Topic 6 - Lecture Examples

Topic 6 - Lecture Examples

You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- Deed of Sale of Shares of StockDocument2 pagesDeed of Sale of Shares of StockArbee Arquiza86% (7)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- FinanceDocument22 pagesFinanceMemo NerNo ratings yet

- Module 13 Notes Payable - Debt ResructuringDocument10 pagesModule 13 Notes Payable - Debt ResructuringryanNo ratings yet

- Investment in Debt Securities Qualifying Exam Review Sample QuestionsDocument7 pagesInvestment in Debt Securities Qualifying Exam Review Sample QuestionsHannah Jane Umbay100% (1)

- Kiem Tra - LMS - So 1 - DADocument8 pagesKiem Tra - LMS - So 1 - DAHuỳnh Minh Gia Hào100% (1)

- Recruitment and SelectionDocument49 pagesRecruitment and SelectionNeha Anand75% (4)

- Ebook Vince Secrets To Smart TradingDocument18 pagesEbook Vince Secrets To Smart TradingMujitha Manorathna100% (1)

- ACT1106 - Bond ExercisesDocument4 pagesACT1106 - Bond ExercisesPj Dela VegaNo ratings yet

- Quiz 2Document10 pagesQuiz 2simcity23No ratings yet

- IAS 32, IFRS7,9 Financial InstrumentsDocument6 pagesIAS 32, IFRS7,9 Financial InstrumentsMazni Hanisah100% (2)

- Test Advance Financial AccountingDocument2 pagesTest Advance Financial AccountingSaadullah ChannaNo ratings yet

- IFRS 9 Financial Instruments Out of Class Practice ENDocument11 pagesIFRS 9 Financial Instruments Out of Class Practice ENHuynh TungNo ratings yet

- ACCT 3312 - Chap 17 Practice QuestionsDocument5 pagesACCT 3312 - Chap 17 Practice QuestionsVernon Dwanye LewisNo ratings yet

- Examples Self IFRS 9 PDFDocument9 pagesExamples Self IFRS 9 PDFErslanNo ratings yet

- Semi-Annual Interest, Journal Entries)Document3 pagesSemi-Annual Interest, Journal Entries)Jazehl Joy ValdezNo ratings yet

- Ae16 Interm AccDocument15 pagesAe16 Interm Accana rosemarie enaoNo ratings yet

- CH15-16-17 Review Problems and SolutionDocument16 pagesCH15-16-17 Review Problems and SolutionJonathan OrrNo ratings yet

- Ia 3 PrelimDocument12 pagesIa 3 PrelimshaylieeeNo ratings yet

- Compre23 FARDocument12 pagesCompre23 FARchristinemariet.ramirezNo ratings yet

- Debt Practice ProblemsDocument11 pagesDebt Practice ProblemsmikeNo ratings yet

- MQ - Ifrs 9Document11 pagesMQ - Ifrs 9Huỳnh Minh Gia HàoNo ratings yet

- Ias: 23 Barrowing Cost: What Are Qualifying Assets?Document4 pagesIas: 23 Barrowing Cost: What Are Qualifying Assets?nishanthanNo ratings yet

- R31 Non-Current (Long-Term) Liabilities Q BankDocument16 pagesR31 Non-Current (Long-Term) Liabilities Q BankAhmedNo ratings yet

- Debt Invest. For Prac - SolvingDocument2 pagesDebt Invest. For Prac - SolvingShekainah BNo ratings yet

- ACC 3003 - Final Exam RevisionDocument19 pagesACC 3003 - Final Exam Revisionfalnuaimi001100% (1)

- 2 InvestmentsDocument4 pages2 InvestmentsAdrian MallariNo ratings yet

- Midterm Exam in Intermediate 2: Identify The Choice That Best Completes The Statement or Answers The QuestionDocument9 pagesMidterm Exam in Intermediate 2: Identify The Choice That Best Completes The Statement or Answers The QuestionGolden KookieNo ratings yet

- واجب متوسطه 2 اختياراتDocument5 pagesواجب متوسطه 2 اختياراتmode.xp.jamelNo ratings yet

