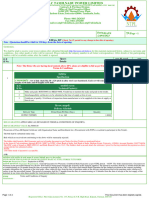

Dhruva Litigation Alert - Preliminary Action Against Suppliers For Non-Payment of GST - Breach of Section 16 (2) (C)

Dhruva Litigation Alert - Preliminary Action Against Suppliers For Non-Payment of GST - Breach of Section 16 (2) (C)

You might also like

- Verified 202 Petition Against Texas Central RailroadDocument39 pagesVerified 202 Petition Against Texas Central RailroadKBTXNo ratings yet

- Uy Vs CA GR No 109557 November 29Document2 pagesUy Vs CA GR No 109557 November 29preiquencyNo ratings yet

- Emergency Motion To Stay Foreclosure Sale Additional Motion Practice MaterialDocument168 pagesEmergency Motion To Stay Foreclosure Sale Additional Motion Practice MaterialRicharnellia-RichieRichBattiest-Collins100% (3)

- CIT v. MKJ Enterprises Ltd.-Cal HCDocument2 pagesCIT v. MKJ Enterprises Ltd.-Cal HCSaksham ShrivastavNo ratings yet

- TS 124 ITAT 2022DEL TP Akzo - Nobel - India - LTDDocument10 pagesTS 124 ITAT 2022DEL TP Akzo - Nobel - India - LTDruchimishra673No ratings yet

- Burden of Proof in Case of ITCDocument45 pagesBurden of Proof in Case of ITCv_sudarshanNo ratings yet

- CNS COMNET SOLUTION PVT LTD Vs CCE & STDocument3 pagesCNS COMNET SOLUTION PVT LTD Vs CCE & STkillertapasNo ratings yet

- Signed Contract 4600011687Document4 pagesSigned Contract 4600011687Alok SinghNo ratings yet

- M dt.16.05.2023 - Ms Duttcon Consultant Engrs P Ltd. KolkataDocument5 pagesM dt.16.05.2023 - Ms Duttcon Consultant Engrs P Ltd. Kolkataduttcon engineeringNo ratings yet

- (2010) 328 ITR 169 (Punjab & Haryana) (19-08-2009) Commissioner of Income-Tax vs. Mandeep SinghDocument2 pages(2010) 328 ITR 169 (Punjab & Haryana) (19-08-2009) Commissioner of Income-Tax vs. Mandeep SinghkalravNo ratings yet

- CIT-Vs-NCR-Corporation-Pvt.-Ltd.-Karnataka-High-Court - ATMs Are ComputerDocument15 pagesCIT-Vs-NCR-Corporation-Pvt.-Ltd.-Karnataka-High-Court - ATMs Are ComputerSoftdynamiteNo ratings yet

- Terms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/02/2019Document2 pagesTerms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/02/2019pravv vvvNo ratings yet

- Your Reliance Bill: Summary of Current Charges Amount (RS)Document3 pagesYour Reliance Bill: Summary of Current Charges Amount (RS)Pratap GunnuNo ratings yet

- 2024 (5) TMI 795 - AT - M - S Ashiana Housing Limited Versus Commissioner of Central Excise &..Document7 pages2024 (5) TMI 795 - AT - M - S Ashiana Housing Limited Versus Commissioner of Central Excise &..ABHINo ratings yet

- Page 1/3Document3 pagesPage 1/3dycmmgncrNo ratings yet

- S dt.16.05.2023 - Ms Duttcon Consultant Engrs P Ltd. KolkataDocument4 pagesS dt.16.05.2023 - Ms Duttcon Consultant Engrs P Ltd. Kolkataduttcon engineeringNo ratings yet

- Airconsystems (I) : PVT - LTDDocument1 pageAirconsystems (I) : PVT - LTDDinesh VallechaNo ratings yet

- Your Reliance Bill: Summary of Current Charges Amount (RS)Document4 pagesYour Reliance Bill: Summary of Current Charges Amount (RS)royal.faraz4u9608No ratings yet

- Specification Tender No 2223110290Document2 pagesSpecification Tender No 2223110290D JayakrishnarajuNo ratings yet

