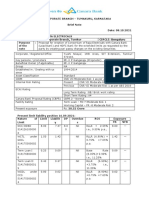

Loan Account Agreement

Loan Account Agreement

You might also like

- Temo Letlotlo GuidelinesDocument36 pagesTemo Letlotlo GuidelinesTiny Kepaletswe88% (8)

- (ENG Ver) POJK 35.POJK.05.2018 Tentang Penyelenggaraan Usaha Perusahaan Pembiayaan PDFDocument75 pages(ENG Ver) POJK 35.POJK.05.2018 Tentang Penyelenggaraan Usaha Perusahaan Pembiayaan PDFIndira S. Setyobudi25% (4)

- Credit Pitch Deck 1Document10 pagesCredit Pitch Deck 1Paul PoetNo ratings yet

- B - Letter 1 - 1st Dispute Letter To Pretend LenderDocument5 pagesB - Letter 1 - 1st Dispute Letter To Pretend Lenderbigwheel897% (35)

- Commercial Lending Training GuideDocument82 pagesCommercial Lending Training GuideSURAVARAPU PHANI KUMAR100% (1)

- The Ultimate Guide To P2P Lending PDFDocument112 pagesThe Ultimate Guide To P2P Lending PDFArthur Liew100% (1)

- Non-Negotiable Promissory NoteDocument2 pagesNon-Negotiable Promissory NoteaplawNo ratings yet

- Credit Appraisal System of Commercial Vehicle Loans.Document43 pagesCredit Appraisal System of Commercial Vehicle Loans.Pravin Kolpe92% (12)

- Loan Account Agreement-2Document12 pagesLoan Account Agreement-2Albert GarciaNo ratings yet

- 2Document11 pages2charlesgoodman010No ratings yet

- 10000001667Document79 pages10000001667Chapter 11 DocketsNo ratings yet

- Loan Documentation - 20231215065004Document13 pagesLoan Documentation - 20231215065004souljarsmile7No ratings yet

- Loan Agreement PDFDocument9 pagesLoan Agreement PDFHengki YonoNo ratings yet

- 2022-10-05T11 - 11 - 20 - LoanAgreement - 1123603 3Document9 pages2022-10-05T11 - 11 - 20 - LoanAgreement - 1123603 3Liliana MendozaNo ratings yet

- 2023-07-17T10 22 47 LoanAgreement 691671Document9 pages2023-07-17T10 22 47 LoanAgreement 691671juantirado0777No ratings yet

- Legal Funding DocumentDocument9 pagesLegal Funding DocumentheysamllpNo ratings yet

- AgreementDocument8 pagesAgreementsahupriyanshu9368No ratings yet

- TC Sky1p 007Document4 pagesTC Sky1p 0074gfswp95xjNo ratings yet

- Nm1-Cash Advance ContractDocument3 pagesNm1-Cash Advance Contractjohndoe6t9No ratings yet

- Promissory Note: BorrowerDocument3 pagesPromissory Note: BorrowerJerry GarqueNo ratings yet

- TC Sky1 062Document4 pagesTC Sky1 062jeffreygrimm8No ratings yet

- Payment AgreementDocument4 pagesPayment AgreementRocketLawyer100% (3)

- Cindi Hunter 2-1-2024Document3 pagesCindi Hunter 2-1-2024cindih763No ratings yet

- SignedDocument14 pagesSignedtrumpu01No ratings yet

- Bofa Qualified Written RequestDocument6 pagesBofa Qualified Written RequestDshane101100% (2)

- Promissory NoteDocument3 pagesPromissory NoteAlfredo Jr MallariNo ratings yet

- Promissory NoteDocument3 pagesPromissory NoteadamsamphiaNo ratings yet

- UntitledDocument4 pagesUntitledValecia G Wolf-RodriguezNo ratings yet

- PromissoryNoteSample November 2021 PDFDocument11 pagesPromissoryNoteSample November 2021 PDFrajputbhupendra787No ratings yet

- Robert KingDocument7 pagesRobert Kingrobert kingNo ratings yet

- Loan Agreement - Advance America LoansDocument4 pagesLoan Agreement - Advance America LoansadvanceamericainstacashNo ratings yet

- Loan Agreement - Ms. Renee WarrenDocument4 pagesLoan Agreement - Ms. Renee WarrenadvanceamericainstacashNo ratings yet

