PPC CH-4 (2024)

PPC CH-4 (2024)

You might also like

- Osha 10-Hour Construction Industry: How To Use This Study GuideDocument39 pagesOsha 10-Hour Construction Industry: How To Use This Study GuideGabriel ParksNo ratings yet

- ELEMENTS OF COST Students NotesDocument6 pagesELEMENTS OF COST Students NotesJkuat MSc. P & L100% (1)

- Informatica Forence 10 2013Document62 pagesInformatica Forence 10 2013Carlos Bernal100% (1)

- CH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisDocument84 pagesCH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisankonmahmudNo ratings yet

- Gross National Income Per Capita 2019, Atlas Method and PPPDocument4 pagesGross National Income Per Capita 2019, Atlas Method and PPPElisha WankogereNo ratings yet

- Swarm WhitepaperDocument46 pagesSwarm WhitepaperJoel Dietz100% (1)

- Chapter-4: Manufacturing Cost Elements and Cost Estimation For Various ProcessDocument21 pagesChapter-4: Manufacturing Cost Elements and Cost Estimation For Various ProcessTerefa FeyisaNo ratings yet

- Java NotesDocument15 pagesJava NotesIqbal HawreNo ratings yet

- ME Module 5Document12 pagesME Module 5Pratham J TudoorNo ratings yet

- Managerial Accounting and Cost ConceptsDocument50 pagesManagerial Accounting and Cost ConceptsGigo Kafare BinoNo ratings yet

- Blocher8e EOC SM Ch03 FinalDocument27 pagesBlocher8e EOC SM Ch03 FinalDiah ArmelizaNo ratings yet

- Cost Concept and ClassificationDocument45 pagesCost Concept and ClassificationMountaha0% (1)

- Lecture 3 - Cost ConceptsDocument23 pagesLecture 3 - Cost ConceptsEmmanuel NamkumbeNo ratings yet

- Brewer 8e PPT Ch01 TDocument54 pagesBrewer 8e PPT Ch01 TJuan Camilo IdarragaNo ratings yet

- Managerial Accounting and Cost Concepts: Solutions To QuestionsDocument13 pagesManagerial Accounting and Cost Concepts: Solutions To QuestionsGera MatsNo ratings yet

- Cost Engineering Lecture NoteDocument62 pagesCost Engineering Lecture Notefentawmelaku1993No ratings yet

- 2B - Unit 2 - Cost Classification Behaviour & Estimation - Workbook SOLUTIONS - 2022Document47 pages2B - Unit 2 - Cost Classification Behaviour & Estimation - Workbook SOLUTIONS - 2022Bono magadaniNo ratings yet

- Managerial Accounting and Cost ConceptsDocument62 pagesManagerial Accounting and Cost ConceptsJuana BoresNo ratings yet

- 1a Cost Classification Form Manufacturing PT of View and Predicting Cost Behaviour - 19 - 12 - 2023Document12 pages1a Cost Classification Form Manufacturing PT of View and Predicting Cost Behaviour - 19 - 12 - 2023Md Rashadul IslamNo ratings yet

- L5 - Types of Costs and Cost Estimation of A ProductDocument82 pagesL5 - Types of Costs and Cost Estimation of A ProducthayliyesusNo ratings yet

- Cost Terms, Concepts, and Classifications: Solutions To QuestionsDocument14 pagesCost Terms, Concepts, and Classifications: Solutions To QuestionsTrishia OliverosNo ratings yet

- CHAPTER 2 Question SolutionsDocument3 pagesCHAPTER 2 Question Solutionscamd1290100% (1)

- Bgteu v2s60Document15 pagesBgteu v2s60maye dataelNo ratings yet

- Chapter 2 - Cost Concepts and Design Economics SolutionsDocument31 pagesChapter 2 - Cost Concepts and Design Economics SolutionsArin Park100% (1)

- Assignment Topics (Case Study-Based) : (Refer Notes On SLE That Has Been Circulated)Document8 pagesAssignment Topics (Case Study-Based) : (Refer Notes On SLE That Has Been Circulated)Bharath T SNo ratings yet

- Introduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualDocument25 pagesIntroduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualMaryJohnsonsmni100% (61)

- An Introduction To Cost Terms and Purposes 2-1Document33 pagesAn Introduction To Cost Terms and Purposes 2-1Moayad TeimatNo ratings yet

