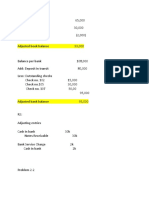

Exercises Bank Recon

Exercises Bank Recon

You might also like

- Problem 15-1 (AICPA Adapted) : Solution 15 - 1 Answer ADocument37 pagesProblem 15-1 (AICPA Adapted) : Solution 15 - 1 Answer AAldrin Lozano87% (15)

- 13 Lamaha Lease 2Document6 pages13 Lamaha Lease 2Elton Austin100% (2)

- Auditing Concept Problems Cash and Cash EquivalentDocument7 pagesAuditing Concept Problems Cash and Cash EquivalentJoanah TayamenNo ratings yet

- Dakota Office ProductssDocument17 pagesDakota Office ProductssSuzan Bakleh100% (5)

- Bank-Reconciliation IADocument10 pagesBank-Reconciliation IAAnaluz Cristine B. CeaNo ratings yet

- Activity 2Document3 pagesActivity 2kathie alegarmeNo ratings yet

- Bank Reconciliation: QuizDocument4 pagesBank Reconciliation: QuizBrgy Baloling50% (2)

- Visa Rules PublicDocument1,031 pagesVisa Rules PublicGabriel Alexandru LipanNo ratings yet

- CincinnatiDocument586 pagesCincinnatiJosephBAndradeIVNo ratings yet

- Bank Reconciliation - Sample ProblemDocument2 pagesBank Reconciliation - Sample ProblemKarl Wilson GonzalesNo ratings yet

- Bank ReconciliationDocument3 pagesBank ReconciliationjinyangsuelNo ratings yet

- Lecture No.2 Petty Cash Fund Bank Recon Lecture Problem SolvingDocument2 pagesLecture No.2 Petty Cash Fund Bank Recon Lecture Problem Solvingdelrosario.kenneth996No ratings yet

- Financial Accounting Second QuarterDocument4 pagesFinancial Accounting Second QuarterAnalisa Rañin BaculotNo ratings yet

- Bank Recon LectureDocument4 pagesBank Recon LectureChristopher Mau BambalanNo ratings yet

- Pak Enings HTDocument15 pagesPak Enings HTVincent SampianoNo ratings yet

- Cash N Cash Equivalent Problem Set 1Document3 pagesCash N Cash Equivalent Problem Set 1Jamaica DavidNo ratings yet

- Reviewer in Accounting - xlsx-3Document59 pagesReviewer in Accounting - xlsx-3Franchesca CortezNo ratings yet

- Proof of CashDocument2 pagesProof of CashRhea Mae CarantoNo ratings yet

- Exercises No1 CCash Equiv and Bank ReconDocument3 pagesExercises No1 CCash Equiv and Bank Recondelrosario.kenneth996No ratings yet

- 5 D35 J1 XIzyh 2 HN 4 C OI59 N PVLG ISz 8 e Re CG TOm UTGbm WHWD WYhthrce 0Document14 pages5 D35 J1 XIzyh 2 HN 4 C OI59 N PVLG ISz 8 e Re CG TOm UTGbm WHWD WYhthrce 0ramosmikay0222No ratings yet

- Assessment Task 1-1Document10 pagesAssessment Task 1-1hahahahaNo ratings yet

- Assignment 2 ACFAR 1231 Bank ReconciliationDocument3 pagesAssignment 2 ACFAR 1231 Bank ReconciliationkakaoNo ratings yet

- Bank ReconciliationDocument6 pagesBank Reconciliationnaih marchessaNo ratings yet

- Module 6 Part 2 Internal ControlDocument15 pagesModule 6 Part 2 Internal ControlKRISTINA CASSANDRA CUEVASNo ratings yet

- FINANCIAL ACCOUNTING - Cash To Receivables Problems and SolutionsDocument8 pagesFINANCIAL ACCOUNTING - Cash To Receivables Problems and Solutionsstan iKONNo ratings yet

- Quiz 1 - Audit of CashDocument4 pagesQuiz 1 - Audit of CashmillescaasiNo ratings yet

- AEC 115-Bank Reconciliation AssignmentDocument3 pagesAEC 115-Bank Reconciliation AssignmentJeyssa YermoNo ratings yet