- MortgageLoanCommitmentMultiState Loan-23221843 Blanks EsignDocument3 pagesMortgageLoanCommitmentMultiState Loan-23221843 Blanks Esignalekseykarp32No ratings yet

- Ocwen Short Sale Approval (2nd Mortgage)Document6 pagesOcwen Short Sale Approval (2nd Mortgage)kwillsonNo ratings yet

- Proof of Claim by First Community BankDocument31 pagesProof of Claim by First Community BankbdcoryellNo ratings yet

- Power Point Report FinalDocument9 pagesPower Point Report FinalcecdeveraNo ratings yet

- Opensky Secured Visa Credit Card - Important Disclosures: Interest Rates and Interest ChargesDocument3 pagesOpensky Secured Visa Credit Card - Important Disclosures: Interest Rates and Interest ChargesTony SparksNo ratings yet

- Loan Agreement PDFDocument8 pagesLoan Agreement PDFWilletta KincaidNo ratings yet

- 2146749Document14 pages2146749Frank CasaleNo ratings yet

- 2023-10-23T13 28 20 LoanAgreement 1398970Document11 pages2023-10-23T13 28 20 LoanAgreement 1398970Michael BlamahNo ratings yet

- Schneider Sent First American A RESPA Qualified Written Request, Complaint, and Dispute of Debt and Validation of Debt LetterDocument9 pagesSchneider Sent First American A RESPA Qualified Written Request, Complaint, and Dispute of Debt and Validation of Debt Letterlarry-612445No ratings yet

- 5056896e-6bc1-404a-9a03-d464a2c2b647Document21 pages5056896e-6bc1-404a-9a03-d464a2c2b647sherrieNo ratings yet

- RESP A Qualified Written Request, Complaint, and Dispute of Debt and Validation of Debt LetterDocument9 pagesRESP A Qualified Written Request, Complaint, and Dispute of Debt and Validation of Debt Letterlarry-612445100% (1)

- Loan AgreementDocument5 pagesLoan AgreementAlice RomeroNo ratings yet

- Repayment ScheduleDocument2 pagesRepayment ScheduleCharina MiclatNo ratings yet

- Signed by Tracy Turner From IP: 98.215.10.60 at Thursday, December 02, 2010 11:51 AMDocument6 pagesSigned by Tracy Turner From IP: 98.215.10.60 at Thursday, December 02, 2010 11:51 AMTymon SwaqqCity ScottNo ratings yet

- Loan Agreement - Mr. Nick Jackson UpfrontDocument4 pagesLoan Agreement - Mr. Nick Jackson UpfrontadvanceamericainstacashNo ratings yet

- Loan Agreement - Ms - Zoiya Isaie Bank DepoDocument4 pagesLoan Agreement - Ms - Zoiya Isaie Bank DepoadvanceamericainstacashNo ratings yet

- Promissory NoteDocument3 pagesPromissory NoteInigo Cairo GabucanNo ratings yet

- Deed of Trust CATAYLODocument15 pagesDeed of Trust CATAYLOEL Filibusterisimo Paul CatayloNo ratings yet

- 308844contract SD3.00Document22 pages308844contract SD3.00Magnus AlbertNo ratings yet

- RepaymentSchedule 2Document2 pagesRepaymentSchedule 2Mae Ann GonzalesNo ratings yet

- Bank Authorization (BA) FormDocument4 pagesBank Authorization (BA) FormAilec FinancesNo ratings yet

- Upgrade - Personal Loans and CardsDocument3 pagesUpgrade - Personal Loans and CardsNina SerovaNo ratings yet

- Loan Agreement Paperwork of $5000.00Document8 pagesLoan Agreement Paperwork of $5000.00Alex SpecimenNo ratings yet

- Loan AgreementDocument2 pagesLoan AgreementTeresaNo ratings yet

- Repayment ScheduleDocument2 pagesRepayment ScheduleMaricris SerranoNo ratings yet

- Offer 16124750Document7 pagesOffer 16124750alyssa babylaiNo ratings yet

- Es Consumer Financing Agree PDFDocument1 pageEs Consumer Financing Agree PDFMylene Malayas PanganibanNo ratings yet

- Lend Him Money That He CanDocument2 pagesLend Him Money That He CanJade RarioNo ratings yet

- FijiFactSheet PLUnsecure CASE11880Document2 pagesFijiFactSheet PLUnsecure CASE11880Tamai Aisea AniseNo ratings yet

