Download as docx, pdf, or txt

You might also like

- Principles of Auditing An Introduction To International Standards On Auditing 3rd Edition Hayes Solu 190402061241Document32 pagesPrinciples of Auditing An Introduction To International Standards On Auditing 3rd Edition Hayes Solu 190402061241Nia100% (2)

- #Financial Management and Debt Control in Public EnterprisesDocument54 pages#Financial Management and Debt Control in Public EnterprisesD J Ben Uzee100% (2)

- Principles of Auditing An Introduction To International Standards On Auditing 3rd Edition Hayes Solutions ManualDocument25 pagesPrinciples of Auditing An Introduction To International Standards On Auditing 3rd Edition Hayes Solutions ManualSherryWalkerozfk98% (59)

- Computerized Transcript Management SystemDocument32 pagesComputerized Transcript Management SystemSolomon olorunlekeNo ratings yet

- Progress Test 1Document6 pagesProgress Test 1tho1009No ratings yet

- Internal Audit Report TemplateDocument17 pagesInternal Audit Report TemplateAsfin Achfani Nur100% (7)

- Managerial Accounting Course OutlineDocument4 pagesManagerial Accounting Course OutlineASMARA HABIB100% (1)

- An Empirical Analysis of The Values of Accounting Information System in An OrganizationDocument15 pagesAn Empirical Analysis of The Values of Accounting Information System in An Organizationasif chowdhuryNo ratings yet

- Mercy JosephDocument59 pagesMercy JosephvinjoecomNo ratings yet

- The Effect of Computer Assisted Audit TeDocument80 pagesThe Effect of Computer Assisted Audit TeRochelle HullezaNo ratings yet

- My Proposal ReaserchDocument24 pagesMy Proposal ReaserchAbdulhamid MustefaNo ratings yet

- Anty Ogaku Preliminary PagesDocument10 pagesAnty Ogaku Preliminary Pagesibrodan681No ratings yet

- Impact of Bank Failure On The Economy of Nigeria. A Case Study of Savannah BankDocument7 pagesImpact of Bank Failure On The Economy of Nigeria. A Case Study of Savannah Bankawom christopher bernardNo ratings yet

- Inventory Management As A Panacea Towards Organization ProfitabilityDocument72 pagesInventory Management As A Panacea Towards Organization ProfitabilityUsman SemiuNo ratings yet

- Effectiveness of Inventory Management in A Manufacturing CompanyDocument81 pagesEffectiveness of Inventory Management in A Manufacturing CompanyAdefila Sunday DadaNo ratings yet

- Assessement of Treasury Single Account On Deposit Money Bank PerformanceDocument4 pagesAssessement of Treasury Single Account On Deposit Money Bank PerformanceUmar Farouq Mohammed GalibNo ratings yet

- An Assessment of The Impact of Non-Monetary Incentives On Employees Performance A Study of Nigerian Communication Commission NCCDocument106 pagesAn Assessment of The Impact of Non-Monetary Incentives On Employees Performance A Study of Nigerian Communication Commission NCCplaycharles89No ratings yet

- ApprovalDocument6 pagesApprovalalexNo ratings yet

- Ahmde BUS CompletedDocument117 pagesAhmde BUS CompletedDANJUMA ADAMUNo ratings yet

- Khadija ProjectDocument56 pagesKhadija ProjectSALISU SULEIMAN SHAMAKINo ratings yet

- Cost Accounting PrinciplesDocument59 pagesCost Accounting PrinciplesToluNo ratings yet

- Caroline Esheya ProjectDocument88 pagesCaroline Esheya ProjectEphraim EkpoNo ratings yet

- Brooks Cover PagesDocument13 pagesBrooks Cover PagesFaith MoneyNo ratings yet

- Corporate Governance in Nigerian Universities, A Study of Financial Management in UnnDocument123 pagesCorporate Governance in Nigerian Universities, A Study of Financial Management in UnnEmmanuel KingsNo ratings yet

- AEV Amended CG Manual 2022 Amendments FinalDocument56 pagesAEV Amended CG Manual 2022 Amendments FinalYna Beatriz BocayaNo ratings yet

- Ugorume Moses ProjectDocument61 pagesUgorume Moses ProjectShaguolo O. JosephNo ratings yet

- Effect of Record Management On Efficiency of Office ManagersDocument65 pagesEffect of Record Management On Efficiency of Office ManagersmarydreNo ratings yet

- AuditingDocument92 pagesAuditingyared100% (1)

- CORRECTIONS THE IMPACT OF INTERNAL CONTROL SYSTEMDocument17 pagesCORRECTIONS THE IMPACT OF INTERNAL CONTROL SYSTEMclintonugorji7No ratings yet

- Design and Implementation of An Automated Inventory Control System For A Manufacturing OrganisationDocument86 pagesDesign and Implementation of An Automated Inventory Control System For A Manufacturing OrganisationIyere Gift100% (1)

