Download as pdf or txt

You might also like

- DailyScoop January 19 2024 by AffairsCloud 1Document30 pagesDailyScoop January 19 2024 by AffairsCloud 1Rem RemNo ratings yet

- Union Budget 2019: Aditya Channam & Rahul NagpalDocument21 pagesUnion Budget 2019: Aditya Channam & Rahul Nagpalravi tejaNo ratings yet

- Budget 2021 - Highlights & Takeaways-MergedDocument22 pagesBudget 2021 - Highlights & Takeaways-MergedRahul RanjanNo ratings yet

- Indian Union Budget 2020Document11 pagesIndian Union Budget 2020Md DhaniyalNo ratings yet

- Bold Step Towards 5 Trillion Economy: CMA Bhogavalli Mallikarjuna GuptaDocument3 pagesBold Step Towards 5 Trillion Economy: CMA Bhogavalli Mallikarjuna GuptavenkannaNo ratings yet

- Impact Analysis: Budget 2014-15Document4 pagesImpact Analysis: Budget 2014-15Raj AraNo ratings yet

- MacroeconomicsDocument7 pagesMacroeconomicsreinaelizabeth890No ratings yet

- Final Mic EcoDocument21 pagesFinal Mic EcoPrajna BhatNo ratings yet

- Key Features of Budget 2012-2013Document15 pagesKey Features of Budget 2012-2013anupbhansali2004No ratings yet

- Deepshika RajputDocument19 pagesDeepshika RajputMRS.NAMRATA KISHNANI BSSSNo ratings yet

- PDF Budget - GovardhanDocument39 pagesPDF Budget - GovardhanGovardhan PandeNo ratings yet

- Fiscal Policy 2020 Introduction To Fiscal PolicyDocument8 pagesFiscal Policy 2020 Introduction To Fiscal PolicyMamata SreenivasNo ratings yet

- The Hindu Review July 2019 PDFDocument23 pagesThe Hindu Review July 2019 PDFSiva ShankarNo ratings yet

- The Hindu Review (July 2019)Document23 pagesThe Hindu Review (July 2019)mense vishalNo ratings yet

- Highlights of Eco 2022 23 14 02 099c41198f 16Document1 pageHighlights of Eco 2022 23 14 02 099c41198f 16cono.rq.an.g.el4.8No ratings yet

- Acn AssignmentDocument5 pagesAcn AssignmentjacksonNo ratings yet

- Union Budget 2019-20Document15 pagesUnion Budget 2019-20Smitha MohanNo ratings yet

- Key Features of Budget 2012-2013Document15 pagesKey Features of Budget 2012-2013Avinash ShahiNo ratings yet

- Compare Budget 2023 With 2022Document8 pagesCompare Budget 2023 With 2022Vartika VNo ratings yet

- Market Strategy: February 2021Document19 pagesMarket Strategy: February 2021Harshvardhan SurekaNo ratings yet

- 15th Finance CommissionDocument6 pages15th Finance CommissionPrajjwal AgrawalNo ratings yet

- Union Budget Highlights 2012-13Document15 pagesUnion Budget Highlights 2012-13rockyNo ratings yet

- YojanaMarch2020summary Part11586344521 PDFDocument29 pagesYojanaMarch2020summary Part11586344521 PDFVikin JainNo ratings yet

- Union Budget 2012-13: HighlightsDocument15 pagesUnion Budget 2012-13: HighlightsNDTVNo ratings yet

- Budget AnalysisDocument9 pagesBudget AnalysisAdeel AshrafNo ratings yet

- Summary of Full Budget 2019: Budget and Survey 2019 Notes: 1Document4 pagesSummary of Full Budget 2019: Budget and Survey 2019 Notes: 1kabu209No ratings yet

- Fin An Ce Mi No R PR OjDocument13 pagesFin An Ce Mi No R PR OjVignesh SuryadevaraNo ratings yet

- Union Budget 2019 - 2020Document26 pagesUnion Budget 2019 - 2020Sunil SaharanNo ratings yet

- Highlights of Union Budget 2019-20Document26 pagesHighlights of Union Budget 2019-20Sunil SaharanNo ratings yet

- Union Budget 2019 - 2020Document26 pagesUnion Budget 2019 - 2020Sunil SaharanNo ratings yet

- Weekly One Liners 31st January To 6th of February 2022Document14 pagesWeekly One Liners 31st January To 6th of February 2022Rajesh ShenoyNo ratings yet

