Download as docx, pdf, or txt

You might also like

- Minsupala Trading Corporation (Workbook)Document14 pagesMinsupala Trading Corporation (Workbook)Luis Melquiades P. Garcia100% (3)

- Name: Section: Score:: ActivityDocument3 pagesName: Section: Score:: ActivityRae Michael57% (7)

- Tugas P2-1A Dan P2-2A Peng - AkuntansiDocument5 pagesTugas P2-1A Dan P2-2A Peng - AkuntansiAlche MistNo ratings yet

- Act1111 Final ExamDocument7 pagesAct1111 Final ExamHaidee Flavier SabidoNo ratings yet

- Mythical Company Requirement A Debit CreditDocument3 pagesMythical Company Requirement A Debit CreditAnonn100% (1)

- HuaweiDocument78 pagesHuaweiAkumarc Kumar100% (2)

- Problem 9-1, 2 & 3Document3 pagesProblem 9-1, 2 & 3Micah April SabularseNo ratings yet

- MULTIPLE CHOICES-answer KeyDocument7 pagesMULTIPLE CHOICES-answer KeyLiaNo ratings yet

- Classroom Exercises On Receivables AnswersDocument4 pagesClassroom Exercises On Receivables AnswersJohn Cedfrey Narne100% (1)

- Problem 9-1,9-2,9-3Document3 pagesProblem 9-1,9-2,9-3Annabeth ChaseNo ratings yet

- Date Particulars Debit CreditDocument5 pagesDate Particulars Debit CreditToun MyNo ratings yet

- Pauline Anne R. Grana 11-ABM-A: To Record Purchase of Merchandise For CashDocument4 pagesPauline Anne R. Grana 11-ABM-A: To Record Purchase of Merchandise For CashPark EunbiNo ratings yet

- INTERMEDIATE ACCOUNTING 1 EditedDocument18 pagesINTERMEDIATE ACCOUNTING 1 EditedApril Mae LomboyNo ratings yet

- Activity 1Document2 pagesActivity 1Lhea VillanuevaNo ratings yet

- INTACC 3 Dilemma Company (Financial Position)Document1 pageINTACC 3 Dilemma Company (Financial Position)Ian SantosNo ratings yet

- IntAcc 1 by Valix 2023 Edition Answer Key From Chapter 4-14Document137 pagesIntAcc 1 by Valix 2023 Edition Answer Key From Chapter 4-14Bella Flair100% (1)

- Receivable FinancingDocument5 pagesReceivable FinancingAphol Joyce MortelNo ratings yet

- Updates - Midterm Lspu ExamDocument6 pagesUpdates - Midterm Lspu ExamAngelo HilomaNo ratings yet

- Statement of Financial PositionDocument2 pagesStatement of Financial PositionmoNo ratings yet

- 07 Receivable Financing 2 SolvingDocument3 pages07 Receivable Financing 2 Solvingkyle mandaresioNo ratings yet

- Name: Lecturer: Course Name: Course CodeDocument6 pagesName: Lecturer: Course Name: Course CodeJaredNo ratings yet

- IA 1 Valix 2020 Ver. Accounts ReceivableDocument8 pagesIA 1 Valix 2020 Ver. Accounts ReceivableAriean Joy DequiñaNo ratings yet

- Basic Accounting Midterm ExamDocument11 pagesBasic Accounting Midterm ExamC J A SNo ratings yet

- Problem SolvingDocument14 pagesProblem SolvingJericho EncarnacionNo ratings yet

- Tugas Akm 3Document1 pageTugas Akm 3cindyegaa27No ratings yet

- Part Ia Journal Entries - FarDocument5 pagesPart Ia Journal Entries - Farshe kioraNo ratings yet

- Problem 4Document6 pagesProblem 4Peachy Rose TorenaNo ratings yet

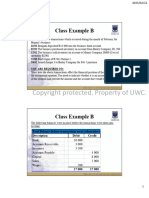

- Class Example B QuestionDocument1 pageClass Example B QuestionkeemorodriquezNo ratings yet

- Single Entry AccountingDocument12 pagesSingle Entry AccountingArjun ThawaniNo ratings yet