- Summary On Cost Concpts and ClassificationsDocument7 pagesSummary On Cost Concpts and ClassificationsMa. Roycelean PascualNo ratings yet

- CT 206 Notes-1Document56 pagesCT 206 Notes-1Flex GodNo ratings yet

- L1-Manufacturer's CostDocument19 pagesL1-Manufacturer's CostomarNo ratings yet

- What Are The Types of Costs in Cost AccountingDocument2 pagesWhat Are The Types of Costs in Cost AccountingAhmed HassanNo ratings yet

- Muslim University of Morogoro - 090058Document14 pagesMuslim University of Morogoro - 090058mika piusNo ratings yet

- Khanda Habeeb RaheemDocument12 pagesKhanda Habeeb RaheemHarith EmaadNo ratings yet

- Inventory: COST OF PRODUCTIONDocument104 pagesInventory: COST OF PRODUCTIONHAFIZ MUHAMMAD UMAR FAROOQ RANANo ratings yet

- Cost HandoutDocument31 pagesCost HandoutTilahun GirmaNo ratings yet

- Garment Costing: Minnie BastinDocument73 pagesGarment Costing: Minnie BastinBastinNo ratings yet

- Econ Module 1 Unit 2Document20 pagesEcon Module 1 Unit 2Lester VirayNo ratings yet

- An Introduction To Managerial Accounting and Cost ConceptsDocument38 pagesAn Introduction To Managerial Accounting and Cost ConceptsHoàng TrangNo ratings yet

- Cost ConceptsDocument56 pagesCost ConceptsAngela De chavezNo ratings yet

- 20200912024025SLCHIA005MA2 Notes Cost BehaviourDocument24 pages20200912024025SLCHIA005MA2 Notes Cost BehaviourDương DươngNo ratings yet

- Elements of Cost: Manisha VermaDocument31 pagesElements of Cost: Manisha VermaPriyanshNo ratings yet

- Unit 1 Section 6Document7 pagesUnit 1 Section 6Babamu Kalmoni JaatoNo ratings yet

- BBA 2003 Cost AccountingDocument24 pagesBBA 2003 Cost AccountingVentus TanNo ratings yet

- Topic 13 Finance For Small BusinessDocument23 pagesTopic 13 Finance For Small BusinessdesaeNo ratings yet

- A Assignment ON "Examples Where Direct Expenses Are Not Included in The Cost of Production"Document7 pagesA Assignment ON "Examples Where Direct Expenses Are Not Included in The Cost of Production"parikharistNo ratings yet

- Chapter 2 UpdatedDocument58 pagesChapter 2 Updatedbing bongNo ratings yet

- Apply Cost FactorDocument23 pagesApply Cost FactoreyasuNo ratings yet

- Introduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualDocument36 pagesIntroduction To Managerial Accounting Canadian 5th Edition Brewer Solutions Manualfayedavidsonhet0cs100% (25)

- Cost Concepts: According To Management FunctionDocument10 pagesCost Concepts: According To Management FunctionQuenn NavalNo ratings yet

- Lec 04 - Managerial Accounting (Concepts & Principles)Document36 pagesLec 04 - Managerial Accounting (Concepts & Principles)Sakib RafeeNo ratings yet

- Cost: As A Resource Sacrificed or Forgone To Achieve A Specific Objective. It Is Usually MeasuredDocument19 pagesCost: As A Resource Sacrificed or Forgone To Achieve A Specific Objective. It Is Usually MeasuredTilahun GirmaNo ratings yet

- Elements of Cost and Its Impact of PricingDocument12 pagesElements of Cost and Its Impact of PricingAnu PriyaNo ratings yet

- Cost Terms, Concepts, and Classifications: Solution To Discussion CaseDocument48 pagesCost Terms, Concepts, and Classifications: Solution To Discussion Casekasad jdnfrnasNo ratings yet

- Cost Concepts and ClassificationsDocument3 pagesCost Concepts and ClassificationsCONCORDIA RAFAEL IVANNo ratings yet

- Costs: Different Ways To Categorize CostsDocument7 pagesCosts: Different Ways To Categorize Costsraul_mahadikNo ratings yet

- Elements of CostDocument17 pagesElements of CostManikant SAhNo ratings yet

- A Study On Cost Control Techniques in Ultratech Cement Company, BengaluruDocument76 pagesA Study On Cost Control Techniques in Ultratech Cement Company, BengaluruChethan.sNo ratings yet

