Download as pdf or txt

You might also like

- Feasibility of Agrivet and Agricultural Supplies in Lake Sebu, South Cotabato, PhilippinesDocument6 pagesFeasibility of Agrivet and Agricultural Supplies in Lake Sebu, South Cotabato, PhilippinesNap Missionnaire75% (12)

- Instructions For Forms 1099-A and 1099-C: (Rev. January 2022)Document6 pagesInstructions For Forms 1099-A and 1099-C: (Rev. January 2022)Carlos BatisteNo ratings yet

- Financial Analysis-Sizing Up Firm Performance: Income Statement 2016 % of Sales Example CalculationsDocument30 pagesFinancial Analysis-Sizing Up Firm Performance: Income Statement 2016 % of Sales Example CalculationsanisaNo ratings yet

- The Statement of Comprehensive Income: Profit For The YearDocument4 pagesThe Statement of Comprehensive Income: Profit For The YearPlawan GhimireNo ratings yet

- IA 3 Chapter 20 River CoDocument1 pageIA 3 Chapter 20 River CoPrytj Elmo QuimboNo ratings yet

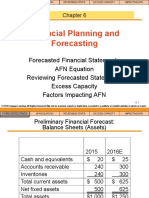

- Planning and ForecastingDocument16 pagesPlanning and ForecastingAinun Nisa NNo ratings yet

- Class 1 7th Feb OxygenDocument17 pagesClass 1 7th Feb OxygenAmit JainNo ratings yet

- Aguilar QuizDocument5 pagesAguilar QuizIankyle AguilarNo ratings yet

- Chapter 5-Financial Planning and ForecastingDocument20 pagesChapter 5-Financial Planning and ForecastingMOHAMAD SAFWAN BIN FAUZI STUDENTNo ratings yet

- Less: Interest On Debt (10% × ' 2,00,000) : © The Institute of Chartered Accountants of IndiaDocument16 pagesLess: Interest On Debt (10% × ' 2,00,000) : © The Institute of Chartered Accountants of IndiaGao YungNo ratings yet

- 12th Accountancy Chapter 1Document4 pages12th Accountancy Chapter 1Ankit JainNo ratings yet

- Ratios - Formulae and Explanation (2019 Version - Abridged)Document10 pagesRatios - Formulae and Explanation (2019 Version - Abridged)King JulianNo ratings yet

- Investment ValuationDocument16 pagesInvestment ValuationJaco CrouseNo ratings yet

- Theory of Capital Structure FMDocument25 pagesTheory of Capital Structure FMalphamal2017No ratings yet

- Compound Interest CalculatorDocument6 pagesCompound Interest Calculatorbajramo1No ratings yet

- IRA No. 4 Answer KeyDocument3 pagesIRA No. 4 Answer KeyProlen AcantoNo ratings yet

- Chapter 8 Performance Measurement Evaluation Nov2020 1Document113 pagesChapter 8 Performance Measurement Evaluation Nov2020 1Question BankNo ratings yet

- CN Divisional Performance Roi & RiDocument8 pagesCN Divisional Performance Roi & RiIqmal khushairiNo ratings yet

- Statement of Profit or Loss For The Year Ended 31 December 2016Document2 pagesStatement of Profit or Loss For The Year Ended 31 December 2016Plawan GhimireNo ratings yet

- Chapter 16 Advanced Accounting Solution ManualDocument94 pagesChapter 16 Advanced Accounting Solution ManualVanessa DozonNo ratings yet

- 80C CalculationDocument2 pages80C CalculationanandpurushothamanNo ratings yet

- Eva Tree ModelDocument11 pagesEva Tree Modelwelcome2jungleNo ratings yet

- Performance Evaluation and Decentralization: Discussion QuestionsDocument20 pagesPerformance Evaluation and Decentralization: Discussion QuestionsMc Jedh CabarrubiasNo ratings yet

- 3.1 Workshop 7 Capital Structure 2021Document2 pages3.1 Workshop 7 Capital Structure 2021bobhamilton3489No ratings yet

- For Yvone Company: 20M InvestmentDocument3 pagesFor Yvone Company: 20M InvestmentRamlei Jan G. RiveraNo ratings yet

- Hindustan Unilever Ltd. Financial ModelDocument15 pagesHindustan Unilever Ltd. Financial Modellasix47725No ratings yet

- PG 3Document6 pagesPG 3Prish AnandNo ratings yet

- Client: PT Jambi Prima Coal Closing Date: 31 Desember 2018Document7 pagesClient: PT Jambi Prima Coal Closing Date: 31 Desember 2018Umar MukhtarNo ratings yet

- Overall Profitability RatiosDocument12 pagesOverall Profitability RatiosAtharva VirehNo ratings yet

