Bca Fam Unit 1

Bca Fam Unit 1

You might also like

- Full Download Ebook PDF Organization Development The Process of Leading Organizational Change 5th Edition PDFDocument35 pagesFull Download Ebook PDF Organization Development The Process of Leading Organizational Change 5th Edition PDFlibby.carr50692% (49)

- QuintoAndar - Series D Pitch Deck Vfinal - May 16, 2019Document40 pagesQuintoAndar - Series D Pitch Deck Vfinal - May 16, 2019Cesar Mendes Junior100% (9)

- Digital Marketing Strategy Implementation and Prac 220825 185854Document124 pagesDigital Marketing Strategy Implementation and Prac 220825 185854Clarah Kusuta100% (3)

- Annexure A - Draft Formal Report - Agst Knysna Mun - Procurement From Knysna T..Document50 pagesAnnexure A - Draft Formal Report - Agst Knysna Mun - Procurement From Knysna T..Sune Payne- Daily MaverickNo ratings yet

- B.C.A Accounting 1st Chapter NotesDocument18 pagesB.C.A Accounting 1st Chapter Notesrakesh87% (23)

- Computer Application II (CICT)Document91 pagesComputer Application II (CICT)Redemta TanuiNo ratings yet

- Chapter 1 - Introduction To AccountingDocument18 pagesChapter 1 - Introduction To AccountingPaiNo ratings yet

- انجليزية 2 كاملDocument29 pagesانجليزية 2 كاملsaleh.01chfNo ratings yet

- BinitaDocument9 pagesBinitaNishan magarNo ratings yet

- Introduction To AccountingDocument16 pagesIntroduction To AccountingPiyushNo ratings yet

- Accounts Project by Abhinav Mishra 11cDocument29 pagesAccounts Project by Abhinav Mishra 11cspam accNo ratings yet

- Finance Material 1Document7 pagesFinance Material 1keerthanaNo ratings yet

- 1Q) What Is Accounting State Its ObjectivesDocument9 pages1Q) What Is Accounting State Its ObjectivesMd FerozNo ratings yet

- 1&2 Lecture Fundamentals of AccountingDocument5 pages1&2 Lecture Fundamentals of Accountingzukhrufeman64No ratings yet

- Chapter 1 Introduction To Accounting PDFDocument18 pagesChapter 1 Introduction To Accounting PDFHussain DilawerNo ratings yet

- AccountingDocument25 pagesAccountinganjalichaubey021No ratings yet

- Basic Accounting NotesDocument43 pagesBasic Accounting Notesgreatkhali33654No ratings yet

- CH - 1 Intro To AccountsDocument55 pagesCH - 1 Intro To Accountschallengekiller01No ratings yet

- Accounting IntroDocument33 pagesAccounting IntroShaji RarothNo ratings yet

- FOA & FOC NotesDocument47 pagesFOA & FOC Notes012AKHILA VIGNESHNo ratings yet

- CMA Foundation (Accounts) by CA Mohit RohraDocument341 pagesCMA Foundation (Accounts) by CA Mohit Rohramalltushar975No ratings yet

- Introduction FADocument28 pagesIntroduction FAShrestha MohantyNo ratings yet

- 61a6cbec682c8 - Book Keeping and AccountingDocument16 pages61a6cbec682c8 - Book Keeping and AccountingAnuska ThapaNo ratings yet

- Finance Study Unit 1Document9 pagesFinance Study Unit 1aman pandeyNo ratings yet

- Accounting Notes PDFDocument67 pagesAccounting Notes PDFEjazAhmadNo ratings yet

- Introduction of AccountingDocument26 pagesIntroduction of AccountingMelboure VishalNo ratings yet

- Study Note 1 Fundamental of AccountingDocument54 pagesStudy Note 1 Fundamental of Accountingnaga naveenNo ratings yet

- Chapter 1 AccountingDocument9 pagesChapter 1 Accounting私はアムリーですUnniyarchaNo ratings yet

- 1571229837unit 1 Introduction To Accounting and FinanceDocument17 pages1571229837unit 1 Introduction To Accounting and FinancePhonepaxa PhoumbundithNo ratings yet