- Solution Manual For Discrete Mathematics and Its Applications 8th Edition by RosenDocument24 pagesSolution Manual For Discrete Mathematics and Its Applications 8th Edition by RosenEileenLeexseb100% (42)

- Chapter 2 Cost Accounting ConceptsDocument22 pagesChapter 2 Cost Accounting ConceptsRosliana RazabNo ratings yet

- Manufacturing ManagementDocument126 pagesManufacturing ManagementSIDDHARTH JHANo ratings yet

- COST Lesson 2Document4 pagesCOST Lesson 2Christian Clyde Zacal Ching0% (1)

- Chapter 2 Answer PDFDocument19 pagesChapter 2 Answer PDFCris VillarNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Integration of Smart Carts in Puregold SupermarketDocument153 pagesIntegration of Smart Carts in Puregold SupermarketKen ParilNo ratings yet

- Office Management Tools (16rsbe7:2) : Sengamalathayaar Educational Trust Women'S CollegeDocument15 pagesOffice Management Tools (16rsbe7:2) : Sengamalathayaar Educational Trust Women'S CollegeKumaran RaniNo ratings yet

- Government of Madhya Pradesh Public Health Engineering DepartmentDocument63 pagesGovernment of Madhya Pradesh Public Health Engineering DepartmentShreyansh SharmaNo ratings yet

- Makalah CJR BibDocument9 pagesMakalah CJR BibRyan AlfandiNo ratings yet

- Advertising 5Document41 pagesAdvertising 5Sông HươngNo ratings yet

- Nantes2018 FLV VerrieresV4Document9 pagesNantes2018 FLV VerrieresV4Fikri Bin Abdul ShukorNo ratings yet

- The Embassy in Jakarta - Overview (2012) PDFDocument17 pagesThe Embassy in Jakarta - Overview (2012) PDFHo Yiu YinNo ratings yet

- Busy Accounting Software Standard EditionDocument4 pagesBusy Accounting Software Standard EditionpremsinghjaniNo ratings yet

- Indian Ports Community SystemDocument6 pagesIndian Ports Community Systempatil sNo ratings yet

- Capital Expenditure Control: DR Palash BairagiDocument38 pagesCapital Expenditure Control: DR Palash Bairagisundaram MishraNo ratings yet

- Account Statement From 27 Mar 2022 To 5 Apr 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 27 Mar 2022 To 5 Apr 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancePiyush AgarwalNo ratings yet

- Introduction To GNU Radio and Software RadioDocument4 pagesIntroduction To GNU Radio and Software RadioDinesh VermaNo ratings yet

- Personal MKTG PKG - Part 2 V2Document3 pagesPersonal MKTG PKG - Part 2 V2Lakshya TripathiNo ratings yet

- The Perfect Site GuideDocument59 pagesThe Perfect Site GuideconstantrazNo ratings yet

- I LuxDocument24 pagesI LuxNirav M. BhavsarNo ratings yet

- In Design: Iman BokhariDocument12 pagesIn Design: Iman Bokharimena_sky11No ratings yet

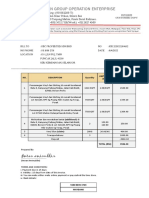

- Ilan Group Operation Enterprise: Imran AminuddinDocument1 pageIlan Group Operation Enterprise: Imran AminuddinIzhar AminuddinNo ratings yet

- The Agricultural Futures MarketDocument10 pagesThe Agricultural Futures MarketBharath ChaitanyaNo ratings yet

- Coordination For Motor Protection: High Performance MCCBDocument0 pagesCoordination For Motor Protection: High Performance MCCBKishore KrishnaNo ratings yet

- Additive Manufacturing ProcessesDocument27 pagesAdditive Manufacturing ProcessesAizrul ShahNo ratings yet

- GodotDocument977 pagesGodotClaudio Alberto ManquirreNo ratings yet

- DEPRECIATIONDocument3 pagesDEPRECIATIONUsirika Sai KumarNo ratings yet

- Pantallas HITACHI DP 6X Training PackageDocument92 pagesPantallas HITACHI DP 6X Training PackagericardoNo ratings yet

- PSR I455Document4 pagesPSR I455caronNo ratings yet

- Project Proposal TemplateDocument2 pagesProject Proposal TemplatejorifeberdenuevoespinosaNo ratings yet

