Cosmetic Solution

Cosmetic Solution

You might also like

- Hospital Project ProposalDocument3 pagesHospital Project Proposalhahagatstad84% (25)

- Legal Advice Letter SampleDocument4 pagesLegal Advice Letter SampleMichelle Hatol100% (5)

- The Raven of Zurich The Memoirs of Felix Somary Compressed PDFDocument167 pagesThe Raven of Zurich The Memoirs of Felix Somary Compressed PDFDavid100% (2)

- Assessment Tool Sitxglc001 Research and Comply With Regulatory RequirementsDocument25 pagesAssessment Tool Sitxglc001 Research and Comply With Regulatory Requirementscya mzn100% (1)

- Matrix CosmeticDocument2 pagesMatrix Cosmeticyimin liuNo ratings yet

- Book 1Document35 pagesBook 1Tarun BohraNo ratings yet

- Year Sales Volume Sales VC FC DepDocument8 pagesYear Sales Volume Sales VC FC DepMohammad Umair SheraziNo ratings yet

- Cart-2 + Production Unit FinalDocument4 pagesCart-2 + Production Unit Finalman789840No ratings yet

- Current Year Base Year Base Year X 100Document4 pagesCurrent Year Base Year Base Year X 100Kathlyn TajadaNo ratings yet

- TLA 4 Answers For DiscussionDocument21 pagesTLA 4 Answers For DiscussionTrisha Monique VillaNo ratings yet

- NPV ExcelDocument7 pagesNPV Excelkhanfaiz4144No ratings yet

- Fatima FertilizersDocument18 pagesFatima FertilizersBarira AkhtarNo ratings yet

- Price VarianceDocument3 pagesPrice VariancetataxpNo ratings yet

- CVP SolutionDocument11 pagesCVP SolutionGmail FixNo ratings yet

- Shahnawaz Inflaction RateDocument4 pagesShahnawaz Inflaction RateshahnawazmotiNo ratings yet

- Bai Tap 7Document6 pagesBai Tap 7Bích DiệuNo ratings yet

- Advanced Corporate Finance Case 2Document3 pagesAdvanced Corporate Finance Case 2Adrien PortemontNo ratings yet

- Installment MethodDocument4 pagesInstallment Methodjessica amorosoNo ratings yet

- Project 2Document3 pagesProject 2Mai HàNo ratings yet

- Scenario Summary: Changing CellsDocument10 pagesScenario Summary: Changing Cellsjerrynguyen291No ratings yet

- 3.16 ContributionDocument8 pages3.16 ContributionVishal SairamNo ratings yet

- Dec 14Document16 pagesDec 14Natasha AzzariennaNo ratings yet

- Essay FIN202Document5 pagesEssay FIN202thaindnds180468No ratings yet

- SFAD Week 1Document4 pagesSFAD Week 1Talha SiddiquiNo ratings yet

- 5,655.00 Additional Investment Needed/financingDocument23 pages5,655.00 Additional Investment Needed/financingMPCINo ratings yet

- Financial StatementDocument36 pagesFinancial StatementJigoku ShojuNo ratings yet

- Acquisition Cash FlowDocument3 pagesAcquisition Cash Flowkaeya alberichNo ratings yet

- Project PDA Conch Republic: Ebit 13,000,000 9,300,000Document4 pagesProject PDA Conch Republic: Ebit 13,000,000 9,300,000Harsya FitrioNo ratings yet

- EEV ANALYSIS BVDocument10 pagesEEV ANALYSIS BVcyics TabNo ratings yet

- Classic Pen HandoutsDocument1 pageClassic Pen HandoutsSuraj KumarNo ratings yet

- Installment SalesDocument13 pagesInstallment SalesMichael BongalontaNo ratings yet

- AF Ch. 4 - Analysis FS - ExcelDocument9 pagesAF Ch. 4 - Analysis FS - ExcelAlfiandriAdinNo ratings yet

- Unit 7 Budgeting SolutionsDocument15 pagesUnit 7 Budgeting SolutionsYogesh BandiNo ratings yet

