Res 293351

Res 293351

You might also like

- Financial Accounting Notes B.com 1st SemDocument64 pagesFinancial Accounting Notes B.com 1st SemJeevesh Roy0% (1)

- Singer Sewing Machine Model 1120Document38 pagesSinger Sewing Machine Model 1120bonehead6967% (6)

- Multiple Choice Questions 1 You Are Bidding in A Second PriceDocument2 pagesMultiple Choice Questions 1 You Are Bidding in A Second Pricetrilocksp SinghNo ratings yet

- Introduction To Financial AccountingDocument64 pagesIntroduction To Financial AccountingAnonymous HumanNo ratings yet

- Fundamentals of AccountingDocument18 pagesFundamentals of AccountingganeshvarmabattulaNo ratings yet

- CA FOUNDATION PAPER 1 ch1Document9 pagesCA FOUNDATION PAPER 1 ch1Saksham NaugaiNo ratings yet

- Part 1 - AccountingDocument12 pagesPart 1 - AccountingAmr YoussefNo ratings yet

- Syllabus: Subject - Financial AccountingDocument30 pagesSyllabus: Subject - Financial AccountingGaurav KhatriNo ratings yet

- Accounting Concepts and ConventionsDocument45 pagesAccounting Concepts and ConventionsPankaj SahaniNo ratings yet

- Basics of Accounting For MBA HRDocument19 pagesBasics of Accounting For MBA HRKundan JhaNo ratings yet

- 6-Principles and Concepts of Measuring IncomeDocument25 pages6-Principles and Concepts of Measuring Incomechobiipiggy26No ratings yet

- Chapter 1 Introduction To AccountingDocument35 pagesChapter 1 Introduction To AccountingdianeNo ratings yet

- BCOM 1 Financial Accounting 1Document63 pagesBCOM 1 Financial Accounting 1karthikeyan01No ratings yet

- Chapter 3A UnlockedDocument28 pagesChapter 3A UnlockedYashNo ratings yet

- Introduction To Accounting 2015-2016: Andreea PonorîcăDocument18 pagesIntroduction To Accounting 2015-2016: Andreea PonorîcăRaluca ToneNo ratings yet

- What Are The 3 Definition of Accounting?Document1 pageWhat Are The 3 Definition of Accounting?Sheila Grace BajaNo ratings yet

- BodyDocument15 pagesBodyRudrasish BeheraNo ratings yet

- Basics of Accounting - I: Financial Accounting / Isu Manufacturing Prithwiraj Sen SarmaDocument40 pagesBasics of Accounting - I: Financial Accounting / Isu Manufacturing Prithwiraj Sen Sarmakadir2613No ratings yet

- Amity Business School: MBA Class of 2011, Semester I Accounting For ManagementDocument27 pagesAmity Business School: MBA Class of 2011, Semester I Accounting For Managementkumaranil_1983No ratings yet

- Chapter 1 IntroductionDocument30 pagesChapter 1 IntroductionVivek GargNo ratings yet

- Lesson 1Document22 pagesLesson 1PoonamNo ratings yet

- المحاسبة باللغة الانجليزية ٤Document16 pagesالمحاسبة باللغة الانجليزية ٤wead888No ratings yet

- Financial Accounting-An Overview: Course ObjectiveDocument6 pagesFinancial Accounting-An Overview: Course ObjectiveJohn DoeNo ratings yet

- Syllabus: Subject - Financial AccountingDocument74 pagesSyllabus: Subject - Financial AccountingAnitha RNo ratings yet

- pptDocument66 pagespptNandini YadavNo ratings yet

- Accounting Concepts and Conventions 1Document48 pagesAccounting Concepts and Conventions 1Jatin PandayNo ratings yet

- Theory Base of Accounting, As and IFRSDocument39 pagesTheory Base of Accounting, As and IFRSYash Goyal0% (1)

- 2 Financial Accounting - Principles - GAAP 22102021 040821pmDocument10 pages2 Financial Accounting - Principles - GAAP 22102021 040821pmSomia aliNo ratings yet

- Paid CourseDocument278 pagesPaid CourseAkshay GajghateNo ratings yet

- Importance of Accounting: IdentifiesDocument20 pagesImportance of Accounting: IdentifiesNikhil GargNo ratings yet

- Advanced Financial Accounting I Lecture NoteDocument49 pagesAdvanced Financial Accounting I Lecture NoteBosz icon DyliteNo ratings yet

