Download as docx, pdf, or txt

You might also like

- Life Asia Training - 01Document50 pagesLife Asia Training - 01CM100% (1)

- Lesson 1-4 Cost - Volume-Profit AnalysisDocument13 pagesLesson 1-4 Cost - Volume-Profit AnalysisClaire BarbaNo ratings yet

- Group 7 BreakevenquantiDocument56 pagesGroup 7 BreakevenquantiAndrei Nicole Mendoza Rivera67% (3)

- Chapter 12 Ap 12Document3 pagesChapter 12 Ap 12freaann03No ratings yet

- Cost Accounting Exercise-11Document5 pagesCost Accounting Exercise-11Ki xxiNo ratings yet

- Chapter 12 Problem 3Document8 pagesChapter 12 Problem 3freaann03No ratings yet

- Practical Problems & Solutions Class Work Upto IL.10Document20 pagesPractical Problems & Solutions Class Work Upto IL.10Dhanishta PramodNo ratings yet

- Additional SolutionDocument4 pagesAdditional Solutionfreaann03No ratings yet

- Assignment 2 CVPDocument9 pagesAssignment 2 CVPhed-llimanganNo ratings yet

- CVP ExercisesDocument10 pagesCVP ExercisesDaiane AlcaideNo ratings yet

- CVP AnalysisDocument5 pagesCVP AnalysisAzumi RaeNo ratings yet

- Tugasan 6 Bab 6Document4 pagesTugasan 6 Bab 6azwan88No ratings yet

- Chapter # 8 Exercise & Problems - AnswersDocument8 pagesChapter # 8 Exercise & Problems - AnswersZia UddinNo ratings yet

- BEP SolutionsDocument4 pagesBEP SolutionsMahediNo ratings yet

- Unit 8 MC CVP Analysis Solutions 3Document32 pagesUnit 8 MC CVP Analysis Solutions 3Ankit AgarwalNo ratings yet

- Ipcc Cost AnswerDocument13 pagesIpcc Cost AnswerHarsha VardhanNo ratings yet

- 4 Lecture - CVP AnalysisDocument34 pages4 Lecture - CVP AnalysisDorothy Enid AguaNo ratings yet

- CVP Analysis in One ProductDocument6 pagesCVP Analysis in One ProductShaira GampongNo ratings yet

- Solution Post-Test3Document6 pagesSolution Post-Test3Shienell PincaNo ratings yet

- CVP - GitttDocument15 pagesCVP - GitttFarid RezaNo ratings yet

- Required: A. Break-Even Point in Units BEP in Units : Total Cost CM Per UnitDocument3 pagesRequired: A. Break-Even Point in Units BEP in Units : Total Cost CM Per UnitarisuNo ratings yet

- Roxas Seatwork-4Document14 pagesRoxas Seatwork-4Ronna Mae RedublaNo ratings yet

- Assgment 1 (Chapter 1-4) : Agung Rizal / 2201827622Document10 pagesAssgment 1 (Chapter 1-4) : Agung Rizal / 2201827622Agung Rizal DewantoroNo ratings yet

- Queens CollegeDocument8 pagesQueens CollegeKALKIDAN KASSAHUNNo ratings yet

- Requirement 1 Total Per Unit: Banitog, Brigitte C. BSA 211 Exercise 1 (Contribution Format Income Statement)Document4 pagesRequirement 1 Total Per Unit: Banitog, Brigitte C. BSA 211 Exercise 1 (Contribution Format Income Statement)MyunimintNo ratings yet

- Chap 12Document13 pagesChap 12freaann03No ratings yet

- Numerical Problems - SolutionsDocument19 pagesNumerical Problems - SolutionsVishesh RohraNo ratings yet

- Suggested Solutions: Where'S Alice? Example ADocument3 pagesSuggested Solutions: Where'S Alice? Example ASufina SallehNo ratings yet

- Numericals On CVP AnalysisDocument2 pagesNumericals On CVP AnalysisAmil SaifiNo ratings yet

- CVP ExercisesDocument7 pagesCVP ExercisesEunize Escalona100% (1)

- 02 29 11 2023 Bep Q 1 - 3Document17 pages02 29 11 2023 Bep Q 1 - 3Gokul KulNo ratings yet

- 320C03Document33 pages320C03ArjelVajvoda100% (3)

- CVP Analysis: PG D M2 0 21-23 RelevantreadingsDocument21 pagesCVP Analysis: PG D M2 0 21-23 RelevantreadingsAthi SivaNo ratings yet