- An Evaluation of Budgeting and Budgetary Control in Brewery IndustryDocument16 pagesAn Evaluation of Budgeting and Budgetary Control in Brewery IndustryPavithra GowthamNo ratings yet

- An Assessment of BudgetingDocument46 pagesAn Assessment of BudgetingjobademuNo ratings yet

- Effect of Federal Government Capital Expenditure On The Nigerian Economic GrowthDocument112 pagesEffect of Federal Government Capital Expenditure On The Nigerian Economic GrowthFelix AkanniNo ratings yet

- Amina Salmanu PRJTDocument50 pagesAmina Salmanu PRJTAbouberker SirdeequeNo ratings yet

- Effectiveness of Inventory Management in A Manufacturing CompanyDocument81 pagesEffectiveness of Inventory Management in A Manufacturing CompanyShaguolo O. Joseph100% (1)

- A Review of The Effect of Efficient Treasury Management On ProfitabilityDocument43 pagesA Review of The Effect of Efficient Treasury Management On ProfitabilityOgunwa GeraldNo ratings yet

- Analyzing Differences in Auditing Between Public and Private EnterprisesDocument62 pagesAnalyzing Differences in Auditing Between Public and Private Enterprisesoscu0802No ratings yet

- Derick ProjectDocument133 pagesDerick ProjectFaith MoneyNo ratings yet

- AJUMUKA SUNDAY PRJCT CompletedDocument97 pagesAJUMUKA SUNDAY PRJCT CompletedFaith MoneyNo ratings yet

- The Role of Corporate Social Responsibility in The Development of SocietyDocument46 pagesThe Role of Corporate Social Responsibility in The Development of SocietyYahya MusaNo ratings yet

- 2004 Guidance Doc For SA8000Document88 pages2004 Guidance Doc For SA8000jiaolei9848No ratings yet

- The Role of Accounting Information in Management Decision MakingDocument8 pagesThe Role of Accounting Information in Management Decision MakingEmesiani TobennaNo ratings yet

- GNIA TelecomDocument159 pagesGNIA TelecomPeachyNo ratings yet

- AUE Study Guide 001 - 2020 - 4 - BDocument170 pagesAUE Study Guide 001 - 2020 - 4 - BLindelwe NeneNo ratings yet

- Revenue App For KekeDocument50 pagesRevenue App For KekerabiusaliskhalidNo ratings yet

- Ap 34PW-1 PDFDocument1 pageAp 34PW-1 PDFRyan PelitoNo ratings yet

- Project 1Document76 pagesProject 1hassan mamudNo ratings yet

- Guidance Document For Social AccountabilityDocument176 pagesGuidance Document For Social AccountabilitytamasraduNo ratings yet

- Govt. Policies NigeriaDocument74 pagesGovt. Policies NigeriaSoham Sinha0% (1)

- Acrobat Document 5Document182 pagesAcrobat Document 5Prakash MECH KiotNo ratings yet

- Design Computerized Antenatal Information System GodiyaDocument42 pagesDesign Computerized Antenatal Information System GodiyaJackie JakeNo ratings yet

- Lagos City Polytechnic Acc 213 e LearningDocument86 pagesLagos City Polytechnic Acc 213 e LearningJohn Maxwell100% (1)

- Internal Control in Swedish Small and Medium Size EnterprisesDocument67 pagesInternal Control in Swedish Small and Medium Size EnterprisesLeo CerenoNo ratings yet

- UntitledDocument105 pagesUntitledMesafint AyeleNo ratings yet

- Dwnload Full Principles of Auditing An Introduction To International Standards On Auditing 3rd Edition Hayes Solutions Manual PDFDocument36 pagesDwnload Full Principles of Auditing An Introduction To International Standards On Auditing 3rd Edition Hayes Solutions Manual PDFtobijayammev100% (10)

- Audit IIDocument77 pagesAudit II፩ne LoveNo ratings yet

- Chapters PagesDocument32 pagesChapters PagesNurul FajriyahNo ratings yet

- Assessment of Electronic Banking and Service DeliveryDocument83 pagesAssessment of Electronic Banking and Service DeliveryKeamogetse MotlogeloaNo ratings yet

- Bose OkehDocument44 pagesBose Okehjomex tundexNo ratings yet

- The Sarbanes-Oxley Section 404 Implementation Toolkit: Practice Aids for Managers and AuditorsFrom EverandThe Sarbanes-Oxley Section 404 Implementation Toolkit: Practice Aids for Managers and AuditorsNo ratings yet

- The Sarbanes-Oxley Section 404 Implementation Toolkit: Practice Aids for Managers and Auditors with CD ROMFrom EverandThe Sarbanes-Oxley Section 404 Implementation Toolkit: Practice Aids for Managers and Auditors with CD ROMNo ratings yet