- INVESTMENTS IN DEBT SECURITIES-ExercisesDocument4 pagesINVESTMENTS IN DEBT SECURITIES-ExercisesJazmine Arianne DalayNo ratings yet

- QUIZ Bonds PayableDocument7 pagesQUIZ Bonds PayableKaren GarciaNo ratings yet

- Far PDFDocument13 pagesFar PDFp9hnbpt5hpNo ratings yet

- Exercise Chapter 14Document37 pagesExercise Chapter 1421070286 Dương Thùy AnhNo ratings yet

- Gen008 P1 ExamDocument11 pagesGen008 P1 ExamMary Lyn DatuinNo ratings yet

- Chapter 14Document4 pagesChapter 14ks1043210No ratings yet

- AACA2 Midterm QDocument10 pagesAACA2 Midterm QChristen HerceNo ratings yet

- Illustrative Examples - Bonds PayableDocument2 pagesIllustrative Examples - Bonds PayableChuchi SubardiagaNo ratings yet

- Final Exam - Acc115Document7 pagesFinal Exam - Acc115angelapearlrNo ratings yet

- Sample Final Exam QuestionsDocument28 pagesSample Final Exam QuestionsHuyNo ratings yet

- Homework 6 - Long-Term Financial LiabilitiesDocument2 pagesHomework 6 - Long-Term Financial LiabilitiesCha PampolinaNo ratings yet

- 2023 JA - FM - QuestionDocument4 pages2023 JA - FM - Questionmiradvance studyNo ratings yet

- Assignment Dilutive SecuritiesDocument2 pagesAssignment Dilutive SecuritiesJohanaNo ratings yet

- Audit of Long-Term LiabilitiesDocument3 pagesAudit of Long-Term LiabilitiesRonamae RevillaNo ratings yet

- Quarter Test 2 QPDocument7 pagesQuarter Test 2 QPOmair HasanNo ratings yet

- ACEINT1 Intermediate Accounting 1 Final Exam SY 2021-2022Document10 pagesACEINT1 Intermediate Accounting 1 Final Exam SY 2021-2022Marriel Fate Cullano100% (1)

- 08 Bond InvestmentDocument3 pages08 Bond InvestmentAllegria Alamo100% (1)

- Quiz - (Evening Class)Document4 pagesQuiz - (Evening Class)JeonNo ratings yet

- Final Examn Dec 2022 CF2 ALLDocument7 pagesFinal Examn Dec 2022 CF2 ALLleyrepavonNo ratings yet

- Topic 03 Non-Current Liabilities - Bonds Payable: Intermediate Accounting 2 - Bernadette L. Baul, CPADocument4 pagesTopic 03 Non-Current Liabilities - Bonds Payable: Intermediate Accounting 2 - Bernadette L. Baul, CPAhIgh QuaLIty SVTNo ratings yet

- Far Drill2Document4 pagesFar Drill2Jung Hwan SoNo ratings yet

- 4 5953918248238974494Document8 pages4 5953918248238974494Muktar jibo0% (1)

- Quiz Pension SHEDocument8 pagesQuiz Pension SHEErine ContranoNo ratings yet

- ACCT 301B - CH 13 In-Class ExercisesDocument10 pagesACCT 301B - CH 13 In-Class ExercisesJudith Garcia0% (1)

- 15.501/516 Problem Set 7 Long-Term Debt, Leases and Off-Balance Sheet Financing I. Accounting For BondsDocument2 pages15.501/516 Problem Set 7 Long-Term Debt, Leases and Off-Balance Sheet Financing I. Accounting For BondsRadhika KapurNo ratings yet

- HANDOUT - Bonds PayableDocument4 pagesHANDOUT - Bonds PayableMarian Augelio PolancoNo ratings yet

- Fa2 Tut 5Document5 pagesFa2 Tut 5Truong Thi Ha Trang 1KT-19No ratings yet

- ILLUSTRATIVE-EXAMPLES InvFADocument4 pagesILLUSTRATIVE-EXAMPLES InvFACyrss BaldemosNo ratings yet

