Download as pdf or txt

You might also like

- VAT - CPA Reviewer in Taxation - Enrico D. Tabag PDFDocument103 pagesVAT - CPA Reviewer in Taxation - Enrico D. Tabag PDFDGAENo ratings yet

- CombinepdfDocument129 pagesCombinepdfMary Jane G. FACERONDANo ratings yet

- Bustax Final ExamDocument13 pagesBustax Final Examshudaye100% (3)

- Deductions From Gross IncomeDocument49 pagesDeductions From Gross IncomeRoronoa ZoroNo ratings yet

- Intro To Business Taxation: Group 2Document32 pagesIntro To Business Taxation: Group 2Hardly Dare GonzalesNo ratings yet

- BUSTAXADocument9 pagesBUSTAXATitania ErzaNo ratings yet

- Transfer and Business Taxation - MIDTERMDocument14 pagesTransfer and Business Taxation - MIDTERMYvette Pauline JovenNo ratings yet

- Consumption Tax On Sales (Percentage Tax)Document32 pagesConsumption Tax On Sales (Percentage Tax)Alicia Feliciano100% (1)

- VAT NotesDocument8 pagesVAT NotesFayie De LunaNo ratings yet

- Percentage Taxes NotesDocument4 pagesPercentage Taxes Notesrajahmati_28No ratings yet

- Tax2 Seatworks-03.23.2020Document2 pagesTax2 Seatworks-03.23.2020Allen Fey De JesusNo ratings yet

- Business and Transfer TaxationDocument5 pagesBusiness and Transfer TaxationElizabeth OlaNo ratings yet

- Infographics - TaxDocument12 pagesInfographics - TaxPablo InocencioNo ratings yet

- Business Tax SummaryDocument10 pagesBusiness Tax SummaryJohn Raymond MarzanNo ratings yet

- TAX Chapter 5 Reviewer - Summary Principles of Business Taxation TAX Chapter 5 Reviewer - Summary Principles of Business TaxationDocument5 pagesTAX Chapter 5 Reviewer - Summary Principles of Business Taxation TAX Chapter 5 Reviewer - Summary Principles of Business TaxationMakoy BixenmanNo ratings yet

- Async 2022 VAT UPDATEDocument8 pagesAsync 2022 VAT UPDATEBogs QuitainNo ratings yet

- BIR Form 2551Q: Quarterly Percentage TaxDocument8 pagesBIR Form 2551Q: Quarterly Percentage TaxAngelyn SamandeNo ratings yet

- Value Added Tax - : - Output VAT: Zero-Rated SalesDocument23 pagesValue Added Tax - : - Output VAT: Zero-Rated SalesAjey MendiolaNo ratings yet

- BUSTAX Notes M4-5Document12 pagesBUSTAX Notes M4-5Rosette TuazonNo ratings yet

- Business Taxation: - Back To BasicDocument56 pagesBusiness Taxation: - Back To BasicWearIt Co.No ratings yet

- Percentage Tax Who Are Required To File?Document4 pagesPercentage Tax Who Are Required To File?Angelyn SamandeNo ratings yet

- Business Taxation: - Back To BasicDocument56 pagesBusiness Taxation: - Back To BasicWearIt Co.No ratings yet

- Business TaxesDocument50 pagesBusiness TaxesMacatol KristineNo ratings yet

- Subject To VAT Subject To VAT 3) Real Property Utilized For Socialized Housing VAT ExemptDocument32 pagesSubject To VAT Subject To VAT 3) Real Property Utilized For Socialized Housing VAT ExemptNikka SanzNo ratings yet

- M3 Exempt Sales of Goods Properties & ServicesDocument27 pagesM3 Exempt Sales of Goods Properties & ServicesAlicia FelicianoNo ratings yet

- Business Taxation: Rex B. Banggawan, Cpa, MbaDocument50 pagesBusiness Taxation: Rex B. Banggawan, Cpa, MbaAllyson VillalobosNo ratings yet

- Value Added Tax: A. Business TaxesDocument3 pagesValue Added Tax: A. Business TaxesNerish PlazaNo ratings yet

- Bustax Chapter 8 PDFDocument11 pagesBustax Chapter 8 PDFPineda, Paula MarieNo ratings yet

- Modified Finals VatDocument3 pagesModified Finals VatClyden Jaile RamirezNo ratings yet

- Adzu Tax02 A Learning Packet 2 Value Added TaxDocument9 pagesAdzu Tax02 A Learning Packet 2 Value Added TaxJustine Paul Pangasi-an100% (1)