- Tendernotice 1Document3 pagesTendernotice 1rafikul123No ratings yet

- Office of The Area General Manager, Wani North Area PO: Bhalar, Tah:Wani, Dist - Yavatmal (MS) PIN-445304Document98 pagesOffice of The Area General Manager, Wani North Area PO: Bhalar, Tah:Wani, Dist - Yavatmal (MS) PIN-445304SauravNo ratings yet

- Tendernotice 1Document38 pagesTendernotice 1GARIMA SONINo ratings yet

- Catalog DetailsDocument9 pagesCatalog Detailsgcgary87No ratings yet

- CIR vs. Petron, G. R. No. 185568 (2012)Document14 pagesCIR vs. Petron, G. R. No. 185568 (2012)Aaron James PuasoNo ratings yet

- Approval LetterDocument2 pagesApproval LetterhariharaboopathiNo ratings yet

- Supreme Court: Republic of TheDocument23 pagesSupreme Court: Republic of TheKin Pearly FloresNo ratings yet

- Tech Tab TS245126 106295207Document6 pagesTech Tab TS245126 106295207sesaretails2015No ratings yet

- This Document Is Important and Requires Your Immediate AttentionDocument32 pagesThis Document Is Important and Requires Your Immediate AttentionRupesh Kumar BeheraNo ratings yet

- 2022-10-14 - Beterman Engineering Private Limited - Transport ServiceDocument3 pages2022-10-14 - Beterman Engineering Private Limited - Transport ServiceSajjan SantukaNo ratings yet

- Tendernotice NIQDocument11 pagesTendernotice NIQB DroidanNo ratings yet

- Tax Invoice: IRNDocument1 pageTax Invoice: IRNCA Shrikant VaranasiNo ratings yet

- Lakshmi Subbaiaah Madurai TexDocument37 pagesLakshmi Subbaiaah Madurai TexParameshwaran NanjundanNo ratings yet

- Tech Tab 72245267 106290865Document5 pagesTech Tab 72245267 106290865sesaretails2015No ratings yet

- Case Law 2023 10 Centax 190 Bom 22 08 2023Document6 pagesCase Law 2023 10 Centax 190 Bom 22 08 2023Ashwini ChandrasekaranNo ratings yet

- Service Proforma Invoice - ACCEPTANCE Tata Projects-020Document1 pageService Proforma Invoice - ACCEPTANCE Tata Projects-020maneesh bhardwajNo ratings yet

- J 2014 SCC OnLine CESTAT 3489Document2 pagesJ 2014 SCC OnLine CESTAT 3489Jayant SharmaNo ratings yet

- TS 333 ITAT 2013DEL TS 333 ITAT 2013DEL SPX India PVT LTDDocument5 pagesTS 333 ITAT 2013DEL TS 333 ITAT 2013DEL SPX India PVT LTDbharath289No ratings yet

- Terms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/05/2021Document2 pagesTerms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/05/2021krisivaNo ratings yet

- ACT Invoice Mar19Document2 pagesACT Invoice Mar19Ravi ShankarNo ratings yet

- 1484813626powder Blending TenderDocument17 pages1484813626powder Blending TenderNagendra KumarNo ratings yet

- 4 Tender - HubliDocument31 pages4 Tender - HubliRafikul RahemanNo ratings yet

- Your Reliance Bill: Summary of Current Charges Amount (RS)Document3 pagesYour Reliance Bill: Summary of Current Charges Amount (RS)contactmeprabirNo ratings yet

- Ds Tata Power Solar Systems Limited 1: Outline AgreementDocument8 pagesDs Tata Power Solar Systems Limited 1: Outline AgreementM Q ASLAMNo ratings yet

- Loan Sanction LetterDocument3 pagesLoan Sanction Lettergaurav sondhiNo ratings yet

- CL 8909Document6 pagesCL 8909IshanNo ratings yet

- State of Tamil Nadu vs. S. Rajendran, Liquidator of Daehsan Trading India Pvt. Ltd. and Anr.Document5 pagesState of Tamil Nadu vs. S. Rajendran, Liquidator of Daehsan Trading India Pvt. Ltd. and Anr.Sachika VijNo ratings yet

- Tab Trametinib (82235639)Document13 pagesTab Trametinib (82235639)dycmmgncrNo ratings yet

