Download as pdf or txt

You might also like

- Elijah Vue Criminal ComplaintDocument4 pagesElijah Vue Criminal ComplaintLeigh Egan100% (1)

- DS 50 - Ver 1 Rev 2 Jan 2014Document75 pagesDS 50 - Ver 1 Rev 2 Jan 2014Amin AminiNo ratings yet

- Exercise No. 2 What Is Good Legal Writing SummaryDocument2 pagesExercise No. 2 What Is Good Legal Writing SummaryKarleen Gayle C. MalateNo ratings yet

- Lost Duplicate RC Book Police FIR Blank Template Format For TeamBHPDocument1 pageLost Duplicate RC Book Police FIR Blank Template Format For TeamBHPAswin Prasad90% (10)

- Inventory Transfer Request - 20231116 - 102023AMDocument1 pageInventory Transfer Request - 20231116 - 102023AMWaqar HadiNo ratings yet

- 3X IntercoDocument3 pages3X IntercoYong BenedictNo ratings yet

- NCA Question Bank Solutions - 08042024Document9 pagesNCA Question Bank Solutions - 08042024Boitumelo MatjeleNo ratings yet

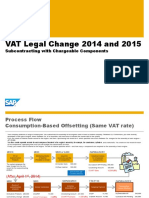

- VAT Legal Change 2014 and 2015: Subcontracting With Chargeable ComponentsDocument8 pagesVAT Legal Change 2014 and 2015: Subcontracting With Chargeable ComponentsTaro YamadaNo ratings yet

- FREP01-OS Consolidation P2 - TWCC LTD SolutionDocument6 pagesFREP01-OS Consolidation P2 - TWCC LTD SolutionZintle KeswaNo ratings yet

- MOCK Test SOLUTIONDocument5 pagesMOCK Test SOLUTIONNcebakazi DawedeNo ratings yet

- FCA # 100321-Ex-Proof Operated Forklift-SW Vietnam-DN Plant - ApprovedDocument3 pagesFCA # 100321-Ex-Proof Operated Forklift-SW Vietnam-DN Plant - ApprovedGraceNo ratings yet

- Memorandum Question 10 Jeff Limited 2021Document2 pagesMemorandum Question 10 Jeff Limited 2021NOKUHLE ARTHELNo ratings yet

- Assignment 3 (Acc - Receivable) BaruDocument23 pagesAssignment 3 (Acc - Receivable) BaruniaNo ratings yet

- Daily Margin Statement 0215125531Document1 pageDaily Margin Statement 0215125531sc068976No ratings yet

- Press Release Suzlon Energy Limited: Details of Instruments/facilities in Annexure-1Document5 pagesPress Release Suzlon Energy Limited: Details of Instruments/facilities in Annexure-1Thakur Anmol RajputNo ratings yet

- FAC3761 - Exam Prep - Mock Question Paper - Suggested SolutionDocument9 pagesFAC3761 - Exam Prep - Mock Question Paper - Suggested SolutionRene EngelbrechtNo ratings yet

- Class Example 1, 3, 6 (Solutions)Document8 pagesClass Example 1, 3, 6 (Solutions)Given RefilweNo ratings yet

- Security List DetailsDocument1,795 pagesSecurity List Detailssantosh0% (1)

- Security List Details PDFDocument1,795 pagesSecurity List Details PDFsantoshNo ratings yet

- Adi Sarana Armada: Anteraja's Collaboration With Grab and GojekDocument7 pagesAdi Sarana Armada: Anteraja's Collaboration With Grab and Gojekbobby prayogoNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument12 pages© The Institute of Chartered Accountants of IndiaMiku JainNo ratings yet

- Forecast - WH5 Cost Report JanDocument7 pagesForecast - WH5 Cost Report JanMarkyNo ratings yet

- Nabors Industries Inc 2Q20 Credit ReportDocument7 pagesNabors Industries Inc 2Q20 Credit ReportKaramo CisséNo ratings yet

- Accounting MemoDocument9 pagesAccounting MemoNoma VioNo ratings yet

- Amar Talati - 2021 - 1120S - K1Document4 pagesAmar Talati - 2021 - 1120S - K1a_a_talatiNo ratings yet

- LNL Iklcqd /: Grand Total 13,748 4,208 0 0 9,103Document1 pageLNL Iklcqd /: Grand Total 13,748 4,208 0 0 9,103Shubha DiwakarNo ratings yet