- Other Percentage TaxesDocument40 pagesOther Percentage TaxesKay Hanalee Villanueva NorioNo ratings yet

- Notes Other Tax PercentageDocument7 pagesNotes Other Tax PercentageJohn RellonNo ratings yet

- Income TaxationDocument6 pagesIncome TaxationJahz Aira GamboaNo ratings yet

- Special CorporationsDocument25 pagesSpecial CorporationsHilarie JeanNo ratings yet

- Business Tax PDFDocument9 pagesBusiness Tax PDFEstrada, Jemuel A.No ratings yet

- Reviewer in Business TaxationDocument18 pagesReviewer in Business Taxationdianacaindoy0127No ratings yet

- Whether Donation Is Taxable/Nontaxable Zero Rated/VAT Exempt/VAT Taxable 2 Problems On Donation 2 Problems On VATDocument7 pagesWhether Donation Is Taxable/Nontaxable Zero Rated/VAT Exempt/VAT Taxable 2 Problems On Donation 2 Problems On VATJape PreciaNo ratings yet

- Creditable Tax ReportDocument131 pagesCreditable Tax ReportJieve Licca G. FanoNo ratings yet

- Percentage TaxDocument17 pagesPercentage TaxPrincess Jay NacorNo ratings yet

- Chapter 8 Zero Rated SalesDocument39 pagesChapter 8 Zero Rated SalesCathy Marie Angela ArellanoNo ratings yet

- Income Tax On CorporationDocument53 pagesIncome Tax On CorporationLyka Mae Palarca IrangNo ratings yet

- PT, Excise and DST NotesDocument10 pagesPT, Excise and DST NotesFayie De LunaNo ratings yet

- Output Vat Zero-Rated Sales ch8Document3 pagesOutput Vat Zero-Rated Sales ch8Marionne GNo ratings yet

- Tax Ch6 VAT BinaluyoDocument6 pagesTax Ch6 VAT Binaluyomavrhyck.21No ratings yet

- Income Tax On CorporationDocument54 pagesIncome Tax On CorporationJamielene Tan100% (1)

- VAT Exempt SalesDocument14 pagesVAT Exempt SalesJuvanni SantosNo ratings yet

- Tax2 FinalsDocument8 pagesTax2 FinalsKevin Elrey Arce100% (2)

- 2020 Bustax - VAT - Part1 - Handouts PDFDocument13 pages2020 Bustax - VAT - Part1 - Handouts PDFMila MercadoNo ratings yet

- Tax Quiz 1 ReviewerDocument7 pagesTax Quiz 1 ReviewerDan Reynel T. AlcazarinNo ratings yet

- Other Percentage TaxDocument3 pagesOther Percentage TaxBon BonsNo ratings yet

- Tax Notes Midterms PDFDocument27 pagesTax Notes Midterms PDFTae TaeNo ratings yet

- VAT On ImportationDocument24 pagesVAT On ImportationShamae Duma-anNo ratings yet

- Business TaxesDocument50 pagesBusiness TaxesSunny DaeNo ratings yet

- Percentage Taxes: Kinds of Percentage Taxes Percentage Tax Rates Compliance RequirementsDocument23 pagesPercentage Taxes: Kinds of Percentage Taxes Percentage Tax Rates Compliance RequirementsOtis MelbournNo ratings yet

- Zero - Rated Sales: 0% VAT - Output VATDocument5 pagesZero - Rated Sales: 0% VAT - Output VATNerish PlazaNo ratings yet

- Business TaxationDocument7 pagesBusiness TaxationZehra LeeNo ratings yet

- Tax-Title V Other Percentage TaxesDocument55 pagesTax-Title V Other Percentage Taxesherbertwest19728490No ratings yet

- Business TaxesDocument47 pagesBusiness TaxesJoyce MorganNo ratings yet

- Other Percentage Taxes: Prof. Jeanefer Reyes CPA, MPADocument29 pagesOther Percentage Taxes: Prof. Jeanefer Reyes CPA, MPAmark anthony espirituNo ratings yet

- IRR Update On TRAIN LAWDocument6 pagesIRR Update On TRAIN LAWChrislynNo ratings yet

- Canadian International Taxation: Income Tax Rules for ResidentsFrom EverandCanadian International Taxation: Income Tax Rules for ResidentsNo ratings yet

- Belgium Local Government SlidesDocument17 pagesBelgium Local Government Slidesada montiNo ratings yet

- EFU Gen Student TravelDocument2 pagesEFU Gen Student TravelcharsalanNo ratings yet

