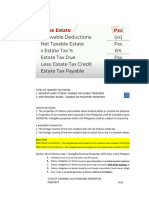

02 Gross Estate

02 Gross Estate

You might also like

- A Comparative Study On The Powers of The President of USA and IndiaDocument17 pagesA Comparative Study On The Powers of The President of USA and Indiajspragati273No ratings yet

- Chapter 2Document52 pagesChapter 2Rygiem Dela CruzNo ratings yet

- Gross EstateDocument11 pagesGross EstatejungoosNo ratings yet

- Gross Estate (Tabag)Document12 pagesGross Estate (Tabag)Cristina Mikhaela C. MagdaelNo ratings yet

- Estate Taxation NotesDocument39 pagesEstate Taxation NotesJovel LayasanNo ratings yet

- Module 1 - Estate TaxationDocument65 pagesModule 1 - Estate TaxationAllan C. MarquezNo ratings yet

- Module 7Document31 pagesModule 7roycedimasulitNo ratings yet

- TAX SITUS-It Is The Place or Authority That Has The Right To Impose and Collect TaxesDocument58 pagesTAX SITUS-It Is The Place or Authority That Has The Right To Impose and Collect TaxesTJ Julian Baltazar100% (1)

- Gross EstateDocument69 pagesGross EstateRedgiemarkNo ratings yet

- Gross EstateDocument6 pagesGross EstateCukeeNo ratings yet

- I. Gross Estate Vis-À-Vis Net Estate Gross EstateDocument18 pagesI. Gross Estate Vis-À-Vis Net Estate Gross EstateIan De DiosNo ratings yet

- Estate Tax - Is The Tax On The Right To Transmit Property at Death and On Certain Transfers Which Are Made by Law The Equivalent ofDocument4 pagesEstate Tax - Is The Tax On The Right To Transmit Property at Death and On Certain Transfers Which Are Made by Law The Equivalent ofAlliah SomidoNo ratings yet

- Taxation Ii Notes PDFDocument16 pagesTaxation Ii Notes PDFAudrey Kristina MaypaNo ratings yet

- Gross Estate IntroductionDocument2 pagesGross Estate IntroductionJustz LimNo ratings yet

- Chapter 2 - Gross Estate PDFDocument6 pagesChapter 2 - Gross Estate PDFVanessa Castor GasparNo ratings yet

- ET2Document5 pagesET2Mary Joy CabilNo ratings yet

- Taxation Ii NotesDocument16 pagesTaxation Ii NotesAudrey Kristina MaypaNo ratings yet

- 3.0 Estate TaxDocument66 pages3.0 Estate Taxmoshi kpop cartNo ratings yet

- I. Gross Estate Vis-À-Vis Net EstateDocument16 pagesI. Gross Estate Vis-À-Vis Net EstateIan De DiosNo ratings yet

- 5.3 Estate TaxDocument67 pages5.3 Estate TaxjehonieeeNo ratings yet

- Chapter 3 - TaxDocument23 pagesChapter 3 - TaxNilda Sahibul BaclayanNo ratings yet

- Tax2 Premid PDFDocument18 pagesTax2 Premid PDFJoben CuencaNo ratings yet

- Resident Citizen Resident Alien Non-Resident Citizen: 10k Transfer Element 5k ExchangeDocument5 pagesResident Citizen Resident Alien Non-Resident Citizen: 10k Transfer Element 5k ExchangeLilliane EstrellaNo ratings yet

- Tax 2 Notes Midterms LamosteDocument6 pagesTax 2 Notes Midterms LamosteRoji Belizar HernandezNo ratings yet

- Gross StateDocument3 pagesGross StateBrigetLimNo ratings yet

- Mobilia Sequuntur Personam-Applies To Intangible Property. Movables Follow The Person. Where The Owner Resides/domicilesDocument11 pagesMobilia Sequuntur Personam-Applies To Intangible Property. Movables Follow The Person. Where The Owner Resides/domicilesMary Joy NavajaNo ratings yet

- Tax 2 ReviewerDocument30 pagesTax 2 ReviewerKriziaItaoNo ratings yet

- Transfer Taxes: SEC. 84 Rates of Estate Tax. - There Shall Be Levied, AssessedDocument16 pagesTransfer Taxes: SEC. 84 Rates of Estate Tax. - There Shall Be Levied, AssessedAster Beane AranetaNo ratings yet

- Taxation TwoDocument66 pagesTaxation TwomashedpotatoaddictNo ratings yet

- 3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Document13 pages3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Abigail Ann PasiliaoNo ratings yet

