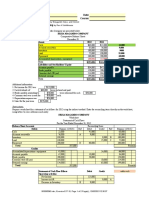

Test 2 Memo (Question 1)

Test 2 Memo (Question 1)

You might also like

- Case 21Document14 pagesCase 21Gabriela LueiroNo ratings yet

- SOALDocument2 pagesSOALjwtrmdhnNo ratings yet

- 13 Week Cash Flow ModelDocument16 pages13 Week Cash Flow ModelASChipLeadNo ratings yet

- B326 MTA Fall 2017-2018 MGLDocument7 pagesB326 MTA Fall 2017-2018 MGLmjlNo ratings yet

- Problem 1 1. Record The Transactions To Account The Investment. P Corporation's BooksDocument2 pagesProblem 1 1. Record The Transactions To Account The Investment. P Corporation's BooksArtisanNo ratings yet

- 2018 Revision Fin Statements MEMO A1Document3 pages2018 Revision Fin Statements MEMO A1oersoncalebNo ratings yet

- The Grape Group (Acquisition) : Cfap 1: A A F RDocument1 pageThe Grape Group (Acquisition) : Cfap 1: A A F R.No ratings yet

- Sloved Questions Financial AnalysisDocument12 pagesSloved Questions Financial AnalysisMurad KhanNo ratings yet

- FINAL EXAM - Part 2Document4 pagesFINAL EXAM - Part 2Elton ArcenasNo ratings yet

- Lecture 2 - Interpreting Financial Statements + Seminar QuestionDocument17 pagesLecture 2 - Interpreting Financial Statements + Seminar QuestionMahad UzairNo ratings yet

- Assessed Coursework 2 - S2 2020 UpdateDocument7 pagesAssessed Coursework 2 - S2 2020 UpdateArmaghan Ali MalikNo ratings yet

- Case Study - BCVE and Preacquistion EntriesDocument3 pagesCase Study - BCVE and Preacquistion EntriesHuỳnh Minh Gia HàoNo ratings yet

- Business Combination Stock AcquisitionDocument2 pagesBusiness Combination Stock AcquisitionTEOPE, EMERLIZA DE CASTRONo ratings yet

- FA3 - GA1 - Group 3Document13 pagesFA3 - GA1 - Group 305 - Trần Mai AnhNo ratings yet

- PE Illustrative-Financial-Statements-2022 PEDocument40 pagesPE Illustrative-Financial-Statements-2022 PECalebNo ratings yet

- Conceptual Framework & Accounting Standards: Preparation & Presentation of Financial StatementsDocument35 pagesConceptual Framework & Accounting Standards: Preparation & Presentation of Financial StatementsJocy DelgadoNo ratings yet

- Chapter 6 - Consolidated Financial Statements (Part 3)Document41 pagesChapter 6 - Consolidated Financial Statements (Part 3)Rena Jocelle NalzaroNo ratings yet

- Chapter 4 Accounting For Business Combinations SolmanDocument16 pagesChapter 4 Accounting For Business Combinations SolmanCharlene Bolandres100% (1)

- BFA301 Solution For Lecture Example 3-2Document6 pagesBFA301 Solution For Lecture Example 3-2erinNo ratings yet

- Intermediate Accounting 3Document105 pagesIntermediate Accounting 3Lehnard Delos Reyes GellorNo ratings yet

- CH 13Document4 pagesCH 13Sri HimajaNo ratings yet

- Additional Consolidation Reporting IssuesDocument61 pagesAdditional Consolidation Reporting IssuesDifaNo ratings yet

- LU5 WorkbookDocument16 pagesLU5 Workbookprowess222No ratings yet

- Liquidity Ratios - Practice QuestionsDocument14 pagesLiquidity Ratios - Practice QuestionsOsama SaleemNo ratings yet

- UntitledDocument5 pagesUntitledm habiburrahman55No ratings yet

- BRS3B Assessment Opportunity 1 2019Document11 pagesBRS3B Assessment Opportunity 1 2019221103909No ratings yet

- Ia Vol 3 Valix Solman 2019Document105 pagesIa Vol 3 Valix Solman 2019Pipz G. CastroNo ratings yet

- Kellogg Company Balance SheetDocument5 pagesKellogg Company Balance SheetGoutham BindigaNo ratings yet

