Sources of International Financing

Sources of International Financing

You might also like

- Solution Manual For Entrepreneurship Starting and Operating A Small Business 5th Edition Caroline Glackin Steve MariottiDocument18 pagesSolution Manual For Entrepreneurship Starting and Operating A Small Business 5th Edition Caroline Glackin Steve MariottiDeanBucktdjx100% (40)

- Adr, GDR - PPT Final by Pruthvi - PPT 24Document24 pagesAdr, GDR - PPT Final by Pruthvi - PPT 24Hemali MangrolaNo ratings yet

- Unit-6 International Sources of FinanceDocument12 pagesUnit-6 International Sources of FinanceShefali TailorNo ratings yet

- Law MantraDocument20 pagesLaw MantraSakshi JhaNo ratings yet

- Consumers and TravelersDocument11 pagesConsumers and TravelersRahul AnandNo ratings yet

- PA&FDocument31 pagesPA&FBharath NaniNo ratings yet

- ADR and GDRDocument3 pagesADR and GDRJonney MarkNo ratings yet

- DEC 2022 - International FinanceDocument10 pagesDEC 2022 - International FinanceindrakumarNo ratings yet

- Chapter 3Document21 pagesChapter 3Manjunath BVNo ratings yet

- External Sources of FinanceDocument3 pagesExternal Sources of FinanceAakash SablaniNo ratings yet

- Ways To Raise Finance From International MarketDocument7 pagesWays To Raise Finance From International Marketankitonway100% (1)

- Presentation By: Chaitra Datta Deepak Gayatri Hanumanth Harish Irfan ImranDocument39 pagesPresentation By: Chaitra Datta Deepak Gayatri Hanumanth Harish Irfan Imranaliaabid2012No ratings yet

- Difference Between GDR and IDRDocument18 pagesDifference Between GDR and IDRpriyanka chawlaNo ratings yet

- Assignment-2: Foreign Direct Investment (Fdi)Document11 pagesAssignment-2: Foreign Direct Investment (Fdi)Paramjeet SinghNo ratings yet

- Sources of International FinancingDocument6 pagesSources of International FinancingSabha Pathy100% (2)

- Financial Management Sessions - 11 - 24Document23 pagesFinancial Management Sessions - 11 - 24AshutoshNo ratings yet

- Foreign Capital and ForeignDocument11 pagesForeign Capital and Foreignalu_tNo ratings yet

- Financial Instruments Gdrs & P-Notes: Nilotpal DasDocument10 pagesFinancial Instruments Gdrs & P-Notes: Nilotpal Dasmokshgoyal2597No ratings yet

- BAJPAIYEE ASSIGNMNET Top 4 International Capital Market InstrumentsDocument21 pagesBAJPAIYEE ASSIGNMNET Top 4 International Capital Market InstrumentsRajat VermaNo ratings yet

- Adr GDRDocument7 pagesAdr GDRAnand SinghNo ratings yet

- CH 6 DRsDocument25 pagesCH 6 DRsNamrata NeopaneyNo ratings yet

- 4.modes of Raising Capital From Foreign MarketDocument16 pages4.modes of Raising Capital From Foreign MarketDr.R.Umamaheswari MBANo ratings yet

- Adr & GDRDocument6 pagesAdr & GDRJaikishan BiswalNo ratings yet

- FDI FII & International Finance ExamplesDocument21 pagesFDI FII & International Finance ExamplesgauravNo ratings yet

- Content: Definition: Global Depository Receipt (GDR) Procedure For Issue of GDR in A CompanyDocument29 pagesContent: Definition: Global Depository Receipt (GDR) Procedure For Issue of GDR in A CompanyVirendra JhaNo ratings yet

- Pallavithakur28064 AssignmentDocument12 pagesPallavithakur28064 AssignmentNoob DaddyNo ratings yet

- 1.3 Capital Market InstrumentsDocument17 pages1.3 Capital Market InstrumentsRajat GuptaNo ratings yet

- Foreign Institutional Investors and Depository ReceiptsDocument45 pagesForeign Institutional Investors and Depository Receiptssunitha2No ratings yet

- Week 4Document6 pagesWeek 4Alma UriasNo ratings yet

- Foreign Exchange and MarketDocument16 pagesForeign Exchange and MarketPrathap PratapNo ratings yet