- Cis PTDocument3 pagesCis PTAlyza LansanganNo ratings yet

- See Zhao Wei U2003083Document5 pagesSee Zhao Wei U2003083zhaoweiNo ratings yet

- CVP AnalysisDocument3 pagesCVP AnalysisTERRIUS AceNo ratings yet

- Cost Volume Profit AnalysisDocument17 pagesCost Volume Profit AnalysisSumaiya Iqbal78No ratings yet

- Num 2Document4 pagesNum 2nilesh nagureNo ratings yet

- Prepared by DR - Hassan Sweillam University of 6 of October, EgyptDocument18 pagesPrepared by DR - Hassan Sweillam University of 6 of October, EgyptjgjghNo ratings yet

- Transfer Pricing Examples - Matz&UDocument13 pagesTransfer Pricing Examples - Matz&UMuhammad azeemNo ratings yet

- Solution For Chapter 22 - Part2Document4 pagesSolution For Chapter 22 - Part2Dương Xuân ĐạtNo ratings yet

- SOLUTION For Break Even Analysis Example ProblemDocument11 pagesSOLUTION For Break Even Analysis Example ProblemArly Kurt TorresNo ratings yet

- Managerial accountingBEP, CM T. ProfitDocument4 pagesManagerial accountingBEP, CM T. ProfitZeinab MohamadNo ratings yet

- MA CHAPTER 4 Marginal Costing 2Document93 pagesMA CHAPTER 4 Marginal Costing 2Mohd Zubair KhanNo ratings yet

- Cost II AssignmentDocument18 pagesCost II AssignmentAddisNo ratings yet

- CVP AnalysisDocument41 pagesCVP AnalysisMasud Khan ShakilNo ratings yet

- CVP AnalysisDocument2 pagesCVP AnalysisRikki Mae TeofistoNo ratings yet

- M3 01. CVP IllustrationDocument2 pagesM3 01. CVP Illustrationhanis nabilaNo ratings yet

- CostingDocument15 pagesCostingPavan ChitragarNo ratings yet

- TLA 4 Answers For DiscussionDocument21 pagesTLA 4 Answers For DiscussionTrisha Monique VillaNo ratings yet

- Chapter 22Document14 pagesChapter 22Nguyên BảoNo ratings yet

- CAC Computations Chap 4 1 20Document9 pagesCAC Computations Chap 4 1 20rochelle lagmayNo ratings yet

- BE AnalysisDocument44 pagesBE Analysissahu.tukun003No ratings yet

- Break EvenDocument28 pagesBreak EvenShovon KaizerNo ratings yet

- Marginal CostingDocument62 pagesMarginal CostingnehaNo ratings yet

- Costing ProblemsDocument74 pagesCosting Problemsmeenakshimanghani85% (47)

- Contribution Margin RatioDocument4 pagesContribution Margin RatioResty VillaroelNo ratings yet

- 15 Marginal CostingDocument14 pages15 Marginal CostingHaresh KNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Mathematical Formulas for Economics and Business: A Simple IntroductionFrom EverandMathematical Formulas for Economics and Business: A Simple IntroductionRating: 4 out of 5 stars4/5 (4)

- Chapter 12 Exercise 1 21Document5 pagesChapter 12 Exercise 1 21freaann03No ratings yet

- Chapter 14 Exercises 34Document7 pagesChapter 14 Exercises 34freaann03No ratings yet

- Chapter 14 Problem 12Document6 pagesChapter 14 Problem 12freaann03No ratings yet

- Chapter 14 Exercise 12Document7 pagesChapter 14 Exercise 12freaann03No ratings yet

- Art MovementsDocument26 pagesArt Movementsfreaann03No ratings yet

- Chapter2. Plant Design Revised-AASTU... 2 (Recovered)Document50 pagesChapter2. Plant Design Revised-AASTU... 2 (Recovered)Amdu BergaNo ratings yet

- Impact of Strategic Planning On Financial Performance of Companies in TurkeyDocument11 pagesImpact of Strategic Planning On Financial Performance of Companies in TurkeyCicko CokaNo ratings yet

- Analisis Pengendalian Internal Atas Persediaan Barang Dagangan Pada Toko Alfamart Sat Boom Baru Palembang Sahila Kusminaini ArminDocument26 pagesAnalisis Pengendalian Internal Atas Persediaan Barang Dagangan Pada Toko Alfamart Sat Boom Baru Palembang Sahila Kusminaini ArminDewi NdutNo ratings yet