- Who Are The Taxpayers Under The Estate Tax 2. What Are The Properties That Comprise An EstateDocument2 pagesWho Are The Taxpayers Under The Estate Tax 2. What Are The Properties That Comprise An EstateYunna JungNo ratings yet

- Taxation IIDocument72 pagesTaxation IIArnold OniaNo ratings yet

- Gross EstateDocument63 pagesGross EstateMark Angelo SibayanNo ratings yet

- Taxation Law II Green NotesDocument126 pagesTaxation Law II Green NotesNewCovenantChurchNo ratings yet

- Chapter 9 Estate TaxDocument10 pagesChapter 9 Estate TaxRhea Mikylla ConchasNo ratings yet

- Notes On Tax2 (1-5)Document4 pagesNotes On Tax2 (1-5)Leomar CastilloNo ratings yet

- TRANSFER TAXES - 2020pptxDocument14 pagesTRANSFER TAXES - 2020pptxMikhael OngNo ratings yet

- 2-Gross EstateDocument12 pages2-Gross EstateJim Kyrone GenobisaNo ratings yet

- Orca Share Media1520856036149Document19 pagesOrca Share Media1520856036149Aybern BawtistaNo ratings yet

- Review Notes For Taxation 2: Sequuntur Personam and Situs of Taxation)Document41 pagesReview Notes For Taxation 2: Sequuntur Personam and Situs of Taxation)JImlan Sahipa IsmaelNo ratings yet

- Chapter 3: GROSS ESTATE: The Decedent at The Time of His Death But Were Already Transferred During His LifetimeDocument7 pagesChapter 3: GROSS ESTATE: The Decedent at The Time of His Death But Were Already Transferred During His LifetimeJonalie LpzNo ratings yet

- Tax2 L02 NotesDocument14 pagesTax2 L02 NotesSavage KongNo ratings yet

- Donors TaxDocument30 pagesDonors TaxZhee BillarinaNo ratings yet

- Tax-2-Recits Estate Tax Donors TaxDocument5 pagesTax-2-Recits Estate Tax Donors TaxEmmanuel MabolocNo ratings yet

- FRANCISCO, Danica Mae E. BSLM 3-1 Assignment #2 I. AnswersDocument3 pagesFRANCISCO, Danica Mae E. BSLM 3-1 Assignment #2 I. AnswersDanica FranciscoNo ratings yet

- Tax2 - L02 - Notes (Business Tax)Document12 pagesTax2 - L02 - Notes (Business Tax)Savage KongNo ratings yet

- LegitimacyDocument11 pagesLegitimacyPrincess EngresoNo ratings yet

- Gross EstateDocument74 pagesGross EstateDonghae FishdaNo ratings yet

- Transfer TaxesDocument26 pagesTransfer TaxesAr Zel ArzelNo ratings yet

- Taxation II Transfer Taxes: SEC. 84. Rate of Estate Tax. - There Shall Be Levied, Assessed, CollectedDocument10 pagesTaxation II Transfer Taxes: SEC. 84. Rate of Estate Tax. - There Shall Be Levied, Assessed, CollectedBianca LaderaNo ratings yet

- Gross Estate 1Document12 pagesGross Estate 1Maja SantosNo ratings yet

- Estate Tax NotesDocument11 pagesEstate Tax NotesClaire Araneta AlcozeroNo ratings yet

- Enhancement Estate Tax2Document35 pagesEnhancement Estate Tax2Kathleen Tabasa ManuelNo ratings yet

- TAX Tax Law 2Document158 pagesTAX Tax Law 2iamtikalonNo ratings yet

- Tax MidtermsDocument23 pagesTax MidtermsCharles RiveraNo ratings yet

- Tax MidtermsDocument13 pagesTax MidtermsCharles RiveraNo ratings yet

- Transfer TaxDocument60 pagesTransfer Taxandrei jim100% (6)

- Transfer Taxes Ust 1Document18 pagesTransfer Taxes Ust 1JAY AUBREY PINEDANo ratings yet

- Screenshot 2023-01-07 at 7.33.02 AMDocument5 pagesScreenshot 2023-01-07 at 7.33.02 AMhchandiramani3No ratings yet

- Principles of Constitutional InterpretationDocument7 pagesPrinciples of Constitutional Interpretationmahima chanchalaniNo ratings yet

- SPL - Cases - Sep - 24 - 2020Document24 pagesSPL - Cases - Sep - 24 - 2020Johnny EnglishNo ratings yet