- Practice Q (Capital Budgeting)Document12 pagesPractice Q (Capital Budgeting)Divyam GargNo ratings yet

- Lille Tissage WorksheetDocument19 pagesLille Tissage WorksheetJaouadiNo ratings yet

- Assignment 1-1Document19 pagesAssignment 1-1mishal zikriaNo ratings yet

- Bai Tap 7Document7 pagesBai Tap 7k60.2114113119No ratings yet

- Classic Pen Working HandoutsDocument1 pageClassic Pen Working HandoutsTushar DuaNo ratings yet

- Bai 2.xlsx de2Document4 pagesBai 2.xlsx de2letruongkhanhdung096No ratings yet

- Sotalbo, Norhie Anne O. 3BSA-2Document11 pagesSotalbo, Norhie Anne O. 3BSA-2Acads PurpsNo ratings yet

- Student Names Student Id Test 1 Test 2 Test 3 Final Internal AssessmentDocument5 pagesStudent Names Student Id Test 1 Test 2 Test 3 Final Internal AssessmentNguyen Dinh Quang MinhNo ratings yet

- Multi Product Break Even Analysis - Excel Tutorials - Subscribe Excel A-Z...Document2 pagesMulti Product Break Even Analysis - Excel Tutorials - Subscribe Excel A-Z...sharjeelraja876No ratings yet

- Chapter 6-ExamplesDocument6 pagesChapter 6-ExamplesNguyen Tan AnhNo ratings yet

- 2020 Expenses: What SUP, Inc. Income Statement For The Year EndedDocument5 pages2020 Expenses: What SUP, Inc. Income Statement For The Year EndedRi BNo ratings yet

- Regular Profit Analysis Common Size Profit Analysis: Income Statement Company A Percent Company B Percent RevenueDocument2 pagesRegular Profit Analysis Common Size Profit Analysis: Income Statement Company A Percent Company B Percent RevenueGolamMostafaNo ratings yet

- V - Common SizeDocument2 pagesV - Common SizeKyriye OngilavNo ratings yet

- UE MC 2023-2024 Exercise 10 B Solution1Document1 pageUE MC 2023-2024 Exercise 10 B Solution1Sami El YadiniNo ratings yet

- Horizontal and Vertical Analaysis: Karysse Arielle Noel Jalao Financial Management Bsac-2BDocument10 pagesHorizontal and Vertical Analaysis: Karysse Arielle Noel Jalao Financial Management Bsac-2BKarysse Arielle Noel JalaoNo ratings yet

- Puma R To L 2020 Master 3 PublishDocument8 pagesPuma R To L 2020 Master 3 PublishIulii IuliikkNo ratings yet

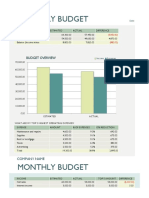

- Monthly Budget: Company NameDocument2 pagesMonthly Budget: Company NameMalleshNo ratings yet

- FINANCIAL ANALYSIS Practice 3Document15 pagesFINANCIAL ANALYSIS Practice 3Hallasgo, Elymar SorianoNo ratings yet

- Monthly Business BudgetDocument4 pagesMonthly Business BudgetOkasha HafeezNo ratings yet

- Madrigal Company Case StudyDocument4 pagesMadrigal Company Case StudyChleo EsperaNo ratings yet

- Midterms MADocument10 pagesMidterms MAJustz LimNo ratings yet

- 351 Jbe CaseDocument10 pages351 Jbe CaseMega ZhafarinaNo ratings yet

- Quiz BusFinHVRJULIANA VILLANUEVA ABM201-1Document10 pagesQuiz BusFinHVRJULIANA VILLANUEVA ABM201-1Juliana Angela VillanuevaNo ratings yet

- Project 2 BT2Document3 pagesProject 2 BT2Võ Thị Thanh NgânNo ratings yet

- Classic Pen IIM RohtakDocument12 pagesClassic Pen IIM RohtakHEM BANSALNo ratings yet