- Decision LetterDocument2 pagesDecision LetterNick MayfieldNo ratings yet

- Accounting WorksheetDocument3 pagesAccounting WorksheetMartha AntonNo ratings yet

- COURSE PLAN - BBA3 - Indian EconomyDocument16 pagesCOURSE PLAN - BBA3 - Indian EconomypriyankaNo ratings yet

- Daftar Saham - Consumer Non-Cyclicals - Utama - 20230530Document4 pagesDaftar Saham - Consumer Non-Cyclicals - Utama - 20230530FAHTNI CHAIRANTI HUTABARAT 2019No ratings yet

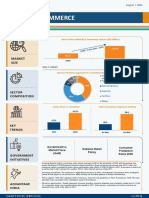

- E Commerce Infographic August 2021Document1 pageE Commerce Infographic August 2021Sudha Swayam PravaNo ratings yet

- On Exim BankDocument22 pagesOn Exim Banksejwalpinki100% (1)

- WWW - Angelone.in.: Naheed Rehan PatelDocument151 pagesWWW - Angelone.in.: Naheed Rehan PatelRam JaneNo ratings yet

- What Is Really Different About Emerging Market Multinationals?Document7 pagesWhat Is Really Different About Emerging Market Multinationals?karishmakakarishmaNo ratings yet

- DocumenteDocument5 pagesDocumentemaxim caldarasanNo ratings yet

- Anup Engineering - NanoNivesh - ICICI DirectDocument8 pagesAnup Engineering - NanoNivesh - ICICI DirectAmit SharmaNo ratings yet

- Meeting-Outcome of The Meeting-uNu1m7Document21 pagesMeeting-Outcome of The Meeting-uNu1m7Ramani KrishnanNo ratings yet

- Lyceum-Northwestern University: L-NU AA-23-02-01-18Document8 pagesLyceum-Northwestern University: L-NU AA-23-02-01-18Amie Jane MirandaNo ratings yet

- PROGRAM OF WORK N Bill of Materials Handwashing Facility SES 2022 UpdatedDocument2 pagesPROGRAM OF WORK N Bill of Materials Handwashing Facility SES 2022 UpdatedGeoff ReyNo ratings yet

- BCG Infrastructure Strategy 2023 Building The Green Hydrogen Economy Mar 2023 RDocument36 pagesBCG Infrastructure Strategy 2023 Building The Green Hydrogen Economy Mar 2023 RRahul RanaNo ratings yet

- Policy Document BajajAllianz General InsuranceDocument6 pagesPolicy Document BajajAllianz General InsuranceVishnu PNo ratings yet

- Past Paper Answers - 2017 (B) : Business Name:-NM Company LTDDocument42 pagesPast Paper Answers - 2017 (B) : Business Name:-NM Company LTDName of RoshanNo ratings yet

- Chapter 9. Office TPM ManualDocument25 pagesChapter 9. Office TPM ManualVivek Kumar100% (1)

- Used Car Financing Aitab Flexi PDSDocument12 pagesUsed Car Financing Aitab Flexi PDSnovtov354No ratings yet

- Practical 8: Visit A Bank/financial Institution To Enquire About Various Funding Schemes For Small Scale EnterpriseDocument4 pagesPractical 8: Visit A Bank/financial Institution To Enquire About Various Funding Schemes For Small Scale Enterprise02 - CM Ankita Adam83% (6)

- Form PDF 240143980290722Document7 pagesForm PDF 240143980290722RebornNo ratings yet

- Lisa Peattie Two PuzzlesDocument6 pagesLisa Peattie Two Puzzlesna22b020No ratings yet

- Foundations of Financial Management: Spreadsheet TemplatesDocument7 pagesFoundations of Financial Management: Spreadsheet Templatesalaa_h1100% (1)

- Ias 12-Income TaxesDocument2 pagesIas 12-Income Taxesbeth alviolaNo ratings yet

- Rate of Return One Project: Engineering EconomyDocument22 pagesRate of Return One Project: Engineering Economyann94bNo ratings yet

- Challenges That Women Entrepreneurs and Startup Are Facing in AddisDocument61 pagesChallenges That Women Entrepreneurs and Startup Are Facing in AddisKalkidan Admasu AyalewNo ratings yet

- Marketing Management 1 WeekDocument19 pagesMarketing Management 1 WeekYousef MansourNo ratings yet