- Market Participants in Securities MarketDocument11 pagesMarket Participants in Securities MarketSandra PhilipNo ratings yet

- Forex Reserves in India: Sources of Forex ReserveDocument8 pagesForex Reserves in India: Sources of Forex ReserveAbhijeet PatilNo ratings yet

- What Is A Multinational Corporation?: A Corporation That Operates in Two or More CountriesDocument43 pagesWhat Is A Multinational Corporation?: A Corporation That Operates in Two or More CountriesSudhanshu SharmaNo ratings yet

- SAPM - Notes-1 PDFDocument9 pagesSAPM - Notes-1 PDFSanjay YadavNo ratings yet

- Euro Issues & GdrsDocument25 pagesEuro Issues & Gdrsvred4uNo ratings yet

- Depository Receipts in India: With A Special Reference To Indian Depository ReceiptsDocument18 pagesDepository Receipts in India: With A Special Reference To Indian Depository Receiptsnikhil rajpurohitNo ratings yet

- Finanical ProductsDocument19 pagesFinanical ProductsHarpreet KaurNo ratings yet

- Depository Receipts PrimerDocument5 pagesDepository Receipts PrimerAstrologer GuruNo ratings yet

- American Depository Receipts (Adr) & Global Depository Receipts (GDR)Document6 pagesAmerican Depository Receipts (Adr) & Global Depository Receipts (GDR)Sanjeet MohantyNo ratings yet

- Master of Business Administration 42Document7 pagesMaster of Business Administration 42ali_rahim1988No ratings yet

- Foreign Direct Investment (Fdi), Foreign Institutional Investment (Fiis) and International Financial ManagementDocument15 pagesForeign Direct Investment (Fdi), Foreign Institutional Investment (Fiis) and International Financial ManagementcasarokarNo ratings yet

- Foreig BNGHGFHGN Capital and Foreign (1) Economic............Document18 pagesForeig BNGHGFHGN Capital and Foreign (1) Economic............Jerome RandolphNo ratings yet

- SMO Unit-Iv Adr, Fdi, GDR, Fii, Euro IssueDocument6 pagesSMO Unit-Iv Adr, Fdi, GDR, Fii, Euro IssueSANGITA ACHARYANo ratings yet

- Depository Receipts: Adr, GDR, Idr Benefits To Different Stake HoldersDocument10 pagesDepository Receipts: Adr, GDR, Idr Benefits To Different Stake HoldersVijai AnandNo ratings yet

- Financing International OperationsDocument16 pagesFinancing International OperationsVikash ShawNo ratings yet

- CA Final Strategic Financial Management, Paper 2 Chapter 11 CA Tarun MahajanDocument32 pagesCA Final Strategic Financial Management, Paper 2 Chapter 11 CA Tarun MahajanPrasanni RaoNo ratings yet

- International InvestmentsDocument4 pagesInternational InvestmentsMehak joshiNo ratings yet

- Ib PPT by Mayur 3525Document11 pagesIb PPT by Mayur 3525rockybalboadiditNo ratings yet

- Foreign Direct Investment (FDI) Refers ToDocument4 pagesForeign Direct Investment (FDI) Refers ToNilava DasNo ratings yet

- Financial Services 1Document42 pagesFinancial Services 1Uma NNo ratings yet

- International Banking and Foreign Exchange ManagementDocument7 pagesInternational Banking and Foreign Exchange ManagementSolve AssignmentNo ratings yet

- International FinanceDocument11 pagesInternational Financerohit chaudharyNo ratings yet

- Securities LawDocument10 pagesSecurities LawKonnoju ShivasreeNo ratings yet

- Foreign Sources of FinanceDocument14 pagesForeign Sources of FinancechandnidevaniNo ratings yet

- Introduction To The StudyDocument41 pagesIntroduction To The StudyUllas MarvilNo ratings yet

- Multilateral InstnDocument6 pagesMultilateral InstnGada DivyaNo ratings yet

- Sovereign Rating (Aamir Nabi) : Sovereign Credit Ratings in The EurozoneDocument25 pagesSovereign Rating (Aamir Nabi) : Sovereign Credit Ratings in The EurozoneDaheem AminNo ratings yet

- Term Paper-Business Environment Topic:Foreign Institution InvestmentDocument29 pagesTerm Paper-Business Environment Topic:Foreign Institution InvestmentRahul TargotraNo ratings yet