- Welcomeletter Up3043cd0180635Document11 pagesWelcomeletter Up3043cd0180635piyushk26016No ratings yet

- Tender ARC MechMainDocument140 pagesTender ARC MechMainDean GeorgeNo ratings yet

- Adobe Scan 01042021 - CompressedDocument6 pagesAdobe Scan 01042021 - CompressedKartik ShuklaNo ratings yet

- Auto TestDocument3 pagesAuto TestMaree AlShehriNo ratings yet

- Lucy Wanjiru Offer LetterDocument2 pagesLucy Wanjiru Offer Letterart lewyNo ratings yet

- Ilovepdf MergedDocument2 pagesIlovepdf MergedVikash ShahNo ratings yet

- Atria Convergence Technologies Limited, Due Date: 15/03/2020Document2 pagesAtria Convergence Technologies Limited, Due Date: 15/03/2020Bharadwaj SubramaniamNo ratings yet

- HD 10155Document227 pagesHD 10155Varun BatraNo ratings yet

- 1684303940-ITA No.1070-D-2022 - Havells India LTDDocument5 pages1684303940-ITA No.1070-D-2022 - Havells India LTDArulnidhi Ramanathan SeshanNo ratings yet

- Bill 446 - MoulyaDocument1 pageBill 446 - MoulyaRajesh RajNo ratings yet

- Mr. Bhanu Prakash Demand LetterDocument2 pagesMr. Bhanu Prakash Demand LetterBhanu PrakashNo ratings yet

- Terms Conditions Tpi Chennai 12TH Oct To 15TH Oct 2022Document6 pagesTerms Conditions Tpi Chennai 12TH Oct To 15TH Oct 2022Etrans 9No ratings yet

- Syonira Invecasts - Approved RPDocument32 pagesSyonira Invecasts - Approved RPyasahitabhardwajNo ratings yet

- Interpretation of Exermption NotfDocument4 pagesInterpretation of Exermption NotfSabrina CanoNo ratings yet

- An Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersFrom EverandAn Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersNo ratings yet

- Free Zone Persons - DDocument135 pagesFree Zone Persons - DSangeetha NaharNo ratings yet

- Aurtus Flash Alert 1714458676Document3 pagesAurtus Flash Alert 1714458676Sangeetha NaharNo ratings yet

- EY Washington Dispatch 1715448186Document8 pagesEY Washington Dispatch 1715448186Sangeetha NaharNo ratings yet

- SPOM TestDocument1 pageSPOM TestSangeetha NaharNo ratings yet

- Philippine Politics and Governance The Legislative BranchDocument18 pagesPhilippine Politics and Governance The Legislative BranchRussell SanicoNo ratings yet

- Ra 8294Document2 pagesRa 8294Rio TolentinoNo ratings yet

- 14) Belgica Vs Executive Secretary Paquito OchoaDocument281 pages14) Belgica Vs Executive Secretary Paquito OchoaMary Joyce Lacambra AquinoNo ratings yet

- Republic Vs Judge HidalgoDocument16 pagesRepublic Vs Judge HidalgoMikkoletNo ratings yet

- Cert II in Security Operations Instructor Lesson Plan TemplateDocument20 pagesCert II in Security Operations Instructor Lesson Plan TemplateSoke1No ratings yet

- Policarpio v. SalamatDocument5 pagesPolicarpio v. SalamatraykarloBNo ratings yet

- PEOPLE vs. GO PINDocument2 pagesPEOPLE vs. GO PINKristela AdraincemNo ratings yet

- Demafelis vs. CADocument6 pagesDemafelis vs. CAXryn MortelNo ratings yet

- Seemaarshadzaheer&Orsvs Municipal Corporation of Greater (2006) 5 SCC 282Document22 pagesSeemaarshadzaheer&Orsvs Municipal Corporation of Greater (2006) 5 SCC 282sai kiran gudisevaNo ratings yet

- Juvenile Justice System Thesis StatementDocument11 pagesJuvenile Justice System Thesis Statementsarahmitchelllittlerock100% (2)

- Vda de Bataclan V MedinaDocument4 pagesVda de Bataclan V MedinaJulius ManaloNo ratings yet