- Ch.13 Accounting StandardsDocument33 pagesCh.13 Accounting StandardsMalayaranjan PanigrahiNo ratings yet

- Accounting FOR ManagementDocument63 pagesAccounting FOR ManagementAnonymous 1ClGHbiT0JNo ratings yet

- Chapter-13 Preparation of Final Accounts of Sole Proprietors PDFDocument20 pagesChapter-13 Preparation of Final Accounts of Sole Proprietors PDFTarushi Yadav , 51BNo ratings yet

- Accountancy B.com Matterial (Final-2017)Document43 pagesAccountancy B.com Matterial (Final-2017)Bheeshm SinghNo ratings yet

- Icte 1033 ModsDocument4 pagesIcte 1033 ModsJoleen DoniegoNo ratings yet

- Confras First Sem LectureDocument52 pagesConfras First Sem LectureRosette SANTOSNo ratings yet

- Concepts: Introduction To Financial AccountingDocument30 pagesConcepts: Introduction To Financial Accountingbmurali37No ratings yet

- Accounting Principles: Accounting Concepts Accounting Conventions System of Book-Keeping System of AccountingDocument11 pagesAccounting Principles: Accounting Concepts Accounting Conventions System of Book-Keeping System of Accountingvinodgupta1960No ratings yet

- Financial Accounting CH1Document23 pagesFinancial Accounting CH1Kunal PradhanNo ratings yet

- Accounting 1 LectureDocument8 pagesAccounting 1 LecturePia louise RamosNo ratings yet

- Chapter Two: Accounting Concepts and PrinciplesDocument45 pagesChapter Two: Accounting Concepts and PrinciplesZerihunNo ratings yet

- Cfi Accounting EbookDocument66 pagesCfi Accounting Ebookmanjit13121990No ratings yet

- Cfi Accounting EbookDocument66 pagesCfi Accounting EbookAmjid MalNo ratings yet

- Reading Material AccountantDocument123 pagesReading Material Accountantsatyanweshi truthseeker100% (1)

- Generally Accepted Accounting Principles (GAAP) and The Accounting EnvironmentDocument29 pagesGenerally Accepted Accounting Principles (GAAP) and The Accounting Environmentmehul100% (3)

- Chapter 2 Conceptual Framework of AccountingDocument21 pagesChapter 2 Conceptual Framework of AccountingBikas AdhikariNo ratings yet

- Foundation FA S1Document18 pagesFoundation FA S1narmadaNo ratings yet

- Chapter - 1: Introduction of Financial AccountingDocument21 pagesChapter - 1: Introduction of Financial AccountingMuhammad AdnanNo ratings yet

- Theory Base of AccountingDocument8 pagesTheory Base of Accountinggadhotiapankaj2No ratings yet

- CHAPTER 2 Accounting Theory Concept and Methodology of Accounting-CYHDocument38 pagesCHAPTER 2 Accounting Theory Concept and Methodology of Accounting-CYHgecemanullangNo ratings yet

- 1 Accounting IntroductionDocument16 pages1 Accounting Introductiontmskannan1967No ratings yet

- QBB Bookkeeping Essentials Action GuideDocument31 pagesQBB Bookkeeping Essentials Action GuidegeorgetacaprarescuNo ratings yet

- Basic Accounting For Non-AccountantsDocument34 pagesBasic Accounting For Non-AccountantsJohn Rey Bantay RodriguezNo ratings yet

- Chapter 2 The Accounting ProcessDocument12 pagesChapter 2 The Accounting ProcessFrakeZNo ratings yet

- AccountancyDocument9 pagesAccountancyBARSHANo ratings yet

- Introduction To AccountingDocument51 pagesIntroduction To Accountingmonkey bean100% (1)

- Introduction To Accounting: (Meaning and Objectives of Accounting and Accounting Information)Document14 pagesIntroduction To Accounting: (Meaning and Objectives of Accounting and Accounting Information)Tanishq NagoriNo ratings yet

- Chapter-5 Introduction To Accounting StandardsDocument9 pagesChapter-5 Introduction To Accounting Standardslenovo lenovoNo ratings yet

- Introductuion To AccountsDocument4 pagesIntroductuion To AccountsJoanne CrysantherNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Multiple Choice Test CS Type 123Document5 pagesMultiple Choice Test CS Type 123RiskaNo ratings yet