- Modes To Raise Foreign FundsDocument14 pagesModes To Raise Foreign FundsVishakha SuriNo ratings yet

- A Practical Approach to the Study of Indian Capital MarketsFrom EverandA Practical Approach to the Study of Indian Capital MarketsNo ratings yet

- Understanding Shelf OfferingsDocument27 pagesUnderstanding Shelf Offeringsscd9750No ratings yet

- Kotak PMS Special Situations Value Presentation - Jan 18Document36 pagesKotak PMS Special Situations Value Presentation - Jan 18kanna275No ratings yet

- 1191 Six Rules For Investing in StocksDocument21 pages1191 Six Rules For Investing in StocksMaso berfaedah100% (6)

- Quarz Capital Management CSE Global Presentation FINAL 26th Feb 2018Document23 pagesQuarz Capital Management CSE Global Presentation FINAL 26th Feb 2018pmoerzhNo ratings yet

- Chapter 7 - Cash Flow AnalysisDocument18 pagesChapter 7 - Cash Flow AnalysisulfaNo ratings yet

- Nov 10Document7 pagesNov 10chandreshNo ratings yet

- MBAC 6060 Chapter 5Document53 pagesMBAC 6060 Chapter 5Christy AngkouwNo ratings yet

- CH 01Document77 pagesCH 01Ngoc PhamNo ratings yet

- Exicomdrhp 20231003123506Document471 pagesExicomdrhp 20231003123506C GauravNo ratings yet

- Portfolio Investment ManagementDocument242 pagesPortfolio Investment ManagementFishah Sadri100% (5)

- Reviewer On Partnership AccountingDocument27 pagesReviewer On Partnership AccountingannegelieNo ratings yet

- Closure - Form Ver 1.1-201802221526458136617Document1 pageClosure - Form Ver 1.1-201802221526458136617Anshuman SinghNo ratings yet

- Beams11 ppt09Document19 pagesBeams11 ppt09Mario RosaNo ratings yet

- International Business AssignmentDocument5 pagesInternational Business Assignmentkanika joshiNo ratings yet

- Acc 325 Ch. 8 AnswersDocument10 pagesAcc 325 Ch. 8 AnswersMohammad WaleedNo ratings yet

- Long-Term Assets I: Property Plant, and EquipmentDocument13 pagesLong-Term Assets I: Property Plant, and EquipmentErjan BhaehakiNo ratings yet

- KSE Listing Regulations (Notes)Document5 pagesKSE Listing Regulations (Notes)araza_962307No ratings yet

- Bus Alevel Aqa Calccards SampleDocument11 pagesBus Alevel Aqa Calccards Sampletalha ubaidNo ratings yet

- Security Analysis Portfolio Management AssignmentDocument4 pagesSecurity Analysis Portfolio Management AssignmentNidhi ShahNo ratings yet

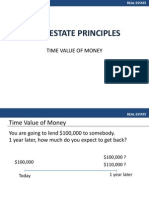

- Time Value of MoneyDocument32 pagesTime Value of MoneyChristian WashingtonNo ratings yet

- CV-8-Abdul Mohaimin Patwary PDFDocument3 pagesCV-8-Abdul Mohaimin Patwary PDFMohaimin PatwaryNo ratings yet

- Financial Management Week 2 AssignmentDocument2 pagesFinancial Management Week 2 AssignmentAndrea Monique AlejagaNo ratings yet

- Intermediate Examination: Suggested Answers To QuestionsDocument16 pagesIntermediate Examination: Suggested Answers To QuestionsDINESH K SADAYAKUMARNo ratings yet

- Board Question Paper: September 2021: Book Keeping & AccountancyDocument5 pagesBoard Question Paper: September 2021: Book Keeping & AccountancyPriyansh ShahNo ratings yet

- Chap 12Document23 pagesChap 12Maria SyNo ratings yet

- HU501 Economics For EngineersDocument1 pageHU501 Economics For EngineersMyWBUT - Home for Engineers33% (3)

- Loyal VC - Brief and Invite DetailsDocument1 pageLoyal VC - Brief and Invite DetailsmchroNo ratings yet

- Sol. Man. - Chapter 11 - Investments - Additional ConceptsDocument10 pagesSol. Man. - Chapter 11 - Investments - Additional ConceptsKaisser Niel Mari FormentoNo ratings yet