- Control Account Tutorial Questions 2023-2024Document10 pagesControl Account Tutorial Questions 2023-2024nyimbilene23No ratings yet

- Bank ReconciliationDocument12 pagesBank ReconciliationJieniel ShanielNo ratings yet

- Bank Reconciliation IllustrationDocument2 pagesBank Reconciliation IllustrationRia BryleNo ratings yet

- ActivityDocument1 pageActivityUwuuUNo ratings yet

- Second Exam Msa1 ReviewerDocument4 pagesSecond Exam Msa1 ReviewerPaul Marben PolinarNo ratings yet

- Module 6 P2 Internal Control - BSA & BSMADocument14 pagesModule 6 P2 Internal Control - BSA & BSMAramosmikay0222No ratings yet

- Classroom Exercises On Receivables AnswersDocument4 pagesClassroom Exercises On Receivables AnswersJohn Cedfrey Narne100% (1)

- 4 5805514475188521061Document8 pages4 5805514475188521061Gena HamdaNo ratings yet

- Problem 57Document1 pageProblem 57YukidoNo ratings yet

- ACGA 504/ HCGA 507 General Accounting - Part 2Document17 pagesACGA 504/ HCGA 507 General Accounting - Part 2Eliza BethNo ratings yet

- FAR 0 Bank Recon and Proof of Cash Drill ProblemsDocument6 pagesFAR 0 Bank Recon and Proof of Cash Drill Problemsyeeaahh56No ratings yet

- Proof of Cash ProblemsDocument2 pagesProof of Cash ProblemsSamantha Marie Arevalo100% (1)

- Proof+of+Cash ProblemsDocument2 pagesProof+of+Cash ProblemshelaihjsNo ratings yet

- P01. Cash and Cash Equivalents AnswersDocument8 pagesP01. Cash and Cash Equivalents AnswersIosif DzhugasviliNo ratings yet

- Ga Problem SolvingDocument9 pagesGa Problem SolvinggarciarhodjeannemarthaNo ratings yet

- Bank Reconciliation: Basic ProblemsDocument25 pagesBank Reconciliation: Basic ProblemsAndrea FontiverosNo ratings yet

- Chapter 13-Cash ControlDocument25 pagesChapter 13-Cash ControlShaila MarceloNo ratings yet

- NOTES Practice Solving - Robles and EmpleoDocument52 pagesNOTES Practice Solving - Robles and EmpleoLeah La MadridNo ratings yet

- LESSON 3.2 - Bank ReconciliationDocument4 pagesLESSON 3.2 - Bank ReconciliationIshi MaxineNo ratings yet

- ACCTG 102 Practice Sets Quizzes ExamsDocument25 pagesACCTG 102 Practice Sets Quizzes ExamsheythereitsclaireNo ratings yet

- And POCDocument3 pagesAnd POCjudeaharmony.wamildaNo ratings yet

- Bank ReconciliationDocument6 pagesBank Reconciliationclarisse jaramillaNo ratings yet

- Chapter 2 Last PartDocument11 pagesChapter 2 Last PartXENA LOPEZ100% (2)

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- Bank Reconciliation - SolutionsDocument6 pagesBank Reconciliation - SolutionsNIAZ HUSSAIN100% (1)

- Cash Cash Equivalent Bank ReconDocument4 pagesCash Cash Equivalent Bank Reconmavie arellanoNo ratings yet

- Take Home Exam 1 Cash and Cash EquivalentsDocument2 pagesTake Home Exam 1 Cash and Cash EquivalentsJi Eun VinceNo ratings yet

- AUD02 - 05 Audit of Cash and Cash EquivalentsDocument3 pagesAUD02 - 05 Audit of Cash and Cash EquivalentsMark BajacanNo ratings yet

- Control Account QuestionsDocument6 pagesControl Account QuestionsJaneth Patrick100% (2)

- ACCT 315 AssignmentDocument11 pagesACCT 315 AssignmenthumaNo ratings yet

- Makeup Test Reviewer PDFDocument43 pagesMakeup Test Reviewer PDFandrea arapocNo ratings yet

