Download as pdf or txt

You might also like

- Panadyne International Sieve ChartDocument1 pagePanadyne International Sieve ChartSimanchal KarNo ratings yet

- Web Application Development Dos and DontsDocument18 pagesWeb Application Development Dos and Dontsaatish1No ratings yet

- Heavy Industries Corporation of Malaysia BerhadDocument6 pagesHeavy Industries Corporation of Malaysia BerhadInocencio Tiburcio100% (1)

- DieselDocument7 pagesDieselAbdulaziz Al OmarNo ratings yet

- BUMI Presentation - FY 2020 Earnings Call - 18 May 2021Document33 pagesBUMI Presentation - FY 2020 Earnings Call - 18 May 2021gns1234567890No ratings yet

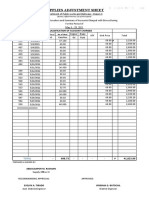

- Supplies Adjustment Sheet: Classification of Account ChargedDocument4 pagesSupplies Adjustment Sheet: Classification of Account Chargeddatla mamaNo ratings yet

- CW Performance UpdateDocument25 pagesCW Performance UpdateYunyong SungkhagornmanitNo ratings yet

- CMA - Sem 5 - Section B - WorkbookDocument47 pagesCMA - Sem 5 - Section B - WorkbookMohd AmanNo ratings yet

- Diseño de Un Open Pit Por Corrida: Primera Corrida Segunda CorridaDocument6 pagesDiseño de Un Open Pit Por Corrida: Primera Corrida Segunda CorridaDarwin Joan AvendañoNo ratings yet

- Rayon 1, 30 Juni 2021 Asman Areal & Budidaya 3Document4 pagesRayon 1, 30 Juni 2021 Asman Areal & Budidaya 3Jaya NegaraNo ratings yet

- Tableau Gratuit Heures de TravailDocument5 pagesTableau Gratuit Heures de Travailoumayma dallaNo ratings yet

- MamposteriaDocument9 pagesMamposteriaSteven F. EscuderoNo ratings yet

- Chem DBDocument17 pagesChem DBmd abNo ratings yet

- UTA-Cabling-Standards-Tieu Chuan Ve Cap Mang-Tu Cap MangDocument78 pagesUTA-Cabling-Standards-Tieu Chuan Ve Cap Mang-Tu Cap MangDũng Tiêu Lê AnhNo ratings yet

- Opname Format Baru SkaliDocument20 pagesOpname Format Baru Skaliedi subaliNo ratings yet

- BIMBSec Corp Day - 2022 Economic OutlookDocument17 pagesBIMBSec Corp Day - 2022 Economic Outlookmuhammad ihsanNo ratings yet

- Rekap LCM 20 Mei 2020Document24 pagesRekap LCM 20 Mei 2020yoga saktiNo ratings yet

- Aplikasi Analisis Ulangan Harian Kurikulum 2013 TerbaruDocument9 pagesAplikasi Analisis Ulangan Harian Kurikulum 2013 TerbaruDedi SuwitoNo ratings yet

- Consolidado Grupos Asignaturas OficioDocument5 pagesConsolidado Grupos Asignaturas Oficiojohn jairo martinez machadoNo ratings yet

- Domestic Performance To December 2023Document2 pagesDomestic Performance To December 2023tim chambersNo ratings yet

- Economic Highlights - Fuel and Sugar Prices Were Raised To Reduce - 16/7/2010Document3 pagesEconomic Highlights - Fuel and Sugar Prices Were Raised To Reduce - 16/7/2010Rhb InvestNo ratings yet

- Note On High PCI at BF2Document6 pagesNote On High PCI at BF2Sk BeheraNo ratings yet

- Razduzenje MK-3Document8 pagesRazduzenje MK-3Samir JoguncicNo ratings yet

- PT SiemonDocument87 pagesPT Siemonnova novitaNo ratings yet

- BOR 42.50% 79.59% Avlos 2.6 AVLOS 2.6 Hari TOI 35.87 35.56 BTO 9.48 10.26 BOR 79.59% Avlos TOI 35.56 Hari BTO 2.8 HariDocument4 pagesBOR 42.50% 79.59% Avlos 2.6 AVLOS 2.6 Hari TOI 35.87 35.56 BTO 9.48 10.26 BOR 79.59% Avlos TOI 35.56 Hari BTO 2.8 Hariwahyu romadhonNo ratings yet

- Telkom Indonesia (Persero) TBK PT ADR Rep 100 B (TLK)Document2 pagesTelkom Indonesia (Persero) TBK PT ADR Rep 100 B (TLK)Carlos FrancoNo ratings yet

- End of Hole PKSDocument3 pagesEnd of Hole PKSIkhlasul IhsanNo ratings yet

- Final Breeder Seed Indent For Rabi 2021-22 For PortalDocument16 pagesFinal Breeder Seed Indent For Rabi 2021-22 For PortalAvijitSinharoyNo ratings yet