- Pricewell Single Entity Financial StatementsDocument6 pagesPricewell Single Entity Financial StatementsBig SmutNo ratings yet

- ACCTG 7 Chapter 9 Problems 1 and 2Document10 pagesACCTG 7 Chapter 9 Problems 1 and 2freaann03No ratings yet

- 1.1 - Whatif &PTDocument28 pages1.1 - Whatif &PTSalman AhmadNo ratings yet

- StratCost Quiz 2Document6 pagesStratCost Quiz 2ElleNo ratings yet

- Seatwork 4 - Decentralized OperationsDocument3 pagesSeatwork 4 - Decentralized OperationsJessaLyza CordovaNo ratings yet

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- Vendor FirefightingDocument26 pagesVendor Firefightingjaiswal.utkarshNo ratings yet

- The Best Shopping Cities ADocument7 pagesThe Best Shopping Cities Ail4891100% (2)

- Deep Hole Drlling On Maching Centres BOTEKDocument2 pagesDeep Hole Drlling On Maching Centres BOTEKmapalptsNo ratings yet

- CYFIRMA Introduction March2022Document35 pagesCYFIRMA Introduction March2022hin PeterNo ratings yet

- Global Private Equity - JapanDocument16 pagesGlobal Private Equity - JapanabhishaqueNo ratings yet

- Srs of Raliway Booking SystemDocument15 pagesSrs of Raliway Booking Systemkrupal5No ratings yet

- Unit 3 SQLDocument24 pagesUnit 3 SQLBhanu Prakash ReddyNo ratings yet

- Ms Important Questions For Final ExamDocument2 pagesMs Important Questions For Final ExamChiran RavaniNo ratings yet

- Historical Development of LibrariesDocument11 pagesHistorical Development of Librariestamerat bahtaNo ratings yet

- Prosthodontics PonticsDocument16 pagesProsthodontics PonticsLavanya R B100% (1)

- Curriculum Vitae: MD: Kawsar MollaDocument2 pagesCurriculum Vitae: MD: Kawsar MollaMostakNo ratings yet

- Coca Cola To Produce Paper Bottles British English TeacherDocument9 pagesCoca Cola To Produce Paper Bottles British English TeacherNil SierraNo ratings yet

- Create A Positive Brand Image For Mallika Hemachandra MenDocument20 pagesCreate A Positive Brand Image For Mallika Hemachandra MenSajith PrasangaNo ratings yet

- System of ExcitationDocument20 pagesSystem of ExcitationWesley RibeiroNo ratings yet

- Gopal A Krishnan 2018Document4 pagesGopal A Krishnan 2018Vishnu VNo ratings yet

- Excavation and TimberingDocument22 pagesExcavation and TimberingGanga DahalNo ratings yet

- Pmo WHSDocument31 pagesPmo WHSKOKO KUSUMAYANTONo ratings yet

- ES10-N01-Service-manual 6139 062015 ENDocument71 pagesES10-N01-Service-manual 6139 062015 ENsilvano pieriniNo ratings yet

- Dell p2717h Monitor User's Guide ENGLEZADocument60 pagesDell p2717h Monitor User's Guide ENGLEZAMarius DinuNo ratings yet

- Business Research Chapter 3Document24 pagesBusiness Research Chapter 3Abduselam AliyiNo ratings yet

- TIB BW 6.3.5 ConceptsDocument46 pagesTIB BW 6.3.5 Conceptspankaj somNo ratings yet

- (Lib24.vn) Bai-Tap-Doc-Hieu-Mon-Tieng-Anh-11Document4 pages(Lib24.vn) Bai-Tap-Doc-Hieu-Mon-Tieng-Anh-11Thư AnNo ratings yet

- 1 s2.0 S2590198222000197 MainDocument8 pages1 s2.0 S2590198222000197 MaindashakrezubNo ratings yet

- Height ProjectDocument9 pagesHeight ProjectAnvi bNo ratings yet

- TechPro II ManualDocument44 pagesTechPro II ManualEdsonNo ratings yet

- Denso Engine Management SystemsDocument184 pagesDenso Engine Management SystemsNiculae Noica100% (1)