- Balance SHDocument2 pagesBalance SHRaj GoyalNo ratings yet

- ACG211E Test 1 Suggested SolutionDocument5 pagesACG211E Test 1 Suggested Solutionsphesihlemkhize1204No ratings yet

- SOLUTION TO SCHEDULE 3gDocument4 pagesSOLUTION TO SCHEDULE 3gKrushna Omprakash MundadaNo ratings yet

- Far320 Capital Reduction ExercisesDocument7 pagesFar320 Capital Reduction ExercisesALIA MAISARA MD AKHIRNo ratings yet

- Consolidation and Equity Accounting - ExampleDocument12 pagesConsolidation and Equity Accounting - ExampleRobert lincolnNo ratings yet

- 2024 MGB Group 06 v1Document5 pages2024 MGB Group 06 v1sakshisingh0712No ratings yet

- Academia - Week 2 - Assignment - UnderstDocument12 pagesAcademia - Week 2 - Assignment - UnderstLovey AgarwalNo ratings yet

- 2023 - Session12 - 13 FSA2 - MBA - SentDocument32 pages2023 - Session12 - 13 FSA2 - MBA - SentAkshat MathurNo ratings yet

- Unit 5-Group Statements L IFRS 3 Business Combinations (2024)Document9 pagesUnit 5-Group Statements L IFRS 3 Business Combinations (2024)jamileethomNo ratings yet

- Notes For Ratios: Accounting Principles AssetsDocument14 pagesNotes For Ratios: Accounting Principles AssetsSudhanshu MathurNo ratings yet

- Accounting IAS (Malaysia) Model Answers Series 2 2007 Old SyllabusDocument18 pagesAccounting IAS (Malaysia) Model Answers Series 2 2007 Old SyllabusAung Zaw HtweNo ratings yet

- Accounts Questions Compiler PDFDocument187 pagesAccounts Questions Compiler PDFBrinda RNo ratings yet

- Firda Arfianti - LC53 - Consolidated Workpaper, Wholly Owned SubsidiaryDocument3 pagesFirda Arfianti - LC53 - Consolidated Workpaper, Wholly Owned SubsidiaryFirdaNo ratings yet

- Merck & Company, Inc. Year 9 Selected Financial Data ($ Millions) Income Statement DataDocument2 pagesMerck & Company, Inc. Year 9 Selected Financial Data ($ Millions) Income Statement DataUmme Laila JatoiNo ratings yet

- RNOA 17th AprilDocument2 pagesRNOA 17th AprilUmme Laila JatoiNo ratings yet

- Material 1.1 Additional NotesDocument2 pagesMaterial 1.1 Additional NotesCristine Joy BenitezNo ratings yet

- AFI3512 Test 4 2022 QuestionDocument6 pagesAFI3512 Test 4 2022 Questionkevgoat217No ratings yet

- Abc Chapter 2Document22 pagesAbc Chapter 2ZNo ratings yet

- Case CosminDocument6 pagesCase CosminRoche ChenNo ratings yet

- ASS 1 2021 Part A SolutionDocument4 pagesASS 1 2021 Part A SolutionOdzulaho DemanaNo ratings yet

- Genuime Company Required 1 Debit CreditDocument15 pagesGenuime Company Required 1 Debit CreditAnonnNo ratings yet

- Financial Accounting Paper WajeehaDocument8 pagesFinancial Accounting Paper WajeehaTAIMOOR REHMANNo ratings yet

- QuizDocument41 pagesQuizbar barNo ratings yet

- Name: Date: Instructor: Course: Accounting Principles Primer On Using Excel in AccountingDocument2 pagesName: Date: Instructor: Course: Accounting Principles Primer On Using Excel in AccountingHernando MaulanaNo ratings yet

- Acctg 305 Midterm Quiz 1 (With Answers)Document4 pagesAcctg 305 Midterm Quiz 1 (With Answers)Michelle Joyce KuizonNo ratings yet

- Kelompok 6 - UTS AKMDocument18 pagesKelompok 6 - UTS AKM21-010 Desi MailaniNo ratings yet

- Question No 1: Journal EntriesDocument3 pagesQuestion No 1: Journal EntriesMUKHTALIFNo ratings yet

- Cap III Group I RTP Dec 2023Document111 pagesCap III Group I RTP Dec 2023meme.arena786No ratings yet

- Safetex Complete Answer ICAEWDocument2 pagesSafetex Complete Answer ICAEWMuhammmad Ramzan YasinNo ratings yet