- Timing Difference: Check Payment (Receivable) But Not Yet Deposited by PayeeDocument6 pagesTiming Difference: Check Payment (Receivable) But Not Yet Deposited by PayeeannyeongNo ratings yet

- UntitledDocument5 pagesUntitledShevina Maghari shsnohsNo ratings yet

- MC - Bank Reconciliation and Proof of CashDocument4 pagesMC - Bank Reconciliation and Proof of CashGwen Ashley Dela PenaNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsFrancine Thea M. Lantaya100% (1)

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- Concentrating Solar Power in Developing Countries: Regulatory and Financial Incentives for Scaling UpFrom EverandConcentrating Solar Power in Developing Countries: Regulatory and Financial Incentives for Scaling UpNo ratings yet

- List of Scheduled Commercial Banks: (Refer To para 2 (B) of Notification Dated October 08, 2018)Document2 pagesList of Scheduled Commercial Banks: (Refer To para 2 (B) of Notification Dated October 08, 2018)Vikram PhalakNo ratings yet

- NFJPIA Mockboard 2011 P1Document7 pagesNFJPIA Mockboard 2011 P1jhefster_81No ratings yet

- Activity 1 - Audit of Receivables and RevenuesDocument2 pagesActivity 1 - Audit of Receivables and RevenuesColeen Joy Sebastian PagalingNo ratings yet

- Increase Credit Limit PDFDocument1 pageIncrease Credit Limit PDFemc2_mcvNo ratings yet

- S.No Student'S Name A/C Holder Name A/C Number Ifsc Code Bank Name RemittanceDocument8 pagesS.No Student'S Name A/C Holder Name A/C Number Ifsc Code Bank Name Remittancejyoti kumariNo ratings yet

- CH 2 - The Philippine Financial SystemDocument14 pagesCH 2 - The Philippine Financial SystemjsmnfrncscNo ratings yet

- Top Ten Largest Commercial Banks in The Philippines (Jellynfile)Document21 pagesTop Ten Largest Commercial Banks in The Philippines (Jellynfile)Ralph Evander IdulNo ratings yet

- FIN 401 Final Report BodyDocument9 pagesFIN 401 Final Report Body1711........100% (1)

- Project ReportDocument25 pagesProject ReportAarshiya Mina SheelNo ratings yet

- BPI Family Bank V FrancoDocument1 pageBPI Family Bank V FrancojoyceNo ratings yet

- Study of E-Banking Scenario in India: Shubhara JindalDocument4 pagesStudy of E-Banking Scenario in India: Shubhara JindalSahul RanaNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsnikkitaaaNo ratings yet

- Principles of Insurance (1) Total SlidesDocument147 pagesPrinciples of Insurance (1) Total SlidesdaohoaflowerNo ratings yet

- Customer Bank AccountDocument872 pagesCustomer Bank AccountNaresh KumarNo ratings yet

- Itc14 mcp23Document8 pagesItc14 mcp23Lee TeukNo ratings yet

- Coding and Decoding QuestionsDocument28 pagesCoding and Decoding QuestionsAbdulawwal IntisorNo ratings yet

- Annual Report 2007Document20 pagesAnnual Report 2007SolidariteInternationale100% (2)

- Sbi ProjectDocument60 pagesSbi Projectjithu100% (3)

- CertanceDocument22 pagesCertanceZechen MaNo ratings yet

- New Supplier E-Payment FormDocument2 pagesNew Supplier E-Payment FormTareeke ThompsonNo ratings yet

- MM12 - Forex Scandal - WikipediaDocument3 pagesMM12 - Forex Scandal - WikipediaAtul SharmaNo ratings yet

- Statutory Audit ChecklistDocument6 pagesStatutory Audit ChecklistCA SwaroopNo ratings yet

- Basic Accounting Promissory NotesDocument12 pagesBasic Accounting Promissory NotesJean Lewis RossNo ratings yet

- History of PNBDocument2 pagesHistory of PNBAlliah SomidoNo ratings yet

- Bank Reconciliation Assignment 2Document8 pagesBank Reconciliation Assignment 2Caira De AsisNo ratings yet