Download as pdf or txt

You might also like

- Hospital Project ProposalDocument3 pagesHospital Project Proposalhahagatstad84% (25)

- Legal Advice Letter SampleDocument4 pagesLegal Advice Letter SampleMichelle Hatol100% (5)

- The Raven of Zurich The Memoirs of Felix Somary Compressed PDFDocument167 pagesThe Raven of Zurich The Memoirs of Felix Somary Compressed PDFDavid100% (2)

- Assessment Tool Sitxglc001 Research and Comply With Regulatory RequirementsDocument25 pagesAssessment Tool Sitxglc001 Research and Comply With Regulatory Requirementscya mzn100% (1)

- Matrix CosmeticDocument2 pagesMatrix Cosmeticyimin liuNo ratings yet

- Book 1Document35 pagesBook 1Tarun BohraNo ratings yet

- Year Sales Volume Sales VC FC DepDocument8 pagesYear Sales Volume Sales VC FC DepMohammad Umair SheraziNo ratings yet

- Cart-2 + Production Unit FinalDocument4 pagesCart-2 + Production Unit Finalman789840No ratings yet

- Current Year Base Year Base Year X 100Document4 pagesCurrent Year Base Year Base Year X 100Kathlyn TajadaNo ratings yet

- TLA 4 Answers For DiscussionDocument21 pagesTLA 4 Answers For DiscussionTrisha Monique VillaNo ratings yet

- NPV ExcelDocument7 pagesNPV Excelkhanfaiz4144No ratings yet

- Fatima FertilizersDocument18 pagesFatima FertilizersBarira AkhtarNo ratings yet

- Price VarianceDocument3 pagesPrice VariancetataxpNo ratings yet

- CVP SolutionDocument11 pagesCVP SolutionGmail FixNo ratings yet

- Shahnawaz Inflaction RateDocument4 pagesShahnawaz Inflaction RateshahnawazmotiNo ratings yet

- Bai Tap 7Document6 pagesBai Tap 7Bích DiệuNo ratings yet

- Advanced Corporate Finance Case 2Document3 pagesAdvanced Corporate Finance Case 2Adrien PortemontNo ratings yet

- Installment MethodDocument4 pagesInstallment Methodjessica amorosoNo ratings yet

- Project 2Document3 pagesProject 2Mai HàNo ratings yet

- Scenario Summary: Changing CellsDocument10 pagesScenario Summary: Changing Cellsjerrynguyen291No ratings yet

- 3.16 ContributionDocument8 pages3.16 ContributionVishal SairamNo ratings yet

- Dec 14Document16 pagesDec 14Natasha AzzariennaNo ratings yet

- Essay FIN202Document5 pagesEssay FIN202thaindnds180468No ratings yet

- SFAD Week 1Document4 pagesSFAD Week 1Talha SiddiquiNo ratings yet

- 5,655.00 Additional Investment Needed/financingDocument23 pages5,655.00 Additional Investment Needed/financingMPCINo ratings yet

- Financial StatementDocument36 pagesFinancial StatementJigoku ShojuNo ratings yet

- Acquisition Cash FlowDocument3 pagesAcquisition Cash Flowkaeya alberichNo ratings yet

- Project PDA Conch Republic: Ebit 13,000,000 9,300,000Document4 pagesProject PDA Conch Republic: Ebit 13,000,000 9,300,000Harsya FitrioNo ratings yet

- EEV ANALYSIS BVDocument10 pagesEEV ANALYSIS BVcyics TabNo ratings yet

- Classic Pen HandoutsDocument1 pageClassic Pen HandoutsSuraj KumarNo ratings yet

- Installment SalesDocument13 pagesInstallment SalesMichael BongalontaNo ratings yet

- AF Ch. 4 - Analysis FS - ExcelDocument9 pagesAF Ch. 4 - Analysis FS - ExcelAlfiandriAdinNo ratings yet

