Download as docx, pdf, or txt

You might also like

- Financial Accounting Reviewer - Chapter 55Document9 pagesFinancial Accounting Reviewer - Chapter 55Coursehero PremiumNo ratings yet

- Financial Modeling John MoschellaDocument175 pagesFinancial Modeling John MoschellaNgọc Ngọc100% (2)

- Production Concept Extra Problems PDFDocument1 pageProduction Concept Extra Problems PDFRami AbdelaalNo ratings yet

- Financial Accounting and Reporting: Blank PageDocument28 pagesFinancial Accounting and Reporting: Blank PageMehtab NaqviNo ratings yet

- Mock TestDocument2 pagesMock Test123honglinh1234No ratings yet

- Mock Exam Paper - 28 - April - 2022Document3 pagesMock Exam Paper - 28 - April - 2022dilinhtinh04No ratings yet

- Today Agenda: What Is A Project?Document9 pagesToday Agenda: What Is A Project?Nouman SheikhNo ratings yet

- Neon Sign BoardsDocument9 pagesNeon Sign Boardsbantibhai0770No ratings yet

- 2023 OctDocument11 pages2023 OctChandani FernandoNo ratings yet

- BMS College of Engineering, Bangalore-560019: December 2016 Semester End Main ExaminationsDocument3 pagesBMS College of Engineering, Bangalore-560019: December 2016 Semester End Main Examinationshemavathi jayNo ratings yet

- Air Bubble PackingDocument9 pagesAir Bubble PackingSneha Sagar SharmaNo ratings yet

- Singapore Institute of Management: University of London Preliminary Exam 2015Document10 pagesSingapore Institute of Management: University of London Preliminary Exam 2015Pei TingNo ratings yet

- Project Profile On Manufacturing of Palm PlateDocument9 pagesProject Profile On Manufacturing of Palm PlateGangaraboina Praveen MudirajNo ratings yet

- Engineering EcoDocument26 pagesEngineering EcoEric John Enriquez100% (2)

- Cost Accounting: T I C A PDocument6 pagesCost Accounting: T I C A PShehrozSTNo ratings yet

- Handout Standard ABC and PERTDocument3 pagesHandout Standard ABC and PERTdarlenexjoyceNo ratings yet

- Cost Accounting985 Cxa9nf2nks PDFDocument6 pagesCost Accounting985 Cxa9nf2nks PDFjay gargNo ratings yet

- CA Final - CA Inter - CA IPCC - CA Foundation Online Test SeriesDocument17 pagesCA Final - CA Inter - CA IPCC - CA Foundation Online Test SeriesAyush ThÃkkarNo ratings yet

- Infosys LTD Standalone Audit Report To Shareholders For FY 2019Document3 pagesInfosys LTD Standalone Audit Report To Shareholders For FY 2019Sundarasudarsan RengarajanNo ratings yet

- Answer: (D) : C(S) G(S) - + y R e UDocument12 pagesAnswer: (D) : C(S) G(S) - + y R e USiddheswar BiswalNo ratings yet

- Cost and Management Accounting RTP CAP-III June 2016Document43 pagesCost and Management Accounting RTP CAP-III June 2016Artha sarokarNo ratings yet

- P2-Q and As-Advanced Management Accounting - June 2010 Dec 2010 and June 2011Document95 pagesP2-Q and As-Advanced Management Accounting - June 2010 Dec 2010 and June 2011HAbbunoNo ratings yet

- Automobile Body Building (Bus Body) : Sl. No. Activity Period (In Weeks)Document8 pagesAutomobile Body Building (Bus Body) : Sl. No. Activity Period (In Weeks)Ajit ChauhanNo ratings yet

- Skans School of Accountancy Cost & Management AccountingDocument3 pagesSkans School of Accountancy Cost & Management AccountingmaryNo ratings yet

- Engineering Economy AssignmentDocument1 pageEngineering Economy Assignmentprateekagrawal812004No ratings yet

- Engg Econ QuestionsDocument7 pagesEngg Econ QuestionsSherwin Dela CruzzNo ratings yet

- Topic 2 Cost Concepts and Analysis HandoutsDocument5 pagesTopic 2 Cost Concepts and Analysis HandoutsJohn Kenneth ColarinaNo ratings yet

- CMA QN August 2018Document7 pagesCMA QN August 2018Goremushandu MungarevaniNo ratings yet

