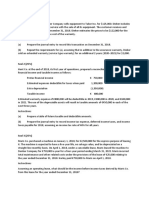

Case Rewiev #1 Cyf

Case Rewiev #1 Cyf

You might also like

- Tax Questions & SolutionsDocument126 pagesTax Questions & SolutionsTawanda Tatenda Herbert100% (8)

- International TaxationDocument8 pagesInternational TaxationkinslinNo ratings yet

- Abi Premium 1Document1 pageAbi Premium 1manikandan BalasubramaniyanNo ratings yet

- Fake PaystubDocument1 pageFake PaystubBrandon CarpenterNo ratings yet

- Ammar Yasir - 041911333245 - Tugas AKM III WEEK 8Document7 pagesAmmar Yasir - 041911333245 - Tugas AKM III WEEK 8sari ayuNo ratings yet

- MODULE 3 - Installment SalesDocument8 pagesMODULE 3 - Installment SalesEdison Salgado Castigador50% (2)

- Chapter 49-Pfrs For SmesDocument6 pagesChapter 49-Pfrs For SmesEmma Mariz Garcia40% (5)

- Tax Accounting Set ADocument4 pagesTax Accounting Set AGopti EmmanuelNo ratings yet

- FAR Vol 2 Chapter 16 18Document14 pagesFAR Vol 2 Chapter 16 18Allen Fey De Jesus100% (1)

- Deferred Income Tax Asset and LiabilityDocument4 pagesDeferred Income Tax Asset and Liabilityalcazar rtuNo ratings yet

- Tut TaxDocument6 pagesTut TaxKieu Anh Bui LeNo ratings yet

- CHAPTER 10. Corporation TaxDocument55 pagesCHAPTER 10. Corporation TaxAmanda RuseirNo ratings yet

- Tutorial 6 - 2024Document4 pagesTutorial 6 - 2024Giang Dương HươngNo ratings yet

- Test Contabil - SavvyDocument3 pagesTest Contabil - SavvyBogdan NiculaNo ratings yet

- Intermediate Accounting II Assignment Session 7Document2 pagesIntermediate Accounting II Assignment Session 7izza zahratunnisaNo ratings yet

- Accounting For Income TaxDocument4 pagesAccounting For Income TaxShaira Bugayong0% (2)

- Acc 3013 - Fwa Revision QuestionsDocument12 pagesAcc 3013 - Fwa Revision Questionsfalnuaimi001No ratings yet

- Accounting For Income Tax ExamDocument6 pagesAccounting For Income Tax ExamAnn Christine C. Chua100% (2)

- Assignments 9.1 and 9.2Document2 pagesAssignments 9.1 and 9.2carmen.magarinosbNo ratings yet

- Accounting For Taxes 6Document7 pagesAccounting For Taxes 6charlene kate bunaoNo ratings yet

- AUD02 - A - 04 Misstatement in The Financial StatementsDocument2 pagesAUD02 - A - 04 Misstatement in The Financial StatementsMark BajacanNo ratings yet

- SOAL Kuis Materi UAS Inter 2Document2 pagesSOAL Kuis Materi UAS Inter 2vania 322019087No ratings yet

- SOAL Kuis Materi UAS Inter 2Document2 pagesSOAL Kuis Materi UAS Inter 2vania 322019087No ratings yet

- Principles of Taxation ND2020Document2 pagesPrinciples of Taxation ND2020Sharif MahmudNo ratings yet

- Lecture 3Document57 pagesLecture 3Hoàng NhiNo ratings yet

- Accounting For Income TaxesDocument12 pagesAccounting For Income TaxesRMG Career Society BDNo ratings yet

- 29 Ke-toan-quoc-te-2 201109 Đề-01 Cky3 CLC 13h30 10.09.2021-2Document10 pages29 Ke-toan-quoc-te-2 201109 Đề-01 Cky3 CLC 13h30 10.09.2021-2uthanh2209No ratings yet

- Covid 19 Levy 04 Jan 2021Document30 pagesCovid 19 Levy 04 Jan 2021musicals.muNo ratings yet

- 5.09 Analysis of Income TaxesDocument10 pages5.09 Analysis of Income TaxesClaptrapjackNo ratings yet

- KẾ TOÁN QUỐC TẾ 1 - TEST GIỮA KỲDocument41 pagesKẾ TOÁN QUỐC TẾ 1 - TEST GIỮA KỲLINH PHAN THINo ratings yet

