Download as docx, pdf, or txt

You might also like

- 2022 T1 Form - CompletedDocument8 pages2022 T1 Form - CompletedARSH GROVERNo ratings yet

- Provident Fund ActDocument14 pagesProvident Fund ActAkanksha Dubey0% (1)

- Labour Laws - Part 1 (PF)Document33 pagesLabour Laws - Part 1 (PF)samarth agrawalNo ratings yet

- Labour LawDocument8 pagesLabour LawHarshada SinghNo ratings yet

- Employees' Provident Fund and Miscellaneous ActDocument20 pagesEmployees' Provident Fund and Miscellaneous ActAnchal PundirNo ratings yet

- HRMMDocument8 pagesHRMMAnand PandeyNo ratings yet

- Ill NCP UpdatedDocument200 pagesIll NCP Updatedsubham kumar dalaraNo ratings yet

- Employees Provident Funds Act, 1952: Coverage of Act - The Act Has Been Extended To Factories Mines Other Than CoalDocument10 pagesEmployees Provident Funds Act, 1952: Coverage of Act - The Act Has Been Extended To Factories Mines Other Than CoalGokul RanghamannarNo ratings yet

- Presentation On PF Misc Provision Acts 1952Document45 pagesPresentation On PF Misc Provision Acts 1952puja_05100% (2)

- Employee State Insurance Corporation Act 1948Document26 pagesEmployee State Insurance Corporation Act 1948prachi_richaNo ratings yet

- Esic, 1948Document108 pagesEsic, 1948Bidisha GhoshalNo ratings yet

- Chapter 5 - Employees State Insurance Act 1948Document18 pagesChapter 5 - Employees State Insurance Act 1948Hyma TennetiNo ratings yet

- Definitions-In This Act, Unless The Context Otherwise Requires - "Appropriate Government" MeansDocument10 pagesDefinitions-In This Act, Unless The Context Otherwise Requires - "Appropriate Government" Meansmimansha barethNo ratings yet

- Labour Law AssignmentDocument3 pagesLabour Law AssignmentANOUSHKANo ratings yet

- Labour Welfare LawDocument19 pagesLabour Welfare Lawacharyatushar1007No ratings yet

- Every Thing Abt PFDocument24 pagesEvery Thing Abt PFVivek SrivastawaNo ratings yet

- Social Security of Workers: Presented By: Nikita Begum Talukdar Assistant Professor Upes School of LawDocument48 pagesSocial Security of Workers: Presented By: Nikita Begum Talukdar Assistant Professor Upes School of Lawdeepak singhalNo ratings yet

- ESI - Net InformationDocument8 pagesESI - Net Informationsandee1983No ratings yet

- Employee Provident Fund Act 1952Document14 pagesEmployee Provident Fund Act 1952Shaista NasirNo ratings yet

- Employee State Insurance Act, 1948: Related Legislations: ESI (Central) Rules, 1950 and ESI (General) Regulations, 1950Document81 pagesEmployee State Insurance Act, 1948: Related Legislations: ESI (Central) Rules, 1950 and ESI (General) Regulations, 1950Harsha PatelNo ratings yet

- Employees Provident Fund Act, 1952Document0 pagesEmployees Provident Fund Act, 1952Sunil ShawNo ratings yet

- Labour LawsDocument20 pagesLabour LawsHarshvardhan KambleNo ratings yet

- Labour CodeDocument3 pagesLabour CodesyutnzfdhjxbspfnglNo ratings yet

- Applicability of EPF ActDocument13 pagesApplicability of EPF ActRajat0786No ratings yet

- P & A Compl - Induction MNGTDocument5 pagesP & A Compl - Induction MNGTAnimesh1981No ratings yet

- Employee State Insurance ActDocument27 pagesEmployee State Insurance ActAmrit SukumarNo ratings yet

- V IllrDocument14 pagesV IllrVasugi KumarNo ratings yet

- Assignment of Labour LawDocument6 pagesAssignment of Labour LawUrvashi DwivediNo ratings yet

- Employee State Insurance ActDocument7 pagesEmployee State Insurance ActSurya Sai RamNo ratings yet

- The Employees' Provident Funds and Miscellaneous Provisions Act, 1952Document34 pagesThe Employees' Provident Funds and Miscellaneous Provisions Act, 1952Sandeep Kumar SinghNo ratings yet

- Social Security in IndiaDocument49 pagesSocial Security in IndiaKaran Gupta100% (1)