- The End of The EU Affair The UK General Election of 20192021west European PoliticsDocument13 pagesThe End of The EU Affair The UK General Election of 20192021west European PoliticsarmandoibanezNo ratings yet

- Hex BoltsDocument13 pagesHex BoltsSandeep SNo ratings yet

- Michael Dillon in 1999 (Dehumanization Is Worse Than Death)Document2 pagesMichael Dillon in 1999 (Dehumanization Is Worse Than Death)Charles Riley Wanless0% (1)

- Judges Write in Opposition To Consolidating CircuitsDocument7 pagesJudges Write in Opposition To Consolidating CircuitsJeff WeinerNo ratings yet

- Pillar 2 CompleteDocument278 pagesPillar 2 CompleteAnshul SinghNo ratings yet

- Arr 262 PDFDocument150 pagesArr 262 PDFMalcolm YirdikNo ratings yet

- Journal A NEW TRAINING PROGRAM IN DEVELOPING CULTURAL INTELLIGENCE CAN ALSO IMPROVE INNOVATIVE WORK BEHAVIOUR AND RESILIENCEDocument20 pagesJournal A NEW TRAINING PROGRAM IN DEVELOPING CULTURAL INTELLIGENCE CAN ALSO IMPROVE INNOVATIVE WORK BEHAVIOUR AND RESILIENCEAudrey KalaNo ratings yet

- Duare Tran Prakalpa Application Form Evergreen TutorialDocument2 pagesDuare Tran Prakalpa Application Form Evergreen Tutorialsujit patraNo ratings yet

- MDAAudit MirzaDocument3,251 pagesMDAAudit Mirzavaishnavidixit724No ratings yet

- Napoleon Bonaparte Domestic Policies-1Document23 pagesNapoleon Bonaparte Domestic Policies-1Kudakwashe TakavadaNo ratings yet

- 2014 BASIC 8 CIVIC EDUC 2ND TERM E-NOTES - docxREVIEWEDDocument17 pages2014 BASIC 8 CIVIC EDUC 2ND TERM E-NOTES - docxREVIEWEDpalmer okiemuteNo ratings yet

- Last Will and Testament of Aira Rowena Abad TalactacDocument4 pagesLast Will and Testament of Aira Rowena Abad TalactacairarowenaNo ratings yet

- Murder Case: by Joylynn Awurama BineyDocument15 pagesMurder Case: by Joylynn Awurama Bineyjoylynn bineyNo ratings yet

- Form: Gewerbe-Anmeldung (Gewa 1) (Registration of A Business in Germany)Document4 pagesForm: Gewerbe-Anmeldung (Gewa 1) (Registration of A Business in Germany)Xinwei Eddie OuyangNo ratings yet

- Audit of Cash Employee FraudDocument29 pagesAudit of Cash Employee FraudBusiness MatterNo ratings yet

- Alcantara vs. Director of PrisonsDocument8 pagesAlcantara vs. Director of PrisonsLea RealNo ratings yet

- Bass ClefDocument29 pagesBass ClefSerhii DatkoNo ratings yet

- Aakash Institute: NCERT Solutions For Class 8 History Chapter 11: The Making of The National MovementDocument6 pagesAakash Institute: NCERT Solutions For Class 8 History Chapter 11: The Making of The National Movementnaniac raniNo ratings yet

- Peixoto, Angel - IRS Form 2848Document2 pagesPeixoto, Angel - IRS Form 2848MariaNo ratings yet

- Exercise-Power Sharing: Social Science - XDocument1 pageExercise-Power Sharing: Social Science - XVaishnaviNo ratings yet

- LA Metro - 684Document3 pagesLA Metro - 684cartographicaNo ratings yet

- 22T TitleContingencyDocument1 page22T TitleContingencyJanet NNo ratings yet

- ASTM C1527C1527M-11 - Standard Specification For Travertine Dimension StoneDocument2 pagesASTM C1527C1527M-11 - Standard Specification For Travertine Dimension StoneAniket InarkarNo ratings yet

- CA CPT Fundamentals of Accounting PPT Bills of Exchange and Promissory Notes Part 1Document21 pagesCA CPT Fundamentals of Accounting PPT Bills of Exchange and Promissory Notes Part 1Palani Muthusamy100% (1)

- Herbert Spencer: Social Darwinism: (Memorize)Document6 pagesHerbert Spencer: Social Darwinism: (Memorize)Adnan RaheemNo ratings yet