- 2023-Cacc012 - Final - Main Examination Question Paper - 27 Nov 2023 - Assignment To Supp StudentsDocument9 pages2023-Cacc012 - Final - Main Examination Question Paper - 27 Nov 2023 - Assignment To Supp Studentsnkgapelet46No ratings yet

- F9 Past PapersDocument32 pagesF9 Past PapersBurhan Maqsood100% (1)

- FinMan Unit 5 Tutorial Valuation of Bonds Revised Sep2021Document3 pagesFinMan Unit 5 Tutorial Valuation of Bonds Revised Sep2021Debbie DebzNo ratings yet

- Chapter 2 TB - Long Term Liabilities StudentsDocument7 pagesChapter 2 TB - Long Term Liabilities StudentsMohammed Al-ghamdiNo ratings yet

- Satyam Fraud NewDocument21 pagesSatyam Fraud NewNitin Kumar0% (1)

- Notes Chapter 4 FARDocument5 pagesNotes Chapter 4 FARcpacfa78% (9)

- Havells India Ltd-15Document226 pagesHavells India Ltd-15Apoorva GuptaNo ratings yet

- Driving SchoolDocument14 pagesDriving SchoolKhalid MemonNo ratings yet

- ACCT3563 Revision Workshop Slides + QuestionsDocument9 pagesACCT3563 Revision Workshop Slides + QuestionsstephanieNo ratings yet

- Financial Statements, Taxes, and Cash Flow: Lecturer Dr. Le Thanh HuyenDocument47 pagesFinancial Statements, Taxes, and Cash Flow: Lecturer Dr. Le Thanh HuyenLê naNo ratings yet

- DocxDocument35 pagesDocxjikee11No ratings yet

- PFRS 7 Financial Instruments DisclosuresDocument20 pagesPFRS 7 Financial Instruments DisclosureseiraNo ratings yet

- AVP Compliance Director in New York City NY Resume Thomas SomelofskeDocument2 pagesAVP Compliance Director in New York City NY Resume Thomas SomelofskeThomas SomelofskeNo ratings yet

- PEFFinal Prospectus PEFDocument386 pagesPEFFinal Prospectus PEFJohn LimNo ratings yet

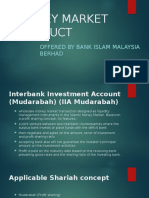

- Money Market BimbDocument9 pagesMoney Market BimbAncoi Ariff CyrilNo ratings yet

- India Business Law Directory 2012-2013Document39 pagesIndia Business Law Directory 2012-2013pittaisaacnewtonNo ratings yet

- PL Tax Compliance Sample Paper OneDocument9 pagesPL Tax Compliance Sample Paper Onekarlr9No ratings yet

- 5 Accounting PrinciplesDocument3 pages5 Accounting Principleswhiteorchid11100% (1)

- CH 15Document24 pagesCH 15sumihosaNo ratings yet

- FINA01052383 - Tutorial 3 Problem SetDocument5 pagesFINA01052383 - Tutorial 3 Problem SetJunaid Arshad50% (2)

- BFLS 2016 Registration FormDocument2 pagesBFLS 2016 Registration FormManan TyagiNo ratings yet

- Paper On Corporate BondsDocument4 pagesPaper On Corporate BondsSaurabh BhatnagarNo ratings yet

- Class 1Document4 pagesClass 1skjacobpoolNo ratings yet

- Of Long-Term Growth: Nurturing The RootsDocument68 pagesOf Long-Term Growth: Nurturing The RootsDhea Rizky AprillaNo ratings yet

- SynopsisDocument4 pagesSynopsispriya68kNo ratings yet

- Bongaigaon Ref - FinanDocument10 pagesBongaigaon Ref - FinansdNo ratings yet

- Sankalp Kant - GM BDDocument2 pagesSankalp Kant - GM BDhimanshu royNo ratings yet

- Accenture The Future of Fintech and Banking Digitallydisrupted or ReimaDocument12 pagesAccenture The Future of Fintech and Banking Digitallydisrupted or ReimaRon Finberg100% (1)

- Let's Get Down To Business!Document15 pagesLet's Get Down To Business!Saravanan PanneervelNo ratings yet