- Lecture-2 Employees' Provident Funds and Miscellaneous Provisions Act, 1952Document7 pagesLecture-2 Employees' Provident Funds and Miscellaneous Provisions Act, 1952lakshmikanthsrNo ratings yet

- Unit 4 IRDocument18 pagesUnit 4 IRpreeti20.officeNo ratings yet

- Labour Laws PresentationDocument124 pagesLabour Laws PresentationMuthyala NagarajuNo ratings yet

- Q.1. Explain in Detail About ESI Act. Ans.:: The Employee State Insurance Act, 1948Document4 pagesQ.1. Explain in Detail About ESI Act. Ans.:: The Employee State Insurance Act, 1948nitin KindoNo ratings yet

- Payment of Gratuity ActDocument32 pagesPayment of Gratuity ActPrikshit SainiNo ratings yet

- 1 1 Employees PF ActDocument9 pages1 1 Employees PF ActSudha SatishNo ratings yet

- Retirement BenefitsDocument9 pagesRetirement BenefitsSandeep SavarkarNo ratings yet

- Employee Provident Fund & Miscellaneous ACT 1952: Abhishek NagreDocument28 pagesEmployee Provident Fund & Miscellaneous ACT 1952: Abhishek NagreSaiPhaniNo ratings yet

- HOME Assignment of Labour LawDocument9 pagesHOME Assignment of Labour LawKashish KalraNo ratings yet

- Payment of Gratuity Act 1972Document21 pagesPayment of Gratuity Act 1972Nitali VatsarajNo ratings yet

- Employees Provident Fund & Misc. Provisions Act, 1952Document36 pagesEmployees Provident Fund & Misc. Provisions Act, 1952Arun ShettarNo ratings yet

- Unit V I.LDocument10 pagesUnit V I.LPooja MishraNo ratings yet

- Employees Provident Fund & Miscellaneous Provision Act, 1958Document10 pagesEmployees Provident Fund & Miscellaneous Provision Act, 1958Maulik VoraNo ratings yet

- ESIC by CA Pranav ChandakDocument15 pagesESIC by CA Pranav ChandakMehak Kaushikk100% (1)

- 20 (Twenty) or More PersonsDocument12 pages20 (Twenty) or More PersonsakashNo ratings yet

- Labour Laws in IndiaDocument9 pagesLabour Laws in Indiaaparna160673No ratings yet

- Institute of Management Studies (DAVV)Document14 pagesInstitute of Management Studies (DAVV)Anukrati BagherwalNo ratings yet

- EPF ActDocument5 pagesEPF ActRajpreet kaur KadambNo ratings yet

- EpfoDocument33 pagesEpfoSHRISHTI SINGH100% (1)

- Unit 5Document43 pagesUnit 5mStarboyNo ratings yet

- Act Labour Employees StateinsuranceDocument15 pagesAct Labour Employees StateinsuranceShivam KumarNo ratings yet

- EOBIDocument15 pagesEOBIZeeshan ShafiqueNo ratings yet

- Payment of Gratuity Act, 1972Document7 pagesPayment of Gratuity Act, 1972Viney VermaNo ratings yet

- BBA-MBA Integrated Programme Advanced Course On OB & HRM Individual Assignment Submitted byDocument19 pagesBBA-MBA Integrated Programme Advanced Course On OB & HRM Individual Assignment Submitted byAalokNo ratings yet

- Code On Social SecurityDocument12 pagesCode On Social SecurityShivani WagleNo ratings yet

- EsiDocument65 pagesEsipsugwekarNo ratings yet

- Pensions in Italy: The guide to pensions in Italy, with the rules for accessing ordinary and early retirement in the public and private systemFrom EverandPensions in Italy: The guide to pensions in Italy, with the rules for accessing ordinary and early retirement in the public and private systemNo ratings yet

- Bar Review Companion: Labor Laws and Social Legislation: Anvil Law Books Series, #3From EverandBar Review Companion: Labor Laws and Social Legislation: Anvil Law Books Series, #3No ratings yet

- Theory of Firm Under PERFECT CompetitionDocument24 pagesTheory of Firm Under PERFECT CompetitionJasmine JeganNo ratings yet

- Theory of Consumer BehaviorDocument30 pagesTheory of Consumer BehaviorJasmine JeganNo ratings yet

- Theory of Consumer Behaviour-1Document31 pagesTheory of Consumer Behaviour-1Jasmine JeganNo ratings yet

- Indian Partnership Act, 1932Document19 pagesIndian Partnership Act, 1932Jasmine JeganNo ratings yet

- Separation Declaration: Family Law Act 1975Document3 pagesSeparation Declaration: Family Law Act 1975Flordeluna Aying-SanoNo ratings yet