- G495Q柴油机设计 机体Document31 pagesG495Q柴油机设计 机体bang KrisNo ratings yet

Download as pdf or txt

You might also like

- Osha 10-Hour Construction Industry: How To Use This Study GuideDocument39 pagesOsha 10-Hour Construction Industry: How To Use This Study GuideGabriel ParksNo ratings yet

- ELEMENTS OF COST Students NotesDocument6 pagesELEMENTS OF COST Students NotesJkuat MSc. P & L100% (1)

- Informatica Forence 10 2013Document62 pagesInformatica Forence 10 2013Carlos Bernal100% (1)

- CH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisDocument84 pagesCH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisankonmahmudNo ratings yet

- Gross National Income Per Capita 2019, Atlas Method and PPPDocument4 pagesGross National Income Per Capita 2019, Atlas Method and PPPElisha WankogereNo ratings yet

- Swarm WhitepaperDocument46 pagesSwarm WhitepaperJoel Dietz100% (1)

- Chapter-4: Manufacturing Cost Elements and Cost Estimation For Various ProcessDocument21 pagesChapter-4: Manufacturing Cost Elements and Cost Estimation For Various ProcessTerefa FeyisaNo ratings yet

- Java NotesDocument15 pagesJava NotesIqbal HawreNo ratings yet

- ME Module 5Document12 pagesME Module 5Pratham J TudoorNo ratings yet

- Managerial Accounting and Cost ConceptsDocument50 pagesManagerial Accounting and Cost ConceptsGigo Kafare BinoNo ratings yet

- Blocher8e EOC SM Ch03 FinalDocument27 pagesBlocher8e EOC SM Ch03 FinalDiah ArmelizaNo ratings yet

- Cost Concept and ClassificationDocument45 pagesCost Concept and ClassificationMountaha0% (1)

- Lecture 3 - Cost ConceptsDocument23 pagesLecture 3 - Cost ConceptsEmmanuel NamkumbeNo ratings yet

- Brewer 8e PPT Ch01 TDocument54 pagesBrewer 8e PPT Ch01 TJuan Camilo IdarragaNo ratings yet

- Managerial Accounting and Cost Concepts: Solutions To QuestionsDocument13 pagesManagerial Accounting and Cost Concepts: Solutions To QuestionsGera MatsNo ratings yet

- Cost Engineering Lecture NoteDocument62 pagesCost Engineering Lecture Notefentawmelaku1993No ratings yet

- 2B - Unit 2 - Cost Classification Behaviour & Estimation - Workbook SOLUTIONS - 2022Document47 pages2B - Unit 2 - Cost Classification Behaviour & Estimation - Workbook SOLUTIONS - 2022Bono magadaniNo ratings yet

- Managerial Accounting and Cost ConceptsDocument62 pagesManagerial Accounting and Cost ConceptsJuana BoresNo ratings yet

- 1a Cost Classification Form Manufacturing PT of View and Predicting Cost Behaviour - 19 - 12 - 2023Document12 pages1a Cost Classification Form Manufacturing PT of View and Predicting Cost Behaviour - 19 - 12 - 2023Md Rashadul IslamNo ratings yet

- L5 - Types of Costs and Cost Estimation of A ProductDocument82 pagesL5 - Types of Costs and Cost Estimation of A ProducthayliyesusNo ratings yet

- Cost Terms, Concepts, and Classifications: Solutions To QuestionsDocument14 pagesCost Terms, Concepts, and Classifications: Solutions To QuestionsTrishia OliverosNo ratings yet

- CHAPTER 2 Question SolutionsDocument3 pagesCHAPTER 2 Question Solutionscamd1290100% (1)

- Bgteu v2s60Document15 pagesBgteu v2s60maye dataelNo ratings yet

- Chapter 2 - Cost Concepts and Design Economics SolutionsDocument31 pagesChapter 2 - Cost Concepts and Design Economics SolutionsArin Park100% (1)

- Assignment Topics (Case Study-Based) : (Refer Notes On SLE That Has Been Circulated)Document8 pagesAssignment Topics (Case Study-Based) : (Refer Notes On SLE That Has Been Circulated)Bharath T SNo ratings yet

- Introduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualDocument25 pagesIntroduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualMaryJohnsonsmni100% (61)

- An Introduction To Cost Terms and Purposes 2-1Document33 pagesAn Introduction To Cost Terms and Purposes 2-1Moayad TeimatNo ratings yet