- Cost of Capital: Risk & ReturnDocument27 pagesCost of Capital: Risk & ReturnKrisi ManNo ratings yet

- CorpFin 2021 Fall 2 Risk Lecture 11Document27 pagesCorpFin 2021 Fall 2 Risk Lecture 11Krisi ManNo ratings yet

- Shareholder Value Creation-2Document5 pagesShareholder Value Creation-2tanadof294No ratings yet

- Investment Valuation Model TemplateDocument37 pagesInvestment Valuation Model TemplateousmaneNo ratings yet

- MAnagement and Services Accounting REportDocument14 pagesMAnagement and Services Accounting REportAessy AldeaNo ratings yet

- NEW INCOME TAX FORM 2023-24 Sakuntala MohantaDocument2 pagesNEW INCOME TAX FORM 2023-24 Sakuntala MohantaSHIELD LUCKYNo ratings yet

- Accounting BasicsDocument3 pagesAccounting BasicsmanichaitanyaNo ratings yet

- Financial Management Strategy-MBA-731: Work-SheetDocument8 pagesFinancial Management Strategy-MBA-731: Work-SheetEyuael SolomonNo ratings yet

- Chapter 16 Advanced Accounting Solution ManualDocument119 pagesChapter 16 Advanced Accounting Solution ManualAsuncion BarquerosNo ratings yet

- Income Tax Calculator FY 2020 2021Document8 pagesIncome Tax Calculator FY 2020 2021GhanshyamNo ratings yet

- Income Tax Calculator FY 2020 2021Document8 pagesIncome Tax Calculator FY 2020 2021bikofax543No ratings yet

- Test 4 ValuationDocument4 pagesTest 4 ValuationIrfan ShaikhNo ratings yet

- Project Red: Problem 9-3: Daisy CompanyDocument2 pagesProject Red: Problem 9-3: Daisy CompanyJPNo ratings yet

- Capital Structure TheoriesDocument12 pagesCapital Structure Theoriesganesh gowthamNo ratings yet

- IDFC FIRST Bank Limited Sixth Annual Report FY 2019 20Document273 pagesIDFC FIRST Bank Limited Sixth Annual Report FY 2019 20Sourabh PorwalNo ratings yet

- Chapter 3 - LeveragesDocument9 pagesChapter 3 - LeveragesParth GargNo ratings yet

- Gross Profit/net Sales Gross Profit/revenue Net Income/Total AssetsDocument85 pagesGross Profit/net Sales Gross Profit/revenue Net Income/Total AssetsMaria Dana BrillantesNo ratings yet

- Investment Objective: Fund Fact Sheet As of September 2020Document2 pagesInvestment Objective: Fund Fact Sheet As of September 2020Neil MijaresNo ratings yet

- Income and Expenditure of JakartaDocument10 pagesIncome and Expenditure of JakartaAlfi Nur LailiyahNo ratings yet

- CA Inter FM Super 50 Q by Sanjay Saraf SirDocument129 pagesCA Inter FM Super 50 Q by Sanjay Saraf SirSaroj AdhikariNo ratings yet

- Chap - Test - CH4 - Financial Ratio Analysis and Their Implications To ManagementDocument10 pagesChap - Test - CH4 - Financial Ratio Analysis and Their Implications To Managementroyette ladicaNo ratings yet

- Quiz # 1Document1 pageQuiz # 1JamNo ratings yet

- Tax Rebate Calculator of Salaried Class Indviduals 2013-14Document4 pagesTax Rebate Calculator of Salaried Class Indviduals 2013-14waheedNo ratings yet

- CF Assignment 3 (B)Document13 pagesCF Assignment 3 (B)Just Some EditsNo ratings yet

- Microdrive Case SolutionDocument3 pagesMicrodrive Case SolutionKING KARTHIKNo ratings yet

- HFMDocument1 pageHFMJPNo ratings yet

- Lebanon's Economy An Analysis and Some Recommendations: Esther Baroudy & Hady Farah 20 January 2020Document17 pagesLebanon's Economy An Analysis and Some Recommendations: Esther Baroudy & Hady Farah 20 January 2020terryhadyNo ratings yet

- Balance Sheet: Abakada EnterpriseDocument2 pagesBalance Sheet: Abakada EnterpriseBea GarciaNo ratings yet

- Why Debt Is CheapDocument1 pageWhy Debt Is CheapWhirlMindNo ratings yet

- Slides Credit Analysis Corporate Credit Analysis RatiosDocument22 pagesSlides Credit Analysis Corporate Credit Analysis Ratiosabdalla hafezNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Bacao ES - Bank-Reconciliation-Statement - February 2021Document2 pagesBacao ES - Bank-Reconciliation-Statement - February 2021Mhalou Jocson EchanoNo ratings yet

