Download as pdf or txt

You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Practical Wisdom - The Right Way To Do The Right Thing - PDFDocument5 pagesPractical Wisdom - The Right Way To Do The Right Thing - PDFChauhan RadhaNo ratings yet

- Service-manual-SG Emachines E725 E525 031809Document236 pagesService-manual-SG Emachines E725 E525 031809andhrimnirNo ratings yet

- Toshiba Case 3Document4 pagesToshiba Case 3Deta Detade100% (1)

- CREATE Zalamea Briefing + RRsDocument76 pagesCREATE Zalamea Briefing + RRsGerryNo ratings yet

- "Individual Paper Return For Tax Year 2021: SignatureDocument25 pages"Individual Paper Return For Tax Year 2021: SignatureWaqas MehmoodNo ratings yet

- Individual Paper Return For Tax Year 2020: SignatureDocument26 pagesIndividual Paper Return For Tax Year 2020: SignaturejamalNo ratings yet

- In Come Tax Return Form 2019Document48 pagesIn Come Tax Return Form 2019Mirza Naseer AbbasNo ratings yet

- Appendix 7b - Rror-SagfDocument1 pageAppendix 7b - Rror-SagfEdwin Siruno LopezNo ratings yet

- GST Handwritten Notes Charts Etc 30032018Document90 pagesGST Handwritten Notes Charts Etc 30032018Prasad Rao60% (5)

- Module 3 ACCTDocument16 pagesModule 3 ACCTFathimath NoohaNo ratings yet

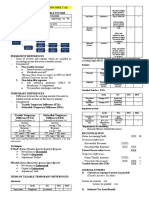

- IAS 12 BinderDocument20 pagesIAS 12 BinderUmer Shah100% (1)

- IND AS 12 Income TaxesDocument5 pagesIND AS 12 Income TaxesPavan Kumar PurohitNo ratings yet

- FR - Ias 12Document1 pageFR - Ias 12Zubair JallohNo ratings yet

- Business Expenses Worksheet 2020Document2 pagesBusiness Expenses Worksheet 2020Dendi MonNo ratings yet

- 2 - CIT - Tax AdjustmentsDocument56 pages2 - CIT - Tax AdjustmentsMaricarmen SilvaNo ratings yet

- FBR Tax FilingDocument48 pagesFBR Tax FilingMuhammad Waqas Hanif100% (2)

- Individual Paper Return For Tax Year 2019: SignatureDocument10 pagesIndividual Paper Return For Tax Year 2019: SignatureEngr Saad Bin SarfrazNo ratings yet

- Manual Return 2023Document28 pagesManual Return 2023arsalanghuralgtNo ratings yet

- Individual Paper Returnfor Tax Year 2022Document25 pagesIndividual Paper Returnfor Tax Year 2022abdul karimNo ratings yet

- US Internal Revenue Service: fct1 - 1996Document2 pagesUS Internal Revenue Service: fct1 - 1996IRSNo ratings yet

- Salary Tds Computation Sheet Sec 192bDocument1 pageSalary Tds Computation Sheet Sec 192bpradhan13No ratings yet

- BIR Form No. 1600Document2 pagesBIR Form No. 1600Lorraine Steffany BanguisNo ratings yet

- Manage Taxes - 8Document1 pageManage Taxes - 8I'm RangaNo ratings yet

- Acknowledgement HauajwbwbajsjajaDocument1 pageAcknowledgement HauajwbwbajsjajaAnkush ManhasNo ratings yet

- IA2 Income TaxesDocument1 pageIA2 Income TaxesJoey Mhey BenicoNo ratings yet

- Income Tax Calculator 2018-2019Document1 pageIncome Tax Calculator 2018-2019Muhammad Hanif SuchwaniNo ratings yet

- Problem Set 6Document9 pagesProblem Set 6Jade BilisNo ratings yet

- Accounting Standard 22Document23 pagesAccounting Standard 22Rida TaarnnumNo ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement 2021-22: Do Not Send This Acknowledgement To CPC, BengaluruDupati K VeerappaNo ratings yet

- FRA - 10-Income TaxesDocument35 pagesFRA - 10-Income Taxeskmayank0723No ratings yet

- 2021 GeneralDocument8 pages2021 GeneralWajiha HaroonNo ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement 2021-22: Do Not Send This Acknowledgement To CPC, BengaluruDIVYANSHU SHEKHARNo ratings yet