- Ap01 Cash To Accrual BasisDocument3 pagesAp01 Cash To Accrual BasisJean Fajardo BadilloNo ratings yet

- Bac 101Document6 pagesBac 101Ishak IshakNo ratings yet

- TASK #3 FarDocument8 pagesTASK #3 FarNicolle AmoyanNo ratings yet

- Quiz 4 FarDocument6 pagesQuiz 4 FarNicolle AmoyanNo ratings yet

- Questions On Preparation of Financial Statements 1-4Document4 pagesQuestions On Preparation of Financial Statements 1-4LaoneNo ratings yet

- Endngrsi - Akuntsi - Jurnal (2) NewDocument10 pagesEndngrsi - Akuntsi - Jurnal (2) NewMirzanun Nurul WakhidahNo ratings yet

- Activity 3-IntAcc1Document2 pagesActivity 3-IntAcc10322-1975No ratings yet

- Auditing Answers To ProblemDocument6 pagesAuditing Answers To ProblemAngela CondeNo ratings yet

- Cash Flow StatementDocument3 pagesCash Flow StatementanupsuchakNo ratings yet

- Pittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditDocument23 pagesPittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditAnonnNo ratings yet

- Unit III Partnership LiquidationDocument20 pagesUnit III Partnership LiquidationLeslie Mae Vargas ZafeNo ratings yet

- 05 Posting To LedgerDocument2 pages05 Posting To LedgerTrisha Mae BrazaNo ratings yet

- Assignment, ANdallo, Ransey Ace DDocument3 pagesAssignment, ANdallo, Ransey Ace DRansey Ace AndalloNo ratings yet

- Balance SheetDocument2 pagesBalance SheetKeight NuevaNo ratings yet

- Exercise 3-1Document4 pagesExercise 3-1Soo Tong JiangNo ratings yet

- FABM 2 HANDOUTS 1st QRTRDocument17 pagesFABM 2 HANDOUTS 1st QRTRDanise PorrasNo ratings yet

- Jawaban Soal, Akuntansi Menengah 1Document7 pagesJawaban Soal, Akuntansi Menengah 1Mira OktaviaNo ratings yet

- Merchandising Business - Sample Problem (Answers)Document4 pagesMerchandising Business - Sample Problem (Answers)Eana MabalotNo ratings yet

- Far 1Document2 pagesFar 1Stephanie Jane0% (1)

- Chapter 4 - Intermediate Accounting Volume 1Document8 pagesChapter 4 - Intermediate Accounting Volume 1Buenaventura, Elijah B.No ratings yet

- Date Account Title/Explanation PR Debit CreditDocument6 pagesDate Account Title/Explanation PR Debit CreditMarvin GwapoNo ratings yet

- Notes Receivable SampleDocument6 pagesNotes Receivable SamplekrizzmaaaayNo ratings yet

- A. 1a Problem 4Document1 pageA. 1a Problem 4shuzoNo ratings yet

- Accounts Paper 1 November 2008Document9 pagesAccounts Paper 1 November 2008Munashe BinhaNo ratings yet

- Morale Company Provided The Following Transactions:: University - Year 2 AccountingDocument2 pagesMorale Company Provided The Following Transactions:: University - Year 2 Accountingcollegestudent2000No ratings yet

- HW CH2Document3 pagesHW CH2Hà HoàngNo ratings yet

- Sample Worksheet K204050266 P3.5Document16 pagesSample Worksheet K204050266 P3.5Trâm Mai Thị ThùyNo ratings yet

- EnrichmentDocument2 pagesEnrichmentsabit.michelle0903No ratings yet

- HW2 - Ch2 The Recording Process NewDocument17 pagesHW2 - Ch2 The Recording Process Newvico lorenzoNo ratings yet

- CODE1Document7 pagesCODE1JF FNo ratings yet

- Using Economic Indicators to Improve Investment AnalysisFrom EverandUsing Economic Indicators to Improve Investment AnalysisRating: 3.5 out of 5 stars3.5/5 (1)

- Advising Entrepreneurs: Dynamic Strategies for Financial GrowthFrom EverandAdvising Entrepreneurs: Dynamic Strategies for Financial GrowthNo ratings yet