- FM-GSIS-OPS-PPL-02 - Optional Life Insurance Policy Loan Application - Rev2 - 10may2024Document2 pagesFM-GSIS-OPS-PPL-02 - Optional Life Insurance Policy Loan Application - Rev2 - 10may2024jenjen.sombiseNo ratings yet

- James WestDocument5 pagesJames Westflycody32No ratings yet

- Credit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsFrom EverandCredit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsNo ratings yet

- Chapter 20: Managing Credit Risk On The Balance SheetDocument17 pagesChapter 20: Managing Credit Risk On The Balance SheetAmmar Ali AyubNo ratings yet

- Cibil Report RAM BABU VISHWKARMA1579275405637Document7 pagesCibil Report RAM BABU VISHWKARMA1579275405637MONISH NAYAR100% (1)

- Security Analysis Chapter 10 Specific Standards For Bond InvestmentDocument2 pagesSecurity Analysis Chapter 10 Specific Standards For Bond InvestmentTheodor ToncaNo ratings yet

- Policy Manual: St. Martin of Tours Credit and Development CooperativeDocument7 pagesPolicy Manual: St. Martin of Tours Credit and Development CooperativePepito CruzNo ratings yet

- Chapter 1: Overview of Commercial Banks' Loans 1. Overview of Commercial BanksDocument10 pagesChapter 1: Overview of Commercial Banks' Loans 1. Overview of Commercial BanksHuỳnh Lữ Thị NhưNo ratings yet

- Raja Electricals Consortium Brief Note 08 10 2021Document3 pagesRaja Electricals Consortium Brief Note 08 10 2021MSME SULABH TUMAKURUNo ratings yet

- UniCreditUpdate2015RD (English) PDFDocument224 pagesUniCreditUpdate2015RD (English) PDFAuristene Dos Anjos CostaNo ratings yet

- Royal Wrist WatchDocument41 pagesRoyal Wrist Watchks95408503No ratings yet

- Entrepreneurship & Sources of Business FinanceDocument14 pagesEntrepreneurship & Sources of Business FinancePETER OTIENONo ratings yet

- Module IiDocument12 pagesModule IiArlan Joseph LopezNo ratings yet

- LOAN CLASSIFICATION For Report WorkDocument41 pagesLOAN CLASSIFICATION For Report WorkSuvro AvroNo ratings yet

- 24 XXX XXX TP Cibil ReportDocument3 pages24 XXX XXX TP Cibil ReportjansevakendranpnNo ratings yet

- Circular 257Document5 pagesCircular 257Carlos VelascoNo ratings yet

- Sacco Societies Act 2008Document139 pagesSacco Societies Act 2008James GikingoNo ratings yet

- IFC OTROSI Omnibus AgreementDocument50 pagesIFC OTROSI Omnibus AgreementMaria VelascoNo ratings yet

- CIBIL - Rani JaiswalDocument5 pagesCIBIL - Rani JaiswalAnkitNo ratings yet

- Verma Glass CoDocument8 pagesVerma Glass CoJai Bhushan BharmouriaNo ratings yet

- Elanjiyam Agro Services 15/A, South Street, Udayar Palayam, Ariyalur-612804Document11 pagesElanjiyam Agro Services 15/A, South Street, Udayar Palayam, Ariyalur-612804ramNo ratings yet

- Secretary's Certificate - Corporate Account Opening I Account Reactivation As of 06.2022Document5 pagesSecretary's Certificate - Corporate Account Opening I Account Reactivation As of 06.2022SUBSCRIPTION DEPARTMENTNo ratings yet

- Banking Theory and Practice Chapter FiveDocument23 pagesBanking Theory and Practice Chapter Fivemubarek oumerNo ratings yet

- uprtmt Qeourt: First DivisionDocument13 pagesuprtmt Qeourt: First DivisionEarl TabasuaresNo ratings yet

- Curran David Prom NoteDocument9 pagesCurran David Prom NotemikeNo ratings yet

- Effect of Bank Credit On Small Scale Entrepreneurial Development in NigeriaDocument59 pagesEffect of Bank Credit On Small Scale Entrepreneurial Development in NigeriaJoshua Ayomide OyadokunNo ratings yet

- NUANCES OF CHETTIAR FINANCING AT BRITISH MALAYA, Mid 1870's To Early 1890sDocument19 pagesNUANCES OF CHETTIAR FINANCING AT BRITISH MALAYA, Mid 1870's To Early 1890sManjeetNo ratings yet