- S Z C I S ..................................................................................................................... 12Document15 pagesS Z C I S ..................................................................................................................... 12darkheart_29No ratings yet

Download as pdf or txt

You might also like

- Solution Manual For Entrepreneurship Starting and Operating A Small Business 5th Edition Caroline Glackin Steve MariottiDocument18 pagesSolution Manual For Entrepreneurship Starting and Operating A Small Business 5th Edition Caroline Glackin Steve MariottiDeanBucktdjx100% (40)

- Adr, GDR - PPT Final by Pruthvi - PPT 24Document24 pagesAdr, GDR - PPT Final by Pruthvi - PPT 24Hemali MangrolaNo ratings yet

- Unit-6 International Sources of FinanceDocument12 pagesUnit-6 International Sources of FinanceShefali TailorNo ratings yet

- Law MantraDocument20 pagesLaw MantraSakshi JhaNo ratings yet

- Consumers and TravelersDocument11 pagesConsumers and TravelersRahul AnandNo ratings yet

- PA&FDocument31 pagesPA&FBharath NaniNo ratings yet

- ADR and GDRDocument3 pagesADR and GDRJonney MarkNo ratings yet

- DEC 2022 - International FinanceDocument10 pagesDEC 2022 - International FinanceindrakumarNo ratings yet

- Chapter 3Document21 pagesChapter 3Manjunath BVNo ratings yet

- External Sources of FinanceDocument3 pagesExternal Sources of FinanceAakash SablaniNo ratings yet

- Ways To Raise Finance From International MarketDocument7 pagesWays To Raise Finance From International Marketankitonway100% (1)

- Presentation By: Chaitra Datta Deepak Gayatri Hanumanth Harish Irfan ImranDocument39 pagesPresentation By: Chaitra Datta Deepak Gayatri Hanumanth Harish Irfan Imranaliaabid2012No ratings yet

- Difference Between GDR and IDRDocument18 pagesDifference Between GDR and IDRpriyanka chawlaNo ratings yet

- Assignment-2: Foreign Direct Investment (Fdi)Document11 pagesAssignment-2: Foreign Direct Investment (Fdi)Paramjeet SinghNo ratings yet

- Sources of International FinancingDocument6 pagesSources of International FinancingSabha Pathy100% (2)

- Financial Management Sessions - 11 - 24Document23 pagesFinancial Management Sessions - 11 - 24AshutoshNo ratings yet

- Foreign Capital and ForeignDocument11 pagesForeign Capital and Foreignalu_tNo ratings yet

- Financial Instruments Gdrs & P-Notes: Nilotpal DasDocument10 pagesFinancial Instruments Gdrs & P-Notes: Nilotpal Dasmokshgoyal2597No ratings yet

- BAJPAIYEE ASSIGNMNET Top 4 International Capital Market InstrumentsDocument21 pagesBAJPAIYEE ASSIGNMNET Top 4 International Capital Market InstrumentsRajat VermaNo ratings yet

- Adr GDRDocument7 pagesAdr GDRAnand SinghNo ratings yet

- CH 6 DRsDocument25 pagesCH 6 DRsNamrata NeopaneyNo ratings yet

- 4.modes of Raising Capital From Foreign MarketDocument16 pages4.modes of Raising Capital From Foreign MarketDr.R.Umamaheswari MBANo ratings yet

- Adr & GDRDocument6 pagesAdr & GDRJaikishan BiswalNo ratings yet

- FDI FII & International Finance ExamplesDocument21 pagesFDI FII & International Finance ExamplesgauravNo ratings yet

- Content: Definition: Global Depository Receipt (GDR) Procedure For Issue of GDR in A CompanyDocument29 pagesContent: Definition: Global Depository Receipt (GDR) Procedure For Issue of GDR in A CompanyVirendra JhaNo ratings yet

- Pallavithakur28064 AssignmentDocument12 pagesPallavithakur28064 AssignmentNoob DaddyNo ratings yet

- 1.3 Capital Market InstrumentsDocument17 pages1.3 Capital Market InstrumentsRajat GuptaNo ratings yet

- Foreign Institutional Investors and Depository ReceiptsDocument45 pagesForeign Institutional Investors and Depository Receiptssunitha2No ratings yet

- Week 4Document6 pagesWeek 4Alma UriasNo ratings yet

- Foreign Exchange and MarketDocument16 pagesForeign Exchange and MarketPrathap PratapNo ratings yet