- Common Law Power of Attorney FormDocument25 pagesCommon Law Power of Attorney Formwhitecliff1100% (3)

Download as pdf or txt

You might also like

- Problem 15-1 (AICPA Adapted) : Solution 15 - 1 Answer ADocument37 pagesProblem 15-1 (AICPA Adapted) : Solution 15 - 1 Answer AAldrin Lozano87% (15)

- 13 Lamaha Lease 2Document6 pages13 Lamaha Lease 2Elton Austin100% (2)

- Auditing Concept Problems Cash and Cash EquivalentDocument7 pagesAuditing Concept Problems Cash and Cash EquivalentJoanah TayamenNo ratings yet

- Dakota Office ProductssDocument17 pagesDakota Office ProductssSuzan Bakleh100% (5)

- Bank-Reconciliation IADocument10 pagesBank-Reconciliation IAAnaluz Cristine B. CeaNo ratings yet

- Activity 2Document3 pagesActivity 2kathie alegarmeNo ratings yet

- Bank Reconciliation: QuizDocument4 pagesBank Reconciliation: QuizBrgy Baloling50% (2)

- Visa Rules PublicDocument1,031 pagesVisa Rules PublicGabriel Alexandru LipanNo ratings yet

- CincinnatiDocument586 pagesCincinnatiJosephBAndradeIVNo ratings yet

- Bank Reconciliation - Sample ProblemDocument2 pagesBank Reconciliation - Sample ProblemKarl Wilson GonzalesNo ratings yet

- Bank ReconciliationDocument3 pagesBank ReconciliationjinyangsuelNo ratings yet

- Lecture No.2 Petty Cash Fund Bank Recon Lecture Problem SolvingDocument2 pagesLecture No.2 Petty Cash Fund Bank Recon Lecture Problem Solvingdelrosario.kenneth996No ratings yet

- Financial Accounting Second QuarterDocument4 pagesFinancial Accounting Second QuarterAnalisa Rañin BaculotNo ratings yet

- Bank Recon LectureDocument4 pagesBank Recon LectureChristopher Mau BambalanNo ratings yet

- Pak Enings HTDocument15 pagesPak Enings HTVincent SampianoNo ratings yet

- Cash N Cash Equivalent Problem Set 1Document3 pagesCash N Cash Equivalent Problem Set 1Jamaica DavidNo ratings yet

- Reviewer in Accounting - xlsx-3Document59 pagesReviewer in Accounting - xlsx-3Franchesca CortezNo ratings yet

- Proof of CashDocument2 pagesProof of CashRhea Mae CarantoNo ratings yet

- Exercises No1 CCash Equiv and Bank ReconDocument3 pagesExercises No1 CCash Equiv and Bank Recondelrosario.kenneth996No ratings yet

- 5 D35 J1 XIzyh 2 HN 4 C OI59 N PVLG ISz 8 e Re CG TOm UTGbm WHWD WYhthrce 0Document14 pages5 D35 J1 XIzyh 2 HN 4 C OI59 N PVLG ISz 8 e Re CG TOm UTGbm WHWD WYhthrce 0ramosmikay0222No ratings yet

- Assessment Task 1-1Document10 pagesAssessment Task 1-1hahahahaNo ratings yet

- Assignment 2 ACFAR 1231 Bank ReconciliationDocument3 pagesAssignment 2 ACFAR 1231 Bank ReconciliationkakaoNo ratings yet

- Bank ReconciliationDocument6 pagesBank Reconciliationnaih marchessaNo ratings yet

- Module 6 Part 2 Internal ControlDocument15 pagesModule 6 Part 2 Internal ControlKRISTINA CASSANDRA CUEVASNo ratings yet

- FINANCIAL ACCOUNTING - Cash To Receivables Problems and SolutionsDocument8 pagesFINANCIAL ACCOUNTING - Cash To Receivables Problems and Solutionsstan iKONNo ratings yet

- Quiz 1 - Audit of CashDocument4 pagesQuiz 1 - Audit of CashmillescaasiNo ratings yet

- AEC 115-Bank Reconciliation AssignmentDocument3 pagesAEC 115-Bank Reconciliation AssignmentJeyssa YermoNo ratings yet