Download as pdf or txt

You might also like

- Temo Letlotlo GuidelinesDocument36 pagesTemo Letlotlo GuidelinesTiny Kepaletswe88% (8)

- (ENG Ver) POJK 35.POJK.05.2018 Tentang Penyelenggaraan Usaha Perusahaan Pembiayaan PDFDocument75 pages(ENG Ver) POJK 35.POJK.05.2018 Tentang Penyelenggaraan Usaha Perusahaan Pembiayaan PDFIndira S. Setyobudi25% (4)

- Credit Pitch Deck 1Document10 pagesCredit Pitch Deck 1Paul PoetNo ratings yet

- B - Letter 1 - 1st Dispute Letter To Pretend LenderDocument5 pagesB - Letter 1 - 1st Dispute Letter To Pretend Lenderbigwheel897% (35)

- Commercial Lending Training GuideDocument82 pagesCommercial Lending Training GuideSURAVARAPU PHANI KUMAR100% (1)

- The Ultimate Guide To P2P Lending PDFDocument112 pagesThe Ultimate Guide To P2P Lending PDFArthur Liew100% (1)

- Non-Negotiable Promissory NoteDocument2 pagesNon-Negotiable Promissory NoteaplawNo ratings yet

- Credit Appraisal System of Commercial Vehicle Loans.Document43 pagesCredit Appraisal System of Commercial Vehicle Loans.Pravin Kolpe92% (12)

- Loan Account Agreement-2Document12 pagesLoan Account Agreement-2Albert GarciaNo ratings yet

- 2Document11 pages2charlesgoodman010No ratings yet

- 10000001667Document79 pages10000001667Chapter 11 DocketsNo ratings yet

- Loan Documentation - 20231215065004Document13 pagesLoan Documentation - 20231215065004souljarsmile7No ratings yet

- Loan Agreement PDFDocument9 pagesLoan Agreement PDFHengki YonoNo ratings yet

- 2022-10-05T11 - 11 - 20 - LoanAgreement - 1123603 3Document9 pages2022-10-05T11 - 11 - 20 - LoanAgreement - 1123603 3Liliana MendozaNo ratings yet

- 2023-07-17T10 22 47 LoanAgreement 691671Document9 pages2023-07-17T10 22 47 LoanAgreement 691671juantirado0777No ratings yet

- Legal Funding DocumentDocument9 pagesLegal Funding DocumentheysamllpNo ratings yet

- AgreementDocument8 pagesAgreementsahupriyanshu9368No ratings yet

- TC Sky1p 007Document4 pagesTC Sky1p 0074gfswp95xjNo ratings yet

- Nm1-Cash Advance ContractDocument3 pagesNm1-Cash Advance Contractjohndoe6t9No ratings yet

- Promissory Note: BorrowerDocument3 pagesPromissory Note: BorrowerJerry GarqueNo ratings yet

- TC Sky1 062Document4 pagesTC Sky1 062jeffreygrimm8No ratings yet

- Payment AgreementDocument4 pagesPayment AgreementRocketLawyer100% (3)

- Cindi Hunter 2-1-2024Document3 pagesCindi Hunter 2-1-2024cindih763No ratings yet

- SignedDocument14 pagesSignedtrumpu01No ratings yet

- Bofa Qualified Written RequestDocument6 pagesBofa Qualified Written RequestDshane101100% (2)

- Promissory NoteDocument3 pagesPromissory NoteAlfredo Jr MallariNo ratings yet

- Promissory NoteDocument3 pagesPromissory NoteadamsamphiaNo ratings yet

- UntitledDocument4 pagesUntitledValecia G Wolf-RodriguezNo ratings yet

- PromissoryNoteSample November 2021 PDFDocument11 pagesPromissoryNoteSample November 2021 PDFrajputbhupendra787No ratings yet

- Robert KingDocument7 pagesRobert Kingrobert kingNo ratings yet

- Loan Agreement - Advance America LoansDocument4 pagesLoan Agreement - Advance America LoansadvanceamericainstacashNo ratings yet

- Loan Agreement - Ms. Renee WarrenDocument4 pagesLoan Agreement - Ms. Renee WarrenadvanceamericainstacashNo ratings yet

- MortgageLoanCommitmentMultiState Loan-23221843 Blanks EsignDocument3 pagesMortgageLoanCommitmentMultiState Loan-23221843 Blanks Esignalekseykarp32No ratings yet

