Download as xlsx, pdf, or txt

You might also like

- Partnership Formation: Name: Date: Professor: Section: Score: QuizDocument5 pagesPartnership Formation: Name: Date: Professor: Section: Score: QuizWenjun100% (3)

- Financial Analysis Homework Week 8Document15 pagesFinancial Analysis Homework Week 8effulgentflameNo ratings yet

- Partnership Formation ActivityDocument8 pagesPartnership Formation ActivityShaira UntalanNo ratings yet

- Supplement Chapter 5 DT AnswersDocument11 pagesSupplement Chapter 5 DT AnswersJea BalagtasNo ratings yet

- 2the Complete Biogas HandbookDocument7 pages2the Complete Biogas HandbookJhe Inibam100% (1)

- Parcor CompuDocument14 pagesParcor CompuErika delos Santos100% (3)

- B.) CC, P25,000: PP, P21,000 Aa, P38,000Document22 pagesB.) CC, P25,000: PP, P21,000 Aa, P38,000Wendelyn TutorNo ratings yet

- Quiz 3 Partnership DissolutionDocument6 pagesQuiz 3 Partnership DissolutionWenjun100% (1)

- Admission of A New Partner: Total AssetsDocument10 pagesAdmission of A New Partner: Total AssetsJuliana Cheng100% (5)

- FIL 124 - Final TestDocument16 pagesFIL 124 - Final TestChavey Jean V. RenidoNo ratings yet

- Working Papers For Partnership DissolutionDocument21 pagesWorking Papers For Partnership DissolutioncaraaatbongNo ratings yet

- Dissolution and Liquidation Sample ProblemsDocument5 pagesDissolution and Liquidation Sample ProblemsShaz NagaNo ratings yet

- Partnership DissolutionDocument15 pagesPartnership DissolutionAbc xyzNo ratings yet

- Quiz - Chapter 3 - Partnership Dissolution - 2020 EditionDocument4 pagesQuiz - Chapter 3 - Partnership Dissolution - 2020 EditionHell Luci50% (2)

- Acctg301 PartnershipDissolutionDocument16 pagesAcctg301 PartnershipDissolutionTiu Voughn ImmanuelNo ratings yet

- Afar302 A - PD 3Document5 pagesAfar302 A - PD 3Nicole TeruelNo ratings yet

- Partnership Dissolution Name: Date: Professor: Section: Score: QuizDocument5 pagesPartnership Dissolution Name: Date: Professor: Section: Score: QuizNahwi KimpaNo ratings yet

- p1 Quiz With TheoryDocument15 pagesp1 Quiz With TheoryGrace CorpoNo ratings yet

- p1 Quiz With TheoryDocument16 pagesp1 Quiz With TheoryRica RegorisNo ratings yet

- Partnership Dissolution - 2Document27 pagesPartnership Dissolution - 2Trisha GarciaNo ratings yet

- Quiz 1 Partnership AnswersDocument4 pagesQuiz 1 Partnership Answersdianel villarico100% (2)

- QUIZ 02: Partnership Operations Name: - ID No.Document6 pagesQUIZ 02: Partnership Operations Name: - ID No.yoj cepilloNo ratings yet

- AFAR 03 Partnership DissolutionDocument4 pagesAFAR 03 Partnership DissolutionDerick jorgeNo ratings yet

- 110 Quiz3 PartnershipDocument3 pages110 Quiz3 PartnershipKN DumpNo ratings yet

- NSBZDocument6 pagesNSBZKenncy100% (4)

- Quiz - Chapter 4 - Partnership Liquidation - 2020 EditionDocument4 pagesQuiz - Chapter 4 - Partnership Liquidation - 2020 EditionHell LuciNo ratings yet

- ILLUSTRATIVE PROBLEMS - Partnership Dissolution (Change in Ownership Structure)Document5 pagesILLUSTRATIVE PROBLEMS - Partnership Dissolution (Change in Ownership Structure)Mathew LumapasNo ratings yet

- Partnership 2Document45 pagesPartnership 2Леиа Аморес0% (1)

- AST Seatwork - 05 15 2021Document6 pagesAST Seatwork - 05 15 2021Joshua UmaliNo ratings yet

- Dissolution Problems DiscussionDocument8 pagesDissolution Problems DiscussionCalmaMoyjeNo ratings yet

- Long QuizDocument5 pagesLong QuizMitch Tokong MinglanaNo ratings yet

- CHAPTER 13 PROB 1-2 - GOZUNKAYE - XLSX - Sheet1Document10 pagesCHAPTER 13 PROB 1-2 - GOZUNKAYE - XLSX - Sheet1kaye gozunNo ratings yet

- Partnership ExercisesDocument17 pagesPartnership ExercisesDan RyanNo ratings yet

- Partnership Dissolution 4Document6 pagesPartnership Dissolution 4Karl Wilson GonzalesNo ratings yet

- Larong Aihzel G. Ast Long Quiz 1Document5 pagesLarong Aihzel G. Ast Long Quiz 1Mitch Tokong MinglanaNo ratings yet