- Chapter Five PrintDocument18 pagesChapter Five PrintGedionNo ratings yet

- Lecture 2 A Further Loot at Financial StatementsDocument33 pagesLecture 2 A Further Loot at Financial StatementsMajdiNo ratings yet

- Wa0002Document17 pagesWa0002Vanshu's lifeNo ratings yet

- Ross 10e Chap002 PPTDocument34 pagesRoss 10e Chap002 PPTAramis SantanaNo ratings yet

- FINA3010 Session4Document70 pagesFINA3010 Session4eddy ngNo ratings yet

- IBIG 06 08 Case Description SolutionsDocument8 pagesIBIG 06 08 Case Description Solutionsjohnson jakeNo ratings yet

- 34 Tongwell PLCDocument2 pages34 Tongwell PLCxichristinaNo ratings yet

- Valuation NotesDocument4 pagesValuation NotesArielle CabritoNo ratings yet

- CH 13Document42 pagesCH 13mariam mohammedNo ratings yet

- Financial Management & Economics For Finance: by Ca Swapnil PatniDocument5 pagesFinancial Management & Economics For Finance: by Ca Swapnil PatniSohail Ahmed KhiljiNo ratings yet

- Capital BudgetingDocument26 pagesCapital BudgetingTisha SosaNo ratings yet

- CF Qs C4 (B11)Document6 pagesCF Qs C4 (B11)shah gNo ratings yet

- Capital BudgetingDocument48 pagesCapital Budgetingarthur portalNo ratings yet

- SSY Vs MF CalculatorDocument8 pagesSSY Vs MF CalculatorSiva Prasad TNo ratings yet

- 7.30.14 Accounting For M&A - Accounting For Business Combinations Acquisition MethodDocument13 pages7.30.14 Accounting For M&A - Accounting For Business Combinations Acquisition MethodSantos MotaNo ratings yet

- F7.2 - Mock Test 1Document5 pagesF7.2 - Mock Test 1huusinh2402No ratings yet

- Highlight IFRSDocument16 pagesHighlight IFRSBảo Hân VũNo ratings yet

- Lectorial and Tutorial Q Scots and AbishotDocument2 pagesLectorial and Tutorial Q Scots and AbishotLê Quốc TriệuNo ratings yet

- Ellen Fin3701 S2Document6 pagesEllen Fin3701 S2George DywiliNo ratings yet

- Financial Statements 24 Questions AnswersDocument6 pagesFinancial Statements 24 Questions AnswersGideon Turner100% (2)

- 42-Shubham Hanbar-Sybaf A (Business Economics 2)Document11 pages42-Shubham Hanbar-Sybaf A (Business Economics 2)shubham hanbarNo ratings yet

- Solution Chapter 6 Financial Statements Pre Adjustments 1Document8 pagesSolution Chapter 6 Financial Statements Pre Adjustments 1IsmahNo ratings yet

- Consolidation MCQSDocument7 pagesConsolidation MCQSvyom rajNo ratings yet

- Pre IPO WhatsappDocument7 pagesPre IPO WhatsappviehnuhdjdhNo ratings yet

- VHINSON - Intermediate Accounting 3 (2023 - 2024 Edition) - 101Document1 pageVHINSON - Intermediate Accounting 3 (2023 - 2024 Edition) - 101Alyssa NacionNo ratings yet

- DCF Residential Training - 5may2017Document23 pagesDCF Residential Training - 5may2017Sarthak ShuklaNo ratings yet

- Accounting Eng ABDocument20 pagesAccounting Eng ABsajolramdaw1609No ratings yet

- Preparation Kit 2024 - IIM ShillongDocument129 pagesPreparation Kit 2024 - IIM ShillongBhagyashree MahajanNo ratings yet

- DCF and Pensions The Footnotes AnalystDocument10 pagesDCF and Pensions The Footnotes Analystmichael odiemboNo ratings yet

- 3.4 Final Accounts Balance Sheet (Statement of Financial Position)Document45 pages3.4 Final Accounts Balance Sheet (Statement of Financial Position)Magdalena NeuschitzerNo ratings yet

- Analysis SumsDocument11 pagesAnalysis SumsJessy NairNo ratings yet

- Chapter 8 Performance Measurement Evaluation Nov2020 1Document113 pagesChapter 8 Performance Measurement Evaluation Nov2020 1Question BankNo ratings yet