- Ocwen Short Sale Approval (2nd Mortgage)Document6 pagesOcwen Short Sale Approval (2nd Mortgage)kwillsonNo ratings yet

- Proof of Claim by First Community BankDocument31 pagesProof of Claim by First Community BankbdcoryellNo ratings yet

- Power Point Report FinalDocument9 pagesPower Point Report FinalcecdeveraNo ratings yet

- Opensky Secured Visa Credit Card - Important Disclosures: Interest Rates and Interest ChargesDocument3 pagesOpensky Secured Visa Credit Card - Important Disclosures: Interest Rates and Interest ChargesTony SparksNo ratings yet

- Loan Agreement PDFDocument8 pagesLoan Agreement PDFWilletta KincaidNo ratings yet

- 2146749Document14 pages2146749Frank CasaleNo ratings yet

- 2023-10-23T13 28 20 LoanAgreement 1398970Document11 pages2023-10-23T13 28 20 LoanAgreement 1398970Michael BlamahNo ratings yet

- Schneider Sent First American A RESPA Qualified Written Request, Complaint, and Dispute of Debt and Validation of Debt LetterDocument9 pagesSchneider Sent First American A RESPA Qualified Written Request, Complaint, and Dispute of Debt and Validation of Debt Letterlarry-612445No ratings yet

- 5056896e-6bc1-404a-9a03-d464a2c2b647Document21 pages5056896e-6bc1-404a-9a03-d464a2c2b647sherrieNo ratings yet

- RESP A Qualified Written Request, Complaint, and Dispute of Debt and Validation of Debt LetterDocument9 pagesRESP A Qualified Written Request, Complaint, and Dispute of Debt and Validation of Debt Letterlarry-612445100% (1)

- Loan AgreementDocument5 pagesLoan AgreementAlice RomeroNo ratings yet

- Repayment ScheduleDocument2 pagesRepayment ScheduleCharina MiclatNo ratings yet

- Signed by Tracy Turner From IP: 98.215.10.60 at Thursday, December 02, 2010 11:51 AMDocument6 pagesSigned by Tracy Turner From IP: 98.215.10.60 at Thursday, December 02, 2010 11:51 AMTymon SwaqqCity ScottNo ratings yet

- Loan Agreement - Mr. Nick Jackson UpfrontDocument4 pagesLoan Agreement - Mr. Nick Jackson UpfrontadvanceamericainstacashNo ratings yet

- Loan Agreement - Ms - Zoiya Isaie Bank DepoDocument4 pagesLoan Agreement - Ms - Zoiya Isaie Bank DepoadvanceamericainstacashNo ratings yet

- Promissory NoteDocument3 pagesPromissory NoteInigo Cairo GabucanNo ratings yet

- Deed of Trust CATAYLODocument15 pagesDeed of Trust CATAYLOEL Filibusterisimo Paul CatayloNo ratings yet

- 308844contract SD3.00Document22 pages308844contract SD3.00Magnus AlbertNo ratings yet

- RepaymentSchedule 2Document2 pagesRepaymentSchedule 2Mae Ann GonzalesNo ratings yet

- Bank Authorization (BA) FormDocument4 pagesBank Authorization (BA) FormAilec FinancesNo ratings yet

- Upgrade - Personal Loans and CardsDocument3 pagesUpgrade - Personal Loans and CardsNina SerovaNo ratings yet

- Loan Agreement Paperwork of $5000.00Document8 pagesLoan Agreement Paperwork of $5000.00Alex SpecimenNo ratings yet

- Loan AgreementDocument2 pagesLoan AgreementTeresaNo ratings yet

- Repayment ScheduleDocument2 pagesRepayment ScheduleMaricris SerranoNo ratings yet

- Offer 16124750Document7 pagesOffer 16124750alyssa babylaiNo ratings yet

- Es Consumer Financing Agree PDFDocument1 pageEs Consumer Financing Agree PDFMylene Malayas PanganibanNo ratings yet

- Lend Him Money That He CanDocument2 pagesLend Him Money That He CanJade RarioNo ratings yet

- FijiFactSheet PLUnsecure CASE11880Document2 pagesFijiFactSheet PLUnsecure CASE11880Tamai Aisea AniseNo ratings yet