- Control Account Tutorial Questions 2023-2024Document10 pagesControl Account Tutorial Questions 2023-2024nyimbilene23No ratings yet

- Bank ReconciliationDocument12 pagesBank ReconciliationJieniel ShanielNo ratings yet

- Bank Reconciliation IllustrationDocument2 pagesBank Reconciliation IllustrationRia BryleNo ratings yet

- ActivityDocument1 pageActivityUwuuUNo ratings yet

- Second Exam Msa1 ReviewerDocument4 pagesSecond Exam Msa1 ReviewerPaul Marben PolinarNo ratings yet

- Module 6 P2 Internal Control - BSA & BSMADocument14 pagesModule 6 P2 Internal Control - BSA & BSMAramosmikay0222No ratings yet

- Classroom Exercises On Receivables AnswersDocument4 pagesClassroom Exercises On Receivables AnswersJohn Cedfrey Narne100% (1)

- 4 5805514475188521061Document8 pages4 5805514475188521061Gena HamdaNo ratings yet

- Problem 57Document1 pageProblem 57YukidoNo ratings yet

- ACGA 504/ HCGA 507 General Accounting - Part 2Document17 pagesACGA 504/ HCGA 507 General Accounting - Part 2Eliza BethNo ratings yet

- FAR 0 Bank Recon and Proof of Cash Drill ProblemsDocument6 pagesFAR 0 Bank Recon and Proof of Cash Drill Problemsyeeaahh56No ratings yet

- Proof of Cash ProblemsDocument2 pagesProof of Cash ProblemsSamantha Marie Arevalo100% (1)

- Proof+of+Cash ProblemsDocument2 pagesProof+of+Cash ProblemshelaihjsNo ratings yet

- P01. Cash and Cash Equivalents AnswersDocument8 pagesP01. Cash and Cash Equivalents AnswersIosif DzhugasviliNo ratings yet

- Ga Problem SolvingDocument9 pagesGa Problem SolvinggarciarhodjeannemarthaNo ratings yet

- Bank Reconciliation: Basic ProblemsDocument25 pagesBank Reconciliation: Basic ProblemsAndrea FontiverosNo ratings yet

- Chapter 13-Cash ControlDocument25 pagesChapter 13-Cash ControlShaila MarceloNo ratings yet

- NOTES Practice Solving - Robles and EmpleoDocument52 pagesNOTES Practice Solving - Robles and EmpleoLeah La MadridNo ratings yet

- LESSON 3.2 - Bank ReconciliationDocument4 pagesLESSON 3.2 - Bank ReconciliationIshi MaxineNo ratings yet

- ACCTG 102 Practice Sets Quizzes ExamsDocument25 pagesACCTG 102 Practice Sets Quizzes ExamsheythereitsclaireNo ratings yet

- And POCDocument3 pagesAnd POCjudeaharmony.wamildaNo ratings yet

- Bank ReconciliationDocument6 pagesBank Reconciliationclarisse jaramillaNo ratings yet

- Chapter 2 Last PartDocument11 pagesChapter 2 Last PartXENA LOPEZ100% (2)

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- Bank Reconciliation - SolutionsDocument6 pagesBank Reconciliation - SolutionsNIAZ HUSSAIN100% (1)

- Cash Cash Equivalent Bank ReconDocument4 pagesCash Cash Equivalent Bank Reconmavie arellanoNo ratings yet

- Take Home Exam 1 Cash and Cash EquivalentsDocument2 pagesTake Home Exam 1 Cash and Cash EquivalentsJi Eun VinceNo ratings yet

- AUD02 - 05 Audit of Cash and Cash EquivalentsDocument3 pagesAUD02 - 05 Audit of Cash and Cash EquivalentsMark BajacanNo ratings yet

- Control Account QuestionsDocument6 pagesControl Account QuestionsJaneth Patrick100% (2)

- ACCT 315 AssignmentDocument11 pagesACCT 315 AssignmenthumaNo ratings yet

- Makeup Test Reviewer PDFDocument43 pagesMakeup Test Reviewer PDFandrea arapocNo ratings yet