- Chapter 1Document50 pagesChapter 1sujal sikariyaNo ratings yet

- ACN AccountDocument48 pagesACN AccountAswin AcharyaNo ratings yet

- CBSE Quick Revision Notes and Chapter Summary: Class-11 Accountancy Chapter 1 - Introduction To AccountingDocument6 pagesCBSE Quick Revision Notes and Chapter Summary: Class-11 Accountancy Chapter 1 - Introduction To AccountingSai Surya Stallone50% (2)

- Accountancy BookDocument534 pagesAccountancy BookAshuNo ratings yet

- L1 - Introduction To Financial Accounting (FA)Document20 pagesL1 - Introduction To Financial Accounting (FA)JosephNo ratings yet

- Unit-I FA-IDocument20 pagesUnit-I FA-IpramikaNo ratings yet

- Introduction To AccountingDocument17 pagesIntroduction To AccountingjatinneysasinghNo ratings yet

- BaaccenDocument4 pagesBaaccenshylabaguio15No ratings yet

- Siva Sivani: Institute of ManagementDocument16 pagesSiva Sivani: Institute of ManagementjettycspNo ratings yet

- Unit 1 AFMDocument26 pagesUnit 1 AFMRenu KulkarniNo ratings yet

- Accounting+ Chapter 1Document21 pagesAccounting+ Chapter 1pronab kumarNo ratings yet

- Accountancy Summary Notes Class 11Document34 pagesAccountancy Summary Notes Class 11mamta.bdvrrmaNo ratings yet

- Accounting For Managers (AFM)Document100 pagesAccounting For Managers (AFM)Mansi Sharma100% (1)

- Accounting 1Document25 pagesAccounting 1Harsh RanjanNo ratings yet

- Financial AnalysisDocument30 pagesFinancial AnalysissrinivasanscribdNo ratings yet

- Financial Accounts Complete Notes-1Document113 pagesFinancial Accounts Complete Notes-1sharmaaditya20041122No ratings yet

- UNIT-1 AccountsDocument34 pagesUNIT-1 AccountsPiyush KumarNo ratings yet

- AccountingDocument15 pagesAccountingGohil HiralNo ratings yet

- Overview On Accounting and Book KeepingDocument5 pagesOverview On Accounting and Book Keepingkatherin peralta cruzNo ratings yet

- Fundamentels of Accounting Lect 1Document9 pagesFundamentels of Accounting Lect 1Jahanzaib ButtNo ratings yet

- Financial AccountingDocument20 pagesFinancial AccountingShangh PeterNo ratings yet

- Lesson 1 For Master 1 AccoDocument3 pagesLesson 1 For Master 1 AccomenasriaachrefwalaaddineNo ratings yet

- Chapter OneDocument75 pagesChapter Onerolex190703No ratings yet

- Accounting Process and Cost Volume Profit AnalysisDocument19 pagesAccounting Process and Cost Volume Profit AnalysisArafat KhanNo ratings yet

- Sba 1102Document87 pagesSba 1102LogeshNo ratings yet

- Notes On Introduction To AccountingDocument6 pagesNotes On Introduction To AccountingChaaru VarshiniNo ratings yet

- Accounting ProcessDocument53 pagesAccounting ProcessAlPHA NiNjANo ratings yet

- AccountsDocument147 pagesAccountsKrishna BambaNo ratings yet

- Class 11 Accountancy 2024-25 Notes Chapter 1 Introduction of Accounting - RemovedDocument26 pagesClass 11 Accountancy 2024-25 Notes Chapter 1 Introduction of Accounting - RemovedROHIT PAREEKNo ratings yet

- Rohit Yadav 55Document7 pagesRohit Yadav 55Sameer ChoudharyNo ratings yet

- GAURAVDocument12 pagesGAURAVSaurabh MishraNo ratings yet

- Accountancy Class Xi: Chapter-1 Introduction of AccountingDocument10 pagesAccountancy Class Xi: Chapter-1 Introduction of AccountingRohit VermaNo ratings yet

