Download as pdf or txt

You might also like

- Acct2015 - 2021 Paper Final SolutionDocument128 pagesAcct2015 - 2021 Paper Final SolutionTan TaylorNo ratings yet

- Quiz 2.1 AccountingDocument4 pagesQuiz 2.1 AccountingColine DueñasNo ratings yet

- ParCor Chapter3 BuenaventuraDocument19 pagesParCor Chapter3 BuenaventuraAnonn100% (3)

- Consolidation FP ExampleDocument4 pagesConsolidation FP ExampleYoooNo ratings yet

- 4 3Document3 pages4 3ANDI TE'A MARI SIMBALANo ratings yet

- Seatwork Problem 1Document11 pagesSeatwork Problem 1Zihr EllerycNo ratings yet

- Chapter 3 Review AnswersDocument2 pagesChapter 3 Review Answersapi-358995037No ratings yet

- LiquidationDocument18 pagesLiquidationSamaica MontemayorNo ratings yet

- Semi Final AccountingDocument8 pagesSemi Final AccountingSherryl DumagpiNo ratings yet

- 3J's Farm Cash Priority Program For The Period Ended XXXXXDocument5 pages3J's Farm Cash Priority Program For The Period Ended XXXXXRicart Von LauretaNo ratings yet

- Review Midterm (MyAnswers)Document30 pagesReview Midterm (MyAnswers)Jester SarabiaNo ratings yet

- Partnership Liquidation Exam AnswersDocument7 pagesPartnership Liquidation Exam AnswersAlexandriteNo ratings yet

- Chapter 4 - Partnership Liquidation Practice ExercisesDocument3 pagesChapter 4 - Partnership Liquidation Practice ExercisessanjoeNo ratings yet

- Thornado Partnership Statement of Liquidation August 1, 2016 To October 31, 2016Document3 pagesThornado Partnership Statement of Liquidation August 1, 2016 To October 31, 2016Joannah maeNo ratings yet

- Statement of LiquidationDocument2 pagesStatement of LiquidationSherilyn BunagNo ratings yet

- Rosalie Balhag CleanersDocument1 pageRosalie Balhag CleanersDominique Abrajano100% (1)

- A 1. FormationDocument3 pagesA 1. Formationmartinfaith958No ratings yet

- Refat Mukmin - Asy 23Document7 pagesRefat Mukmin - Asy 232310102052.refatNo ratings yet

- MC Solution Pages 2 61 To 2 66Document8 pagesMC Solution Pages 2 61 To 2 66sumagpangkeannecleinNo ratings yet

- Worksheet Pr. 1 Chap 9Document4 pagesWorksheet Pr. 1 Chap 9airamaecsibbalucaNo ratings yet

- Solution of Assignment Eco-04 Case: Mike (The Plumber) - A True StoryDocument5 pagesSolution of Assignment Eco-04 Case: Mike (The Plumber) - A True StoryYusuf HusseinNo ratings yet

- Accum. Depreciation, Fur. & Fixture Merchandise Inventory Furniture & FixtureDocument6 pagesAccum. Depreciation, Fur. & Fixture Merchandise Inventory Furniture & FixtureJoana TrinidadNo ratings yet

- Problem 1 - Chavie CompanyDocument7 pagesProblem 1 - Chavie CompanyBeatrice TehNo ratings yet

- Name: Edmalyn R. Canton - BSA 1 - BE 302 Morning Subject/course: 892 - Acc 111 Activity 34Document6 pagesName: Edmalyn R. Canton - BSA 1 - BE 302 Morning Subject/course: 892 - Acc 111 Activity 34Adam CuencaNo ratings yet

- ABC Company Worksheet For The Year Ended December 31, 2019Document1 pageABC Company Worksheet For The Year Ended December 31, 2019Rosemarie VillanuevaNo ratings yet

- Partnership LiquidationDocument8 pagesPartnership LiquidationJhane XiNo ratings yet

- Septya Ayu Neraca Saldo KlasikDocument1 pageSeptya Ayu Neraca Saldo KlasikwongtawengtawengNo ratings yet