- Project Report On BUDGET (2022-23) : Computer Applications in BusinessDocument15 pagesProject Report On BUDGET (2022-23) : Computer Applications in BusinessDeepu yadavNo ratings yet

- Union Budget 2021 Highlights and ImpactDocument10 pagesUnion Budget 2021 Highlights and Impact200409120010No ratings yet

- Special Coverage: Most Important For Full MarksDocument21 pagesSpecial Coverage: Most Important For Full MarksLekshmi UNo ratings yet

- India Budget 2012-13Document5 pagesIndia Budget 2012-13findprabhuNo ratings yet

- I M S Engineering College Ghaziabad: Presented To Supriya Mam Presented by Shobhit Verma Ved PrakashDocument16 pagesI M S Engineering College Ghaziabad: Presented To Supriya Mam Presented by Shobhit Verma Ved PrakashLavi VermaNo ratings yet

- Union Budget 2022: 92nd Union Budget 2022-23: Key Highlights of Union BudgetDocument4 pagesUnion Budget 2022: 92nd Union Budget 2022-23: Key Highlights of Union BudgetsiddNo ratings yet

- Macroeconomic PolicyDocument6 pagesMacroeconomic Policyrakibul hasanNo ratings yet

- Union BudgetDocument9 pagesUnion BudgetsameeraNo ratings yet

- Compliance With Annual Reduction Targets Specified Under The FRBM ActDocument38 pagesCompliance With Annual Reduction Targets Specified Under The FRBM ActBhanu UpadhyayNo ratings yet

- Budget BOOK FinalDocument19 pagesBudget BOOK FinalAmin ChhipaNo ratings yet

- Etm 2012 3 17 1Document1 pageEtm 2012 3 17 1abhi16No ratings yet

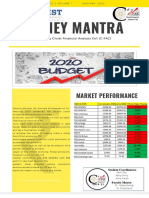

- Money Mantra: Market PerformanceDocument4 pagesMoney Mantra: Market PerformanceAlbin SibyNo ratings yet

- The Hindu Review July 2019Document24 pagesThe Hindu Review July 2019Anas HashmiNo ratings yet

- BudgetDocument24 pagesBudgetSumit BhanderiNo ratings yet

- A Critical Analysis of The Union Budget 2021Document4 pagesA Critical Analysis of The Union Budget 2021Jamila MustafaNo ratings yet

- Budget 2009Document7 pagesBudget 2009akashNo ratings yet

- BudgetDocument13 pagesBudgetRavneetNo ratings yet

- Highlights of The Union Budget 2022 Partt 222Document33 pagesHighlights of The Union Budget 2022 Partt 222KUSUMA ANo ratings yet

- Budget Main PagesDocument43 pagesBudget Main Pagesneha16septNo ratings yet

- Driving Growth Union Budget 2023 24Document25 pagesDriving Growth Union Budget 2023 24shwetaNo ratings yet

- Economic Survey 2022-23Document26 pagesEconomic Survey 2022-23Naveen GopeNo ratings yet

- Union Budget 2024Document68 pagesUnion Budget 2024Scribd007No ratings yet

- Indian Economy and The ChallengesDocument8 pagesIndian Economy and The ChallengesNehaNo ratings yet

- Union Budget Analysis - 2022-23Document8 pagesUnion Budget Analysis - 2022-23PRIYA PAULNo ratings yet

- Budget 2024 25 Summary 1706888004Document20 pagesBudget 2024 25 Summary 1706888004scientist xyzNo ratings yet

- A Brief Analysis of National Budget Fiscal Year 2023-24Document10 pagesA Brief Analysis of National Budget Fiscal Year 2023-24Foysal AhmedNo ratings yet

- Strengthening Fiscal Decentralization in Nepal’s Transition to FederalismFrom EverandStrengthening Fiscal Decentralization in Nepal’s Transition to FederalismNo ratings yet

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesFrom EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- L21.2 2nd May 11 AM B-1 To 5Document5 pagesL21.2 2nd May 11 AM B-1 To 5denhkNo ratings yet

- Causelist 141Document274 pagesCauselist 141denhkNo ratings yet

- Eco 500 MCQ Vivek Singh PDFDocument210 pagesEco 500 MCQ Vivek Singh PDFdenhkNo ratings yet

- PIB Summary October 2022Document9 pagesPIB Summary October 2022denhkNo ratings yet

- Cutoff 2021Document1 pageCutoff 2021denhkNo ratings yet

- KSG CSP20 Test 29Document28 pagesKSG CSP20 Test 29denhkNo ratings yet

- MachinesDocument95 pagesMachinesdenhkNo ratings yet

- Presented by - Mitesh NaikDocument18 pagesPresented by - Mitesh NaikdenhkNo ratings yet