- Financial Accounting and Analysis: Unit-1Document71 pagesFinancial Accounting and Analysis: Unit-1subham singhNo ratings yet

- Definition of AccountingDocument2 pagesDefinition of Accountingkiara maeNo ratings yet

- Hospitality Conversion ChecklistDocument7 pagesHospitality Conversion ChecklistИгорь МореходовNo ratings yet

- DHBVNDocument4 pagesDHBVNAshok SharmaNo ratings yet

- TDS RatesDocument1 pageTDS Ratespankaj_adv5314No ratings yet

- State The Reasons Behind The Failure of Xerox and NokiaDocument4 pagesState The Reasons Behind The Failure of Xerox and NokiaSyed NomanNo ratings yet

- Specification For PermitDocument3 pagesSpecification For PermitErnie ConcepcionNo ratings yet

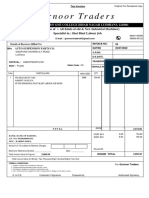

- Gurnoor Traders: Sale & Purchase Of:-All Kinds of Old & New Industrial Machinery Specialist In: Shot Blast Labour JobDocument1 pageGurnoor Traders: Sale & Purchase Of:-All Kinds of Old & New Industrial Machinery Specialist In: Shot Blast Labour JobANMOLNo ratings yet

- dsm08 ModeltalkDocument7 pagesdsm08 ModeltalkAtzmon_HentovNo ratings yet

- A Prep Guide For Case InterviewsDocument56 pagesA Prep Guide For Case InterviewsVikramAditya Kumar TanejaNo ratings yet

- Capstone Project Final 2Document52 pagesCapstone Project Final 2priyankaNo ratings yet

- QSCM Upto 1st I.A.Document10 pagesQSCM Upto 1st I.A.Md.saifaadil AttarNo ratings yet

- Service Design Itil v3Document1 pageService Design Itil v3Afif Kamal FiskaNo ratings yet

- Vidadi ƏlizadəDocument9 pagesVidadi ƏlizadəChingiz QarayevNo ratings yet

- Agile, CMMI, Rup, ISO/IEC 12207... Is There A Method in This Madness?Document5 pagesAgile, CMMI, Rup, ISO/IEC 12207... Is There A Method in This Madness?Segundo Fidel Puerto GaravitoNo ratings yet

- CRJ and CPJ Template 2Document6 pagesCRJ and CPJ Template 2amme katrinaNo ratings yet

- Drug War II Public CitizenDocument51 pagesDrug War II Public CitizenGaby ArguedasNo ratings yet

- De Leon, Patricia A - RESUMEDocument2 pagesDe Leon, Patricia A - RESUMEDe Leon Patricia A.No ratings yet

- TLE CSS Grade10 Quarter3 Week6Document2 pagesTLE CSS Grade10 Quarter3 Week6Axel Nicerio RoveloNo ratings yet

- Options, Futures, and Other Derivatives, 8th Edition, 1Document65 pagesOptions, Futures, and Other Derivatives, 8th Edition, 1Mohammed NajihNo ratings yet

- Final Assignment: Code: 3 Lecturer's SignatureDocument2 pagesFinal Assignment: Code: 3 Lecturer's SignatureBạn Đại Vui TínhNo ratings yet

- LAS w3Document6 pagesLAS w3Pats MinaoNo ratings yet

- Qubole Open Data Lake Platform Aws Ra PDFDocument1 pageQubole Open Data Lake Platform Aws Ra PDFwiredfrombackNo ratings yet

- BS NOTES Kombaz-1Document331 pagesBS NOTES Kombaz-1tiller kambanjeNo ratings yet

- Eng - Osama BadrDocument3 pagesEng - Osama BadrAmr GodaNo ratings yet

- 5.2 Manajemen OrganisasiDocument12 pages5.2 Manajemen OrganisasiMochammad HafizhNo ratings yet

- Propell L&R Practice Test READING PART 5Document4 pagesPropell L&R Practice Test READING PART 5Kim HyeinNo ratings yet