- Masters Research Proposal-CorrectedDocument44 pagesMasters Research Proposal-Correctedomolloh asangoNo ratings yet

- AC2201 CHAPTER 19 NotesDocument3 pagesAC2201 CHAPTER 19 NotesKemuel TantuanNo ratings yet

- 11 - 2023 - Aiboc - UFBU - Meeting With IBA On 28.02.2023Document2 pages11 - 2023 - Aiboc - UFBU - Meeting With IBA On 28.02.2023NAOMIKA DUTTANo ratings yet

- Legislative Compliance Rates Sheet EnclosedDocument4 pagesLegislative Compliance Rates Sheet Enclosedlarryching_884369919No ratings yet

- Financial Statement Analysis of TCS and INFOSYSDocument43 pagesFinancial Statement Analysis of TCS and INFOSYSRitwik Subudhi100% (1)

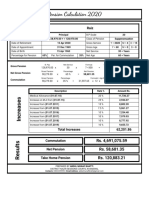

- Pension CalculationDocument1 pagePension CalculationAhmad FarhanNo ratings yet

- Employee Benefits: Cruz, Jerica May A. CBET-01-501EDocument21 pagesEmployee Benefits: Cruz, Jerica May A. CBET-01-501Eclara san miguelNo ratings yet

- SBI+Life+-+Smart+Annuity+Plus NPS+Single+Pager V03Document3 pagesSBI+Life+-+Smart+Annuity+Plus NPS+Single+Pager V03Mangal SinghNo ratings yet

- AP IT FY 2022-23 Income Tax Software 23.01.2023Document14 pagesAP IT FY 2022-23 Income Tax Software 23.01.2023Nitesh SreeNo ratings yet

- Funciones y Operaciones Del Calculo de La NominaDocument51 pagesFunciones y Operaciones Del Calculo de La NominafranklinbasanteNo ratings yet

- NPS 2022Document12 pagesNPS 2022karthic kumarNo ratings yet

- Innovative Practices Followed by The Institution To Enhance Financial Inclusion Canara BankDocument4 pagesInnovative Practices Followed by The Institution To Enhance Financial Inclusion Canara BankShanu RajpalNo ratings yet

- The Employees' Pension SchemeDocument2 pagesThe Employees' Pension Schemesai KRISHNANo ratings yet

- Shorter Life Expectancy Gives UK Pensions An Unexpected Windfall - Financial TimesDocument4 pagesShorter Life Expectancy Gives UK Pensions An Unexpected Windfall - Financial TimesAleksandar SpasojevicNo ratings yet

- Module in Income Taxation by Jewelyn C. Espares-CioconDocument33 pagesModule in Income Taxation by Jewelyn C. Espares-CioconmarkbagzNo ratings yet

- Life Insurence SiaDocument116 pagesLife Insurence Siabagi alekhya100% (1)

- Form 13 - (PF Transfer Form)Document2 pagesForm 13 - (PF Transfer Form)Abhishek DasguptaNo ratings yet

- MA13131Document3 pagesMA13131gamers SatisfactionNo ratings yet

- Central Recordkeeping AgencyDocument3 pagesCentral Recordkeeping AgencyAnuj SoniNo ratings yet

- EmpBen TheoriesDocument8 pagesEmpBen TheoriesCarl Dhaniel Garcia SalenNo ratings yet

- Salary HP Liability in Special CasesDocument30 pagesSalary HP Liability in Special CasesParth ThakkarNo ratings yet

- Financial Economics AssiggDocument16 pagesFinancial Economics Assiggkalid kalNo ratings yet

- SSS and GSIS PresentationDocument10 pagesSSS and GSIS PresentationMarvic AmazonaNo ratings yet

- Letter of Authority - (Dpdo Pensioners) (To Be Obtained in Dulicate) FromDocument2 pagesLetter of Authority - (Dpdo Pensioners) (To Be Obtained in Dulicate) FromsunilNo ratings yet

- Lecture8 SIQ3003 PDFDocument16 pagesLecture8 SIQ3003 PDFFion TayNo ratings yet

- Chapter 1 Lecture Notes.2021Document18 pagesChapter 1 Lecture Notes.2021Hoyin SinNo ratings yet

- Indemnity Cum Declaration Undertaking NOC For PA ClaimsDocument1 pageIndemnity Cum Declaration Undertaking NOC For PA Claimssaurav960% (1)

- Pension Calculator With Commuted LeaveDocument3 pagesPension Calculator With Commuted LeaveAp ChandranNo ratings yet