- Market Participants in Securities MarketDocument11 pagesMarket Participants in Securities MarketSandra PhilipNo ratings yet

- Forex Reserves in India: Sources of Forex ReserveDocument8 pagesForex Reserves in India: Sources of Forex ReserveAbhijeet PatilNo ratings yet

- What Is A Multinational Corporation?: A Corporation That Operates in Two or More CountriesDocument43 pagesWhat Is A Multinational Corporation?: A Corporation That Operates in Two or More CountriesSudhanshu SharmaNo ratings yet

- SAPM - Notes-1 PDFDocument9 pagesSAPM - Notes-1 PDFSanjay YadavNo ratings yet

- Euro Issues & GdrsDocument25 pagesEuro Issues & Gdrsvred4uNo ratings yet

- Depository Receipts in India: With A Special Reference To Indian Depository ReceiptsDocument18 pagesDepository Receipts in India: With A Special Reference To Indian Depository Receiptsnikhil rajpurohitNo ratings yet

- Finanical ProductsDocument19 pagesFinanical ProductsHarpreet KaurNo ratings yet

- Depository Receipts PrimerDocument5 pagesDepository Receipts PrimerAstrologer GuruNo ratings yet

- American Depository Receipts (Adr) & Global Depository Receipts (GDR)Document6 pagesAmerican Depository Receipts (Adr) & Global Depository Receipts (GDR)Sanjeet MohantyNo ratings yet

- Master of Business Administration 42Document7 pagesMaster of Business Administration 42ali_rahim1988No ratings yet

- Foreign Direct Investment (Fdi), Foreign Institutional Investment (Fiis) and International Financial ManagementDocument15 pagesForeign Direct Investment (Fdi), Foreign Institutional Investment (Fiis) and International Financial ManagementcasarokarNo ratings yet

- Foreig BNGHGFHGN Capital and Foreign (1) Economic............Document18 pagesForeig BNGHGFHGN Capital and Foreign (1) Economic............Jerome RandolphNo ratings yet

- SMO Unit-Iv Adr, Fdi, GDR, Fii, Euro IssueDocument6 pagesSMO Unit-Iv Adr, Fdi, GDR, Fii, Euro IssueSANGITA ACHARYANo ratings yet

- Depository Receipts: Adr, GDR, Idr Benefits To Different Stake HoldersDocument10 pagesDepository Receipts: Adr, GDR, Idr Benefits To Different Stake HoldersVijai AnandNo ratings yet

- Financing International OperationsDocument16 pagesFinancing International OperationsVikash ShawNo ratings yet

- CA Final Strategic Financial Management, Paper 2 Chapter 11 CA Tarun MahajanDocument32 pagesCA Final Strategic Financial Management, Paper 2 Chapter 11 CA Tarun MahajanPrasanni RaoNo ratings yet

- International InvestmentsDocument4 pagesInternational InvestmentsMehak joshiNo ratings yet

- Ib PPT by Mayur 3525Document11 pagesIb PPT by Mayur 3525rockybalboadiditNo ratings yet

- Foreign Direct Investment (FDI) Refers ToDocument4 pagesForeign Direct Investment (FDI) Refers ToNilava DasNo ratings yet

- Financial Services 1Document42 pagesFinancial Services 1Uma NNo ratings yet

- International Banking and Foreign Exchange ManagementDocument7 pagesInternational Banking and Foreign Exchange ManagementSolve AssignmentNo ratings yet

- International FinanceDocument11 pagesInternational Financerohit chaudharyNo ratings yet

- Securities LawDocument10 pagesSecurities LawKonnoju ShivasreeNo ratings yet

- Foreign Sources of FinanceDocument14 pagesForeign Sources of FinancechandnidevaniNo ratings yet

- Introduction To The StudyDocument41 pagesIntroduction To The StudyUllas MarvilNo ratings yet

- Multilateral InstnDocument6 pagesMultilateral InstnGada DivyaNo ratings yet

- Sovereign Rating (Aamir Nabi) : Sovereign Credit Ratings in The EurozoneDocument25 pagesSovereign Rating (Aamir Nabi) : Sovereign Credit Ratings in The EurozoneDaheem AminNo ratings yet

- Term Paper-Business Environment Topic:Foreign Institution InvestmentDocument29 pagesTerm Paper-Business Environment Topic:Foreign Institution InvestmentRahul TargotraNo ratings yet