- Running Metrico Print OurDocument1 pageRunning Metrico Print Ourram singhNo ratings yet

- Statement of Changes in Owners' Equity: P/L Balance SheetDocument6 pagesStatement of Changes in Owners' Equity: P/L Balance SheetJF FNo ratings yet

- 2023 Grade 11 Provincial Examination Accounting P1 (English) November 2023 Possible AnswerDocument9 pages2023 Grade 11 Provincial Examination Accounting P1 (English) November 2023 Possible AnswerChantelle IsaksNo ratings yet

- Total No. of Printedpages-11 Maximummarks - 100 ..: PC! Group I-Paper Advanced AccountingDocument11 pagesTotal No. of Printedpages-11 Maximummarks - 100 ..: PC! Group I-Paper Advanced AccountingNyonikaNo ratings yet

- NESTLEDocument141 pagesNESTLENataly Abanto VasquezNo ratings yet

- LO7 FULL Solution 2019Document16 pagesLO7 FULL Solution 2019Frederick LekalakalaNo ratings yet

- RV101 July 2021 Exam SolutionDocument11 pagesRV101 July 2021 Exam SolutionpartlinemokhothuNo ratings yet

- Angel Broking Limited.: Daily Margin Statement For The Day: 31/12/2021Document1 pageAngel Broking Limited.: Daily Margin Statement For The Day: 31/12/2021MUTHYALA NEERAJANo ratings yet

- Angel Broking Limited.: Daily Margin Statement For The Day: 31/12/2021Document1 pageAngel Broking Limited.: Daily Margin Statement For The Day: 31/12/2021MUTHYALA NEERAJANo ratings yet

- Angel Broking Limited.: Daily Margin Statement For The Day: 31/12/2021Document1 pageAngel Broking Limited.: Daily Margin Statement For The Day: 31/12/2021MUTHYALA NEERAJANo ratings yet

- Lease Assets Assessment Dec19 CHI Template 01012020 321052022Document7 pagesLease Assets Assessment Dec19 CHI Template 01012020 321052022Steven LaiNo ratings yet

- 1tb01005-005c17-Hah-Xx-Xx-Sdw-Me-05005-C1-Projected Floor Loading (A)Document2 pages1tb01005-005c17-Hah-Xx-Xx-Sdw-Me-05005-C1-Projected Floor Loading (A)MAZHAR ALINo ratings yet

- Far510 Test Dec 2020 SSDocument6 pagesFar510 Test Dec 2020 SS2022478048No ratings yet

- Ringi Linea de Credito OginDocument1 pageRingi Linea de Credito OginJose CordovaNo ratings yet

- Chun Ling Trial Exam 2022 - P2 (Answers)Document9 pagesChun Ling Trial Exam 2022 - P2 (Answers)Wei WenNo ratings yet

- BK Chapter 12Document8 pagesBK Chapter 1232 Yeow Zi Xuan姚祉杏No ratings yet

- CAF 07 Notes 2Document356 pagesCAF 07 Notes 2Scarlett IvyNo ratings yet

- LBCTCDocument35 pagesLBCTCJF FNo ratings yet

- Grand Total: DA: UnallocDocument1 pageGrand Total: DA: UnallocratiozNo ratings yet

- Form No. 26AS Annual Tax Statement Under Section 203AADocument8 pagesForm No. 26AS Annual Tax Statement Under Section 203AApandey_manishNo ratings yet

- Gr11 Accounting P1 (ENG) NOV Possible Answers-2Document9 pagesGr11 Accounting P1 (ENG) NOV Possible Answers-2Shriddhi MaharajNo ratings yet

- Mast!: Distribution SheetDocument47 pagesMast!: Distribution SheetSandro Barbagelata HuachacaNo ratings yet

- Ab5431 20220105 Combined Margin StatementDocument1 pageAb5431 20220105 Combined Margin Statementthotada durga prasadNo ratings yet

- Assignment 4 SolutionDocument2 pagesAssignment 4 SolutionThulani NdlovuNo ratings yet

- mmt070510 FV DBSVDocument9 pagesmmt070510 FV DBSVfivemoreminsNo ratings yet

- Tutorial 40F - Suggested SolutionDocument4 pagesTutorial 40F - Suggested Solutionmusa morinNo ratings yet