- ACCO1115 - 2021 - JULY - EXAM - OnlineDocument11 pagesACCO1115 - 2021 - JULY - EXAM - OnlineSarah RanduNo ratings yet

- ABC Co LTD - Case Study Test - RevisedDocument2 pagesABC Co LTD - Case Study Test - Revisedroman marian89No ratings yet

- Bài tập chủ đề 6Document7 pagesBài tập chủ đề 6thanhtrucNo ratings yet

- BACC 2206- Intermediate Accounting II _ Assignment Jan - April 2023Document3 pagesBACC 2206- Intermediate Accounting II _ Assignment Jan - April 2023jacintavike42No ratings yet

- VAT Other Aspects - January 2024Document5 pagesVAT Other Aspects - January 2024Charisma CharlesNo ratings yet

- Quizzz Intac 3Document10 pagesQuizzz Intac 3lana del reyNo ratings yet

- AP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document4 pagesAP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Kate PaquizNo ratings yet

- 3.2 Business Profit TaxDocument53 pages3.2 Business Profit TaxBizu AtnafuNo ratings yet

- Answer Key - Income Tax Peer Tutoring Quiz (Chapter 4)Document4 pagesAnswer Key - Income Tax Peer Tutoring Quiz (Chapter 4)Jahz Aira GamboaNo ratings yet

- Audit of Liabilities Quiz 3Document3 pagesAudit of Liabilities Quiz 3Cattleya50% (2)

- Ey Ireland Early Payment of 2020 Excess Randd Tax CreditsDocument5 pagesEy Ireland Early Payment of 2020 Excess Randd Tax CreditsharryNo ratings yet

- W5 - AS2 - Deferred TaxesDocument2 pagesW5 - AS2 - Deferred TaxesJere Mae MarananNo ratings yet

- F00540010220143001Homework Chapter 19 and 21Document2 pagesF00540010220143001Homework Chapter 19 and 21Nur Hidayah K FNo ratings yet

- Ac5007 QuestionsDocument8 pagesAc5007 QuestionsyinlengNo ratings yet

- AccountingDocument6 pagesAccountingBlue HourNo ratings yet

- 4 - CIT - TI ReductionsDocument13 pages4 - CIT - TI ReductionsMaricarmen SilvaNo ratings yet

- FA2-08 Income TaxesDocument3 pagesFA2-08 Income Taxeskrisha millo0% (1)

- Tax Planning and Compliance: Page 1 of 5Document5 pagesTax Planning and Compliance: Page 1 of 5Srikrishna DharNo ratings yet

- TAX PLANNING & COMPLIANCE - MA-2022 - QuestionDocument6 pagesTAX PLANNING & COMPLIANCE - MA-2022 - QuestionsajedulNo ratings yet

- Income Tax - ExercisesDocument2 pagesIncome Tax - ExercisesEnges FormulaNo ratings yet

- Chapter 22 Deferred Tax Asset and LiabilityDocument8 pagesChapter 22 Deferred Tax Asset and LiabilityCheesca Macabanti - 12 Euclid-Digital ModularNo ratings yet

- Revision 1-9 MCDocument5 pagesRevision 1-9 MCdilinhtinh04No ratings yet

- Assumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceDocument4 pagesAssumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceAireyNo ratings yet

- W4 TaxesDocument35 pagesW4 TaxesVanessa LeeNo ratings yet

- 20th Regional Mid Year Convention Cup 6 Easy RoundDocument18 pages20th Regional Mid Year Convention Cup 6 Easy RoundSophia De GuzmanNo ratings yet

- Financial Accounting 3.1Document6 pagesFinancial Accounting 3.1Tawanda HerbertNo ratings yet

- Kế Toán Quốc Tế: Select oneDocument8 pagesKế Toán Quốc Tế: Select oneLoki Luke100% (1)

- Income Taxes - Question BookDocument27 pagesIncome Taxes - Question Bookandiswa zuluNo ratings yet

- Additional Question 1Document1 pageAdditional Question 1Nurul AinaNo ratings yet

- Final Examn Dec 2022 CF2 ALLDocument7 pagesFinal Examn Dec 2022 CF2 ALLleyrepavonNo ratings yet

- 17 CPA ADVANCED TAXATION Paper 17Document9 pages17 CPA ADVANCED TAXATION Paper 17kabendejunior4No ratings yet