- Financial Statement AnalysisDocument6 pagesFinancial Statement AnalysisuaenaNo ratings yet

- Market Cap To GDP RatioDocument8 pagesMarket Cap To GDP RatiokalpeshNo ratings yet

- Test 1Document11 pagesTest 1VânAnh Nguyễn100% (1)

- Financials - Biomass Briquetting - 5 YearsDocument14 pagesFinancials - Biomass Briquetting - 5 YearsSHARMA TRAVELS LATURNo ratings yet

- ADB ExampleDocument2 pagesADB Examplealexapodadera4No ratings yet

- Chapter 8 - ProblemDocument26 pagesChapter 8 - ProblemMa. Leonor Nikka CuevasNo ratings yet

- 2Q10 Op Fund Quarterly LetterDocument24 pages2Q10 Op Fund Quarterly Letterscribduser76No ratings yet

- Tai Chinh Quoc Te Nguyen Cam Nhung c4 The Theory of Purchasing Power Parity (PPP) and Generalized Model of The Exchange Rate (Cuuduongthancong - Com)Document35 pagesTai Chinh Quoc Te Nguyen Cam Nhung c4 The Theory of Purchasing Power Parity (PPP) and Generalized Model of The Exchange Rate (Cuuduongthancong - Com)Thái Nguyễn Thị HồngNo ratings yet

- 2020 Annual ReportDocument128 pages2020 Annual ReportSaul PimientaNo ratings yet

- FS Gudang SIMULATION 50050Document82 pagesFS Gudang SIMULATION 50050Wibowo 'woki' Siswo NNo ratings yet

- Torque v1.41Document35 pagesTorque v1.41suchitasamalNo ratings yet

- Making Capital Investment Decisions: Mcgraw-Hill/IrwinDocument32 pagesMaking Capital Investment Decisions: Mcgraw-Hill/Irwinsarvenaz kamali matinNo ratings yet

- Math 101 Simple and Compound InterestDocument41 pagesMath 101 Simple and Compound InterestAdi Garcia ArcenasNo ratings yet

- Tender Schedule Interior Works Union Bank of India Collectorate Branch Jagtial Ro KarimnagarDocument54 pagesTender Schedule Interior Works Union Bank of India Collectorate Branch Jagtial Ro KarimnagarashokNo ratings yet

- New Mooe Forms 2024 - Inset4 6Document125 pagesNew Mooe Forms 2024 - Inset4 6Noemi MoradoNo ratings yet

- Bonds Payable PDFDocument6 pagesBonds Payable PDFAnthony Tunying MantuhacNo ratings yet

- E0023 - Home Loans - HDFC BankDocument79 pagesE0023 - Home Loans - HDFC BankwebstdsnrNo ratings yet

- 2nd TQ With Tos He 6Document7 pages2nd TQ With Tos He 6Raymund BondeNo ratings yet

- Tax Law Research Paper TopicsDocument5 pagesTax Law Research Paper Topicsxfdacdbkf100% (1)

- Chapter 21. Capital Budgeting and Cost Analysis (Cost Accounting)Document54 pagesChapter 21. Capital Budgeting and Cost Analysis (Cost Accounting)Nguyen Dac Thich100% (2)

- Instant Personal Loan - OfferingfinserveDocument9 pagesInstant Personal Loan - Offeringfinserveoffering serveNo ratings yet

- Accounting Week 2Document3 pagesAccounting Week 2Erryn M. ParamythaNo ratings yet

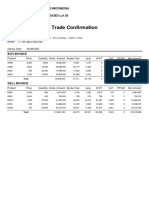

- Trade ConfirmationDocument2 pagesTrade Confirmationfrahmana01No ratings yet

- ch12 - Debt FinancingDocument60 pagesch12 - Debt Financingsongvuthy100% (1)

- Smart Junior Product Brochure NewDocument11 pagesSmart Junior Product Brochure Newmanuk193No ratings yet

- Risk-Adjusted Return On Capital ModelsDocument27 pagesRisk-Adjusted Return On Capital ModelsA. Saeed KhawajaNo ratings yet

- Introduction To Risk and Return: Mohd Effandi Bin Yusoff Faculty of Management and Human Resource ManagementDocument23 pagesIntroduction To Risk and Return: Mohd Effandi Bin Yusoff Faculty of Management and Human Resource ManagementIqbal AzharNo ratings yet

- Ministry of Corporate Affairs Receipt G.A.R.7: Icici BankDocument1 pageMinistry of Corporate Affairs Receipt G.A.R.7: Icici BankBhavin SagarNo ratings yet