Download as pdf or txt

You might also like

- Case 21Document14 pagesCase 21Gabriela LueiroNo ratings yet

- SOALDocument2 pagesSOALjwtrmdhnNo ratings yet

- 13 Week Cash Flow ModelDocument16 pages13 Week Cash Flow ModelASChipLeadNo ratings yet

- B326 MTA Fall 2017-2018 MGLDocument7 pagesB326 MTA Fall 2017-2018 MGLmjlNo ratings yet

- Problem 1 1. Record The Transactions To Account The Investment. P Corporation's BooksDocument2 pagesProblem 1 1. Record The Transactions To Account The Investment. P Corporation's BooksArtisanNo ratings yet

- 2018 Revision Fin Statements MEMO A1Document3 pages2018 Revision Fin Statements MEMO A1oersoncalebNo ratings yet

- The Grape Group (Acquisition) : Cfap 1: A A F RDocument1 pageThe Grape Group (Acquisition) : Cfap 1: A A F R.No ratings yet

- Sloved Questions Financial AnalysisDocument12 pagesSloved Questions Financial AnalysisMurad KhanNo ratings yet

- FINAL EXAM - Part 2Document4 pagesFINAL EXAM - Part 2Elton ArcenasNo ratings yet

- Lecture 2 - Interpreting Financial Statements + Seminar QuestionDocument17 pagesLecture 2 - Interpreting Financial Statements + Seminar QuestionMahad UzairNo ratings yet

- Assessed Coursework 2 - S2 2020 UpdateDocument7 pagesAssessed Coursework 2 - S2 2020 UpdateArmaghan Ali MalikNo ratings yet

- Case Study - BCVE and Preacquistion EntriesDocument3 pagesCase Study - BCVE and Preacquistion EntriesHuỳnh Minh Gia HàoNo ratings yet

- Business Combination Stock AcquisitionDocument2 pagesBusiness Combination Stock AcquisitionTEOPE, EMERLIZA DE CASTRONo ratings yet

- FA3 - GA1 - Group 3Document13 pagesFA3 - GA1 - Group 305 - Trần Mai AnhNo ratings yet

- PE Illustrative-Financial-Statements-2022 PEDocument40 pagesPE Illustrative-Financial-Statements-2022 PECalebNo ratings yet

- Conceptual Framework & Accounting Standards: Preparation & Presentation of Financial StatementsDocument35 pagesConceptual Framework & Accounting Standards: Preparation & Presentation of Financial StatementsJocy DelgadoNo ratings yet

- Chapter 6 - Consolidated Financial Statements (Part 3)Document41 pagesChapter 6 - Consolidated Financial Statements (Part 3)Rena Jocelle NalzaroNo ratings yet

- Chapter 4 Accounting For Business Combinations SolmanDocument16 pagesChapter 4 Accounting For Business Combinations SolmanCharlene Bolandres100% (1)

- BFA301 Solution For Lecture Example 3-2Document6 pagesBFA301 Solution For Lecture Example 3-2erinNo ratings yet

- Intermediate Accounting 3Document105 pagesIntermediate Accounting 3Lehnard Delos Reyes GellorNo ratings yet

- CH 13Document4 pagesCH 13Sri HimajaNo ratings yet

- Additional Consolidation Reporting IssuesDocument61 pagesAdditional Consolidation Reporting IssuesDifaNo ratings yet

- LU5 WorkbookDocument16 pagesLU5 Workbookprowess222No ratings yet

- Liquidity Ratios - Practice QuestionsDocument14 pagesLiquidity Ratios - Practice QuestionsOsama SaleemNo ratings yet

- UntitledDocument5 pagesUntitledm habiburrahman55No ratings yet

- BRS3B Assessment Opportunity 1 2019Document11 pagesBRS3B Assessment Opportunity 1 2019221103909No ratings yet

- Ia Vol 3 Valix Solman 2019Document105 pagesIa Vol 3 Valix Solman 2019Pipz G. CastroNo ratings yet

- Kellogg Company Balance SheetDocument5 pagesKellogg Company Balance SheetGoutham BindigaNo ratings yet

- Balance SHDocument2 pagesBalance SHRaj GoyalNo ratings yet

- ACG211E Test 1 Suggested SolutionDocument5 pagesACG211E Test 1 Suggested Solutionsphesihlemkhize1204No ratings yet