- Taxtest 1Document5 pagesTaxtest 1alaaomarmazharmohamedNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Tax2 Bar Q - A (2007-2016) (LSG1718)Document46 pagesTax2 Bar Q - A (2007-2016) (LSG1718)Naethan Jhoe L. CiprianoNo ratings yet

- Kanya KarungalDocument13 pagesKanya KarungalramNo ratings yet

- ReSA Batch 47 ScheduleDocument1 pageReSA Batch 47 ScheduleyshizamNo ratings yet

- Financial Accounting Solution ch14Document23 pagesFinancial Accounting Solution ch14hw cNo ratings yet

- ACCCOB1 Quiz 1 Monday Set A Answer Key PDFDocument4 pagesACCCOB1 Quiz 1 Monday Set A Answer Key PDFfanchasticommsNo ratings yet

- Valix 17 20 MCQ and Theory Emp Ben She PDFDocument48 pagesValix 17 20 MCQ and Theory Emp Ben She PDFMitchie FaustinoNo ratings yet

- Semester Teaching Plan 2021-2022 Semester 1: Subject Code and Title Course Convenor Course InstructorsDocument5 pagesSemester Teaching Plan 2021-2022 Semester 1: Subject Code and Title Course Convenor Course InstructorsDimitriNo ratings yet

- SudhaDocument7 pagesSudhaSneha AgrawalNo ratings yet

- Problem 5Document3 pagesProblem 5Rudy LugasNo ratings yet

- CHAPTER 13 B - Special Allowable Itemized Deductions and NOLCODocument2 pagesCHAPTER 13 B - Special Allowable Itemized Deductions and NOLCODeviane CalabriaNo ratings yet

- Research Paper On Cash Flow ManagementDocument4 pagesResearch Paper On Cash Flow Managementihprzlbkf100% (1)

- New Jersey Complete Business Registration PacketDocument47 pagesNew Jersey Complete Business Registration PacketWen' George BeyNo ratings yet

- COMM1140 - 2021T1 - Week 1 Lecture Slides - Master Deck From Live LectureDocument43 pagesCOMM1140 - 2021T1 - Week 1 Lecture Slides - Master Deck From Live LectureLia LeNo ratings yet

- Sample Final Exam Questions W19 March 31 With Answers - Leverage DividendsDocument3 pagesSample Final Exam Questions W19 March 31 With Answers - Leverage Dividendsbusiness docNo ratings yet

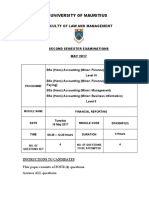

- University of Mauritius: Faculty of Law and ManagementDocument9 pagesUniversity of Mauritius: Faculty of Law and ManagementMîñåk ŞhïïNo ratings yet

- Module No 4 - Capital Gains TaxDocument8 pagesModule No 4 - Capital Gains TaxBetty SantiagoNo ratings yet

- Financial Statements and Ratio AnalysisDocument9 pagesFinancial Statements and Ratio AnalysisRabie HarounNo ratings yet

- Section 10 of The Income Tax ActDocument10 pagesSection 10 of The Income Tax ActVANSHIKA SINGHNo ratings yet

- 06 Financial Statement Preparation, Closing Entries, and Reversing EntriesDocument18 pages06 Financial Statement Preparation, Closing Entries, and Reversing Entriescarlo bundalianNo ratings yet

- Financial Management: Roll No. Total No. of Pages: 02 Total No. of Questions: 08 BBA (Sem.-4)Document2 pagesFinancial Management: Roll No. Total No. of Pages: 02 Total No. of Questions: 08 BBA (Sem.-4)Shlok MittalNo ratings yet

- Ratio AnalysisDocument36 pagesRatio Analysisjigar ramNo ratings yet

- Wage and Tax Statement: OMB No. 1545-0008Document4 pagesWage and Tax Statement: OMB No. 1545-0008jgoldson235No ratings yet

- Relative ValuationDocument26 pagesRelative ValuationRAKESH SINGHNo ratings yet

- Sekai 05Document2 pagesSekai 05Micaela EncinasNo ratings yet

- Chapter 2911Document19 pagesChapter 2911Madhu kumarNo ratings yet

- Domondon Taxation 2022 Bar Bulletin No. 31 S. 2022Document210 pagesDomondon Taxation 2022 Bar Bulletin No. 31 S. 2022Cedric Comon100% (1)