- LGS 210Document308 pagesLGS 210Ahmad Shex MhamadNo ratings yet

- DK BASU VS STate of West BengalDocument14 pagesDK BASU VS STate of West BengalAbhinav Malik100% (3)

- Ra 9262 ConstitutionalityDocument2 pagesRa 9262 ConstitutionalityRyan JD LimNo ratings yet

- Festejo V Fernando (Eng)Document6 pagesFestejo V Fernando (Eng)UlNo ratings yet

- Citibank, N.A. vs. CADocument2 pagesCitibank, N.A. vs. CAJL A H-DimaculanganNo ratings yet

- G. Sabio v. Gordon 504 SCRA 704Document2 pagesG. Sabio v. Gordon 504 SCRA 704mj lopezNo ratings yet

- 6 Heirs of Peter Donton Vs StierDocument18 pages6 Heirs of Peter Donton Vs StierClive HendelsonNo ratings yet

- CIR V ReyesDocument4 pagesCIR V ReyesAndrea GatchalianNo ratings yet

- Syllabus CRPCDocument5 pagesSyllabus CRPCksvv prasadNo ratings yet

- 09 Orbos v. BungubungDocument4 pages09 Orbos v. BungubungAlec VenturaNo ratings yet

- Sec.41 of CR - PCDocument7 pagesSec.41 of CR - PCDesai Sharath KumarNo ratings yet

- 1610 Tax Insight - Tech Mahindra LTDDocument3 pages1610 Tax Insight - Tech Mahindra LTDAlpa Shah DesaiNo ratings yet

- Felix E. Mendiola For PetitionerDocument3 pagesFelix E. Mendiola For PetitionerRosalie CastroNo ratings yet

- Loadmasters Customs Services V Glodel Brokerage - 639 SCRA 69Document14 pagesLoadmasters Customs Services V Glodel Brokerage - 639 SCRA 69Krista YntigNo ratings yet

- Application For Authorization of A Class ActionDocument18 pagesApplication For Authorization of A Class ActionNunatsiaqNewsNo ratings yet

- Faceless Appeals Conceptual Framework 110323 PDFDocument134 pagesFaceless Appeals Conceptual Framework 110323 PDFVishwas PatilNo ratings yet

Download as pdf or txt

You might also like

- Verified 202 Petition Against Texas Central RailroadDocument39 pagesVerified 202 Petition Against Texas Central RailroadKBTXNo ratings yet

- Uy Vs CA GR No 109557 November 29Document2 pagesUy Vs CA GR No 109557 November 29preiquencyNo ratings yet

- Emergency Motion To Stay Foreclosure Sale Additional Motion Practice MaterialDocument168 pagesEmergency Motion To Stay Foreclosure Sale Additional Motion Practice MaterialRicharnellia-RichieRichBattiest-Collins100% (3)

- CIT v. MKJ Enterprises Ltd.-Cal HCDocument2 pagesCIT v. MKJ Enterprises Ltd.-Cal HCSaksham ShrivastavNo ratings yet

- TS 124 ITAT 2022DEL TP Akzo - Nobel - India - LTDDocument10 pagesTS 124 ITAT 2022DEL TP Akzo - Nobel - India - LTDruchimishra673No ratings yet

- Burden of Proof in Case of ITCDocument45 pagesBurden of Proof in Case of ITCv_sudarshanNo ratings yet

- CNS COMNET SOLUTION PVT LTD Vs CCE & STDocument3 pagesCNS COMNET SOLUTION PVT LTD Vs CCE & STkillertapasNo ratings yet

- Signed Contract 4600011687Document4 pagesSigned Contract 4600011687Alok SinghNo ratings yet

- M dt.16.05.2023 - Ms Duttcon Consultant Engrs P Ltd. KolkataDocument5 pagesM dt.16.05.2023 - Ms Duttcon Consultant Engrs P Ltd. Kolkataduttcon engineeringNo ratings yet

- (2010) 328 ITR 169 (Punjab & Haryana) (19-08-2009) Commissioner of Income-Tax vs. Mandeep SinghDocument2 pages(2010) 328 ITR 169 (Punjab & Haryana) (19-08-2009) Commissioner of Income-Tax vs. Mandeep SinghkalravNo ratings yet