- 175 Charlotte LietaerDocument15 pages175 Charlotte LietaerKen BulkoNo ratings yet

Download as pdf or txt

You might also like

- Full Download Ebook PDF Organization Development The Process of Leading Organizational Change 5th Edition PDFDocument35 pagesFull Download Ebook PDF Organization Development The Process of Leading Organizational Change 5th Edition PDFlibby.carr50692% (49)

- QuintoAndar - Series D Pitch Deck Vfinal - May 16, 2019Document40 pagesQuintoAndar - Series D Pitch Deck Vfinal - May 16, 2019Cesar Mendes Junior100% (9)

- Digital Marketing Strategy Implementation and Prac 220825 185854Document124 pagesDigital Marketing Strategy Implementation and Prac 220825 185854Clarah Kusuta100% (3)

- Annexure A - Draft Formal Report - Agst Knysna Mun - Procurement From Knysna T..Document50 pagesAnnexure A - Draft Formal Report - Agst Knysna Mun - Procurement From Knysna T..Sune Payne- Daily MaverickNo ratings yet

- B.C.A Accounting 1st Chapter NotesDocument18 pagesB.C.A Accounting 1st Chapter Notesrakesh87% (23)

- Computer Application II (CICT)Document91 pagesComputer Application II (CICT)Redemta TanuiNo ratings yet

- Chapter 1 - Introduction To AccountingDocument18 pagesChapter 1 - Introduction To AccountingPaiNo ratings yet

- انجليزية 2 كاملDocument29 pagesانجليزية 2 كاملsaleh.01chfNo ratings yet

- BinitaDocument9 pagesBinitaNishan magarNo ratings yet

- Introduction To AccountingDocument16 pagesIntroduction To AccountingPiyushNo ratings yet

- Accounts Project by Abhinav Mishra 11cDocument29 pagesAccounts Project by Abhinav Mishra 11cspam accNo ratings yet

- Finance Material 1Document7 pagesFinance Material 1keerthanaNo ratings yet

- 1Q) What Is Accounting State Its ObjectivesDocument9 pages1Q) What Is Accounting State Its ObjectivesMd FerozNo ratings yet

- 1&2 Lecture Fundamentals of AccountingDocument5 pages1&2 Lecture Fundamentals of Accountingzukhrufeman64No ratings yet

- Chapter 1 Introduction To Accounting PDFDocument18 pagesChapter 1 Introduction To Accounting PDFHussain DilawerNo ratings yet

- AccountingDocument25 pagesAccountinganjalichaubey021No ratings yet

- Basic Accounting NotesDocument43 pagesBasic Accounting Notesgreatkhali33654No ratings yet

- CH - 1 Intro To AccountsDocument55 pagesCH - 1 Intro To Accountschallengekiller01No ratings yet

- Accounting IntroDocument33 pagesAccounting IntroShaji RarothNo ratings yet

- FOA & FOC NotesDocument47 pagesFOA & FOC Notes012AKHILA VIGNESHNo ratings yet

- CMA Foundation (Accounts) by CA Mohit RohraDocument341 pagesCMA Foundation (Accounts) by CA Mohit Rohramalltushar975No ratings yet

- Introduction FADocument28 pagesIntroduction FAShrestha MohantyNo ratings yet

- 61a6cbec682c8 - Book Keeping and AccountingDocument16 pages61a6cbec682c8 - Book Keeping and AccountingAnuska ThapaNo ratings yet

- Finance Study Unit 1Document9 pagesFinance Study Unit 1aman pandeyNo ratings yet

- Accounting Notes PDFDocument67 pagesAccounting Notes PDFEjazAhmadNo ratings yet

- Introduction of AccountingDocument26 pagesIntroduction of AccountingMelboure VishalNo ratings yet

- Study Note 1 Fundamental of AccountingDocument54 pagesStudy Note 1 Fundamental of Accountingnaga naveenNo ratings yet

- Chapter 1 AccountingDocument9 pagesChapter 1 Accounting私はアムリーですUnniyarchaNo ratings yet