- Summary On Cost Concpts and ClassificationsDocument7 pagesSummary On Cost Concpts and ClassificationsMa. Roycelean PascualNo ratings yet

- CT 206 Notes-1Document56 pagesCT 206 Notes-1Flex GodNo ratings yet

- L1-Manufacturer's CostDocument19 pagesL1-Manufacturer's CostomarNo ratings yet

- What Are The Types of Costs in Cost AccountingDocument2 pagesWhat Are The Types of Costs in Cost AccountingAhmed HassanNo ratings yet

- Muslim University of Morogoro - 090058Document14 pagesMuslim University of Morogoro - 090058mika piusNo ratings yet

- Khanda Habeeb RaheemDocument12 pagesKhanda Habeeb RaheemHarith EmaadNo ratings yet

- Inventory: COST OF PRODUCTIONDocument104 pagesInventory: COST OF PRODUCTIONHAFIZ MUHAMMAD UMAR FAROOQ RANANo ratings yet

- Cost HandoutDocument31 pagesCost HandoutTilahun GirmaNo ratings yet

- Garment Costing: Minnie BastinDocument73 pagesGarment Costing: Minnie BastinBastinNo ratings yet

- Econ Module 1 Unit 2Document20 pagesEcon Module 1 Unit 2Lester VirayNo ratings yet

- An Introduction To Managerial Accounting and Cost ConceptsDocument38 pagesAn Introduction To Managerial Accounting and Cost ConceptsHoàng TrangNo ratings yet

- Cost ConceptsDocument56 pagesCost ConceptsAngela De chavezNo ratings yet

- 20200912024025SLCHIA005MA2 Notes Cost BehaviourDocument24 pages20200912024025SLCHIA005MA2 Notes Cost BehaviourDương DươngNo ratings yet

- Elements of Cost: Manisha VermaDocument31 pagesElements of Cost: Manisha VermaPriyanshNo ratings yet

- Unit 1 Section 6Document7 pagesUnit 1 Section 6Babamu Kalmoni JaatoNo ratings yet

- BBA 2003 Cost AccountingDocument24 pagesBBA 2003 Cost AccountingVentus TanNo ratings yet

- Topic 13 Finance For Small BusinessDocument23 pagesTopic 13 Finance For Small BusinessdesaeNo ratings yet

- A Assignment ON "Examples Where Direct Expenses Are Not Included in The Cost of Production"Document7 pagesA Assignment ON "Examples Where Direct Expenses Are Not Included in The Cost of Production"parikharistNo ratings yet

- Chapter 2 UpdatedDocument58 pagesChapter 2 Updatedbing bongNo ratings yet

- Apply Cost FactorDocument23 pagesApply Cost FactoreyasuNo ratings yet

- Introduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualDocument36 pagesIntroduction To Managerial Accounting Canadian 5th Edition Brewer Solutions Manualfayedavidsonhet0cs100% (25)

- Cost Concepts: According To Management FunctionDocument10 pagesCost Concepts: According To Management FunctionQuenn NavalNo ratings yet

- Lec 04 - Managerial Accounting (Concepts & Principles)Document36 pagesLec 04 - Managerial Accounting (Concepts & Principles)Sakib RafeeNo ratings yet

- Cost: As A Resource Sacrificed or Forgone To Achieve A Specific Objective. It Is Usually MeasuredDocument19 pagesCost: As A Resource Sacrificed or Forgone To Achieve A Specific Objective. It Is Usually MeasuredTilahun GirmaNo ratings yet

- Elements of Cost and Its Impact of PricingDocument12 pagesElements of Cost and Its Impact of PricingAnu PriyaNo ratings yet

- Cost Terms, Concepts, and Classifications: Solution To Discussion CaseDocument48 pagesCost Terms, Concepts, and Classifications: Solution To Discussion Casekasad jdnfrnasNo ratings yet

- Cost Concepts and ClassificationsDocument3 pagesCost Concepts and ClassificationsCONCORDIA RAFAEL IVANNo ratings yet

- Costs: Different Ways To Categorize CostsDocument7 pagesCosts: Different Ways To Categorize Costsraul_mahadikNo ratings yet

- Elements of CostDocument17 pagesElements of CostManikant SAhNo ratings yet

- A Study On Cost Control Techniques in Ultratech Cement Company, BengaluruDocument76 pagesA Study On Cost Control Techniques in Ultratech Cement Company, BengaluruChethan.sNo ratings yet