- Beyond Sarbanes-Oxley Compliance: Effective Enterprise Risk ManagementFrom EverandBeyond Sarbanes-Oxley Compliance: Effective Enterprise Risk ManagementNo ratings yet

- 20170724-Transparency-Supplemental Guidelines GSIS FOI PolicyDocument116 pages20170724-Transparency-Supplemental Guidelines GSIS FOI PolicyAguilar QuezonNo ratings yet

- EPC Job DescriptionsDocument31 pagesEPC Job Descriptionsacalerom3625No ratings yet

- Under Four Flags (Smith Bell)Document6 pagesUnder Four Flags (Smith Bell)marcheinNo ratings yet

- Constitution of ISK of 12 02 10 Revised Very Final Version 2020Document28 pagesConstitution of ISK of 12 02 10 Revised Very Final Version 2020Epaja Jeremiah JesseNo ratings yet

- COA DECISION NO. 2022-086 Salaries of JO Under SPDocument15 pagesCOA DECISION NO. 2022-086 Salaries of JO Under SPchocoNo ratings yet

- Purchase Controls QuestionnaireDocument3 pagesPurchase Controls QuestionnaireMarieJoiaNo ratings yet

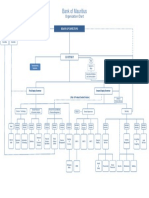

- Organisation Structure Bank of MauritiusDocument1 pageOrganisation Structure Bank of MauritiuscvikasguptaNo ratings yet

- Temporary Adv. Settlement Process - Annex - ADocument3 pagesTemporary Adv. Settlement Process - Annex - ASDE BSS KollamNo ratings yet

- Md. Sahed Ikbal ID #1330979Document30 pagesMd. Sahed Ikbal ID #1330979Ibrahim Khailil 1915216660No ratings yet

- CA Inter Audit Top 50 Question May 2021Document54 pagesCA Inter Audit Top 50 Question May 2021Pankaj MeenaNo ratings yet

- ISO 14001 All-in-One Package PDFDocument39 pagesISO 14001 All-in-One Package PDFArga KrisnaNo ratings yet

- BSBFIN501 VET Unit Assessment PackDocument45 pagesBSBFIN501 VET Unit Assessment PackAngela .ANo ratings yet

- KODA LTD 2011 Annual ReportDocument109 pagesKODA LTD 2011 Annual ReportWeR1 Consultants Pte LtdNo ratings yet

- 2017 About Face 2017 Audit Protocol FinalDocument92 pages2017 About Face 2017 Audit Protocol FinalHUGO VASQUEZNo ratings yet

- Asuprin Activity 4Document4 pagesAsuprin Activity 4Melvin BagasinNo ratings yet

- Case Studies in Project Management - Miller Park StadiumDocument27 pagesCase Studies in Project Management - Miller Park Stadiummaswing-1100% (2)

- The Metrocentre Partnership Report and Financial Statements For The Year Ended 31 December 2019Document37 pagesThe Metrocentre Partnership Report and Financial Statements For The Year Ended 31 December 2019Roshan PriyadarshiNo ratings yet

- CookBook 09 Internal Audits - 09-2018Document2 pagesCookBook 09 Internal Audits - 09-2018Jacek SobczykNo ratings yet

- Audcase 2Document3 pagesAudcase 2Ian Stromwell Guzman0% (1)

- RESeARCH SBMDocument11 pagesRESeARCH SBMRocel May Recones VargasNo ratings yet

- SSL Add-On - Amortization of AccrualsDocument9 pagesSSL Add-On - Amortization of AccrualsSri Sathya Sai Anugraha GruhamNo ratings yet

- 11.11.2017 Audit of PPEDocument9 pages11.11.2017 Audit of PPEPatOcampoNo ratings yet

- Summit Corporation Limited-1Document2 pagesSummit Corporation Limited-1jowila5377No ratings yet

- HR Audit HR Accounting - Module 6Document27 pagesHR Audit HR Accounting - Module 6Aakash KrNo ratings yet

- PAS 700 and 701 Graphic OrganizerDocument2 pagesPAS 700 and 701 Graphic OrganizerwencyNo ratings yet

- Mandatory Requirement of Implementing Internal Financial Controls For All Companies - Vishnu Daya & Co LLPDocument5 pagesMandatory Requirement of Implementing Internal Financial Controls For All Companies - Vishnu Daya & Co LLPKRISHNA RAO KNo ratings yet

- IMS - Integrated Management System Implementation Steps-Sterling - Rev00-240914 PDFDocument28 pagesIMS - Integrated Management System Implementation Steps-Sterling - Rev00-240914 PDFNorman AinomugishaNo ratings yet

- Skills Audit FormDocument10 pagesSkills Audit FormPurwanto Soe'ebNo ratings yet