- Partnership Operations - AssignmentDocument6 pagesPartnership Operations - AssignmentRosmar AbanerraNo ratings yet

- Dissolution Problems DiscussionDocument9 pagesDissolution Problems Discussionlexfred55No ratings yet

- RESA MCQsDocument56 pagesRESA MCQsWendelyn Tutor100% (1)

- AFAR - Partnership Formation and OperationDocument2 pagesAFAR - Partnership Formation and OperationJoanna Rose DeciarNo ratings yet

- Partnership DissolutionDocument5 pagesPartnership DissolutionJae Nathaniel Arroyo OronanNo ratings yet

- Some Advac Problems by DayagDocument6 pagesSome Advac Problems by DayagElijah Montefalco100% (1)

- Template - QE - Advance AccountingDocument18 pagesTemplate - QE - Advance AccountingJykx SiaoNo ratings yet

- Sol. Man. - Chapter 13 - Partnership DissolutionDocument8 pagesSol. Man. - Chapter 13 - Partnership DissolutionPeter PiperNo ratings yet

- Case 1: Purhase of Interest - Goodwill To Old PartnersDocument12 pagesCase 1: Purhase of Interest - Goodwill To Old PartnersAEDRIAN LEE DERECHONo ratings yet

- Prelim PartnershipDissolutionSampleProblemDocument12 pagesPrelim PartnershipDissolutionSampleProblemLee SuarezNo ratings yet

- Partnership Operations - 2021 Online ClassDocument38 pagesPartnership Operations - 2021 Online ClassAnne AlagNo ratings yet

- Sol. Man. - Chapter 13 - Partnership DissolutionDocument7 pagesSol. Man. - Chapter 13 - Partnership DissolutioncpawannabeNo ratings yet

- School of Accountancy & Management Accounting For Special Transaction Midterm ExaminationDocument11 pagesSchool of Accountancy & Management Accounting For Special Transaction Midterm ExaminationTasha MarieNo ratings yet

- Lesson 4 Partnership DissolutionDocument17 pagesLesson 4 Partnership DissolutionheyheyNo ratings yet

- Assignment 1 - Partnership DissolutionDocument7 pagesAssignment 1 - Partnership DissolutionchxrlttxNo ratings yet

- Chapter 3Document13 pagesChapter 3Adan EveNo ratings yet

- Partnership LiquidationDocument31 pagesPartnership LiquidationRosmar AbanerraNo ratings yet

- Retirement of A PartnerDocument6 pagesRetirement of A Partnerprksh_451253087No ratings yet

- Quiz 2 - Dissolution and LiquidationDocument2 pagesQuiz 2 - Dissolution and LiquidationMarcel BermudezNo ratings yet

- Partnership DissolutionDocument7 pagesPartnership DissolutionAngel Frolen B. RacinezNo ratings yet

- Afar 2 - 3Document1 pageAfar 2 - 3Panda ErarNo ratings yet

- AST 4-Partnership DissolutionDocument9 pagesAST 4-Partnership DissolutionMarvin MercadoNo ratings yet

- Partnership FormationDocument12 pagesPartnership FormationAbc xyzNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Wiley Practitioner's Guide to GAAS 2017: Covering all SASs, SSAEs, SSARSs, and InterpretationsFrom EverandWiley Practitioner's Guide to GAAS 2017: Covering all SASs, SSAEs, SSARSs, and InterpretationsNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Activity in Accounting For CorporationDocument2 pagesActivity in Accounting For CorporationcaraaatbongNo ratings yet

- Working Papers For CorporationDocument8 pagesWorking Papers For CorporationcaraaatbongNo ratings yet

- DepletionDocument2 pagesDepletioncaraaatbongNo ratings yet

- 2nd Interim in Purposive CommunicationDocument4 pages2nd Interim in Purposive CommunicationcaraaatbongNo ratings yet

- Purposivecommunication - Communication Processes, Principles, and Ethics (Autosaved)Document24 pagesPurposivecommunication - Communication Processes, Principles, and Ethics (Autosaved)caraaatbongNo ratings yet

- MT MBAFACRR1X With Answers For StudentsDocument15 pagesMT MBAFACRR1X With Answers For StudentscaraaatbongNo ratings yet

- Chapter3purposivecom 201108134308Document29 pagesChapter3purposivecom 201108134308caraaatbongNo ratings yet

- Chapter 4 - Incorporation of PartnershpDocument8 pagesChapter 4 - Incorporation of PartnershpcaraaatbongNo ratings yet

- Assignment in Partnership OperationsDocument4 pagesAssignment in Partnership OperationscaraaatbongNo ratings yet

- Finals Reviewer DevpsychDocument15 pagesFinals Reviewer DevpsychcaraaatbongNo ratings yet

- Enhancing Procurement Strategies For Resolving Agency Issues in ClientDocument6 pagesEnhancing Procurement Strategies For Resolving Agency Issues in ClientcaraaatbongNo ratings yet

- Reviewer in Business FinanceDocument2 pagesReviewer in Business FinancecaraaatbongNo ratings yet