- FM-GSIS-OPS-PPL-02 - Optional Life Insurance Policy Loan Application - Rev2 - 10may2024Document2 pagesFM-GSIS-OPS-PPL-02 - Optional Life Insurance Policy Loan Application - Rev2 - 10may2024jenjen.sombiseNo ratings yet

- James WestDocument5 pagesJames Westflycody32No ratings yet

- Credit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsFrom EverandCredit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsNo ratings yet

- Chapter 20: Managing Credit Risk On The Balance SheetDocument17 pagesChapter 20: Managing Credit Risk On The Balance SheetAmmar Ali AyubNo ratings yet

- Cibil Report RAM BABU VISHWKARMA1579275405637Document7 pagesCibil Report RAM BABU VISHWKARMA1579275405637MONISH NAYAR100% (1)

- Security Analysis Chapter 10 Specific Standards For Bond InvestmentDocument2 pagesSecurity Analysis Chapter 10 Specific Standards For Bond InvestmentTheodor ToncaNo ratings yet

- Policy Manual: St. Martin of Tours Credit and Development CooperativeDocument7 pagesPolicy Manual: St. Martin of Tours Credit and Development CooperativePepito CruzNo ratings yet

- Chapter 1: Overview of Commercial Banks' Loans 1. Overview of Commercial BanksDocument10 pagesChapter 1: Overview of Commercial Banks' Loans 1. Overview of Commercial BanksHuỳnh Lữ Thị NhưNo ratings yet

- Raja Electricals Consortium Brief Note 08 10 2021Document3 pagesRaja Electricals Consortium Brief Note 08 10 2021MSME SULABH TUMAKURUNo ratings yet

- UniCreditUpdate2015RD (English) PDFDocument224 pagesUniCreditUpdate2015RD (English) PDFAuristene Dos Anjos CostaNo ratings yet

- Royal Wrist WatchDocument41 pagesRoyal Wrist Watchks95408503No ratings yet

- Entrepreneurship & Sources of Business FinanceDocument14 pagesEntrepreneurship & Sources of Business FinancePETER OTIENONo ratings yet

- Module IiDocument12 pagesModule IiArlan Joseph LopezNo ratings yet

- LOAN CLASSIFICATION For Report WorkDocument41 pagesLOAN CLASSIFICATION For Report WorkSuvro AvroNo ratings yet

- 24 XXX XXX TP Cibil ReportDocument3 pages24 XXX XXX TP Cibil ReportjansevakendranpnNo ratings yet

- Circular 257Document5 pagesCircular 257Carlos VelascoNo ratings yet

- Sacco Societies Act 2008Document139 pagesSacco Societies Act 2008James GikingoNo ratings yet

- IFC OTROSI Omnibus AgreementDocument50 pagesIFC OTROSI Omnibus AgreementMaria VelascoNo ratings yet

- CIBIL - Rani JaiswalDocument5 pagesCIBIL - Rani JaiswalAnkitNo ratings yet

- Verma Glass CoDocument8 pagesVerma Glass CoJai Bhushan BharmouriaNo ratings yet

- Elanjiyam Agro Services 15/A, South Street, Udayar Palayam, Ariyalur-612804Document11 pagesElanjiyam Agro Services 15/A, South Street, Udayar Palayam, Ariyalur-612804ramNo ratings yet

- Secretary's Certificate - Corporate Account Opening I Account Reactivation As of 06.2022Document5 pagesSecretary's Certificate - Corporate Account Opening I Account Reactivation As of 06.2022SUBSCRIPTION DEPARTMENTNo ratings yet

- Banking Theory and Practice Chapter FiveDocument23 pagesBanking Theory and Practice Chapter Fivemubarek oumerNo ratings yet

- uprtmt Qeourt: First DivisionDocument13 pagesuprtmt Qeourt: First DivisionEarl TabasuaresNo ratings yet

- Curran David Prom NoteDocument9 pagesCurran David Prom NotemikeNo ratings yet

- Effect of Bank Credit On Small Scale Entrepreneurial Development in NigeriaDocument59 pagesEffect of Bank Credit On Small Scale Entrepreneurial Development in NigeriaJoshua Ayomide OyadokunNo ratings yet

- NUANCES OF CHETTIAR FINANCING AT BRITISH MALAYA, Mid 1870's To Early 1890sDocument19 pagesNUANCES OF CHETTIAR FINANCING AT BRITISH MALAYA, Mid 1870's To Early 1890sManjeetNo ratings yet