- CIT-Vs-NCR-Corporation-Pvt.-Ltd.-Karnataka-High-Court - ATMs Are ComputerDocument15 pagesCIT-Vs-NCR-Corporation-Pvt.-Ltd.-Karnataka-High-Court - ATMs Are ComputerSoftdynamiteNo ratings yet

- Terms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/02/2019Document2 pagesTerms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/02/2019pravv vvvNo ratings yet

- Your Reliance Bill: Summary of Current Charges Amount (RS)Document3 pagesYour Reliance Bill: Summary of Current Charges Amount (RS)Pratap GunnuNo ratings yet

- 2024 (5) TMI 795 - AT - M - S Ashiana Housing Limited Versus Commissioner of Central Excise &..Document7 pages2024 (5) TMI 795 - AT - M - S Ashiana Housing Limited Versus Commissioner of Central Excise &..ABHINo ratings yet

- Page 1/3Document3 pagesPage 1/3dycmmgncrNo ratings yet

- S dt.16.05.2023 - Ms Duttcon Consultant Engrs P Ltd. KolkataDocument4 pagesS dt.16.05.2023 - Ms Duttcon Consultant Engrs P Ltd. Kolkataduttcon engineeringNo ratings yet

- Airconsystems (I) : PVT - LTDDocument1 pageAirconsystems (I) : PVT - LTDDinesh VallechaNo ratings yet

- Your Reliance Bill: Summary of Current Charges Amount (RS)Document4 pagesYour Reliance Bill: Summary of Current Charges Amount (RS)royal.faraz4u9608No ratings yet

- Specification Tender No 2223110290Document2 pagesSpecification Tender No 2223110290D JayakrishnarajuNo ratings yet

- Tendernotice 1Document3 pagesTendernotice 1rafikul123No ratings yet

- Office of The Area General Manager, Wani North Area PO: Bhalar, Tah:Wani, Dist - Yavatmal (MS) PIN-445304Document98 pagesOffice of The Area General Manager, Wani North Area PO: Bhalar, Tah:Wani, Dist - Yavatmal (MS) PIN-445304SauravNo ratings yet

- Tendernotice 1Document38 pagesTendernotice 1GARIMA SONINo ratings yet

- Catalog DetailsDocument9 pagesCatalog Detailsgcgary87No ratings yet

- CIR vs. Petron, G. R. No. 185568 (2012)Document14 pagesCIR vs. Petron, G. R. No. 185568 (2012)Aaron James PuasoNo ratings yet

- Approval LetterDocument2 pagesApproval LetterhariharaboopathiNo ratings yet

- Supreme Court: Republic of TheDocument23 pagesSupreme Court: Republic of TheKin Pearly FloresNo ratings yet

- Tech Tab TS245126 106295207Document6 pagesTech Tab TS245126 106295207sesaretails2015No ratings yet

- This Document Is Important and Requires Your Immediate AttentionDocument32 pagesThis Document Is Important and Requires Your Immediate AttentionRupesh Kumar BeheraNo ratings yet

- 2022-10-14 - Beterman Engineering Private Limited - Transport ServiceDocument3 pages2022-10-14 - Beterman Engineering Private Limited - Transport ServiceSajjan SantukaNo ratings yet

- Tendernotice NIQDocument11 pagesTendernotice NIQB DroidanNo ratings yet

- Tax Invoice: IRNDocument1 pageTax Invoice: IRNCA Shrikant VaranasiNo ratings yet

- Lakshmi Subbaiaah Madurai TexDocument37 pagesLakshmi Subbaiaah Madurai TexParameshwaran NanjundanNo ratings yet

- Tech Tab 72245267 106290865Document5 pagesTech Tab 72245267 106290865sesaretails2015No ratings yet

- Case Law 2023 10 Centax 190 Bom 22 08 2023Document6 pagesCase Law 2023 10 Centax 190 Bom 22 08 2023Ashwini ChandrasekaranNo ratings yet

- Service Proforma Invoice - ACCEPTANCE Tata Projects-020Document1 pageService Proforma Invoice - ACCEPTANCE Tata Projects-020maneesh bhardwajNo ratings yet