- Unit 4 - DPSPS, RRSPs and TFSAsDocument61 pagesUnit 4 - DPSPS, RRSPs and TFSAsMITALI SWADIYANo ratings yet

Download as pdf or txt

You might also like

- Tax Questions & SolutionsDocument126 pagesTax Questions & SolutionsTawanda Tatenda Herbert100% (8)

- International TaxationDocument8 pagesInternational TaxationkinslinNo ratings yet

- Abi Premium 1Document1 pageAbi Premium 1manikandan BalasubramaniyanNo ratings yet

- Fake PaystubDocument1 pageFake PaystubBrandon CarpenterNo ratings yet

- Ammar Yasir - 041911333245 - Tugas AKM III WEEK 8Document7 pagesAmmar Yasir - 041911333245 - Tugas AKM III WEEK 8sari ayuNo ratings yet

- MODULE 3 - Installment SalesDocument8 pagesMODULE 3 - Installment SalesEdison Salgado Castigador50% (2)

- Chapter 49-Pfrs For SmesDocument6 pagesChapter 49-Pfrs For SmesEmma Mariz Garcia40% (5)

- Tax Accounting Set ADocument4 pagesTax Accounting Set AGopti EmmanuelNo ratings yet

- FAR Vol 2 Chapter 16 18Document14 pagesFAR Vol 2 Chapter 16 18Allen Fey De Jesus100% (1)

- Deferred Income Tax Asset and LiabilityDocument4 pagesDeferred Income Tax Asset and Liabilityalcazar rtuNo ratings yet

- Tut TaxDocument6 pagesTut TaxKieu Anh Bui LeNo ratings yet

- CHAPTER 10. Corporation TaxDocument55 pagesCHAPTER 10. Corporation TaxAmanda RuseirNo ratings yet

- Tutorial 6 - 2024Document4 pagesTutorial 6 - 2024Giang Dương HươngNo ratings yet

- Test Contabil - SavvyDocument3 pagesTest Contabil - SavvyBogdan NiculaNo ratings yet

- Intermediate Accounting II Assignment Session 7Document2 pagesIntermediate Accounting II Assignment Session 7izza zahratunnisaNo ratings yet

- Accounting For Income TaxDocument4 pagesAccounting For Income TaxShaira Bugayong0% (2)

- Acc 3013 - Fwa Revision QuestionsDocument12 pagesAcc 3013 - Fwa Revision Questionsfalnuaimi001No ratings yet

- Accounting For Income Tax ExamDocument6 pagesAccounting For Income Tax ExamAnn Christine C. Chua100% (2)

- Assignments 9.1 and 9.2Document2 pagesAssignments 9.1 and 9.2carmen.magarinosbNo ratings yet

- Accounting For Taxes 6Document7 pagesAccounting For Taxes 6charlene kate bunaoNo ratings yet

- AUD02 - A - 04 Misstatement in The Financial StatementsDocument2 pagesAUD02 - A - 04 Misstatement in The Financial StatementsMark BajacanNo ratings yet

- SOAL Kuis Materi UAS Inter 2Document2 pagesSOAL Kuis Materi UAS Inter 2vania 322019087No ratings yet

- SOAL Kuis Materi UAS Inter 2Document2 pagesSOAL Kuis Materi UAS Inter 2vania 322019087No ratings yet

- Principles of Taxation ND2020Document2 pagesPrinciples of Taxation ND2020Sharif MahmudNo ratings yet

- Lecture 3Document57 pagesLecture 3Hoàng NhiNo ratings yet

- Accounting For Income TaxesDocument12 pagesAccounting For Income TaxesRMG Career Society BDNo ratings yet

- 29 Ke-toan-quoc-te-2 201109 Đề-01 Cky3 CLC 13h30 10.09.2021-2Document10 pages29 Ke-toan-quoc-te-2 201109 Đề-01 Cky3 CLC 13h30 10.09.2021-2uthanh2209No ratings yet

- Covid 19 Levy 04 Jan 2021Document30 pagesCovid 19 Levy 04 Jan 2021musicals.muNo ratings yet

- 5.09 Analysis of Income TaxesDocument10 pages5.09 Analysis of Income TaxesClaptrapjackNo ratings yet

- KẾ TOÁN QUỐC TẾ 1 - TEST GIỮA KỲDocument41 pagesKẾ TOÁN QUỐC TẾ 1 - TEST GIỮA KỲLINH PHAN THINo ratings yet