- Skripsi - Adm. Bisnis (Taat Sutriono - 0616051051)Document120 pagesSkripsi - Adm. Bisnis (Taat Sutriono - 0616051051)Latifah HanumNo ratings yet

- CISP Construction: Main MenuDocument13 pagesCISP Construction: Main MenuhvyvuyvNo ratings yet

- Org and Mgt. Q4LAS1Document22 pagesOrg and Mgt. Q4LAS1Jaslor LavinaNo ratings yet

- Delivery Challan: (Under Rule 55 of The CGST Rules, 2017)Document20 pagesDelivery Challan: (Under Rule 55 of The CGST Rules, 2017)SurajPandeyNo ratings yet

- Revised Confirmation of Johor Student Leader Council (JSLC)Document6 pagesRevised Confirmation of Johor Student Leader Council (JSLC)Shahmel IrfanNo ratings yet

- House Revit Model Size 80'-0 X 49'-0Document14 pagesHouse Revit Model Size 80'-0 X 49'-0Hanibal TesfamichaelNo ratings yet

- Linear Programming Linear ProgrammingDocument53 pagesLinear Programming Linear ProgrammingTisha SetiaNo ratings yet

- Blue Dot Engineering SDN BHD 669 Bawah Jalan Haruan 4/10 Oakland Industrial Park 70300 SerembanDocument1 pageBlue Dot Engineering SDN BHD 669 Bawah Jalan Haruan 4/10 Oakland Industrial Park 70300 SerembanCHAN MEE FERN MoeNo ratings yet

- A Tender File 2Document1 pageA Tender File 2sheila louiseNo ratings yet

- SALN 2023 SAMPLE For Additional FormatDocument4 pagesSALN 2023 SAMPLE For Additional Formatft84mddrhmNo ratings yet

- Competition Law: The Key Features: Sukesh Mishra Director (Law) Competition Commission of IndiaDocument48 pagesCompetition Law: The Key Features: Sukesh Mishra Director (Law) Competition Commission of IndiaAshhab KhanNo ratings yet

- Vit Hostels Vellore Campus: Hostel & Mess Fees For First Years StudentsDocument2 pagesVit Hostels Vellore Campus: Hostel & Mess Fees For First Years StudentsRajdeep ChaudhariNo ratings yet

- 4 BCG MatrixDocument3 pages4 BCG MatrixH Khoi NguyenNo ratings yet

- Social Media AssignmntDocument40 pagesSocial Media AssignmntNorlatifahNo ratings yet

- 1 ModelsDocument30 pages1 Modelssara alshNo ratings yet

- BA - Probability 2Document3 pagesBA - Probability 2AkshayNo ratings yet

- College of Leadership and Governance: School of Policy StudiesDocument8 pagesCollege of Leadership and Governance: School of Policy Studieskassahun meseleNo ratings yet

- ERD - Ecommerce DatabaseDocument1 pageERD - Ecommerce Databasefrank malleyNo ratings yet

- TOB-XFZH05 Vacuum Planetary MixerDocument9 pagesTOB-XFZH05 Vacuum Planetary Mixerdang thi ngoc ThuyNo ratings yet

- Ar TFC 22Document108 pagesAr TFC 22oetoerbNo ratings yet

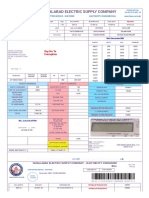

- Fesco Online BillDocument2 pagesFesco Online BillWaqar AkramNo ratings yet

- Maha Transco - CompressedDocument4 pagesMaha Transco - CompressedMaitri Auto Electrical East AfricaNo ratings yet

- Cavity Masonry Panel DesignDocument1 pageCavity Masonry Panel DesignAnonymous koR9VtfNo ratings yet

- AUD610 June2016Document9 pagesAUD610 June2016Nurfara ZakariaNo ratings yet

- Assignment 1 - Case Study Analysis: ECON1193B: Business Statistics 1Document7 pagesAssignment 1 - Case Study Analysis: ECON1193B: Business Statistics 1Phong LữNo ratings yet

- Extended Revision Exercises: Number: Worksheet 5: FractionsDocument3 pagesExtended Revision Exercises: Number: Worksheet 5: Fractionsmk hatNo ratings yet

- Solid Recovered Fuels - Specifications andDocument8 pagesSolid Recovered Fuels - Specifications andLaraCarralNo ratings yet