- Major Paper 3Document4 pagesMajor Paper 3api-302038454No ratings yet

Download as pdf or txt

You might also like

- A Comparative Study On The Powers of The President of USA and IndiaDocument17 pagesA Comparative Study On The Powers of The President of USA and Indiajspragati273No ratings yet

- Chapter 2Document52 pagesChapter 2Rygiem Dela CruzNo ratings yet

- Gross EstateDocument11 pagesGross EstatejungoosNo ratings yet

- Gross Estate (Tabag)Document12 pagesGross Estate (Tabag)Cristina Mikhaela C. MagdaelNo ratings yet

- Estate Taxation NotesDocument39 pagesEstate Taxation NotesJovel LayasanNo ratings yet

- Module 1 - Estate TaxationDocument65 pagesModule 1 - Estate TaxationAllan C. MarquezNo ratings yet

- Module 7Document31 pagesModule 7roycedimasulitNo ratings yet

- TAX SITUS-It Is The Place or Authority That Has The Right To Impose and Collect TaxesDocument58 pagesTAX SITUS-It Is The Place or Authority That Has The Right To Impose and Collect TaxesTJ Julian Baltazar100% (1)

- Gross EstateDocument69 pagesGross EstateRedgiemarkNo ratings yet

- Gross EstateDocument6 pagesGross EstateCukeeNo ratings yet

- I. Gross Estate Vis-À-Vis Net Estate Gross EstateDocument18 pagesI. Gross Estate Vis-À-Vis Net Estate Gross EstateIan De DiosNo ratings yet

- Estate Tax - Is The Tax On The Right To Transmit Property at Death and On Certain Transfers Which Are Made by Law The Equivalent ofDocument4 pagesEstate Tax - Is The Tax On The Right To Transmit Property at Death and On Certain Transfers Which Are Made by Law The Equivalent ofAlliah SomidoNo ratings yet

- Taxation Ii Notes PDFDocument16 pagesTaxation Ii Notes PDFAudrey Kristina MaypaNo ratings yet

- Gross Estate IntroductionDocument2 pagesGross Estate IntroductionJustz LimNo ratings yet

- Chapter 2 - Gross Estate PDFDocument6 pagesChapter 2 - Gross Estate PDFVanessa Castor GasparNo ratings yet

- ET2Document5 pagesET2Mary Joy CabilNo ratings yet

- Taxation Ii NotesDocument16 pagesTaxation Ii NotesAudrey Kristina MaypaNo ratings yet

- 3.0 Estate TaxDocument66 pages3.0 Estate Taxmoshi kpop cartNo ratings yet

- I. Gross Estate Vis-À-Vis Net EstateDocument16 pagesI. Gross Estate Vis-À-Vis Net EstateIan De DiosNo ratings yet

- 5.3 Estate TaxDocument67 pages5.3 Estate TaxjehonieeeNo ratings yet

- Chapter 3 - TaxDocument23 pagesChapter 3 - TaxNilda Sahibul BaclayanNo ratings yet

- Tax2 Premid PDFDocument18 pagesTax2 Premid PDFJoben CuencaNo ratings yet

- Resident Citizen Resident Alien Non-Resident Citizen: 10k Transfer Element 5k ExchangeDocument5 pagesResident Citizen Resident Alien Non-Resident Citizen: 10k Transfer Element 5k ExchangeLilliane EstrellaNo ratings yet

- Tax 2 Notes Midterms LamosteDocument6 pagesTax 2 Notes Midterms LamosteRoji Belizar HernandezNo ratings yet

- Gross StateDocument3 pagesGross StateBrigetLimNo ratings yet

- Mobilia Sequuntur Personam-Applies To Intangible Property. Movables Follow The Person. Where The Owner Resides/domicilesDocument11 pagesMobilia Sequuntur Personam-Applies To Intangible Property. Movables Follow The Person. Where The Owner Resides/domicilesMary Joy NavajaNo ratings yet

- Tax 2 ReviewerDocument30 pagesTax 2 ReviewerKriziaItaoNo ratings yet

- Transfer Taxes: SEC. 84 Rates of Estate Tax. - There Shall Be Levied, AssessedDocument16 pagesTransfer Taxes: SEC. 84 Rates of Estate Tax. - There Shall Be Levied, AssessedAster Beane AranetaNo ratings yet

- Taxation TwoDocument66 pagesTaxation TwomashedpotatoaddictNo ratings yet

- 3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Document13 pages3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Abigail Ann PasiliaoNo ratings yet