- 21.12.24 Mayor Baker LetterDocument2 pages21.12.24 Mayor Baker LetterWendy LiberatoreNo ratings yet

- Commissioner Vs Magsaysay LinesDocument2 pagesCommissioner Vs Magsaysay LinesVerlynMayThereseCaroNo ratings yet

- Quarterly Remittance Return of Final Income Taxes Withheld: Background InformationDocument2 pagesQuarterly Remittance Return of Final Income Taxes Withheld: Background InformationVincent John RigorNo ratings yet

- P.O. MATERIAL - Mamidipally LineDocument30 pagesP.O. MATERIAL - Mamidipally LineBEPL TendersNo ratings yet

- CH 22 - 26Document43 pagesCH 22 - 26Mahammad AliyevNo ratings yet

- Case Digest DADIZON V. HON. COURT OF APPEALSDocument2 pagesCase Digest DADIZON V. HON. COURT OF APPEALSTaj Ngilay100% (1)

- PestleDocument8 pagesPestleTasmina ZamanNo ratings yet

- Nozick: Entitlement Theory & Self-OwnershipDocument14 pagesNozick: Entitlement Theory & Self-OwnershipRav SandhuNo ratings yet

- Lipsa Pradhan (SIP PDFDocument10 pagesLipsa Pradhan (SIP PDFDebasis sahuNo ratings yet

- Fdi in India PDFDocument12 pagesFdi in India PDFpnjhub legalNo ratings yet

- Agent/ Intermediary Name and Code:POLICYBAZAAR INSURANCE BROKERS PRIVATE LIMITED BRC0000434Document5 pagesAgent/ Intermediary Name and Code:POLICYBAZAAR INSURANCE BROKERS PRIVATE LIMITED BRC0000434hiteshmohakar15No ratings yet

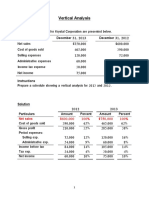

- Vertical Analysis SolutionsDocument5 pagesVertical Analysis SolutionsSamer IsmaelNo ratings yet

- Commercial Dispatch Eedition 3-16-21Document12 pagesCommercial Dispatch Eedition 3-16-21The DispatchNo ratings yet

- Chapter 2: Tax AdministrationDocument3 pagesChapter 2: Tax AdministrationHezroNo ratings yet

- A Ship Loaded With Honey Assessing The Honey Trade in The Crown of Aragon Fifteenth To Sixteenth CenturiesDocument24 pagesA Ship Loaded With Honey Assessing The Honey Trade in The Crown of Aragon Fifteenth To Sixteenth CenturiesdaduduNo ratings yet

- Carreon Margery Legal Forms Midterm 01272017Document9 pagesCarreon Margery Legal Forms Midterm 01272017marge carreonNo ratings yet

- Lotus Enclave (Phase-Ii) - 2/3 BHK Villas: Preferential Location Charges (PLC)Document2 pagesLotus Enclave (Phase-Ii) - 2/3 BHK Villas: Preferential Location Charges (PLC)SAROJNo ratings yet

- Petrol Head School: Business ReportDocument19 pagesPetrol Head School: Business ReportHouDaAakNo ratings yet

- Westwoods April 2023Document2 pagesWestwoods April 2023SeshasaiNo ratings yet

- Cambridge International AS & A Level: Business 9609/32 February/March 2022Document23 pagesCambridge International AS & A Level: Business 9609/32 February/March 2022thabo bhejaneNo ratings yet

- Tax Evasion and Tax Avoidance With Case StudyDocument39 pagesTax Evasion and Tax Avoidance With Case StudyKatrine Olga Ramones-CastilloNo ratings yet

- Michael Sanderson On Equality of Arms in The Law in AustraliaDocument28 pagesMichael Sanderson On Equality of Arms in The Law in AustraliaSenateBriberyInquiryNo ratings yet

- JFC Existing Audit Accounting Systems1Document5 pagesJFC Existing Audit Accounting Systems1Acier KozukiNo ratings yet

- The Market MechanismDocument2 pagesThe Market MechanismJanna Marie CalabioNo ratings yet

- Financial Analysis Honda Atlas Cars Pakistan 1Document6 pagesFinancial Analysis Honda Atlas Cars Pakistan 126342634No ratings yet

- CB2402 Week 3 Part 2Document4 pagesCB2402 Week 3 Part 2RoyChungNo ratings yet

- BM (Unit 2) NotesDocument17 pagesBM (Unit 2) NotesMohd asimNo ratings yet