Download as pdf or txt

You might also like

- Financial Accounting Notes B.com 1st SemDocument64 pagesFinancial Accounting Notes B.com 1st SemJeevesh Roy0% (1)

- Singer Sewing Machine Model 1120Document38 pagesSinger Sewing Machine Model 1120bonehead6967% (6)

- Multiple Choice Questions 1 You Are Bidding in A Second PriceDocument2 pagesMultiple Choice Questions 1 You Are Bidding in A Second Pricetrilocksp SinghNo ratings yet

- Introduction To Financial AccountingDocument64 pagesIntroduction To Financial AccountingAnonymous HumanNo ratings yet

- Fundamentals of AccountingDocument18 pagesFundamentals of AccountingganeshvarmabattulaNo ratings yet

- CA FOUNDATION PAPER 1 ch1Document9 pagesCA FOUNDATION PAPER 1 ch1Saksham NaugaiNo ratings yet

- Part 1 - AccountingDocument12 pagesPart 1 - AccountingAmr YoussefNo ratings yet

- Syllabus: Subject - Financial AccountingDocument30 pagesSyllabus: Subject - Financial AccountingGaurav KhatriNo ratings yet

- Accounting Concepts and ConventionsDocument45 pagesAccounting Concepts and ConventionsPankaj SahaniNo ratings yet

- Basics of Accounting For MBA HRDocument19 pagesBasics of Accounting For MBA HRKundan JhaNo ratings yet

- 6-Principles and Concepts of Measuring IncomeDocument25 pages6-Principles and Concepts of Measuring Incomechobiipiggy26No ratings yet

- Chapter 1 Introduction To AccountingDocument35 pagesChapter 1 Introduction To AccountingdianeNo ratings yet

- BCOM 1 Financial Accounting 1Document63 pagesBCOM 1 Financial Accounting 1karthikeyan01No ratings yet

- Chapter 3A UnlockedDocument28 pagesChapter 3A UnlockedYashNo ratings yet

- Introduction To Accounting 2015-2016: Andreea PonorîcăDocument18 pagesIntroduction To Accounting 2015-2016: Andreea PonorîcăRaluca ToneNo ratings yet

- What Are The 3 Definition of Accounting?Document1 pageWhat Are The 3 Definition of Accounting?Sheila Grace BajaNo ratings yet

- BodyDocument15 pagesBodyRudrasish BeheraNo ratings yet

- Basics of Accounting - I: Financial Accounting / Isu Manufacturing Prithwiraj Sen SarmaDocument40 pagesBasics of Accounting - I: Financial Accounting / Isu Manufacturing Prithwiraj Sen Sarmakadir2613No ratings yet

- Amity Business School: MBA Class of 2011, Semester I Accounting For ManagementDocument27 pagesAmity Business School: MBA Class of 2011, Semester I Accounting For Managementkumaranil_1983No ratings yet

- Chapter 1 IntroductionDocument30 pagesChapter 1 IntroductionVivek GargNo ratings yet

- Lesson 1Document22 pagesLesson 1PoonamNo ratings yet

- المحاسبة باللغة الانجليزية ٤Document16 pagesالمحاسبة باللغة الانجليزية ٤wead888No ratings yet

- Financial Accounting-An Overview: Course ObjectiveDocument6 pagesFinancial Accounting-An Overview: Course ObjectiveJohn DoeNo ratings yet

- Syllabus: Subject - Financial AccountingDocument74 pagesSyllabus: Subject - Financial AccountingAnitha RNo ratings yet

- pptDocument66 pagespptNandini YadavNo ratings yet

- Accounting Concepts and Conventions 1Document48 pagesAccounting Concepts and Conventions 1Jatin PandayNo ratings yet

- Theory Base of Accounting, As and IFRSDocument39 pagesTheory Base of Accounting, As and IFRSYash Goyal0% (1)

- 2 Financial Accounting - Principles - GAAP 22102021 040821pmDocument10 pages2 Financial Accounting - Principles - GAAP 22102021 040821pmSomia aliNo ratings yet

- Paid CourseDocument278 pagesPaid CourseAkshay GajghateNo ratings yet

- Importance of Accounting: IdentifiesDocument20 pagesImportance of Accounting: IdentifiesNikhil GargNo ratings yet