- Who Are The Taxpayers Under The Estate Tax 2. What Are The Properties That Comprise An EstateDocument2 pagesWho Are The Taxpayers Under The Estate Tax 2. What Are The Properties That Comprise An EstateYunna JungNo ratings yet

- Taxation IIDocument72 pagesTaxation IIArnold OniaNo ratings yet

- Gross EstateDocument63 pagesGross EstateMark Angelo SibayanNo ratings yet

- Taxation Law II Green NotesDocument126 pagesTaxation Law II Green NotesNewCovenantChurchNo ratings yet

- Chapter 9 Estate TaxDocument10 pagesChapter 9 Estate TaxRhea Mikylla ConchasNo ratings yet

- Notes On Tax2 (1-5)Document4 pagesNotes On Tax2 (1-5)Leomar CastilloNo ratings yet

- TRANSFER TAXES - 2020pptxDocument14 pagesTRANSFER TAXES - 2020pptxMikhael OngNo ratings yet

- 2-Gross EstateDocument12 pages2-Gross EstateJim Kyrone GenobisaNo ratings yet

- Orca Share Media1520856036149Document19 pagesOrca Share Media1520856036149Aybern BawtistaNo ratings yet

- Review Notes For Taxation 2: Sequuntur Personam and Situs of Taxation)Document41 pagesReview Notes For Taxation 2: Sequuntur Personam and Situs of Taxation)JImlan Sahipa IsmaelNo ratings yet

- Chapter 3: GROSS ESTATE: The Decedent at The Time of His Death But Were Already Transferred During His LifetimeDocument7 pagesChapter 3: GROSS ESTATE: The Decedent at The Time of His Death But Were Already Transferred During His LifetimeJonalie LpzNo ratings yet

- Tax2 L02 NotesDocument14 pagesTax2 L02 NotesSavage KongNo ratings yet

- Donors TaxDocument30 pagesDonors TaxZhee BillarinaNo ratings yet

- Tax-2-Recits Estate Tax Donors TaxDocument5 pagesTax-2-Recits Estate Tax Donors TaxEmmanuel MabolocNo ratings yet

- FRANCISCO, Danica Mae E. BSLM 3-1 Assignment #2 I. AnswersDocument3 pagesFRANCISCO, Danica Mae E. BSLM 3-1 Assignment #2 I. AnswersDanica FranciscoNo ratings yet

- Tax2 - L02 - Notes (Business Tax)Document12 pagesTax2 - L02 - Notes (Business Tax)Savage KongNo ratings yet

- LegitimacyDocument11 pagesLegitimacyPrincess EngresoNo ratings yet

- Gross EstateDocument74 pagesGross EstateDonghae FishdaNo ratings yet

- Transfer TaxesDocument26 pagesTransfer TaxesAr Zel ArzelNo ratings yet

- Taxation II Transfer Taxes: SEC. 84. Rate of Estate Tax. - There Shall Be Levied, Assessed, CollectedDocument10 pagesTaxation II Transfer Taxes: SEC. 84. Rate of Estate Tax. - There Shall Be Levied, Assessed, CollectedBianca LaderaNo ratings yet

- Gross Estate 1Document12 pagesGross Estate 1Maja SantosNo ratings yet

- Estate Tax NotesDocument11 pagesEstate Tax NotesClaire Araneta AlcozeroNo ratings yet

- Enhancement Estate Tax2Document35 pagesEnhancement Estate Tax2Kathleen Tabasa ManuelNo ratings yet

- TAX Tax Law 2Document158 pagesTAX Tax Law 2iamtikalonNo ratings yet

- Tax MidtermsDocument23 pagesTax MidtermsCharles RiveraNo ratings yet

- Tax MidtermsDocument13 pagesTax MidtermsCharles RiveraNo ratings yet

- Transfer TaxDocument60 pagesTransfer Taxandrei jim100% (6)

- Transfer Taxes Ust 1Document18 pagesTransfer Taxes Ust 1JAY AUBREY PINEDANo ratings yet

- Screenshot 2023-01-07 at 7.33.02 AMDocument5 pagesScreenshot 2023-01-07 at 7.33.02 AMhchandiramani3No ratings yet

- Principles of Constitutional InterpretationDocument7 pagesPrinciples of Constitutional Interpretationmahima chanchalaniNo ratings yet

- SPL - Cases - Sep - 24 - 2020Document24 pagesSPL - Cases - Sep - 24 - 2020Johnny EnglishNo ratings yet