- Dude Where Is My Stuff AmvDocument11 pagesDude Where Is My Stuff AmveweNo ratings yet

- Bill Evans Business Bank Economic Briefing-March 2023Document36 pagesBill Evans Business Bank Economic Briefing-March 2023chingweisuNo ratings yet

- Denah Pengembangan Unit C3-19 Alt.3 (R1)Document1 pageDenah Pengembangan Unit C3-19 Alt.3 (R1)eyangutioyeNo ratings yet

- !2 - Model - 13june2022 - Bronze - A+30000Document647 pages!2 - Model - 13june2022 - Bronze - A+30000TamereNo ratings yet

- Ret Transactions 09022021164505Document3 pagesRet Transactions 09022021164505Miroslav MilosevskiNo ratings yet

- Denah Pengembangan Unit C3-19 Alt.2 (R1)Document1 pageDenah Pengembangan Unit C3-19 Alt.2 (R1)eyangutioyeNo ratings yet

- Denah Pengembangan Unit c3-19 Alt.2 (r1)Document1 pageDenah Pengembangan Unit c3-19 Alt.2 (r1)eyangutioyeNo ratings yet

- Febuari 2020 Unilever SkinDocument379 pagesFebuari 2020 Unilever SkinAlvan AlvianNo ratings yet

- Mis Tabla de ApuestasDocument7 pagesMis Tabla de ApuestasDiegoNo ratings yet

- Controle de Ações Ricardo CampioloDocument15 pagesControle de Ações Ricardo CampioloRicardo CampioloNo ratings yet

- Laboratorium Mekanika Tanah Fakultas Teknik Universitas Syiah Kuala Cone Penetration TestDocument21 pagesLaboratorium Mekanika Tanah Fakultas Teknik Universitas Syiah Kuala Cone Penetration TestNabila FairuzNo ratings yet

- Opname Format BaruDocument14 pagesOpname Format Baruedi subaliNo ratings yet

- Report 115965 PDFDocument27 pagesReport 115965 PDFabbasamuNo ratings yet

- Programa Semanal 29 fertilizacion-TAEXDocument2 pagesPrograma Semanal 29 fertilizacion-TAEXJose CabreraNo ratings yet

- IA Crop Progress 11-29-21Document2 pagesIA Crop Progress 11-29-21Matt GunnNo ratings yet

- Corona Virus Cases USADocument3 pagesCorona Virus Cases USAIrakli SaliaNo ratings yet

- Purchase OrderDocument54 pagesPurchase OrderTuao United Builders Transport CooperativeNo ratings yet

- GEP June 2020 Chapter1 Fig1.1 1.10Document242 pagesGEP June 2020 Chapter1 Fig1.1 1.10Ronald Pally OrtizNo ratings yet

- Temperatura - Talha Linha 2Document7 pagesTemperatura - Talha Linha 2ANDERSONNo ratings yet

- Temperatura - Talha Linha 2Document7 pagesTemperatura - Talha Linha 2ANDERSONNo ratings yet

- Temperatura - Talha Linha 2Document7 pagesTemperatura - Talha Linha 2ANDERSONNo ratings yet

- Basketball Court LayoutDocument1 pageBasketball Court LayoutrichdaleofficeNo ratings yet

- Technical Background Cluster 2Document10 pagesTechnical Background Cluster 2khoerulNo ratings yet

- Baker Adhesives: Exhibit 1 - Novo Price Calculation On Initial OrderDocument16 pagesBaker Adhesives: Exhibit 1 - Novo Price Calculation On Initial Orderprabhjot SandhuNo ratings yet

- Backup Data PelaksanaanDocument6 pagesBackup Data PelaksanaanJoe HariantoNo ratings yet

- Devengados Vs Marco Inicial Y Sus Modificaciones - 2021 Del Mes de Enero A DiciembreDocument3 pagesDevengados Vs Marco Inicial Y Sus Modificaciones - 2021 Del Mes de Enero A DiciembreFredy Sihuinta HuamanNo ratings yet

- Water BillDocument13 pagesWater BillAilmus MaroNo ratings yet

- Reagen Stok 2Document41 pagesReagen Stok 2Laboratorium RSUMMNo ratings yet

- Denah Pondasi Batu KaliDocument1 pageDenah Pondasi Batu KaliHari SusantiNo ratings yet

- Kalim A. Siddiqui, Byco Petroleum. Petroleum Retail Market in PakistanDocument41 pagesKalim A. Siddiqui, Byco Petroleum. Petroleum Retail Market in PakistansyedqamarNo ratings yet

- Laporan Kehadiran Karyawan: Data Absensi Reguler Hari Libur Hari RayaDocument4 pagesLaporan Kehadiran Karyawan: Data Absensi Reguler Hari Libur Hari RayaBagus shellanNo ratings yet

- Overdue Status 28-02-21Document3 pagesOverdue Status 28-02-21HarsimranSinghNo ratings yet