- Solution Manual For Discrete Mathematics and Its Applications 8th Edition by RosenDocument24 pagesSolution Manual For Discrete Mathematics and Its Applications 8th Edition by RosenEileenLeexseb100% (42)

- Chapter 2 Cost Accounting ConceptsDocument22 pagesChapter 2 Cost Accounting ConceptsRosliana RazabNo ratings yet

- Manufacturing ManagementDocument126 pagesManufacturing ManagementSIDDHARTH JHANo ratings yet

- COST Lesson 2Document4 pagesCOST Lesson 2Christian Clyde Zacal Ching0% (1)

- Chapter 2 Answer PDFDocument19 pagesChapter 2 Answer PDFCris VillarNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Integration of Smart Carts in Puregold SupermarketDocument153 pagesIntegration of Smart Carts in Puregold SupermarketKen ParilNo ratings yet

- Office Management Tools (16rsbe7:2) : Sengamalathayaar Educational Trust Women'S CollegeDocument15 pagesOffice Management Tools (16rsbe7:2) : Sengamalathayaar Educational Trust Women'S CollegeKumaran RaniNo ratings yet

- Government of Madhya Pradesh Public Health Engineering DepartmentDocument63 pagesGovernment of Madhya Pradesh Public Health Engineering DepartmentShreyansh SharmaNo ratings yet

- Makalah CJR BibDocument9 pagesMakalah CJR BibRyan AlfandiNo ratings yet

- Advertising 5Document41 pagesAdvertising 5Sông HươngNo ratings yet

- Nantes2018 FLV VerrieresV4Document9 pagesNantes2018 FLV VerrieresV4Fikri Bin Abdul ShukorNo ratings yet

- The Embassy in Jakarta - Overview (2012) PDFDocument17 pagesThe Embassy in Jakarta - Overview (2012) PDFHo Yiu YinNo ratings yet

- Busy Accounting Software Standard EditionDocument4 pagesBusy Accounting Software Standard EditionpremsinghjaniNo ratings yet

- Indian Ports Community SystemDocument6 pagesIndian Ports Community Systempatil sNo ratings yet

- Capital Expenditure Control: DR Palash BairagiDocument38 pagesCapital Expenditure Control: DR Palash Bairagisundaram MishraNo ratings yet

- Account Statement From 27 Mar 2022 To 5 Apr 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 27 Mar 2022 To 5 Apr 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancePiyush AgarwalNo ratings yet

- Introduction To GNU Radio and Software RadioDocument4 pagesIntroduction To GNU Radio and Software RadioDinesh VermaNo ratings yet

- Personal MKTG PKG - Part 2 V2Document3 pagesPersonal MKTG PKG - Part 2 V2Lakshya TripathiNo ratings yet

- The Perfect Site GuideDocument59 pagesThe Perfect Site GuideconstantrazNo ratings yet

- I LuxDocument24 pagesI LuxNirav M. BhavsarNo ratings yet

- In Design: Iman BokhariDocument12 pagesIn Design: Iman Bokharimena_sky11No ratings yet

- Ilan Group Operation Enterprise: Imran AminuddinDocument1 pageIlan Group Operation Enterprise: Imran AminuddinIzhar AminuddinNo ratings yet

- The Agricultural Futures MarketDocument10 pagesThe Agricultural Futures MarketBharath ChaitanyaNo ratings yet

- Coordination For Motor Protection: High Performance MCCBDocument0 pagesCoordination For Motor Protection: High Performance MCCBKishore KrishnaNo ratings yet

- Additive Manufacturing ProcessesDocument27 pagesAdditive Manufacturing ProcessesAizrul ShahNo ratings yet

- GodotDocument977 pagesGodotClaudio Alberto ManquirreNo ratings yet

- DEPRECIATIONDocument3 pagesDEPRECIATIONUsirika Sai KumarNo ratings yet

- Pantallas HITACHI DP 6X Training PackageDocument92 pagesPantallas HITACHI DP 6X Training PackagericardoNo ratings yet

- PSR I455Document4 pagesPSR I455caronNo ratings yet

- Project Proposal TemplateDocument2 pagesProject Proposal TemplatejorifeberdenuevoespinosaNo ratings yet

- G495Q柴油机设计 机体Document31 pagesG495Q柴油机设计 机体bang KrisNo ratings yet