- US Internal Revenue Service: f943 - 1995Document4 pagesUS Internal Revenue Service: f943 - 1995IRSNo ratings yet

- Acknowledgement Niket Panjiier Army LucknowDocument1 pageAcknowledgement Niket Panjiier Army Lucknowbeauty kumariNo ratings yet

- MODIFIED - TIMTA Annexes For CREATE FAs of 20 June 2021Document14 pagesMODIFIED - TIMTA Annexes For CREATE FAs of 20 June 2021Sunshine PaglinawanNo ratings yet

- US Internal Revenue Service: fct1 - 2000Document2 pagesUS Internal Revenue Service: fct1 - 2000IRSNo ratings yet

- US Internal Revenue Service: fct1 - 1997Document2 pagesUS Internal Revenue Service: fct1 - 1997IRSNo ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Do Not Send This Acknowledgement To CPC, BengaluruDocument2 pagesIndian Income Tax Return Acknowledgement 2021-22: Do Not Send This Acknowledgement To CPC, BengaluruHussain YadavNo ratings yet

- Manual ReturnDocument26 pagesManual ReturnMuhammad Arsalan TariqNo ratings yet

- Accounting of Taxation in Accordance With ITO 1984 (IAS-12)Document35 pagesAccounting of Taxation in Accordance With ITO 1984 (IAS-12)Gazi Md. Ifthakhar HossainNo ratings yet

- Income Taxes: Basic ConceptsDocument7 pagesIncome Taxes: Basic ConceptsTrisha Mae Mendoza MacalinoNo ratings yet

- IAS 12 - Income Taxes - Measurement - Permanent DifferencesDocument4 pagesIAS 12 - Income Taxes - Measurement - Permanent DifferencesReenestus DumeniNo ratings yet

- 9 M - 28-Dec-2020 - 917355441Document1 page9 M - 28-Dec-2020 - 917355441Arihant SatpathyNo ratings yet

- Performa Income StatementDocument1 pagePerforma Income StatementAhsan JamalNo ratings yet

- Handout - Deferred Tax Asset (March 8, 2024)Document30 pagesHandout - Deferred Tax Asset (March 8, 2024)atty.francis.angelo.lopezNo ratings yet

- Form BDocument2 pagesForm BPower MuruganNo ratings yet

- US Internal Revenue Service: f943 - 1996Document4 pagesUS Internal Revenue Service: f943 - 1996IRSNo ratings yet

- 2020 09 13 10 56 29 221 - 1599974789221 - XXXPR9253X - AcknowledgementDocument1 page2020 09 13 10 56 29 221 - 1599974789221 - XXXPR9253X - Acknowledgementraoanagha27No ratings yet

- Ack Fy 2019-20Document1 pageAck Fy 2019-20Prashant MoreNo ratings yet

- Itr Ay 21-22Document6 pagesItr Ay 21-22sagarsavla110No ratings yet

- ITR AY 21-22Document1 pageITR AY 21-22rishi0184parkashNo ratings yet

- 2020 07 31 16 05 55 486 - 1596191755486 - XXXPK8367X - AcknowledgementDocument1 page2020 07 31 16 05 55 486 - 1596191755486 - XXXPK8367X - AcknowledgementSiva Jyothi KNo ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Do Not Send This Acknowledgement To CPC, BengaluruDocument8 pagesIndian Income Tax Return Acknowledgement 2021-22: Do Not Send This Acknowledgement To CPC, Bengalurubhashkar yadavNo ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Do Not Send This Acknowledgement To CPC, BengaluruDocument2 pagesIndian Income Tax Return Acknowledgement 2021-22: Do Not Send This Acknowledgement To CPC, BengaluruHussain YadavNo ratings yet

- Instructions For Filling in Return Form & Wealth Statement Form Sr. InstructionDocument15 pagesInstructions For Filling in Return Form & Wealth Statement Form Sr. InstructionTausif ArshadNo ratings yet

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruMadhan Kumar BobbalaNo ratings yet

- Ack Ahipk1805e 2021-22 452077740280322Document1 pageAck Ahipk1805e 2021-22 452077740280322b.ramanareddy7226No ratings yet

- Farm Expenses Worksheet 2021Document2 pagesFarm Expenses Worksheet 2021Finn KevinNo ratings yet

