviorDocument28 pagesSavings BehaviorEverton Anger CavalheiroNo ratings yet

- Financial Term Paper TopicsDocument7 pagesFinancial Term Paper Topicsafmzweybsyajeq100% (1)

- Financial ManagementDocument443 pagesFinancial ManagementPayam Ashori100% (2)

- Thesis Topics Corporate FinanceDocument8 pagesThesis Topics Corporate FinanceGina Rizzo100% (2)

- Financial Term PaperDocument4 pagesFinancial Term Paperafdtslawm100% (1)

- Personal Financial PlanningDocument21 pagesPersonal Financial PlanningAparna PavaniNo ratings yet

- Local Media6678742499800428630Document25 pagesLocal Media6678742499800428630sean gladimirNo ratings yet

- Digital Assignment - 2: Submitted To: Submitted byDocument12 pagesDigital Assignment - 2: Submitted To: Submitted byMonashreeNo ratings yet

- Behavioural Research MnkjalsjdDocument43 pagesBehavioural Research MnkjalsjdAhmedShujaNo ratings yet

- Research Paper of Finance PDFDocument6 pagesResearch Paper of Finance PDFfvfr9cg8100% (1)

- Financial LiteracyDocument10 pagesFinancial LiteracyRose Marie OderioNo ratings yet

- 6 Financial LiteracyDocument7 pages6 Financial LiteracyELDREI VICEDONo ratings yet

- Solved Paper FSD-2010Document11 pagesSolved Paper FSD-2010Kiran SoniNo ratings yet

- Business Finance - ModuleDocument33 pagesBusiness Finance - ModuleMark Laurence FernandoNo ratings yet

- Competency 2 AdditionalDocument13 pagesCompetency 2 AdditionalDan Jave Dumpa100% (1)

- Finance - Theory & PracticeDocument12 pagesFinance - Theory & PracticeArham OrbNo ratings yet

- IADocument92 pagesIAAbhishekNo ratings yet

- Anagha Ashok MK Final Project 2k19Document97 pagesAnagha Ashok MK Final Project 2k19uday manikantaNo ratings yet

- Assigment: "Money Management"Document12 pagesAssigment: "Money Management"Aqsa NoorNo ratings yet

- A Flangeless Complete Denture Prosthesis A Case Report April 2017 7862206681 3603082Document2 pagesA Flangeless Complete Denture Prosthesis A Case Report April 2017 7862206681 3603082wdyNo ratings yet

- AC 800M Controller: Outline of All ModulesDocument6 pagesAC 800M Controller: Outline of All ModulesSd GhNo ratings yet

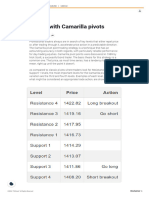

- Trading Stocks With Camarilla PivotsDocument6 pagesTrading Stocks With Camarilla Pivotsluca pilottiNo ratings yet

- Design Thinking ExerciseDocument21 pagesDesign Thinking ExerciseBlake PayriceNo ratings yet

- Nurses Bill of RightsDocument1 pageNurses Bill of RightsFlauros Ryu Jabien100% (1)

- Ob-Gyn Quiz 4Document11 pagesOb-Gyn Quiz 4Ndor BariboloNo ratings yet

- Difference Between Battle and WarDocument3 pagesDifference Between Battle and Warwaniarbaz28No ratings yet

- Manoj Bhargava: From Billionaire Monk To Ground-Breaking Change MakerDocument5 pagesManoj Bhargava: From Billionaire Monk To Ground-Breaking Change MakerAdilAdNo ratings yet

- ACOSTA, Josef De. Historia Natural y Moral de Las IndiasDocument1,022 pagesACOSTA, Josef De. Historia Natural y Moral de Las IndiasJosé Antonio M. Ameijeiras100% (1)

- English Trial 2017 SBP P1+P2 (Answer Scheme)Document14 pagesEnglish Trial 2017 SBP P1+P2 (Answer Scheme)Tan Zhen Xin100% (1)

- 2017 Carryall 500-550 (ERIC and EX-40 EFI)Document442 pages2017 Carryall 500-550 (ERIC and EX-40 EFI)bartolomealmacenNo ratings yet

- Sponge City in Surigao Del SurDocument10 pagesSponge City in Surigao Del SurLearnce MasculinoNo ratings yet

- For The Full Essay Please WHATSAPP 010-2504287: Assignment / TugasanDocument16 pagesFor The Full Essay Please WHATSAPP 010-2504287: Assignment / TugasanSimon RajNo ratings yet

- Data Analytics For Accounting 1st Edition Richardson Solutions ManualDocument25 pagesData Analytics For Accounting 1st Edition Richardson Solutions ManualRhondaHogancank100% (51)

- STP 491-1971Document90 pagesSTP 491-1971Tim SchouwNo ratings yet

- The Giant and The RockDocument6 pagesThe Giant and The RockVangie SalvacionNo ratings yet

- Beeck V Aquaslide 'N' Dive Corp.Document2 pagesBeeck V Aquaslide 'N' Dive Corp.crlstinaaaNo ratings yet

- Interior Design Considerations To Enhance Student Satisfaction in ClassroomsDocument12 pagesInterior Design Considerations To Enhance Student Satisfaction in ClassroomsGlobal Research and Development ServicesNo ratings yet

- Eight Parts of SpeechDocument173 pagesEight Parts of SpeechJan Kenrick SagumNo ratings yet

- Disseminated Intravascular CoagulationDocument4 pagesDisseminated Intravascular CoagulationHendra SshNo ratings yet

- Superagent: A Customer Service Chatbot For E-Commerce WebsitesDocument12 pagesSuperagent: A Customer Service Chatbot For E-Commerce WebsitesAisha AnwarNo ratings yet

- Death and The AfterlifeDocument2 pagesDeath and The AfterlifeAdityaNandanNo ratings yet

- Kerala Agricultural University: Main Campus, Vellanikkara, Thrissur - 680 656, KeralaDocument3 pagesKerala Agricultural University: Main Campus, Vellanikkara, Thrissur - 680 656, KeralaAyyoobNo ratings yet

- County: Complete Car Bare ChassisDocument9 pagesCounty: Complete Car Bare ChassisMachupicchuCuscoNo ratings yet

- Chapter Vii - Ethics For CriminologistsDocument6 pagesChapter Vii - Ethics For CriminologistsMarlboro BlackNo ratings yet