- Jpnsbh400sip2022sbth-027 - SK Ladang Sungai Bendera, KinabatanganDocument15 pagesJpnsbh400sip2022sbth-027 - SK Ladang Sungai Bendera, KinabatanganCks ChongNo ratings yet

- Common Core Connections Math, Grade 2From EverandCommon Core Connections Math, Grade 2Rating: 3 out of 5 stars3/5 (1)

- H2 PsaDocument8 pagesH2 Psamohsen siahpooshNo ratings yet

- Pitch PropertDocument7 pagesPitch Propertmohsen siahpooshNo ratings yet

- Low Sulfur Fuel Oil SpecDocument3 pagesLow Sulfur Fuel Oil Specmohsen siahpooshNo ratings yet

- Carbon BLK SpecificationDocument2 pagesCarbon BLK Specificationmohsen siahpooshNo ratings yet

- Monk - Way of The Forbidden Art (v0.9)Document3 pagesMonk - Way of The Forbidden Art (v0.9)Andrés MasNo ratings yet

- Chương 3Document22 pagesChương 3Mai Duong ThiNo ratings yet

- To Find The Effect of Acids and Alkalies On Tensile Strength of Cotton, Silk and Wool Fibers.Document18 pagesTo Find The Effect of Acids and Alkalies On Tensile Strength of Cotton, Silk and Wool Fibers.Yogesh Singh100% (1)

- Pensioners BpsDocument8 pagesPensioners Bpsvna2971No ratings yet

- Case Study: Beverage Man Takes The PlungeDocument13 pagesCase Study: Beverage Man Takes The PlungeIkko100% (1)

- The Brightest Thing in The World: by Leah Nanako Winkler 1/3/23Document91 pagesThe Brightest Thing in The World: by Leah Nanako Winkler 1/3/23yx7cprjqg6No ratings yet

- ARTS 725-734, 748-749 Donation REVIEW23Document11 pagesARTS 725-734, 748-749 Donation REVIEW23Vikki AmorioNo ratings yet

- Gödel's Incompleteness ResultsDocument14 pagesGödel's Incompleteness ResultssupervenienceNo ratings yet

- Training DW PDFDocument31 pagesTraining DW PDFCeliaZurdoPerladoNo ratings yet

- TERM II FA1 PBL - Grade 4Document1 pageTERM II FA1 PBL - Grade 4toteefruitw.prNo ratings yet

- How To Study The Bible. A Guide To Studying and Interpreting The Holy Scriptures (PDFDrive)Document214 pagesHow To Study The Bible. A Guide To Studying and Interpreting The Holy Scriptures (PDFDrive)QSilvaNo ratings yet

- JohnsonEvinrude ElectricalDocument5 pagesJohnsonEvinrude Electricalwguenon100% (1)

- Africa-chadicMusey English French DictionaryDocument168 pagesAfrica-chadicMusey English French DictionaryJordiAlberca100% (2)

- Macroeconomics 1Document25 pagesMacroeconomics 1eunicemaraNo ratings yet

- Characteristics of Data WarehousingDocument5 pagesCharacteristics of Data WarehousingAnamika Rai PandeyNo ratings yet

- Bosch SpreadsDocument47 pagesBosch SpreadshtalibNo ratings yet

- Pyp Teacher Cover LetterDocument7 pagesPyp Teacher Cover Letterafjwdkwmdbqegq100% (2)

- Influenza: David E. Swayne and David A. HalvorsonDocument27 pagesInfluenza: David E. Swayne and David A. HalvorsonMelissa IvethNo ratings yet

- DLP Entrep Revised 102Document1 pageDLP Entrep Revised 102ClintNo ratings yet

- 1981 HHLDocument206 pages1981 HHLm.khurana093425No ratings yet

- Sancho Agapito Jackelin CarolDocument36 pagesSancho Agapito Jackelin CarolTeòfilo Quispe MedinaNo ratings yet

- 1 s2.0 S1751616123004368 MainDocument11 pages1 s2.0 S1751616123004368 MainMihai MihaiNo ratings yet

- Sea Me We 4Document14 pagesSea Me We 4Uditha MuthumalaNo ratings yet

- Broken When EnteringDocument17 pagesBroken When EnteringAbhilasha BagariyaNo ratings yet

- Hall Effect and Its ApplicationsDocument10 pagesHall Effect and Its ApplicationssenthilkumarNo ratings yet

- 4302 M.Sc. OBSTETRIC AND GYNAECOLOGICAL NURSINGDocument89 pages4302 M.Sc. OBSTETRIC AND GYNAECOLOGICAL NURSINGSteny Ann VargheseNo ratings yet

- Magic Cards - ShadowDocument2 pagesMagic Cards - ShadowLuis RodriguezNo ratings yet

- Garcia V GatchalianDocument2 pagesGarcia V GatchalianJasNo ratings yet