- Factory OverheadDocument2 pagesFactory Overheadenchantadia0% (1)

- Imp 2203 - Costing - Question PaperDocument5 pagesImp 2203 - Costing - Question PaperAnshit BahediaNo ratings yet

- Day 15 - CVP QuestionsDocument4 pagesDay 15 - CVP QuestionsRashmi Ranjan DashNo ratings yet

- Lecture 18Document30 pagesLecture 18Riaz Baloch NotezaiNo ratings yet

- Practice Questions For Cuac217Document11 pagesPractice Questions For Cuac217Tino MakoniNo ratings yet

- Practice Questions For Cuac217Document11 pagesPractice Questions For Cuac217Tino Makoni100% (1)

- T I C A P: HE Nstitute of Hartered Ccountants of AkistanDocument3 pagesT I C A P: HE Nstitute of Hartered Ccountants of AkistanShehrozSTNo ratings yet

- Tutor AkbiDocument1 pageTutor Akbielssa kurniaNo ratings yet

- 7894 Final GR 2 Paper 5 Cost Managementyear 2005Document60 pages7894 Final GR 2 Paper 5 Cost Managementyear 2005Tlm BhopalNo ratings yet

- Tutorial QuestionsDocument7 pagesTutorial Questionsrobinkaby06No ratings yet

- Capital Budgeting 2Document4 pagesCapital Budgeting 2rebecabeczNo ratings yet

- END Examination: Ques. L (A) (B) (8+7) Ques. 2 (A) (B)Document2 pagesEND Examination: Ques. L (A) (B) (8+7) Ques. 2 (A) (B)Lavi LakhotiaNo ratings yet

- Breakeven SPDocument9 pagesBreakeven SPBernard BaluyotNo ratings yet

- MSME Disposable SyringesDocument24 pagesMSME Disposable SyringesNaveenbabu SoundararajanNo ratings yet

- Cost Accounting 2013Document3 pagesCost Accounting 2013GuruKPO0% (1)

- Decision Making QuestionsDocument3 pagesDecision Making QuestionsOsama RiazNo ratings yet

- Project Proposal BriefDocument7 pagesProject Proposal BriefRama KrishnaNo ratings yet

- Problem-42: RequiredDocument7 pagesProblem-42: RequiredRADHIKA V HNo ratings yet

- Capital Allowance 2220Document58 pagesCapital Allowance 2220YanPing AngNo ratings yet

- Project Report Automatic Voltage Stabiliser: Prepared by Rihan Khalyani B.E. ElectricalDocument25 pagesProject Report Automatic Voltage Stabiliser: Prepared by Rihan Khalyani B.E. ElectricalIRVA KHALYANINo ratings yet

- IILM Institute For Higher Education: Assignment For All SectionsDocument4 pagesIILM Institute For Higher Education: Assignment For All SectionsRahul DuaNo ratings yet

- QP MBA FINANCIAL AND MANAGEMENT ACCOUNTING 803FI0C002 Trimester I Cjj8nC4tr8Document5 pagesQP MBA FINANCIAL AND MANAGEMENT ACCOUNTING 803FI0C002 Trimester I Cjj8nC4tr8Rushil JoshiNo ratings yet

- Practice Exam 2018Document16 pagesPractice Exam 2018Leon CzarneckiNo ratings yet

- Paper - 5: Advanced Management Accounting QuestionsDocument38 pagesPaper - 5: Advanced Management Accounting Questionsshubham singhNo ratings yet

- Project Profile On HDPE Pipes PDFDocument9 pagesProject Profile On HDPE Pipes PDFnoeNo ratings yet

- Project Profile On P.P ThermoformingDocument11 pagesProject Profile On P.P ThermoformingAnonymous NUn6MESxNo ratings yet

- CMA AssignmentDocument4 pagesCMA AssignmentniranjanaNo ratings yet

- Economy Problem Set 1Document4 pagesEconomy Problem Set 1jung biNo ratings yet

- Corrugated Boxes1Document8 pagesCorrugated Boxes1abhi050191No ratings yet

- S.No Particulars Old Machine Rs New Machine RsDocument2 pagesS.No Particulars Old Machine Rs New Machine RsnarunsankarNo ratings yet

- EnterprenuerDocument25 pagesEnterprenuerRAMESHKUMAR BNo ratings yet

- Shukla Hinaben TrusharkumarDocument8 pagesShukla Hinaben Trusharkumarrajesh patelNo ratings yet