- Unit 7 Budgeting SolutionsDocument15 pagesUnit 7 Budgeting SolutionsYogesh BandiNo ratings yet

- Practice Q (Capital Budgeting)Document12 pagesPractice Q (Capital Budgeting)Divyam GargNo ratings yet

- Lille Tissage WorksheetDocument19 pagesLille Tissage WorksheetJaouadiNo ratings yet

- Assignment 1-1Document19 pagesAssignment 1-1mishal zikriaNo ratings yet

- Bai Tap 7Document7 pagesBai Tap 7k60.2114113119No ratings yet

- Classic Pen Working HandoutsDocument1 pageClassic Pen Working HandoutsTushar DuaNo ratings yet

- Bai 2.xlsx de2Document4 pagesBai 2.xlsx de2letruongkhanhdung096No ratings yet

- Sotalbo, Norhie Anne O. 3BSA-2Document11 pagesSotalbo, Norhie Anne O. 3BSA-2Acads PurpsNo ratings yet

- Student Names Student Id Test 1 Test 2 Test 3 Final Internal AssessmentDocument5 pagesStudent Names Student Id Test 1 Test 2 Test 3 Final Internal AssessmentNguyen Dinh Quang MinhNo ratings yet

- Multi Product Break Even Analysis - Excel Tutorials - Subscribe Excel A-Z...Document2 pagesMulti Product Break Even Analysis - Excel Tutorials - Subscribe Excel A-Z...sharjeelraja876No ratings yet

- Chapter 6-ExamplesDocument6 pagesChapter 6-ExamplesNguyen Tan AnhNo ratings yet

- 2020 Expenses: What SUP, Inc. Income Statement For The Year EndedDocument5 pages2020 Expenses: What SUP, Inc. Income Statement For The Year EndedRi BNo ratings yet

- Regular Profit Analysis Common Size Profit Analysis: Income Statement Company A Percent Company B Percent RevenueDocument2 pagesRegular Profit Analysis Common Size Profit Analysis: Income Statement Company A Percent Company B Percent RevenueGolamMostafaNo ratings yet

- V - Common SizeDocument2 pagesV - Common SizeKyriye OngilavNo ratings yet

- UE MC 2023-2024 Exercise 10 B Solution1Document1 pageUE MC 2023-2024 Exercise 10 B Solution1Sami El YadiniNo ratings yet

- Horizontal and Vertical Analaysis: Karysse Arielle Noel Jalao Financial Management Bsac-2BDocument10 pagesHorizontal and Vertical Analaysis: Karysse Arielle Noel Jalao Financial Management Bsac-2BKarysse Arielle Noel JalaoNo ratings yet

- Puma R To L 2020 Master 3 PublishDocument8 pagesPuma R To L 2020 Master 3 PublishIulii IuliikkNo ratings yet

- Monthly Budget: Company NameDocument2 pagesMonthly Budget: Company NameMalleshNo ratings yet

- FINANCIAL ANALYSIS Practice 3Document15 pagesFINANCIAL ANALYSIS Practice 3Hallasgo, Elymar SorianoNo ratings yet

- Monthly Business BudgetDocument4 pagesMonthly Business BudgetOkasha HafeezNo ratings yet

- Madrigal Company Case StudyDocument4 pagesMadrigal Company Case StudyChleo EsperaNo ratings yet

- Midterms MADocument10 pagesMidterms MAJustz LimNo ratings yet

- 351 Jbe CaseDocument10 pages351 Jbe CaseMega ZhafarinaNo ratings yet

- Quiz BusFinHVRJULIANA VILLANUEVA ABM201-1Document10 pagesQuiz BusFinHVRJULIANA VILLANUEVA ABM201-1Juliana Angela VillanuevaNo ratings yet

- Project 2 BT2Document3 pagesProject 2 BT2Võ Thị Thanh NgânNo ratings yet

- Classic Pen IIM RohtakDocument12 pagesClassic Pen IIM RohtakHEM BANSALNo ratings yet

- Pricewell Single Entity Financial StatementsDocument6 pagesPricewell Single Entity Financial StatementsBig SmutNo ratings yet