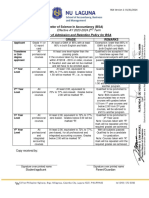

- NU Laguna BSA Admission and Retention Policy Revised 02152024Document1 pageNU Laguna BSA Admission and Retention Policy Revised 02152024caraaatbongNo ratings yet

- POCHEBSA231CDocument1 pagePOCHEBSA231CcaraaatbongNo ratings yet

- NSTP 1 ReviewerDocument6 pagesNSTP 1 ReviewercaraaatbongNo ratings yet

- The Contemporary World ReviewerDocument4 pagesThe Contemporary World ReviewercaraaatbongNo ratings yet

- Jemina InsightsDocument1 pageJemina InsightscaraaatbongNo ratings yet

- Quiz Two: University of Hong Kong CCCH9007 China in The Global EconomyDocument3 pagesQuiz Two: University of Hong Kong CCCH9007 China in The Global EconomyChunming TangNo ratings yet

- Chapter 003 Fundamentals of Cost-Volume-Profit Analysis: True / False QuestionsDocument39 pagesChapter 003 Fundamentals of Cost-Volume-Profit Analysis: True / False QuestionsNaddieNo ratings yet

- Demand Andrews ChecksDocument2 pagesDemand Andrews ChecksCo AlexinneNo ratings yet

- Anna University: Centre For Distance EducationDocument1 pageAnna University: Centre For Distance EducationMeghal SivanNo ratings yet

- 辽宁维航基业科技有限公司 Vh-Marinetech Co.,LtdDocument21 pages辽宁维航基业科技有限公司 Vh-Marinetech Co.,Ltdding liuNo ratings yet

- AP General Ledger Accounting TcodesDocument169 pagesAP General Ledger Accounting TcodesSai MuraliNo ratings yet

- Supply Chain Management ReportsDocument19 pagesSupply Chain Management ReportsSazeeth SinghNo ratings yet

- IMF and World BankDocument2 pagesIMF and World BankMinh HàNo ratings yet

- Prospectus MPL 33rd - National U17 2023Document8 pagesProspectus MPL 33rd - National U17 2023sanchita yadav100% (1)

- DITO Tower Civil Work - Acceptance Checklist 20200521-TCW - 1625704814Document1 pageDITO Tower Civil Work - Acceptance Checklist 20200521-TCW - 1625704814bashirNo ratings yet

- Gyan Ganga: Institute of Technology &sciencesDocument6 pagesGyan Ganga: Institute of Technology &sciencesMandhir NarangNo ratings yet

- Jim Rickard SDocument49 pagesJim Rickard SCaio RossiNo ratings yet

- Kendriya Vidyalaya Dipatoli Formative Assessment - III, (2015-16) Time-Class-V (FIVE) M.M - Grade A+ Subject - Environmental StudiesDocument5 pagesKendriya Vidyalaya Dipatoli Formative Assessment - III, (2015-16) Time-Class-V (FIVE) M.M - Grade A+ Subject - Environmental StudiesSUBHANo ratings yet

- Commercial Building Structural Design ReportDocument76 pagesCommercial Building Structural Design ReportPrakash Singh RawalNo ratings yet

- Standard: APA Citation BasicsDocument3 pagesStandard: APA Citation BasicsAmhara AammhhaarraaNo ratings yet

- Slot Drain Data Sheet - CompDocument1 pageSlot Drain Data Sheet - CompKhalilNo ratings yet

- Customer Based Brand Equity PyramidDocument21 pagesCustomer Based Brand Equity Pyramidsaritaon_1985100% (1)

- TANAPatrika August 2022Document64 pagesTANAPatrika August 2022anushaNo ratings yet

- HousekeepingDocument29 pagesHousekeepingMenchie Rose D. MendezNo ratings yet

- PCFC ReceiptDocument1 pagePCFC ReceiptsalesNo ratings yet

- Sa20086 Chiow Zhao Ying - Assignment 6Document5 pagesSa20086 Chiow Zhao Ying - Assignment 6Zhao YingNo ratings yet

- Activity Based CostingDocument37 pagesActivity Based CostingnuraidaNo ratings yet

- Del Campo, Blessie Ann C. Bsba HRM 2C Eco-Module4 AssignmentDocument4 pagesDel Campo, Blessie Ann C. Bsba HRM 2C Eco-Module4 AssignmentPALE ELIJAH JOSHUA D.No ratings yet

- Apollo Medicine InvoiceMay 19 2022 15 11Document1 pageApollo Medicine InvoiceMay 19 2022 15 11CA Sumit GargNo ratings yet

- آثار النمو الحضري على ديناميكية المجال الحضري للمدينة الجزائريةDocument18 pagesآثار النمو الحضري على ديناميكية المجال الحضري للمدينة الجزائريةالسعيد1992 نايت الحاجNo ratings yet

- LRFDDocument14 pagesLRFDKrischanSayloGelasanNo ratings yet

- Module 2 - 3 Cost Benefit Evaluation TechniquesDocument15 pagesModule 2 - 3 Cost Benefit Evaluation TechniquesKarthik GoudNo ratings yet