- IBHFL IPO Abridged ProspectusDocument48 pagesIBHFL IPO Abridged Prospectusratan203No ratings yet

Download as pdf or txt

You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- Deed of Sale of Shares of StockDocument2 pagesDeed of Sale of Shares of StockArbee Arquiza86% (7)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- FinanceDocument22 pagesFinanceMemo NerNo ratings yet

- Module 13 Notes Payable - Debt ResructuringDocument10 pagesModule 13 Notes Payable - Debt ResructuringryanNo ratings yet

- Investment in Debt Securities Qualifying Exam Review Sample QuestionsDocument7 pagesInvestment in Debt Securities Qualifying Exam Review Sample QuestionsHannah Jane Umbay100% (1)

- Kiem Tra - LMS - So 1 - DADocument8 pagesKiem Tra - LMS - So 1 - DAHuỳnh Minh Gia Hào100% (1)

- Recruitment and SelectionDocument49 pagesRecruitment and SelectionNeha Anand75% (4)

- Ebook Vince Secrets To Smart TradingDocument18 pagesEbook Vince Secrets To Smart TradingMujitha Manorathna100% (1)

- ACT1106 - Bond ExercisesDocument4 pagesACT1106 - Bond ExercisesPj Dela VegaNo ratings yet

- Quiz 2Document10 pagesQuiz 2simcity23No ratings yet

- IAS 32, IFRS7,9 Financial InstrumentsDocument6 pagesIAS 32, IFRS7,9 Financial InstrumentsMazni Hanisah100% (2)

- Test Advance Financial AccountingDocument2 pagesTest Advance Financial AccountingSaadullah ChannaNo ratings yet

- IFRS 9 Financial Instruments Out of Class Practice ENDocument11 pagesIFRS 9 Financial Instruments Out of Class Practice ENHuynh TungNo ratings yet

- ACCT 3312 - Chap 17 Practice QuestionsDocument5 pagesACCT 3312 - Chap 17 Practice QuestionsVernon Dwanye LewisNo ratings yet

- Examples Self IFRS 9 PDFDocument9 pagesExamples Self IFRS 9 PDFErslanNo ratings yet

- Semi-Annual Interest, Journal Entries)Document3 pagesSemi-Annual Interest, Journal Entries)Jazehl Joy ValdezNo ratings yet

- Ae16 Interm AccDocument15 pagesAe16 Interm Accana rosemarie enaoNo ratings yet

- CH15-16-17 Review Problems and SolutionDocument16 pagesCH15-16-17 Review Problems and SolutionJonathan OrrNo ratings yet

- Ia 3 PrelimDocument12 pagesIa 3 PrelimshaylieeeNo ratings yet

- Compre23 FARDocument12 pagesCompre23 FARchristinemariet.ramirezNo ratings yet

- Debt Practice ProblemsDocument11 pagesDebt Practice ProblemsmikeNo ratings yet

- MQ - Ifrs 9Document11 pagesMQ - Ifrs 9Huỳnh Minh Gia HàoNo ratings yet

- Ias: 23 Barrowing Cost: What Are Qualifying Assets?Document4 pagesIas: 23 Barrowing Cost: What Are Qualifying Assets?nishanthanNo ratings yet

- R31 Non-Current (Long-Term) Liabilities Q BankDocument16 pagesR31 Non-Current (Long-Term) Liabilities Q BankAhmedNo ratings yet

- Debt Invest. For Prac - SolvingDocument2 pagesDebt Invest. For Prac - SolvingShekainah BNo ratings yet

- ACC 3003 - Final Exam RevisionDocument19 pagesACC 3003 - Final Exam Revisionfalnuaimi001100% (1)

- 2 InvestmentsDocument4 pages2 InvestmentsAdrian MallariNo ratings yet

- Midterm Exam in Intermediate 2: Identify The Choice That Best Completes The Statement or Answers The QuestionDocument9 pagesMidterm Exam in Intermediate 2: Identify The Choice That Best Completes The Statement or Answers The QuestionGolden KookieNo ratings yet

- واجب متوسطه 2 اختياراتDocument5 pagesواجب متوسطه 2 اختياراتmode.xp.jamelNo ratings yet