- Modes To Raise Foreign FundsDocument14 pagesModes To Raise Foreign FundsVishakha SuriNo ratings yet

- A Practical Approach to the Study of Indian Capital MarketsFrom EverandA Practical Approach to the Study of Indian Capital MarketsNo ratings yet

- Understanding Shelf OfferingsDocument27 pagesUnderstanding Shelf Offeringsscd9750No ratings yet

- Kotak PMS Special Situations Value Presentation - Jan 18Document36 pagesKotak PMS Special Situations Value Presentation - Jan 18kanna275No ratings yet

- 1191 Six Rules For Investing in StocksDocument21 pages1191 Six Rules For Investing in StocksMaso berfaedah100% (6)

- Quarz Capital Management CSE Global Presentation FINAL 26th Feb 2018Document23 pagesQuarz Capital Management CSE Global Presentation FINAL 26th Feb 2018pmoerzhNo ratings yet

- Chapter 7 - Cash Flow AnalysisDocument18 pagesChapter 7 - Cash Flow AnalysisulfaNo ratings yet

- Nov 10Document7 pagesNov 10chandreshNo ratings yet

- MBAC 6060 Chapter 5Document53 pagesMBAC 6060 Chapter 5Christy AngkouwNo ratings yet

- CH 01Document77 pagesCH 01Ngoc PhamNo ratings yet

- Exicomdrhp 20231003123506Document471 pagesExicomdrhp 20231003123506C GauravNo ratings yet

- Portfolio Investment ManagementDocument242 pagesPortfolio Investment ManagementFishah Sadri100% (5)

- Reviewer On Partnership AccountingDocument27 pagesReviewer On Partnership AccountingannegelieNo ratings yet

- Closure - Form Ver 1.1-201802221526458136617Document1 pageClosure - Form Ver 1.1-201802221526458136617Anshuman SinghNo ratings yet

- Beams11 ppt09Document19 pagesBeams11 ppt09Mario RosaNo ratings yet

- International Business AssignmentDocument5 pagesInternational Business Assignmentkanika joshiNo ratings yet

- Acc 325 Ch. 8 AnswersDocument10 pagesAcc 325 Ch. 8 AnswersMohammad WaleedNo ratings yet

- Long-Term Assets I: Property Plant, and EquipmentDocument13 pagesLong-Term Assets I: Property Plant, and EquipmentErjan BhaehakiNo ratings yet

- KSE Listing Regulations (Notes)Document5 pagesKSE Listing Regulations (Notes)araza_962307No ratings yet

- Bus Alevel Aqa Calccards SampleDocument11 pagesBus Alevel Aqa Calccards Sampletalha ubaidNo ratings yet

- Security Analysis Portfolio Management AssignmentDocument4 pagesSecurity Analysis Portfolio Management AssignmentNidhi ShahNo ratings yet

- Time Value of MoneyDocument32 pagesTime Value of MoneyChristian WashingtonNo ratings yet

- CV-8-Abdul Mohaimin Patwary PDFDocument3 pagesCV-8-Abdul Mohaimin Patwary PDFMohaimin PatwaryNo ratings yet

- Financial Management Week 2 AssignmentDocument2 pagesFinancial Management Week 2 AssignmentAndrea Monique AlejagaNo ratings yet

- Intermediate Examination: Suggested Answers To QuestionsDocument16 pagesIntermediate Examination: Suggested Answers To QuestionsDINESH K SADAYAKUMARNo ratings yet

- Board Question Paper: September 2021: Book Keeping & AccountancyDocument5 pagesBoard Question Paper: September 2021: Book Keeping & AccountancyPriyansh ShahNo ratings yet

- Chap 12Document23 pagesChap 12Maria SyNo ratings yet

- HU501 Economics For EngineersDocument1 pageHU501 Economics For EngineersMyWBUT - Home for Engineers33% (3)

- Loyal VC - Brief and Invite DetailsDocument1 pageLoyal VC - Brief and Invite DetailsmchroNo ratings yet

- Sol. Man. - Chapter 11 - Investments - Additional ConceptsDocument10 pagesSol. Man. - Chapter 11 - Investments - Additional ConceptsKaisser Niel Mari FormentoNo ratings yet

- S Z C I S ..................................................................................................................... 12Document15 pagesS Z C I S ..................................................................................................................... 12darkheart_29No ratings yet