- ACCO1115 - 2021 - JULY - EXAM - OnlineDocument11 pagesACCO1115 - 2021 - JULY - EXAM - OnlineSarah RanduNo ratings yet

- ABC Co LTD - Case Study Test - RevisedDocument2 pagesABC Co LTD - Case Study Test - Revisedroman marian89No ratings yet

- Bài tập chủ đề 6Document7 pagesBài tập chủ đề 6thanhtrucNo ratings yet

- BACC 2206- Intermediate Accounting II _ Assignment Jan - April 2023Document3 pagesBACC 2206- Intermediate Accounting II _ Assignment Jan - April 2023jacintavike42No ratings yet

- VAT Other Aspects - January 2024Document5 pagesVAT Other Aspects - January 2024Charisma CharlesNo ratings yet

- Quizzz Intac 3Document10 pagesQuizzz Intac 3lana del reyNo ratings yet

- AP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document4 pagesAP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Kate PaquizNo ratings yet

- 3.2 Business Profit TaxDocument53 pages3.2 Business Profit TaxBizu AtnafuNo ratings yet

- Answer Key - Income Tax Peer Tutoring Quiz (Chapter 4)Document4 pagesAnswer Key - Income Tax Peer Tutoring Quiz (Chapter 4)Jahz Aira GamboaNo ratings yet

- Audit of Liabilities Quiz 3Document3 pagesAudit of Liabilities Quiz 3Cattleya50% (2)

- Ey Ireland Early Payment of 2020 Excess Randd Tax CreditsDocument5 pagesEy Ireland Early Payment of 2020 Excess Randd Tax CreditsharryNo ratings yet

- W5 - AS2 - Deferred TaxesDocument2 pagesW5 - AS2 - Deferred TaxesJere Mae MarananNo ratings yet

- F00540010220143001Homework Chapter 19 and 21Document2 pagesF00540010220143001Homework Chapter 19 and 21Nur Hidayah K FNo ratings yet

- Ac5007 QuestionsDocument8 pagesAc5007 QuestionsyinlengNo ratings yet

- AccountingDocument6 pagesAccountingBlue HourNo ratings yet

- 4 - CIT - TI ReductionsDocument13 pages4 - CIT - TI ReductionsMaricarmen SilvaNo ratings yet

- FA2-08 Income TaxesDocument3 pagesFA2-08 Income Taxeskrisha millo0% (1)

- Tax Planning and Compliance: Page 1 of 5Document5 pagesTax Planning and Compliance: Page 1 of 5Srikrishna DharNo ratings yet

- TAX PLANNING & COMPLIANCE - MA-2022 - QuestionDocument6 pagesTAX PLANNING & COMPLIANCE - MA-2022 - QuestionsajedulNo ratings yet

- Income Tax - ExercisesDocument2 pagesIncome Tax - ExercisesEnges FormulaNo ratings yet

- Chapter 22 Deferred Tax Asset and LiabilityDocument8 pagesChapter 22 Deferred Tax Asset and LiabilityCheesca Macabanti - 12 Euclid-Digital ModularNo ratings yet

- Revision 1-9 MCDocument5 pagesRevision 1-9 MCdilinhtinh04No ratings yet

- Assumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceDocument4 pagesAssumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceAireyNo ratings yet

- W4 TaxesDocument35 pagesW4 TaxesVanessa LeeNo ratings yet

- 20th Regional Mid Year Convention Cup 6 Easy RoundDocument18 pages20th Regional Mid Year Convention Cup 6 Easy RoundSophia De GuzmanNo ratings yet

- Financial Accounting 3.1Document6 pagesFinancial Accounting 3.1Tawanda HerbertNo ratings yet

- Kế Toán Quốc Tế: Select oneDocument8 pagesKế Toán Quốc Tế: Select oneLoki Luke100% (1)

- Income Taxes - Question BookDocument27 pagesIncome Taxes - Question Bookandiswa zuluNo ratings yet

- Additional Question 1Document1 pageAdditional Question 1Nurul AinaNo ratings yet

- Final Examn Dec 2022 CF2 ALLDocument7 pagesFinal Examn Dec 2022 CF2 ALLleyrepavonNo ratings yet

- 17 CPA ADVANCED TAXATION Paper 17Document9 pages17 CPA ADVANCED TAXATION Paper 17kabendejunior4No ratings yet