- INVESTMENTS IN DEBT SECURITIES-ExercisesDocument4 pagesINVESTMENTS IN DEBT SECURITIES-ExercisesJazmine Arianne DalayNo ratings yet

- QUIZ Bonds PayableDocument7 pagesQUIZ Bonds PayableKaren GarciaNo ratings yet

- Far PDFDocument13 pagesFar PDFp9hnbpt5hpNo ratings yet

- Exercise Chapter 14Document37 pagesExercise Chapter 1421070286 Dương Thùy AnhNo ratings yet

- Gen008 P1 ExamDocument11 pagesGen008 P1 ExamMary Lyn DatuinNo ratings yet

- Chapter 14Document4 pagesChapter 14ks1043210No ratings yet

- AACA2 Midterm QDocument10 pagesAACA2 Midterm QChristen HerceNo ratings yet

- Illustrative Examples - Bonds PayableDocument2 pagesIllustrative Examples - Bonds PayableChuchi SubardiagaNo ratings yet

- Final Exam - Acc115Document7 pagesFinal Exam - Acc115angelapearlrNo ratings yet

- Sample Final Exam QuestionsDocument28 pagesSample Final Exam QuestionsHuyNo ratings yet

- Homework 6 - Long-Term Financial LiabilitiesDocument2 pagesHomework 6 - Long-Term Financial LiabilitiesCha PampolinaNo ratings yet

- 2023 JA - FM - QuestionDocument4 pages2023 JA - FM - Questionmiradvance studyNo ratings yet

- Assignment Dilutive SecuritiesDocument2 pagesAssignment Dilutive SecuritiesJohanaNo ratings yet

- Audit of Long-Term LiabilitiesDocument3 pagesAudit of Long-Term LiabilitiesRonamae RevillaNo ratings yet

- Quarter Test 2 QPDocument7 pagesQuarter Test 2 QPOmair HasanNo ratings yet

- ACEINT1 Intermediate Accounting 1 Final Exam SY 2021-2022Document10 pagesACEINT1 Intermediate Accounting 1 Final Exam SY 2021-2022Marriel Fate Cullano100% (1)

- 08 Bond InvestmentDocument3 pages08 Bond InvestmentAllegria Alamo100% (1)

- Quiz - (Evening Class)Document4 pagesQuiz - (Evening Class)JeonNo ratings yet

- Final Examn Dec 2022 CF2 ALLDocument7 pagesFinal Examn Dec 2022 CF2 ALLleyrepavonNo ratings yet

- Topic 03 Non-Current Liabilities - Bonds Payable: Intermediate Accounting 2 - Bernadette L. Baul, CPADocument4 pagesTopic 03 Non-Current Liabilities - Bonds Payable: Intermediate Accounting 2 - Bernadette L. Baul, CPAhIgh QuaLIty SVTNo ratings yet

- Far Drill2Document4 pagesFar Drill2Jung Hwan SoNo ratings yet

- 4 5953918248238974494Document8 pages4 5953918248238974494Muktar jibo0% (1)

- Quiz Pension SHEDocument8 pagesQuiz Pension SHEErine ContranoNo ratings yet

- ACCT 301B - CH 13 In-Class ExercisesDocument10 pagesACCT 301B - CH 13 In-Class ExercisesJudith Garcia0% (1)

- 15.501/516 Problem Set 7 Long-Term Debt, Leases and Off-Balance Sheet Financing I. Accounting For BondsDocument2 pages15.501/516 Problem Set 7 Long-Term Debt, Leases and Off-Balance Sheet Financing I. Accounting For BondsRadhika KapurNo ratings yet

- HANDOUT - Bonds PayableDocument4 pagesHANDOUT - Bonds PayableMarian Augelio PolancoNo ratings yet

- Fa2 Tut 5Document5 pagesFa2 Tut 5Truong Thi Ha Trang 1KT-19No ratings yet

- ILLUSTRATIVE-EXAMPLES InvFADocument4 pagesILLUSTRATIVE-EXAMPLES InvFACyrss BaldemosNo ratings yet