- Business Combination Illustration 2Document77 pagesBusiness Combination Illustration 2Ash CastroNo ratings yet

- Octane Anurag KarnavatiDocument25 pagesOctane Anurag KarnavatiPriyanka NemadeNo ratings yet

- Mahusay, Bsa 315, Module 1-CaseletsDocument9 pagesMahusay, Bsa 315, Module 1-CaseletsJeth MahusayNo ratings yet

- In Pesos Savings Account: Daily Weekly Monthly Annual Daily Weekly Monthly AnnuallyDocument2 pagesIn Pesos Savings Account: Daily Weekly Monthly Annual Daily Weekly Monthly AnnuallyDaisy jane cunananNo ratings yet

- HF Journal Entries PE BookDocument45 pagesHF Journal Entries PE BookManohar VejandlaNo ratings yet

- AccountsDocument4 pagesAccountsVencint LaranNo ratings yet

- Module 5 - With SolutionsDocument12 pagesModule 5 - With SolutionsStella MarieNo ratings yet

- Statement of LiquidationDocument13 pagesStatement of LiquidationnerieroseNo ratings yet

- REV AFAR2 - Partnership (Operation)Document10 pagesREV AFAR2 - Partnership (Operation)Richard LamagnaNo ratings yet

- ABC Company Acquired 100Document2 pagesABC Company Acquired 100Bas, Jammel BañaresNo ratings yet

- Problems On CFS & SFSDocument10 pagesProblems On CFS & SFSnawinarasaNo ratings yet

- Landing On You Travel ServicesDocument4 pagesLanding On You Travel ServicesAngelica EndrenalNo ratings yet

- Cash Flow Question Paper1 PDF FreeDocument10 pagesCash Flow Question Paper1 PDF Freelakshayajasuja2No ratings yet

- Accounting AssignmentDocument2 pagesAccounting AssignmentLloyd Lacabra SalagantinNo ratings yet

- Financial Accounting (Bbaw2103)Document10 pagesFinancial Accounting (Bbaw2103)tachaini2727No ratings yet

- Actual Actual Actual Actual: Cash Flow YearDocument8 pagesActual Actual Actual Actual: Cash Flow YearD J Ben UzeeNo ratings yet

- Accounting Equation ch5Document19 pagesAccounting Equation ch5Ebony Ann delos SantosNo ratings yet

- Lessons Abm - TVLDocument28 pagesLessons Abm - TVLramirezericahNo ratings yet

- H.W ch4q7 Acc418Document4 pagesH.W ch4q7 Acc418SARA ALKHODAIRNo ratings yet

- Accounting Equation ch4Document13 pagesAccounting Equation ch4Ebony Ann delos SantosNo ratings yet

- Cash FlowDocument1 pageCash FlowLeonard TonuiNo ratings yet

- Consolidation FP ExampleDocument4 pagesConsolidation FP ExampleYAUHANo ratings yet

- Partnership Liquidation - Grp1Document2 pagesPartnership Liquidation - Grp1Andrea BreisNo ratings yet

- Ud Abadi (Data Awal)Document2 pagesUd Abadi (Data Awal)syifaNo ratings yet

- MC6Document5 pagesMC6shudayeNo ratings yet

- Chapter4 MC Pt2Document12 pagesChapter4 MC Pt2Anonn100% (1)

- Chapter 4 Business Combination Solution ManualDocument19 pagesChapter 4 Business Combination Solution ManualMaxineNo ratings yet

- Accounts Unadjusted Trial Balance AdjustmentsDocument9 pagesAccounts Unadjusted Trial Balance AdjustmentsEiza LaxaNo ratings yet

- Module 5 - With SolutionsDocument21 pagesModule 5 - With SolutionsSeulgi KangNo ratings yet

- Partnership - Lump Sump and IL Final Exam 2023KEYSDocument4 pagesPartnership - Lump Sump and IL Final Exam 2023KEYSmcseenpiaNo ratings yet

- Date Account Debit Credit: T Accounts CashDocument8 pagesDate Account Debit Credit: T Accounts CashFiona SolacitoNo ratings yet