- SOLUTION TO SCHEDULE 3gDocument4 pagesSOLUTION TO SCHEDULE 3gKrushna Omprakash MundadaNo ratings yet

- Far320 Capital Reduction ExercisesDocument7 pagesFar320 Capital Reduction ExercisesALIA MAISARA MD AKHIRNo ratings yet

- Consolidation and Equity Accounting - ExampleDocument12 pagesConsolidation and Equity Accounting - ExampleRobert lincolnNo ratings yet

- 2024 MGB Group 06 v1Document5 pages2024 MGB Group 06 v1sakshisingh0712No ratings yet

- Academia - Week 2 - Assignment - UnderstDocument12 pagesAcademia - Week 2 - Assignment - UnderstLovey AgarwalNo ratings yet

- 2023 - Session12 - 13 FSA2 - MBA - SentDocument32 pages2023 - Session12 - 13 FSA2 - MBA - SentAkshat MathurNo ratings yet

- Unit 5-Group Statements L IFRS 3 Business Combinations (2024)Document9 pagesUnit 5-Group Statements L IFRS 3 Business Combinations (2024)jamileethomNo ratings yet

- Notes For Ratios: Accounting Principles AssetsDocument14 pagesNotes For Ratios: Accounting Principles AssetsSudhanshu MathurNo ratings yet

- Accounting IAS (Malaysia) Model Answers Series 2 2007 Old SyllabusDocument18 pagesAccounting IAS (Malaysia) Model Answers Series 2 2007 Old SyllabusAung Zaw HtweNo ratings yet

- Accounts Questions Compiler PDFDocument187 pagesAccounts Questions Compiler PDFBrinda RNo ratings yet

- Firda Arfianti - LC53 - Consolidated Workpaper, Wholly Owned SubsidiaryDocument3 pagesFirda Arfianti - LC53 - Consolidated Workpaper, Wholly Owned SubsidiaryFirdaNo ratings yet

- Merck & Company, Inc. Year 9 Selected Financial Data ($ Millions) Income Statement DataDocument2 pagesMerck & Company, Inc. Year 9 Selected Financial Data ($ Millions) Income Statement DataUmme Laila JatoiNo ratings yet

- RNOA 17th AprilDocument2 pagesRNOA 17th AprilUmme Laila JatoiNo ratings yet

- Material 1.1 Additional NotesDocument2 pagesMaterial 1.1 Additional NotesCristine Joy BenitezNo ratings yet

- AFI3512 Test 4 2022 QuestionDocument6 pagesAFI3512 Test 4 2022 Questionkevgoat217No ratings yet

- Abc Chapter 2Document22 pagesAbc Chapter 2ZNo ratings yet

- Case CosminDocument6 pagesCase CosminRoche ChenNo ratings yet

- ASS 1 2021 Part A SolutionDocument4 pagesASS 1 2021 Part A SolutionOdzulaho DemanaNo ratings yet

- Genuime Company Required 1 Debit CreditDocument15 pagesGenuime Company Required 1 Debit CreditAnonnNo ratings yet

- Financial Accounting Paper WajeehaDocument8 pagesFinancial Accounting Paper WajeehaTAIMOOR REHMANNo ratings yet

- QuizDocument41 pagesQuizbar barNo ratings yet

- Name: Date: Instructor: Course: Accounting Principles Primer On Using Excel in AccountingDocument2 pagesName: Date: Instructor: Course: Accounting Principles Primer On Using Excel in AccountingHernando MaulanaNo ratings yet

- Acctg 305 Midterm Quiz 1 (With Answers)Document4 pagesAcctg 305 Midterm Quiz 1 (With Answers)Michelle Joyce KuizonNo ratings yet

- Kelompok 6 - UTS AKMDocument18 pagesKelompok 6 - UTS AKM21-010 Desi MailaniNo ratings yet

- Question No 1: Journal EntriesDocument3 pagesQuestion No 1: Journal EntriesMUKHTALIFNo ratings yet

- Cap III Group I RTP Dec 2023Document111 pagesCap III Group I RTP Dec 2023meme.arena786No ratings yet

- Safetex Complete Answer ICAEWDocument2 pagesSafetex Complete Answer ICAEWMuhammmad Ramzan YasinNo ratings yet