- ACCTG 7 Chapter 9 Problems 1 and 2Document10 pagesACCTG 7 Chapter 9 Problems 1 and 2freaann03No ratings yet

- 1.1 - Whatif &PTDocument28 pages1.1 - Whatif &PTSalman AhmadNo ratings yet

- StratCost Quiz 2Document6 pagesStratCost Quiz 2ElleNo ratings yet

- Seatwork 4 - Decentralized OperationsDocument3 pagesSeatwork 4 - Decentralized OperationsJessaLyza CordovaNo ratings yet

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- Vendor FirefightingDocument26 pagesVendor Firefightingjaiswal.utkarshNo ratings yet

- The Best Shopping Cities ADocument7 pagesThe Best Shopping Cities Ail4891100% (2)

- Deep Hole Drlling On Maching Centres BOTEKDocument2 pagesDeep Hole Drlling On Maching Centres BOTEKmapalptsNo ratings yet

- CYFIRMA Introduction March2022Document35 pagesCYFIRMA Introduction March2022hin PeterNo ratings yet

- Global Private Equity - JapanDocument16 pagesGlobal Private Equity - JapanabhishaqueNo ratings yet

- Srs of Raliway Booking SystemDocument15 pagesSrs of Raliway Booking Systemkrupal5No ratings yet

- Unit 3 SQLDocument24 pagesUnit 3 SQLBhanu Prakash ReddyNo ratings yet

- Ms Important Questions For Final ExamDocument2 pagesMs Important Questions For Final ExamChiran RavaniNo ratings yet

- Historical Development of LibrariesDocument11 pagesHistorical Development of Librariestamerat bahtaNo ratings yet

- Prosthodontics PonticsDocument16 pagesProsthodontics PonticsLavanya R B100% (1)

- Curriculum Vitae: MD: Kawsar MollaDocument2 pagesCurriculum Vitae: MD: Kawsar MollaMostakNo ratings yet

- Coca Cola To Produce Paper Bottles British English TeacherDocument9 pagesCoca Cola To Produce Paper Bottles British English TeacherNil SierraNo ratings yet

- Create A Positive Brand Image For Mallika Hemachandra MenDocument20 pagesCreate A Positive Brand Image For Mallika Hemachandra MenSajith PrasangaNo ratings yet

- System of ExcitationDocument20 pagesSystem of ExcitationWesley RibeiroNo ratings yet

- Gopal A Krishnan 2018Document4 pagesGopal A Krishnan 2018Vishnu VNo ratings yet

- Excavation and TimberingDocument22 pagesExcavation and TimberingGanga DahalNo ratings yet

- Pmo WHSDocument31 pagesPmo WHSKOKO KUSUMAYANTONo ratings yet

- ES10-N01-Service-manual 6139 062015 ENDocument71 pagesES10-N01-Service-manual 6139 062015 ENsilvano pieriniNo ratings yet

- Dell p2717h Monitor User's Guide ENGLEZADocument60 pagesDell p2717h Monitor User's Guide ENGLEZAMarius DinuNo ratings yet

- Business Research Chapter 3Document24 pagesBusiness Research Chapter 3Abduselam AliyiNo ratings yet

- TIB BW 6.3.5 ConceptsDocument46 pagesTIB BW 6.3.5 Conceptspankaj somNo ratings yet

- (Lib24.vn) Bai-Tap-Doc-Hieu-Mon-Tieng-Anh-11Document4 pages(Lib24.vn) Bai-Tap-Doc-Hieu-Mon-Tieng-Anh-11Thư AnNo ratings yet

- 1 s2.0 S2590198222000197 MainDocument8 pages1 s2.0 S2590198222000197 MaindashakrezubNo ratings yet

- Height ProjectDocument9 pagesHeight ProjectAnvi bNo ratings yet

- TechPro II ManualDocument44 pagesTechPro II ManualEdsonNo ratings yet

- Denso Engine Management SystemsDocument184 pagesDenso Engine Management SystemsNiculae Noica100% (1)