- J 2014 SCC OnLine CESTAT 3489Document2 pagesJ 2014 SCC OnLine CESTAT 3489Jayant SharmaNo ratings yet

- TS 333 ITAT 2013DEL TS 333 ITAT 2013DEL SPX India PVT LTDDocument5 pagesTS 333 ITAT 2013DEL TS 333 ITAT 2013DEL SPX India PVT LTDbharath289No ratings yet

- Terms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/05/2021Document2 pagesTerms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/05/2021krisivaNo ratings yet

- ACT Invoice Mar19Document2 pagesACT Invoice Mar19Ravi ShankarNo ratings yet

- 1484813626powder Blending TenderDocument17 pages1484813626powder Blending TenderNagendra KumarNo ratings yet

- 4 Tender - HubliDocument31 pages4 Tender - HubliRafikul RahemanNo ratings yet

- Your Reliance Bill: Summary of Current Charges Amount (RS)Document3 pagesYour Reliance Bill: Summary of Current Charges Amount (RS)contactmeprabirNo ratings yet

- Ds Tata Power Solar Systems Limited 1: Outline AgreementDocument8 pagesDs Tata Power Solar Systems Limited 1: Outline AgreementM Q ASLAMNo ratings yet

- Loan Sanction LetterDocument3 pagesLoan Sanction Lettergaurav sondhiNo ratings yet

- CL 8909Document6 pagesCL 8909IshanNo ratings yet

- State of Tamil Nadu vs. S. Rajendran, Liquidator of Daehsan Trading India Pvt. Ltd. and Anr.Document5 pagesState of Tamil Nadu vs. S. Rajendran, Liquidator of Daehsan Trading India Pvt. Ltd. and Anr.Sachika VijNo ratings yet

- Tab Trametinib (82235639)Document13 pagesTab Trametinib (82235639)dycmmgncrNo ratings yet

- Welcomeletter Up3043cd0180635Document11 pagesWelcomeletter Up3043cd0180635piyushk26016No ratings yet

- Tender ARC MechMainDocument140 pagesTender ARC MechMainDean GeorgeNo ratings yet

- Adobe Scan 01042021 - CompressedDocument6 pagesAdobe Scan 01042021 - CompressedKartik ShuklaNo ratings yet

- Auto TestDocument3 pagesAuto TestMaree AlShehriNo ratings yet

- Lucy Wanjiru Offer LetterDocument2 pagesLucy Wanjiru Offer Letterart lewyNo ratings yet

- Ilovepdf MergedDocument2 pagesIlovepdf MergedVikash ShahNo ratings yet

- Atria Convergence Technologies Limited, Due Date: 15/03/2020Document2 pagesAtria Convergence Technologies Limited, Due Date: 15/03/2020Bharadwaj SubramaniamNo ratings yet

- HD 10155Document227 pagesHD 10155Varun BatraNo ratings yet

- 1684303940-ITA No.1070-D-2022 - Havells India LTDDocument5 pages1684303940-ITA No.1070-D-2022 - Havells India LTDArulnidhi Ramanathan SeshanNo ratings yet

- Bill 446 - MoulyaDocument1 pageBill 446 - MoulyaRajesh RajNo ratings yet

- Mr. Bhanu Prakash Demand LetterDocument2 pagesMr. Bhanu Prakash Demand LetterBhanu PrakashNo ratings yet

- Terms Conditions Tpi Chennai 12TH Oct To 15TH Oct 2022Document6 pagesTerms Conditions Tpi Chennai 12TH Oct To 15TH Oct 2022Etrans 9No ratings yet

- Syonira Invecasts - Approved RPDocument32 pagesSyonira Invecasts - Approved RPyasahitabhardwajNo ratings yet

- Interpretation of Exermption NotfDocument4 pagesInterpretation of Exermption NotfSabrina CanoNo ratings yet

- An Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersFrom EverandAn Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersNo ratings yet

- Free Zone Persons - DDocument135 pagesFree Zone Persons - DSangeetha NaharNo ratings yet

- Aurtus Flash Alert 1714458676Document3 pagesAurtus Flash Alert 1714458676Sangeetha NaharNo ratings yet