- 2023-Cacc012 - Final - Main Examination Question Paper - 27 Nov 2023 - Assignment To Supp StudentsDocument9 pages2023-Cacc012 - Final - Main Examination Question Paper - 27 Nov 2023 - Assignment To Supp Studentsnkgapelet46No ratings yet

- F9 Past PapersDocument32 pagesF9 Past PapersBurhan Maqsood100% (1)

- FinMan Unit 5 Tutorial Valuation of Bonds Revised Sep2021Document3 pagesFinMan Unit 5 Tutorial Valuation of Bonds Revised Sep2021Debbie DebzNo ratings yet

- Chapter 2 TB - Long Term Liabilities StudentsDocument7 pagesChapter 2 TB - Long Term Liabilities StudentsMohammed Al-ghamdiNo ratings yet

- Satyam Fraud NewDocument21 pagesSatyam Fraud NewNitin Kumar0% (1)

- Notes Chapter 4 FARDocument5 pagesNotes Chapter 4 FARcpacfa78% (9)

- Havells India Ltd-15Document226 pagesHavells India Ltd-15Apoorva GuptaNo ratings yet

- Driving SchoolDocument14 pagesDriving SchoolKhalid MemonNo ratings yet

- ACCT3563 Revision Workshop Slides + QuestionsDocument9 pagesACCT3563 Revision Workshop Slides + QuestionsstephanieNo ratings yet

- Financial Statements, Taxes, and Cash Flow: Lecturer Dr. Le Thanh HuyenDocument47 pagesFinancial Statements, Taxes, and Cash Flow: Lecturer Dr. Le Thanh HuyenLê naNo ratings yet

- DocxDocument35 pagesDocxjikee11No ratings yet

- PFRS 7 Financial Instruments DisclosuresDocument20 pagesPFRS 7 Financial Instruments DisclosureseiraNo ratings yet

- AVP Compliance Director in New York City NY Resume Thomas SomelofskeDocument2 pagesAVP Compliance Director in New York City NY Resume Thomas SomelofskeThomas SomelofskeNo ratings yet

- PEFFinal Prospectus PEFDocument386 pagesPEFFinal Prospectus PEFJohn LimNo ratings yet

- Money Market BimbDocument9 pagesMoney Market BimbAncoi Ariff CyrilNo ratings yet

- India Business Law Directory 2012-2013Document39 pagesIndia Business Law Directory 2012-2013pittaisaacnewtonNo ratings yet

- PL Tax Compliance Sample Paper OneDocument9 pagesPL Tax Compliance Sample Paper Onekarlr9No ratings yet

- 5 Accounting PrinciplesDocument3 pages5 Accounting Principleswhiteorchid11100% (1)

- CH 15Document24 pagesCH 15sumihosaNo ratings yet

- FINA01052383 - Tutorial 3 Problem SetDocument5 pagesFINA01052383 - Tutorial 3 Problem SetJunaid Arshad50% (2)

- BFLS 2016 Registration FormDocument2 pagesBFLS 2016 Registration FormManan TyagiNo ratings yet

- Paper On Corporate BondsDocument4 pagesPaper On Corporate BondsSaurabh BhatnagarNo ratings yet

- Class 1Document4 pagesClass 1skjacobpoolNo ratings yet

- Of Long-Term Growth: Nurturing The RootsDocument68 pagesOf Long-Term Growth: Nurturing The RootsDhea Rizky AprillaNo ratings yet

- SynopsisDocument4 pagesSynopsispriya68kNo ratings yet

- Bongaigaon Ref - FinanDocument10 pagesBongaigaon Ref - FinansdNo ratings yet

- Sankalp Kant - GM BDDocument2 pagesSankalp Kant - GM BDhimanshu royNo ratings yet

- Accenture The Future of Fintech and Banking Digitallydisrupted or ReimaDocument12 pagesAccenture The Future of Fintech and Banking Digitallydisrupted or ReimaRon Finberg100% (1)

- Let's Get Down To Business!Document15 pagesLet's Get Down To Business!Saravanan PanneervelNo ratings yet

- IBHFL IPO Abridged ProspectusDocument48 pagesIBHFL IPO Abridged Prospectusratan203No ratings yet