- Waste to Energy in the Age of the Circular Economy: Compendium of Case Studies and Emerging TechnologiesFrom EverandWaste to Energy in the Age of the Circular Economy: Compendium of Case Studies and Emerging TechnologiesRating: 5 out of 5 stars5/5 (1)

- Acca f7 Course NotesDocument202 pagesAcca f7 Course NotessajedulNo ratings yet

- Managerial Economics AssignmentDocument5 pagesManagerial Economics AssignmentTrisha LionelNo ratings yet

- Accounting Standard 1Document14 pagesAccounting Standard 1Isiyaku AdoNo ratings yet

- Finance PROJECT REPORT ON "COMPARATIVE STUDY OF TOP THREE BANKS OF INDIA"Document32 pagesFinance PROJECT REPORT ON "COMPARATIVE STUDY OF TOP THREE BANKS OF INDIA"Deepika KalimuthuNo ratings yet

- Constant Capital Ghana Inflation Index UpdateDocument2 pagesConstant Capital Ghana Inflation Index UpdateKofikoduahNo ratings yet

- Swing Trading Simplified - Larry D SpearsDocument115 pagesSwing Trading Simplified - Larry D SpearsPedja100% (2)

- WB BRR 8495948180Document672 pagesWB BRR 8495948180Sandeep BorseNo ratings yet

- Synopsis - Cost of CapitalDocument2 pagesSynopsis - Cost of Capitalamsu sthNo ratings yet

- Cfin 6th Edition Besley Test BankDocument15 pagesCfin 6th Edition Besley Test Bankdrkevinlee03071984jki100% (32)

- Accounting Ratio - WPS OfficeDocument6 pagesAccounting Ratio - WPS OfficeRommel SalagubangNo ratings yet

- XH-H 3e PPT Chap05Document69 pagesXH-H 3e PPT Chap05An NhiênNo ratings yet

- NSBZDocument6 pagesNSBZKenncy100% (4)

- Sample of Fixed Asset ScheduleDocument1 pageSample of Fixed Asset ScheduleAnnie ChewNo ratings yet

- G1 6.4 Partnership - Amalgamation and Business PurchaseDocument15 pagesG1 6.4 Partnership - Amalgamation and Business Purchasesridhartks100% (2)

- Cost AccountingDocument6 pagesCost AccountingDorianne BorgNo ratings yet

- Grace Hesketh Is The Owner of An Extremely Successful DressDocument2 pagesGrace Hesketh Is The Owner of An Extremely Successful DressAmit PandeyNo ratings yet

- ACBP5121+w Assignment 2Document10 pagesACBP5121+w Assignment 2pillaynorman20No ratings yet

- Security Analysis and Portfolio Management by Rohini Singh 2018Document446 pagesSecurity Analysis and Portfolio Management by Rohini Singh 2018Aman Kumar SharanNo ratings yet

- Horizon Report & AccountsDocument252 pagesHorizon Report & AccountsCyrill Joyce Santelices EgualNo ratings yet

- Credit and TravelDocument14 pagesCredit and TravelrimantasjankusNo ratings yet

- 100x Baggers - 7 Stocks - Motilal - Oswal - Wealth - Creation - Study - 2009 - 2014Document68 pages100x Baggers - 7 Stocks - Motilal - Oswal - Wealth - Creation - Study - 2009 - 2014appujisNo ratings yet

- M&a 3Document25 pagesM&a 3Xavier Francis S. LutaloNo ratings yet

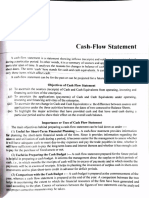

- Cash Flow Statements TheoryDocument16 pagesCash Flow Statements Theorysk9693092588No ratings yet

- Technopreneurship MCQsDocument11 pagesTechnopreneurship MCQsAndra GdlNo ratings yet

- 2016-6-29 Derivatives Oversight and Taxpayer Protection Act Bill TextDocument30 pages2016-6-29 Derivatives Oversight and Taxpayer Protection Act Bill TextMarkWarnerNo ratings yet

- Cpa 1Document2,011 pagesCpa 1mwanziaNo ratings yet

- BPI Short Term Fund - February 2024Document3 pagesBPI Short Term Fund - February 2024Nestor San AgustinNo ratings yet

- Maf620 FMC570Document8 pagesMaf620 FMC570ewinzeNo ratings yet