- EY Washington Dispatch 1715448186Document8 pagesEY Washington Dispatch 1715448186Sangeetha NaharNo ratings yet

- SPOM TestDocument1 pageSPOM TestSangeetha NaharNo ratings yet

- Philippine Politics and Governance The Legislative BranchDocument18 pagesPhilippine Politics and Governance The Legislative BranchRussell SanicoNo ratings yet

- Ra 8294Document2 pagesRa 8294Rio TolentinoNo ratings yet

- 14) Belgica Vs Executive Secretary Paquito OchoaDocument281 pages14) Belgica Vs Executive Secretary Paquito OchoaMary Joyce Lacambra AquinoNo ratings yet

- Republic Vs Judge HidalgoDocument16 pagesRepublic Vs Judge HidalgoMikkoletNo ratings yet

- Cert II in Security Operations Instructor Lesson Plan TemplateDocument20 pagesCert II in Security Operations Instructor Lesson Plan TemplateSoke1No ratings yet

- Policarpio v. SalamatDocument5 pagesPolicarpio v. SalamatraykarloBNo ratings yet

- PEOPLE vs. GO PINDocument2 pagesPEOPLE vs. GO PINKristela AdraincemNo ratings yet

- Demafelis vs. CADocument6 pagesDemafelis vs. CAXryn MortelNo ratings yet

- Seemaarshadzaheer&Orsvs Municipal Corporation of Greater (2006) 5 SCC 282Document22 pagesSeemaarshadzaheer&Orsvs Municipal Corporation of Greater (2006) 5 SCC 282sai kiran gudisevaNo ratings yet

- Juvenile Justice System Thesis StatementDocument11 pagesJuvenile Justice System Thesis Statementsarahmitchelllittlerock100% (2)

- Vda de Bataclan V MedinaDocument4 pagesVda de Bataclan V MedinaJulius ManaloNo ratings yet

- LGS 210Document308 pagesLGS 210Ahmad Shex MhamadNo ratings yet

- DK BASU VS STate of West BengalDocument14 pagesDK BASU VS STate of West BengalAbhinav Malik100% (3)

- Ra 9262 ConstitutionalityDocument2 pagesRa 9262 ConstitutionalityRyan JD LimNo ratings yet

- Festejo V Fernando (Eng)Document6 pagesFestejo V Fernando (Eng)UlNo ratings yet

- Citibank, N.A. vs. CADocument2 pagesCitibank, N.A. vs. CAJL A H-DimaculanganNo ratings yet

- G. Sabio v. Gordon 504 SCRA 704Document2 pagesG. Sabio v. Gordon 504 SCRA 704mj lopezNo ratings yet

- 6 Heirs of Peter Donton Vs StierDocument18 pages6 Heirs of Peter Donton Vs StierClive HendelsonNo ratings yet

- CIR V ReyesDocument4 pagesCIR V ReyesAndrea GatchalianNo ratings yet

- Syllabus CRPCDocument5 pagesSyllabus CRPCksvv prasadNo ratings yet

- 09 Orbos v. BungubungDocument4 pages09 Orbos v. BungubungAlec VenturaNo ratings yet

- Sec.41 of CR - PCDocument7 pagesSec.41 of CR - PCDesai Sharath KumarNo ratings yet

- 1610 Tax Insight - Tech Mahindra LTDDocument3 pages1610 Tax Insight - Tech Mahindra LTDAlpa Shah DesaiNo ratings yet

- Felix E. Mendiola For PetitionerDocument3 pagesFelix E. Mendiola For PetitionerRosalie CastroNo ratings yet

- Loadmasters Customs Services V Glodel Brokerage - 639 SCRA 69Document14 pagesLoadmasters Customs Services V Glodel Brokerage - 639 SCRA 69Krista YntigNo ratings yet

- Application For Authorization of A Class ActionDocument18 pagesApplication For Authorization of A Class ActionNunatsiaqNewsNo ratings yet

- Faceless Appeals Conceptual Framework 110323 PDFDocument134 pagesFaceless Appeals Conceptual Framework 110323 PDFVishwas PatilNo ratings yet