- Taxtest 1Document5 pagesTaxtest 1alaaomarmazharmohamedNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Tax2 Bar Q - A (2007-2016) (LSG1718)Document46 pagesTax2 Bar Q - A (2007-2016) (LSG1718)Naethan Jhoe L. CiprianoNo ratings yet

- Kanya KarungalDocument13 pagesKanya KarungalramNo ratings yet

- ReSA Batch 47 ScheduleDocument1 pageReSA Batch 47 ScheduleyshizamNo ratings yet

- Financial Accounting Solution ch14Document23 pagesFinancial Accounting Solution ch14hw cNo ratings yet

- ACCCOB1 Quiz 1 Monday Set A Answer Key PDFDocument4 pagesACCCOB1 Quiz 1 Monday Set A Answer Key PDFfanchasticommsNo ratings yet

- Valix 17 20 MCQ and Theory Emp Ben She PDFDocument48 pagesValix 17 20 MCQ and Theory Emp Ben She PDFMitchie FaustinoNo ratings yet

- Semester Teaching Plan 2021-2022 Semester 1: Subject Code and Title Course Convenor Course InstructorsDocument5 pagesSemester Teaching Plan 2021-2022 Semester 1: Subject Code and Title Course Convenor Course InstructorsDimitriNo ratings yet

- SudhaDocument7 pagesSudhaSneha AgrawalNo ratings yet

- Problem 5Document3 pagesProblem 5Rudy LugasNo ratings yet

- CHAPTER 13 B - Special Allowable Itemized Deductions and NOLCODocument2 pagesCHAPTER 13 B - Special Allowable Itemized Deductions and NOLCODeviane CalabriaNo ratings yet

- Research Paper On Cash Flow ManagementDocument4 pagesResearch Paper On Cash Flow Managementihprzlbkf100% (1)

- New Jersey Complete Business Registration PacketDocument47 pagesNew Jersey Complete Business Registration PacketWen' George BeyNo ratings yet

- COMM1140 - 2021T1 - Week 1 Lecture Slides - Master Deck From Live LectureDocument43 pagesCOMM1140 - 2021T1 - Week 1 Lecture Slides - Master Deck From Live LectureLia LeNo ratings yet

- Sample Final Exam Questions W19 March 31 With Answers - Leverage DividendsDocument3 pagesSample Final Exam Questions W19 March 31 With Answers - Leverage Dividendsbusiness docNo ratings yet

- University of Mauritius: Faculty of Law and ManagementDocument9 pagesUniversity of Mauritius: Faculty of Law and ManagementMîñåk ŞhïïNo ratings yet

- Module No 4 - Capital Gains TaxDocument8 pagesModule No 4 - Capital Gains TaxBetty SantiagoNo ratings yet

- Financial Statements and Ratio AnalysisDocument9 pagesFinancial Statements and Ratio AnalysisRabie HarounNo ratings yet

- Section 10 of The Income Tax ActDocument10 pagesSection 10 of The Income Tax ActVANSHIKA SINGHNo ratings yet

- 06 Financial Statement Preparation, Closing Entries, and Reversing EntriesDocument18 pages06 Financial Statement Preparation, Closing Entries, and Reversing Entriescarlo bundalianNo ratings yet

- Financial Management: Roll No. Total No. of Pages: 02 Total No. of Questions: 08 BBA (Sem.-4)Document2 pagesFinancial Management: Roll No. Total No. of Pages: 02 Total No. of Questions: 08 BBA (Sem.-4)Shlok MittalNo ratings yet

- Ratio AnalysisDocument36 pagesRatio Analysisjigar ramNo ratings yet

- Wage and Tax Statement: OMB No. 1545-0008Document4 pagesWage and Tax Statement: OMB No. 1545-0008jgoldson235No ratings yet

- Relative ValuationDocument26 pagesRelative ValuationRAKESH SINGHNo ratings yet

- Sekai 05Document2 pagesSekai 05Micaela EncinasNo ratings yet

- Chapter 2911Document19 pagesChapter 2911Madhu kumarNo ratings yet

- Domondon Taxation 2022 Bar Bulletin No. 31 S. 2022Document210 pagesDomondon Taxation 2022 Bar Bulletin No. 31 S. 2022Cedric Comon100% (1)

- Unit 4 - DPSPS, RRSPs and TFSAsDocument61 pagesUnit 4 - DPSPS, RRSPs and TFSAsMITALI SWADIYANo ratings yet