- Carlos Superdrug Corp. v. Department of Social Welfare and Development (DSWD)Document8 pagesCarlos Superdrug Corp. v. Department of Social Welfare and Development (DSWD)Stephanie Reyes GoNo ratings yet

- M Minervini Twitter NoteDocument1 pageM Minervini Twitter NoteLNo ratings yet

- IFMA FMLS SampleExcerpt PDFDocument17 pagesIFMA FMLS SampleExcerpt PDFsanthosh kumar t mNo ratings yet

- 2018-I PD5Document6 pages2018-I PD5magicNo ratings yet

- Reflection Paper: What Global Trade Deals Are Really About?Document1 pageReflection Paper: What Global Trade Deals Are Really About?Rodelia Adeva JaraNo ratings yet

- Managment Team StructureDocument2 pagesManagment Team StructureSandhea Suresh KumarNo ratings yet

- Philippine Corporate Law SyllabusDocument102 pagesPhilippine Corporate Law SyllabusRoa Emetrio NicoNo ratings yet

- CRM at FlipKartDocument8 pagesCRM at FlipKartSaloni Nanda100% (2)

- Statement of Account - 23 - 12 - 52Document3 pagesStatement of Account - 23 - 12 - 52Hamesh GavaliNo ratings yet

- Resume - CA Ajoy SharmaDocument2 pagesResume - CA Ajoy SharmaCA Ajoy SharmaNo ratings yet

- International Macroeconomics 4Th Edition Feenstra Test Bank Full Chapter PDFDocument54 pagesInternational Macroeconomics 4Th Edition Feenstra Test Bank Full Chapter PDFPatriciaSimonrdio100% (10)

- Current Assets and Non-Current Assets: Monday GroupDocument11 pagesCurrent Assets and Non-Current Assets: Monday GroupGJ BadenasNo ratings yet

- UK Food Retailing Industry'Document14 pagesUK Food Retailing Industry'u_upal50% (4)

- Nestle McsDocument14 pagesNestle Mcsprasanna_lad11100% (1)

- ADR and GDRDocument3 pagesADR and GDRJonney MarkNo ratings yet

- Some Common Types of Bill of LadingDocument2 pagesSome Common Types of Bill of LadingSoniya KhuramNo ratings yet

- Fibonacci Tool - How To UseDocument6 pagesFibonacci Tool - How To UseSaurabh DuaNo ratings yet

- Revenue Memorandum Circular No. 39-2007Document6 pagesRevenue Memorandum Circular No. 39-2007Charmaine GraceNo ratings yet

- List of Accounting StandardsDocument5 pagesList of Accounting StandardsPraneeth SaiNo ratings yet

- The Macroeconomic Environment For BusinessDocument18 pagesThe Macroeconomic Environment For BusinessAdriana ChiruNo ratings yet

- GardenDocument30 pagesGardenNilay JogadiaNo ratings yet

- Rehan Ahmad OriginalDocument3 pagesRehan Ahmad OriginalhsaifNo ratings yet

- 1996 - Yermack, D. - Higher Market Valuation of Companies With A Small Board of DirectorsDocument27 pages1996 - Yermack, D. - Higher Market Valuation of Companies With A Small Board of Directorsahmed sharkasNo ratings yet

- Impact of Capital Structure On ProfitabilityDocument264 pagesImpact of Capital Structure On ProfitabilityUsman AliNo ratings yet

- Training User Manual Transactions: A S - A Q O A R (AR)Document82 pagesTraining User Manual Transactions: A S - A Q O A R (AR)devender_bharatha3284No ratings yet

- Insurance AbbreviationsDocument4 pagesInsurance Abbreviationskumaryashwant1984No ratings yet

- A Comparative Study of Recruitment Process Between HDFC Bank and Sbi Bank at Moradabad RegionDocument86 pagesA Comparative Study of Recruitment Process Between HDFC Bank and Sbi Bank at Moradabad RegionbuddysmbdNo ratings yet

- Organization of The Instructor's Manual: PART ONE: IntroductionDocument36 pagesOrganization of The Instructor's Manual: PART ONE: Introductionkevinlopezwzdticmorx100% (37)

- Financial Statements: Class: Bsais 2ADocument12 pagesFinancial Statements: Class: Bsais 2AMadonna LuisNo ratings yet