- Daily Cash Performa13Document3 pagesDaily Cash Performa13Azeem TahirNo ratings yet

- CAF 5 Spring 2022Document7 pagesCAF 5 Spring 2022Zia Ur RahmanNo ratings yet

- Financial Accounting Paper WajeehaDocument8 pagesFinancial Accounting Paper WajeehaTAIMOOR REHMANNo ratings yet

- Wbill 739 33400124638Document1 pageWbill 739 33400124638Jatin MehraNo ratings yet

- MA Report For Jan 11Document3 pagesMA Report For Jan 11harishpillayNo ratings yet

- Reading Details Attur 843Document2 pagesReading Details Attur 843mk gandhiNo ratings yet

- Problems Based On Ledger's Preparation P: Roblem 11Document28 pagesProblems Based On Ledger's Preparation P: Roblem 11Anonymous ameerNo ratings yet

- 0452 s03 Ms 2Document6 pages0452 s03 Ms 2lie chingNo ratings yet

- People v. Masterson: Shawn Holley LetterDocument2 pagesPeople v. Masterson: Shawn Holley LetterTony OrtegaNo ratings yet

- Raja Nand Kumar Case Critical AnalysisDocument6 pagesRaja Nand Kumar Case Critical AnalysisRadharani SharmaNo ratings yet

- Ed 2007.003.CFDocument3 pagesEd 2007.003.CFTony C.No ratings yet

- Land Law EssayDocument6 pagesLand Law Essayezknbk5h100% (2)

- NL17 EnglishDocument4 pagesNL17 EnglishAdrianAlexanderNo ratings yet

- Non-Circumvention, Non-Disclosure and Working AgreementDocument8 pagesNon-Circumvention, Non-Disclosure and Working AgreementclaudeNo ratings yet

- Internet JuneDocument1 pageInternet JuneUgesh ReddyNo ratings yet

- 033 - Cuenco V CADocument4 pages033 - Cuenco V CArgtan3No ratings yet

- R W A Child by His Litigation Friend J V SSHD Judgment UPDATEDDocument28 pagesR W A Child by His Litigation Friend J V SSHD Judgment UPDATEDAli ShafNo ratings yet

- 2018 - BALLB - 23 International Trade Law - Niyati KishoreDocument13 pages2018 - BALLB - 23 International Trade Law - Niyati Kishoreniyati kishoreNo ratings yet

- Memorial For RespondentDocument33 pagesMemorial For RespondentSweet100% (1)

- Assignment 1 Law507Document10 pagesAssignment 1 Law507NUR HIDAYAH AZIHNo ratings yet

- As We All Are AwareDocument17 pagesAs We All Are AwaremgrfanNo ratings yet

- The USADocument5 pagesThe USA1111No ratings yet

- Uganda Tax Amendments 2022-23Document24 pagesUganda Tax Amendments 2022-23Nelson KizangiNo ratings yet

- MIDTERMDocument27 pagesMIDTERMAngeline YongNo ratings yet

- LLB 203 (Crim - Law) Session 1Document5 pagesLLB 203 (Crim - Law) Session 1Walter BassumNo ratings yet

- SB 22457Document20 pagesSB 22457Dinesh DNo ratings yet

- Executive Summary FINALDocument2 pagesExecutive Summary FINALNalini RajamannanNo ratings yet

- Aa1807220145956 RC29072022 PDFDocument3 pagesAa1807220145956 RC29072022 PDFSunitee BaruahNo ratings yet

- Leases and LicensesDocument6 pagesLeases and LicensesShahraiz gillNo ratings yet

- Romeo Tiri Wa July 27, 2018Document1 pageRomeo Tiri Wa July 27, 2018Luppo PcaduNo ratings yet

- Warranty PDFDocument8 pagesWarranty PDFwillupowersNo ratings yet

- Hustler Magazine, Inc. v. FalwellDocument6 pagesHustler Magazine, Inc. v. FalwellAndrina Binogwal TocgongnaNo ratings yet

- Hoa Standing CommitteesDocument1 pageHoa Standing Committeesapi-626429090No ratings yet

- Dimayuga v. Benedicto IIDocument16 pagesDimayuga v. Benedicto IIAlthea Angela GarciaNo ratings yet