- The End of The EU Affair The UK General Election of 20192021west European PoliticsDocument13 pagesThe End of The EU Affair The UK General Election of 20192021west European PoliticsarmandoibanezNo ratings yet

- Hex BoltsDocument13 pagesHex BoltsSandeep SNo ratings yet

- Michael Dillon in 1999 (Dehumanization Is Worse Than Death)Document2 pagesMichael Dillon in 1999 (Dehumanization Is Worse Than Death)Charles Riley Wanless0% (1)

- Judges Write in Opposition To Consolidating CircuitsDocument7 pagesJudges Write in Opposition To Consolidating CircuitsJeff WeinerNo ratings yet

- Pillar 2 CompleteDocument278 pagesPillar 2 CompleteAnshul SinghNo ratings yet

- Arr 262 PDFDocument150 pagesArr 262 PDFMalcolm YirdikNo ratings yet

- Journal A NEW TRAINING PROGRAM IN DEVELOPING CULTURAL INTELLIGENCE CAN ALSO IMPROVE INNOVATIVE WORK BEHAVIOUR AND RESILIENCEDocument20 pagesJournal A NEW TRAINING PROGRAM IN DEVELOPING CULTURAL INTELLIGENCE CAN ALSO IMPROVE INNOVATIVE WORK BEHAVIOUR AND RESILIENCEAudrey KalaNo ratings yet

- Duare Tran Prakalpa Application Form Evergreen TutorialDocument2 pagesDuare Tran Prakalpa Application Form Evergreen Tutorialsujit patraNo ratings yet

- MDAAudit MirzaDocument3,251 pagesMDAAudit Mirzavaishnavidixit724No ratings yet

- Napoleon Bonaparte Domestic Policies-1Document23 pagesNapoleon Bonaparte Domestic Policies-1Kudakwashe TakavadaNo ratings yet

- 2014 BASIC 8 CIVIC EDUC 2ND TERM E-NOTES - docxREVIEWEDDocument17 pages2014 BASIC 8 CIVIC EDUC 2ND TERM E-NOTES - docxREVIEWEDpalmer okiemuteNo ratings yet

- Last Will and Testament of Aira Rowena Abad TalactacDocument4 pagesLast Will and Testament of Aira Rowena Abad TalactacairarowenaNo ratings yet

- Murder Case: by Joylynn Awurama BineyDocument15 pagesMurder Case: by Joylynn Awurama Bineyjoylynn bineyNo ratings yet

- Form: Gewerbe-Anmeldung (Gewa 1) (Registration of A Business in Germany)Document4 pagesForm: Gewerbe-Anmeldung (Gewa 1) (Registration of A Business in Germany)Xinwei Eddie OuyangNo ratings yet

- Audit of Cash Employee FraudDocument29 pagesAudit of Cash Employee FraudBusiness MatterNo ratings yet

- Alcantara vs. Director of PrisonsDocument8 pagesAlcantara vs. Director of PrisonsLea RealNo ratings yet

- Bass ClefDocument29 pagesBass ClefSerhii DatkoNo ratings yet

- Aakash Institute: NCERT Solutions For Class 8 History Chapter 11: The Making of The National MovementDocument6 pagesAakash Institute: NCERT Solutions For Class 8 History Chapter 11: The Making of The National Movementnaniac raniNo ratings yet

- Peixoto, Angel - IRS Form 2848Document2 pagesPeixoto, Angel - IRS Form 2848MariaNo ratings yet

- Exercise-Power Sharing: Social Science - XDocument1 pageExercise-Power Sharing: Social Science - XVaishnaviNo ratings yet

- LA Metro - 684Document3 pagesLA Metro - 684cartographicaNo ratings yet

- 22T TitleContingencyDocument1 page22T TitleContingencyJanet NNo ratings yet

- ASTM C1527C1527M-11 - Standard Specification For Travertine Dimension StoneDocument2 pagesASTM C1527C1527M-11 - Standard Specification For Travertine Dimension StoneAniket InarkarNo ratings yet

- CA CPT Fundamentals of Accounting PPT Bills of Exchange and Promissory Notes Part 1Document21 pagesCA CPT Fundamentals of Accounting PPT Bills of Exchange and Promissory Notes Part 1Palani Muthusamy100% (1)

- Herbert Spencer: Social Darwinism: (Memorize)Document6 pagesHerbert Spencer: Social Darwinism: (Memorize)Adnan RaheemNo ratings yet

- Major Paper 3Document4 pagesMajor Paper 3api-302038454No ratings yet