- MacroDocument2 pagesMacrominnie.patittaNo ratings yet

- Pas 12: Accounting For Income TaxDocument2 pagesPas 12: Accounting For Income TaxKiana FernandezNo ratings yet

- RACS Itr 2020-2021Document1 pageRACS Itr 2020-2021Lakshay SharmaNo ratings yet

- Current Trends of Farm Power Sources inDocument6 pagesCurrent Trends of Farm Power Sources inNakul DevaiahNo ratings yet

- Chapter Outline For FTSDocument1 pageChapter Outline For FTSBalvinder SinghNo ratings yet

- Astaro Security Gateway enDocument4 pagesAstaro Security Gateway enmaxbyzNo ratings yet

- Special Conditions of Contract (SCC) : Section - VDocument16 pagesSpecial Conditions of Contract (SCC) : Section - VAnonymous 7ZYHilDNo ratings yet

- Cesabb 300 B 400Document8 pagesCesabb 300 B 400BeyzaNo ratings yet

- EF4e Intplus Filetest 3bDocument7 pagesEF4e Intplus Filetest 3bjeanneramazanovaNo ratings yet

- 5 Leadership LessonsDocument2 pages5 Leadership LessonsnyniccNo ratings yet

- Analysis of Customer Attitude, Preference and Satisfaction Level of Mutual Fund InvestmentDocument109 pagesAnalysis of Customer Attitude, Preference and Satisfaction Level of Mutual Fund Investmentlalitgitam80% (5)

- Advancement ProposalDocument2 pagesAdvancement ProposalJEFFERSON GOMEZNo ratings yet

- Sro 565-2006Document44 pagesSro 565-2006Abdullah Jathol100% (1)

- Public Sector Accounting Tutorial (Ain)Document2 pagesPublic Sector Accounting Tutorial (Ain)Ain FatihahNo ratings yet

- Anh Văn Chuyên NgànhDocument7 pagesAnh Văn Chuyên Ngành19150004No ratings yet

- Characteristics Finite Element Methods in Computational Fluid Dynamics - J. Iannelli (Springer, 2006) WW PDFDocument744 pagesCharacteristics Finite Element Methods in Computational Fluid Dynamics - J. Iannelli (Springer, 2006) WW PDFsanaNo ratings yet

- Example 12: Design of Panel Walls: SolutionDocument2 pagesExample 12: Design of Panel Walls: SolutionSajidAliKhanNo ratings yet

- (IMechE Conference Transactions) PEP (Professional Engineering Publishers) - Power Station Maintenance - Professional Engineering Publishing (2000) PDFDocument266 pages(IMechE Conference Transactions) PEP (Professional Engineering Publishers) - Power Station Maintenance - Professional Engineering Publishing (2000) PDFAlexanderNo ratings yet

- 0508 First Language Arabic: MARK SCHEME For The October/November 2014 SeriesDocument5 pages0508 First Language Arabic: MARK SCHEME For The October/November 2014 SeriessCience 123No ratings yet

- Score:: 1 Out of 1.00 PointDocument12 pagesScore:: 1 Out of 1.00 PointDiscord YtNo ratings yet

- Applied Economics Module 3 Q1Document21 pagesApplied Economics Module 3 Q1Jefferson Del Rosario100% (1)

- Project WorkDocument6 pagesProject WorkNurbek YaxshimuratovNo ratings yet

- Alim Knit (BD) LTD.: Recommended Process Flow DiagramDocument1 pageAlim Knit (BD) LTD.: Recommended Process Flow DiagramKamrul HasanNo ratings yet

- Strand A Ilp Lesson PlanDocument3 pagesStrand A Ilp Lesson PlanyoNo ratings yet

- Midas - NFX - 2022R1 - Release NoteDocument10 pagesMidas - NFX - 2022R1 - Release NoteCristian Camilo Londoño PiedrahítaNo ratings yet

- Tiger Grey Card CopyrightDocument2 pagesTiger Grey Card Copyrightsabo6181No ratings yet

- Gs Survey & Engineers: Tax InvoiceDocument2 pagesGs Survey & Engineers: Tax InvoiceShivendra KumarNo ratings yet

- GSM System Fundamental TrainingDocument144 pagesGSM System Fundamental Trainingmansonbazzokka100% (2)

- University of Michigan Dissertation ArchiveDocument6 pagesUniversity of Michigan Dissertation ArchiveBuyResumePaperUK100% (1)