- Timing Difference: Check Payment (Receivable) But Not Yet Deposited by PayeeDocument6 pagesTiming Difference: Check Payment (Receivable) But Not Yet Deposited by PayeeannyeongNo ratings yet

- UntitledDocument5 pagesUntitledShevina Maghari shsnohsNo ratings yet

- MC - Bank Reconciliation and Proof of CashDocument4 pagesMC - Bank Reconciliation and Proof of CashGwen Ashley Dela PenaNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsFrancine Thea M. Lantaya100% (1)

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- Concentrating Solar Power in Developing Countries: Regulatory and Financial Incentives for Scaling UpFrom EverandConcentrating Solar Power in Developing Countries: Regulatory and Financial Incentives for Scaling UpNo ratings yet

- List of Scheduled Commercial Banks: (Refer To para 2 (B) of Notification Dated October 08, 2018)Document2 pagesList of Scheduled Commercial Banks: (Refer To para 2 (B) of Notification Dated October 08, 2018)Vikram PhalakNo ratings yet

- NFJPIA Mockboard 2011 P1Document7 pagesNFJPIA Mockboard 2011 P1jhefster_81No ratings yet

- Activity 1 - Audit of Receivables and RevenuesDocument2 pagesActivity 1 - Audit of Receivables and RevenuesColeen Joy Sebastian PagalingNo ratings yet

- Increase Credit Limit PDFDocument1 pageIncrease Credit Limit PDFemc2_mcvNo ratings yet

- S.No Student'S Name A/C Holder Name A/C Number Ifsc Code Bank Name RemittanceDocument8 pagesS.No Student'S Name A/C Holder Name A/C Number Ifsc Code Bank Name Remittancejyoti kumariNo ratings yet

- CH 2 - The Philippine Financial SystemDocument14 pagesCH 2 - The Philippine Financial SystemjsmnfrncscNo ratings yet

- Top Ten Largest Commercial Banks in The Philippines (Jellynfile)Document21 pagesTop Ten Largest Commercial Banks in The Philippines (Jellynfile)Ralph Evander IdulNo ratings yet

- FIN 401 Final Report BodyDocument9 pagesFIN 401 Final Report Body1711........100% (1)

- Project ReportDocument25 pagesProject ReportAarshiya Mina SheelNo ratings yet

- BPI Family Bank V FrancoDocument1 pageBPI Family Bank V FrancojoyceNo ratings yet

- Study of E-Banking Scenario in India: Shubhara JindalDocument4 pagesStudy of E-Banking Scenario in India: Shubhara JindalSahul RanaNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsnikkitaaaNo ratings yet

- Principles of Insurance (1) Total SlidesDocument147 pagesPrinciples of Insurance (1) Total SlidesdaohoaflowerNo ratings yet

- Customer Bank AccountDocument872 pagesCustomer Bank AccountNaresh KumarNo ratings yet

- Itc14 mcp23Document8 pagesItc14 mcp23Lee TeukNo ratings yet

- Coding and Decoding QuestionsDocument28 pagesCoding and Decoding QuestionsAbdulawwal IntisorNo ratings yet

- Annual Report 2007Document20 pagesAnnual Report 2007SolidariteInternationale100% (2)

- Sbi ProjectDocument60 pagesSbi Projectjithu100% (3)

- CertanceDocument22 pagesCertanceZechen MaNo ratings yet

- New Supplier E-Payment FormDocument2 pagesNew Supplier E-Payment FormTareeke ThompsonNo ratings yet

- MM12 - Forex Scandal - WikipediaDocument3 pagesMM12 - Forex Scandal - WikipediaAtul SharmaNo ratings yet

- Statutory Audit ChecklistDocument6 pagesStatutory Audit ChecklistCA SwaroopNo ratings yet

- Basic Accounting Promissory NotesDocument12 pagesBasic Accounting Promissory NotesJean Lewis RossNo ratings yet

- History of PNBDocument2 pagesHistory of PNBAlliah SomidoNo ratings yet

- Bank Reconciliation Assignment 2Document8 pagesBank Reconciliation Assignment 2Caira De AsisNo ratings yet

- Common Law Power of Attorney FormDocument25 pagesCommon Law Power of Attorney Formwhitecliff1100% (3)