- Chapter Five PrintDocument18 pagesChapter Five PrintGedionNo ratings yet

- Lecture 2 A Further Loot at Financial StatementsDocument33 pagesLecture 2 A Further Loot at Financial StatementsMajdiNo ratings yet

- Wa0002Document17 pagesWa0002Vanshu's lifeNo ratings yet

- Ross 10e Chap002 PPTDocument34 pagesRoss 10e Chap002 PPTAramis SantanaNo ratings yet

- FINA3010 Session4Document70 pagesFINA3010 Session4eddy ngNo ratings yet

- IBIG 06 08 Case Description SolutionsDocument8 pagesIBIG 06 08 Case Description Solutionsjohnson jakeNo ratings yet

- 34 Tongwell PLCDocument2 pages34 Tongwell PLCxichristinaNo ratings yet

- Valuation NotesDocument4 pagesValuation NotesArielle CabritoNo ratings yet

- CH 13Document42 pagesCH 13mariam mohammedNo ratings yet

- Financial Management & Economics For Finance: by Ca Swapnil PatniDocument5 pagesFinancial Management & Economics For Finance: by Ca Swapnil PatniSohail Ahmed KhiljiNo ratings yet

- Capital BudgetingDocument26 pagesCapital BudgetingTisha SosaNo ratings yet

- CF Qs C4 (B11)Document6 pagesCF Qs C4 (B11)shah gNo ratings yet

- Capital BudgetingDocument48 pagesCapital Budgetingarthur portalNo ratings yet

- SSY Vs MF CalculatorDocument8 pagesSSY Vs MF CalculatorSiva Prasad TNo ratings yet

- 7.30.14 Accounting For M&A - Accounting For Business Combinations Acquisition MethodDocument13 pages7.30.14 Accounting For M&A - Accounting For Business Combinations Acquisition MethodSantos MotaNo ratings yet

- F7.2 - Mock Test 1Document5 pagesF7.2 - Mock Test 1huusinh2402No ratings yet

- Highlight IFRSDocument16 pagesHighlight IFRSBảo Hân VũNo ratings yet

- Lectorial and Tutorial Q Scots and AbishotDocument2 pagesLectorial and Tutorial Q Scots and AbishotLê Quốc TriệuNo ratings yet

- Ellen Fin3701 S2Document6 pagesEllen Fin3701 S2George DywiliNo ratings yet

- Financial Statements 24 Questions AnswersDocument6 pagesFinancial Statements 24 Questions AnswersGideon Turner100% (2)

- 42-Shubham Hanbar-Sybaf A (Business Economics 2)Document11 pages42-Shubham Hanbar-Sybaf A (Business Economics 2)shubham hanbarNo ratings yet

- Solution Chapter 6 Financial Statements Pre Adjustments 1Document8 pagesSolution Chapter 6 Financial Statements Pre Adjustments 1IsmahNo ratings yet

- Consolidation MCQSDocument7 pagesConsolidation MCQSvyom rajNo ratings yet

- Pre IPO WhatsappDocument7 pagesPre IPO WhatsappviehnuhdjdhNo ratings yet

- VHINSON - Intermediate Accounting 3 (2023 - 2024 Edition) - 101Document1 pageVHINSON - Intermediate Accounting 3 (2023 - 2024 Edition) - 101Alyssa NacionNo ratings yet

- DCF Residential Training - 5may2017Document23 pagesDCF Residential Training - 5may2017Sarthak ShuklaNo ratings yet

- Accounting Eng ABDocument20 pagesAccounting Eng ABsajolramdaw1609No ratings yet

- Preparation Kit 2024 - IIM ShillongDocument129 pagesPreparation Kit 2024 - IIM ShillongBhagyashree MahajanNo ratings yet

- DCF and Pensions The Footnotes AnalystDocument10 pagesDCF and Pensions The Footnotes Analystmichael odiemboNo ratings yet

- 3.4 Final Accounts Balance Sheet (Statement of Financial Position)Document45 pages3.4 Final Accounts Balance Sheet (Statement of Financial Position)Magdalena NeuschitzerNo ratings yet

- Analysis SumsDocument11 pagesAnalysis SumsJessy NairNo ratings yet

- Chapter 8 Performance Measurement Evaluation Nov2020 1Document113 pagesChapter 8 Performance Measurement Evaluation Nov2020 1Question BankNo ratings yet