- Advanced Financial Accounting I Lecture NoteDocument49 pagesAdvanced Financial Accounting I Lecture NoteBosz icon DyliteNo ratings yet

- Ch.13 Accounting StandardsDocument33 pagesCh.13 Accounting StandardsMalayaranjan PanigrahiNo ratings yet

- Accounting FOR ManagementDocument63 pagesAccounting FOR ManagementAnonymous 1ClGHbiT0JNo ratings yet

- Chapter-13 Preparation of Final Accounts of Sole Proprietors PDFDocument20 pagesChapter-13 Preparation of Final Accounts of Sole Proprietors PDFTarushi Yadav , 51BNo ratings yet

- Accountancy B.com Matterial (Final-2017)Document43 pagesAccountancy B.com Matterial (Final-2017)Bheeshm SinghNo ratings yet

- Icte 1033 ModsDocument4 pagesIcte 1033 ModsJoleen DoniegoNo ratings yet

- Confras First Sem LectureDocument52 pagesConfras First Sem LectureRosette SANTOSNo ratings yet

- Concepts: Introduction To Financial AccountingDocument30 pagesConcepts: Introduction To Financial Accountingbmurali37No ratings yet

- Accounting Principles: Accounting Concepts Accounting Conventions System of Book-Keeping System of AccountingDocument11 pagesAccounting Principles: Accounting Concepts Accounting Conventions System of Book-Keeping System of Accountingvinodgupta1960No ratings yet

- Financial Accounting CH1Document23 pagesFinancial Accounting CH1Kunal PradhanNo ratings yet

- Accounting 1 LectureDocument8 pagesAccounting 1 LecturePia louise RamosNo ratings yet

- Chapter Two: Accounting Concepts and PrinciplesDocument45 pagesChapter Two: Accounting Concepts and PrinciplesZerihunNo ratings yet

- Cfi Accounting EbookDocument66 pagesCfi Accounting Ebookmanjit13121990No ratings yet

- Cfi Accounting EbookDocument66 pagesCfi Accounting EbookAmjid MalNo ratings yet

- Reading Material AccountantDocument123 pagesReading Material Accountantsatyanweshi truthseeker100% (1)

- Generally Accepted Accounting Principles (GAAP) and The Accounting EnvironmentDocument29 pagesGenerally Accepted Accounting Principles (GAAP) and The Accounting Environmentmehul100% (3)

- Chapter 2 Conceptual Framework of AccountingDocument21 pagesChapter 2 Conceptual Framework of AccountingBikas AdhikariNo ratings yet

- Foundation FA S1Document18 pagesFoundation FA S1narmadaNo ratings yet

- Chapter - 1: Introduction of Financial AccountingDocument21 pagesChapter - 1: Introduction of Financial AccountingMuhammad AdnanNo ratings yet

- Theory Base of AccountingDocument8 pagesTheory Base of Accountinggadhotiapankaj2No ratings yet

- CHAPTER 2 Accounting Theory Concept and Methodology of Accounting-CYHDocument38 pagesCHAPTER 2 Accounting Theory Concept and Methodology of Accounting-CYHgecemanullangNo ratings yet

- 1 Accounting IntroductionDocument16 pages1 Accounting Introductiontmskannan1967No ratings yet

- QBB Bookkeeping Essentials Action GuideDocument31 pagesQBB Bookkeeping Essentials Action GuidegeorgetacaprarescuNo ratings yet

- Basic Accounting For Non-AccountantsDocument34 pagesBasic Accounting For Non-AccountantsJohn Rey Bantay RodriguezNo ratings yet

- Chapter 2 The Accounting ProcessDocument12 pagesChapter 2 The Accounting ProcessFrakeZNo ratings yet

- AccountancyDocument9 pagesAccountancyBARSHANo ratings yet

- Introduction To AccountingDocument51 pagesIntroduction To Accountingmonkey bean100% (1)

- Introduction To Accounting: (Meaning and Objectives of Accounting and Accounting Information)Document14 pagesIntroduction To Accounting: (Meaning and Objectives of Accounting and Accounting Information)Tanishq NagoriNo ratings yet

- Chapter-5 Introduction To Accounting StandardsDocument9 pagesChapter-5 Introduction To Accounting Standardslenovo lenovoNo ratings yet

- Introductuion To AccountsDocument4 pagesIntroductuion To AccountsJoanne CrysantherNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Multiple Choice Test CS Type 123Document5 pagesMultiple Choice Test CS Type 123RiskaNo ratings yet