- Even Sem 2016Document1 pageEven Sem 2016denhkNo ratings yet

- Ey Private Credit in India v1Document18 pagesEy Private Credit in India v1Naman JainNo ratings yet

- BL - Delhi 23-02Document14 pagesBL - Delhi 23-02aphadnis12No ratings yet

- BL - Mumbai 23-02Document14 pagesBL - Mumbai 23-02aphadnis12No ratings yet

- SHIVALIK - PLAN - RESIDENCE - For Study PurposeDocument12 pagesSHIVALIK - PLAN - RESIDENCE - For Study PurposenmmmNo ratings yet

- Weekly Current Affairs 13th May To 19th May 2024Document19 pagesWeekly Current Affairs 13th May To 19th May 2024renuvijay4567No ratings yet

- International Financial Services Centres Authority IFSCADocument3 pagesInternational Financial Services Centres Authority IFSCAPujitha VadlamudiNo ratings yet

- GIFT City BrochureDocument6 pagesGIFT City BrochureHardikNo ratings yet

- Kotak Mahindra Bank Limited FY22 23Document197 pagesKotak Mahindra Bank Limited FY22 23prabhatkumarrock27No ratings yet

- Conveyance Deed: The Party of The First Part: VendorDocument28 pagesConveyance Deed: The Party of The First Part: VendornmmmNo ratings yet

- IT-ITES Sector Profile V5.1Document19 pagesIT-ITES Sector Profile V5.1gohilvishu03No ratings yet

- In India Japan Trade Relations Report NoexpDocument24 pagesIn India Japan Trade Relations Report NoexpHasratNo ratings yet

- Invitation BookletDocument64 pagesInvitation BookletAssistant Director KHRINo ratings yet

- Opportunities in GIFT City - Nishith Desai & AssociatesDocument75 pagesOpportunities in GIFT City - Nishith Desai & AssociatesRR AnalystNo ratings yet

- Current Affairs Weekly PDF - April 2021 1st Week (1-7) by AffairsCloud 1Document20 pagesCurrent Affairs Weekly PDF - April 2021 1st Week (1-7) by AffairsCloud 1most funny videoNo ratings yet

- Beepedia Monthly Current Affairs (Beepedia) November 2023Document141 pagesBeepedia Monthly Current Affairs (Beepedia) November 2023Vikram SharmaNo ratings yet

- CA Journal - December 2023Document132 pagesCA Journal - December 202309shaaliniNo ratings yet

- GIFT City As India80 S Financial HubDocument5 pagesGIFT City As India80 S Financial HubSarika MauryaNo ratings yet

- Grand Mercure Gandhinagar Gift City PresentationDocument16 pagesGrand Mercure Gandhinagar Gift City PresentationdevendraasalkarNo ratings yet

- Shipping IFSCA Presentation Tokyo Oct 27Document36 pagesShipping IFSCA Presentation Tokyo Oct 27Rajaraman KalyanaramanNo ratings yet

- AIFs in GIFT IFSC Booklet October 2020Document12 pagesAIFs in GIFT IFSC Booklet October 2020Karthick JayNo ratings yet

- Current Affairs Weekly Content PDF February 2023 1st Week by AffairsCloudDocument33 pagesCurrent Affairs Weekly Content PDF February 2023 1st Week by AffairsCloudSagar DebnathNo ratings yet

- IFSCA Presentation 15 November 2023Document48 pagesIFSCA Presentation 15 November 2023Rajaraman KalyanaramanNo ratings yet

- BL - Kolkata 23-02Document14 pagesBL - Kolkata 23-02aphadnis12No ratings yet

- Reva PlanDocument26 pagesReva PlannmmmNo ratings yet

- International Financial Services Centre: IndiaDocument12 pagesInternational Financial Services Centre: IndiaSri NikithaNo ratings yet

- Current Affairs Weekly Content PDF May 2024 2nd Week by AffairsCloud New 1Document27 pagesCurrent Affairs Weekly Content PDF May 2024 2nd Week by AffairsCloud New 1gargmuskan1911No ratings yet

- Icsi Student Training GUIDELINES-2024Document74 pagesIcsi Student Training GUIDELINES-2024Sakshi GuptaNo ratings yet

- World Junior U20 2024Document15 pagesWorld Junior U20 2024danfestudentscouncilNo ratings yet

- BL - Chennai 23-02Document14 pagesBL - Chennai 23-02aphadnis12No ratings yet