- 1571229837unit 1 Introduction To Accounting and FinanceDocument17 pages1571229837unit 1 Introduction To Accounting and FinancePhonepaxa PhoumbundithNo ratings yet

- Chapter 1Document50 pagesChapter 1sujal sikariyaNo ratings yet

- ACN AccountDocument48 pagesACN AccountAswin AcharyaNo ratings yet

- CBSE Quick Revision Notes and Chapter Summary: Class-11 Accountancy Chapter 1 - Introduction To AccountingDocument6 pagesCBSE Quick Revision Notes and Chapter Summary: Class-11 Accountancy Chapter 1 - Introduction To AccountingSai Surya Stallone50% (2)

- Accountancy BookDocument534 pagesAccountancy BookAshuNo ratings yet

- L1 - Introduction To Financial Accounting (FA)Document20 pagesL1 - Introduction To Financial Accounting (FA)JosephNo ratings yet

- Unit-I FA-IDocument20 pagesUnit-I FA-IpramikaNo ratings yet

- Introduction To AccountingDocument17 pagesIntroduction To AccountingjatinneysasinghNo ratings yet

- BaaccenDocument4 pagesBaaccenshylabaguio15No ratings yet

- Siva Sivani: Institute of ManagementDocument16 pagesSiva Sivani: Institute of ManagementjettycspNo ratings yet

- Unit 1 AFMDocument26 pagesUnit 1 AFMRenu KulkarniNo ratings yet

- Accounting+ Chapter 1Document21 pagesAccounting+ Chapter 1pronab kumarNo ratings yet

- Accountancy Summary Notes Class 11Document34 pagesAccountancy Summary Notes Class 11mamta.bdvrrmaNo ratings yet

- Accounting For Managers (AFM)Document100 pagesAccounting For Managers (AFM)Mansi Sharma100% (1)

- Accounting 1Document25 pagesAccounting 1Harsh RanjanNo ratings yet

- Financial AnalysisDocument30 pagesFinancial AnalysissrinivasanscribdNo ratings yet

- Financial Accounts Complete Notes-1Document113 pagesFinancial Accounts Complete Notes-1sharmaaditya20041122No ratings yet

- UNIT-1 AccountsDocument34 pagesUNIT-1 AccountsPiyush KumarNo ratings yet

- AccountingDocument15 pagesAccountingGohil HiralNo ratings yet

- Overview On Accounting and Book KeepingDocument5 pagesOverview On Accounting and Book Keepingkatherin peralta cruzNo ratings yet

- Fundamentels of Accounting Lect 1Document9 pagesFundamentels of Accounting Lect 1Jahanzaib ButtNo ratings yet

- Financial AccountingDocument20 pagesFinancial AccountingShangh PeterNo ratings yet

- Lesson 1 For Master 1 AccoDocument3 pagesLesson 1 For Master 1 AccomenasriaachrefwalaaddineNo ratings yet

- Chapter OneDocument75 pagesChapter Onerolex190703No ratings yet

- Accounting Process and Cost Volume Profit AnalysisDocument19 pagesAccounting Process and Cost Volume Profit AnalysisArafat KhanNo ratings yet

- Sba 1102Document87 pagesSba 1102LogeshNo ratings yet

- Notes On Introduction To AccountingDocument6 pagesNotes On Introduction To AccountingChaaru VarshiniNo ratings yet

- Accounting ProcessDocument53 pagesAccounting ProcessAlPHA NiNjANo ratings yet

- AccountsDocument147 pagesAccountsKrishna BambaNo ratings yet

- Class 11 Accountancy 2024-25 Notes Chapter 1 Introduction of Accounting - RemovedDocument26 pagesClass 11 Accountancy 2024-25 Notes Chapter 1 Introduction of Accounting - RemovedROHIT PAREEKNo ratings yet

- Rohit Yadav 55Document7 pagesRohit Yadav 55Sameer ChoudharyNo ratings yet

- GAURAVDocument12 pagesGAURAVSaurabh MishraNo ratings yet

- Accountancy Class Xi: Chapter-1 Introduction of AccountingDocument10 pagesAccountancy Class Xi: Chapter-1 Introduction of AccountingRohit VermaNo ratings yet