- Skripsi - Adm. Bisnis (Taat Sutriono - 0616051051)Document120 pagesSkripsi - Adm. Bisnis (Taat Sutriono - 0616051051)Latifah HanumNo ratings yet

- CISP Construction: Main MenuDocument13 pagesCISP Construction: Main MenuhvyvuyvNo ratings yet

- Org and Mgt. Q4LAS1Document22 pagesOrg and Mgt. Q4LAS1Jaslor LavinaNo ratings yet

- Delivery Challan: (Under Rule 55 of The CGST Rules, 2017)Document20 pagesDelivery Challan: (Under Rule 55 of The CGST Rules, 2017)SurajPandeyNo ratings yet

- Revised Confirmation of Johor Student Leader Council (JSLC)Document6 pagesRevised Confirmation of Johor Student Leader Council (JSLC)Shahmel IrfanNo ratings yet

- House Revit Model Size 80'-0 X 49'-0Document14 pagesHouse Revit Model Size 80'-0 X 49'-0Hanibal TesfamichaelNo ratings yet

- Linear Programming Linear ProgrammingDocument53 pagesLinear Programming Linear ProgrammingTisha SetiaNo ratings yet

- Blue Dot Engineering SDN BHD 669 Bawah Jalan Haruan 4/10 Oakland Industrial Park 70300 SerembanDocument1 pageBlue Dot Engineering SDN BHD 669 Bawah Jalan Haruan 4/10 Oakland Industrial Park 70300 SerembanCHAN MEE FERN MoeNo ratings yet

- A Tender File 2Document1 pageA Tender File 2sheila louiseNo ratings yet

- SALN 2023 SAMPLE For Additional FormatDocument4 pagesSALN 2023 SAMPLE For Additional Formatft84mddrhmNo ratings yet

- Competition Law: The Key Features: Sukesh Mishra Director (Law) Competition Commission of IndiaDocument48 pagesCompetition Law: The Key Features: Sukesh Mishra Director (Law) Competition Commission of IndiaAshhab KhanNo ratings yet

- Vit Hostels Vellore Campus: Hostel & Mess Fees For First Years StudentsDocument2 pagesVit Hostels Vellore Campus: Hostel & Mess Fees For First Years StudentsRajdeep ChaudhariNo ratings yet

- 4 BCG MatrixDocument3 pages4 BCG MatrixH Khoi NguyenNo ratings yet

- Social Media AssignmntDocument40 pagesSocial Media AssignmntNorlatifahNo ratings yet

- 1 ModelsDocument30 pages1 Modelssara alshNo ratings yet

- BA - Probability 2Document3 pagesBA - Probability 2AkshayNo ratings yet

- College of Leadership and Governance: School of Policy StudiesDocument8 pagesCollege of Leadership and Governance: School of Policy Studieskassahun meseleNo ratings yet

- ERD - Ecommerce DatabaseDocument1 pageERD - Ecommerce Databasefrank malleyNo ratings yet

- TOB-XFZH05 Vacuum Planetary MixerDocument9 pagesTOB-XFZH05 Vacuum Planetary Mixerdang thi ngoc ThuyNo ratings yet

- Ar TFC 22Document108 pagesAr TFC 22oetoerbNo ratings yet

- Fesco Online BillDocument2 pagesFesco Online BillWaqar AkramNo ratings yet

- Maha Transco - CompressedDocument4 pagesMaha Transco - CompressedMaitri Auto Electrical East AfricaNo ratings yet

- Cavity Masonry Panel DesignDocument1 pageCavity Masonry Panel DesignAnonymous koR9VtfNo ratings yet

- AUD610 June2016Document9 pagesAUD610 June2016Nurfara ZakariaNo ratings yet

- Assignment 1 - Case Study Analysis: ECON1193B: Business Statistics 1Document7 pagesAssignment 1 - Case Study Analysis: ECON1193B: Business Statistics 1Phong LữNo ratings yet

- Extended Revision Exercises: Number: Worksheet 5: FractionsDocument3 pagesExtended Revision Exercises: Number: Worksheet 5: Fractionsmk hatNo ratings yet

- Solid Recovered Fuels - Specifications andDocument8 pagesSolid Recovered Fuels - Specifications andLaraCarralNo ratings yet