- GPV & SCF (Assignment)Document16 pagesGPV & SCF (Assignment)Mica Moreen GuillermoNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument32 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAshok LakshmananNo ratings yet

- Article Review and SummaryDocument5 pagesArticle Review and SummaryOmariba ReubenNo ratings yet

- Barclays #236586Document1 pageBarclays #236586РоманNo ratings yet

- Edmonton Opera - Work Sheet 2Document9 pagesEdmonton Opera - Work Sheet 2spam.ml2023No ratings yet

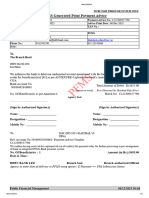

- PFMS Generated Print Payment Advice: To, The Branch HeadDocument2 pagesPFMS Generated Print Payment Advice: To, The Branch HeadAnurag gargNo ratings yet

- Questions On Preparation of Financial Statements 1-4Document4 pagesQuestions On Preparation of Financial Statements 1-4LaoneNo ratings yet

- Assignment 7Document3 pagesAssignment 7Arunim YadavNo ratings yet

- CSIR Format For UCDocument2 pagesCSIR Format For UCAmitNo ratings yet

- Acs Programs & Staff: APRIL 2010Document11 pagesAcs Programs & Staff: APRIL 2010carson_schefstad6105No ratings yet

- Money and BankingDocument20 pagesMoney and BankingFAH EEMNo ratings yet

- Small Group Case Studies Fall Assignment 2010Document4 pagesSmall Group Case Studies Fall Assignment 2010Laurence Ibay Palileo0% (2)

- Fundi Card StatementDocument2 pagesFundi Card StatementtseisimolebohengNo ratings yet

- Retirement Calculator: Calculate Current ExpensesDocument1 pageRetirement Calculator: Calculate Current ExpensesHARSHBHATTERNo ratings yet

- SB CollectDocument1 pageSB CollectChirag jNo ratings yet

- Cibil - Saurabh RaskarDocument4 pagesCibil - Saurabh RaskarSaurabh RaskarNo ratings yet

- Wire TransferDocument1 pageWire TransferEdoja Rocky100% (4)

- ConsolidateStatement Mar 20Document5 pagesConsolidateStatement Mar 20Coid CekNo ratings yet

- Compound InterestDocument1 pageCompound InterestBlack Ink Tutorials & ServicesNo ratings yet

- Adobe Scan 10 Oct 2022Document7 pagesAdobe Scan 10 Oct 2022Dhrisha GadaNo ratings yet

- Ibs Lahad Datu 1 31/12/23Document4 pagesIbs Lahad Datu 1 31/12/23fidatulsyafikahsamsualam12No ratings yet

- OLMC Schedule of Fees 2024 - FINALDocument2 pagesOLMC Schedule of Fees 2024 - FINALtxf.ftfNo ratings yet

- Chapter 5 ExercisesDocument4 pagesChapter 5 ExercisesShaheera Suhaimi0% (1)

- UHBVNDocument1 pageUHBVNsaksham22441No ratings yet

- Application Processing Fee Challan Application Processing Fee ChallanDocument1 pageApplication Processing Fee Challan Application Processing Fee ChallansayemlaeeqNo ratings yet

- Unit 3 Use of E Tax CalculatorDocument2 pagesUnit 3 Use of E Tax CalculatorSayan MitraNo ratings yet

- ANNUITYDocument10 pagesANNUITYgailNo ratings yet

- S10 107 TWNDocument3 pagesS10 107 TWNJinko JankoNo ratings yet

- Corporations in Financial Difficulty: Multiple Choice QuestionsDocument27 pagesCorporations in Financial Difficulty: Multiple Choice QuestionsDieter LudwigNo ratings yet

- Estatement 21032023Document1 pageEstatement 21032023Vivi MeilyanitaNo ratings yet

- College Information Sheets Ug 2023 Ver 3 05.08.2023.Document52 pagesCollege Information Sheets Ug 2023 Ver 3 05.08.2023.ashishmahawar1510No ratings yet