- Financial Accounting and Analysis: Unit-1Document71 pagesFinancial Accounting and Analysis: Unit-1subham singhNo ratings yet

- Definition of AccountingDocument2 pagesDefinition of Accountingkiara maeNo ratings yet

- Hospitality Conversion ChecklistDocument7 pagesHospitality Conversion ChecklistИгорь МореходовNo ratings yet

- DHBVNDocument4 pagesDHBVNAshok SharmaNo ratings yet

- TDS RatesDocument1 pageTDS Ratespankaj_adv5314No ratings yet

- State The Reasons Behind The Failure of Xerox and NokiaDocument4 pagesState The Reasons Behind The Failure of Xerox and NokiaSyed NomanNo ratings yet

- Specification For PermitDocument3 pagesSpecification For PermitErnie ConcepcionNo ratings yet

- Gurnoor Traders: Sale & Purchase Of:-All Kinds of Old & New Industrial Machinery Specialist In: Shot Blast Labour JobDocument1 pageGurnoor Traders: Sale & Purchase Of:-All Kinds of Old & New Industrial Machinery Specialist In: Shot Blast Labour JobANMOLNo ratings yet

- dsm08 ModeltalkDocument7 pagesdsm08 ModeltalkAtzmon_HentovNo ratings yet

- A Prep Guide For Case InterviewsDocument56 pagesA Prep Guide For Case InterviewsVikramAditya Kumar TanejaNo ratings yet

- Capstone Project Final 2Document52 pagesCapstone Project Final 2priyankaNo ratings yet

- QSCM Upto 1st I.A.Document10 pagesQSCM Upto 1st I.A.Md.saifaadil AttarNo ratings yet

- Service Design Itil v3Document1 pageService Design Itil v3Afif Kamal FiskaNo ratings yet

- Vidadi ƏlizadəDocument9 pagesVidadi ƏlizadəChingiz QarayevNo ratings yet

- Agile, CMMI, Rup, ISO/IEC 12207... Is There A Method in This Madness?Document5 pagesAgile, CMMI, Rup, ISO/IEC 12207... Is There A Method in This Madness?Segundo Fidel Puerto GaravitoNo ratings yet

- CRJ and CPJ Template 2Document6 pagesCRJ and CPJ Template 2amme katrinaNo ratings yet

- Drug War II Public CitizenDocument51 pagesDrug War II Public CitizenGaby ArguedasNo ratings yet

- De Leon, Patricia A - RESUMEDocument2 pagesDe Leon, Patricia A - RESUMEDe Leon Patricia A.No ratings yet

- TLE CSS Grade10 Quarter3 Week6Document2 pagesTLE CSS Grade10 Quarter3 Week6Axel Nicerio RoveloNo ratings yet

- Options, Futures, and Other Derivatives, 8th Edition, 1Document65 pagesOptions, Futures, and Other Derivatives, 8th Edition, 1Mohammed NajihNo ratings yet

- Final Assignment: Code: 3 Lecturer's SignatureDocument2 pagesFinal Assignment: Code: 3 Lecturer's SignatureBạn Đại Vui TínhNo ratings yet

- LAS w3Document6 pagesLAS w3Pats MinaoNo ratings yet

- Qubole Open Data Lake Platform Aws Ra PDFDocument1 pageQubole Open Data Lake Platform Aws Ra PDFwiredfrombackNo ratings yet

- BS NOTES Kombaz-1Document331 pagesBS NOTES Kombaz-1tiller kambanjeNo ratings yet

- Eng - Osama BadrDocument3 pagesEng - Osama BadrAmr GodaNo ratings yet

- 5.2 Manajemen OrganisasiDocument12 pages5.2 Manajemen OrganisasiMochammad HafizhNo ratings yet

- Propell L&R Practice Test READING PART 5Document4 pagesPropell L&R Practice Test READING PART 5Kim HyeinNo ratings yet

- 175 Charlotte LietaerDocument15 pages175 Charlotte LietaerKen BulkoNo ratings yet