Download as pdf or txt

You might also like

- Talent Level 3 Tests Keys and ScriptsDocument17 pagesTalent Level 3 Tests Keys and ScriptsLUISA CASTRO CUNEO100% (1)

- ACCOUNTING 3 PPE ProblemsDocument4 pagesACCOUNTING 3 PPE ProblemsMina ChouNo ratings yet

- Ac3a Qe Oct2014 (TQ)Document15 pagesAc3a Qe Oct2014 (TQ)Julrick Cubio EgbusNo ratings yet

- Chapter 11-Investments in Noncurrent Operating Assets-Utilization and RetirementDocument33 pagesChapter 11-Investments in Noncurrent Operating Assets-Utilization and RetirementYukiNo ratings yet

- 2016 Vol 1 CH 8 Answers - Fin Acc SolManDocument7 pages2016 Vol 1 CH 8 Answers - Fin Acc SolManPamela Cruz100% (1)

- TB Chapter12Document33 pagesTB Chapter12CGNo ratings yet

- 6902 - Investment Property and Other InvestmentDocument3 pages6902 - Investment Property and Other InvestmentAljur SalamedaNo ratings yet

- Cup 3 Questions Answer KeyDocument34 pagesCup 3 Questions Answer KeyDenmarc John AragosNo ratings yet

- CA 04 - Job Order CostingDocument17 pagesCA 04 - Job Order CostingJoshua UmaliNo ratings yet

- Activity # 1: Management Advisory Services Part 1Document2 pagesActivity # 1: Management Advisory Services Part 1Vince BesarioNo ratings yet

- (Odd) Acc 101 LT#2B PDFDocument5 pages(Odd) Acc 101 LT#2B PDF有福No ratings yet

- Borrowing Costs - Assignment - For PostingDocument1 pageBorrowing Costs - Assignment - For Postingemman neriNo ratings yet

- Single Entry and Cash and AccrualDocument7 pagesSingle Entry and Cash and AccrualRinna LegaspiNo ratings yet

- ACCO 3026 Final ExamDocument11 pagesACCO 3026 Final ExamClarisseNo ratings yet

- Acctg405 Q6Document2 pagesAcctg405 Q6Baron MirandaNo ratings yet

- Quiz Recl FinancingDocument1 pageQuiz Recl FinancingLou Brad IgnacioNo ratings yet

- Chapter 7-The Revenue/Receivables/Cash Cycle: Multiple ChoiceDocument32 pagesChapter 7-The Revenue/Receivables/Cash Cycle: Multiple ChoiceLeonardoNo ratings yet

- Review - Practical Accounting 1Document2 pagesReview - Practical Accounting 1Kath LeynesNo ratings yet

- Cost Concepts, Classification and Segregation: M.S.M.CDocument7 pagesCost Concepts, Classification and Segregation: M.S.M.CAllen CarlNo ratings yet

- Solution: LCNRV Cost Bags 550,000 Bags 800,000 Shoes 1,000,000 Shoes 1,000,000 Clothing 700,000 Clothing 700,000 Lingerie 350,000 Lingerie 500,00Document3 pagesSolution: LCNRV Cost Bags 550,000 Bags 800,000 Shoes 1,000,000 Shoes 1,000,000 Clothing 700,000 Clothing 700,000 Lingerie 350,000 Lingerie 500,00Christian Clyde Zacal ChingNo ratings yet

- An SME Prepared The Following Post Closing Trial Balance at YearDocument1 pageAn SME Prepared The Following Post Closing Trial Balance at YearRaca DesuNo ratings yet

- Chapter 14Document47 pagesChapter 14darylleNo ratings yet

- Seatwork in Audit 2-3Document8 pagesSeatwork in Audit 2-3Shr BnNo ratings yet

- DocxDocument12 pagesDocxNothingNo ratings yet

- Applied Auditing Audit of Cash and ReceivablesDocument2 pagesApplied Auditing Audit of Cash and ReceivablesCar Mae LaNo ratings yet

- College: of Business AdministrationDocument5 pagesCollege: of Business AdministrationAna Mae HernandezNo ratings yet

- Gialogo, Jessie Lyn San Sebastian College - Recoletos Quiz: Required: Answer The FollowingDocument12 pagesGialogo, Jessie Lyn San Sebastian College - Recoletos Quiz: Required: Answer The FollowingMeidrick Rheeyonie Gialogo AlbaNo ratings yet

- Repair Cost Probabilit yDocument2 pagesRepair Cost Probabilit yNicole AguinaldoNo ratings yet

- 5share OptionsDocument21 pages5share OptionsnengNo ratings yet

- Special Revenue Recognition Special Revenue RecognitionDocument4 pagesSpecial Revenue Recognition Special Revenue RecognitionCee Gee BeeNo ratings yet

- Review QuestionairesDocument18 pagesReview QuestionairesAngelica DuarteNo ratings yet

- ReviewerDocument5 pagesReviewermaricielaNo ratings yet

- Quiz - Intangible Assets With QuestionsDocument3 pagesQuiz - Intangible Assets With Questionsjanus lopezNo ratings yet

- FA Mod1 2013Document551 pagesFA Mod1 2013Anoop Singh100% (2)

- True/False: Variable Costing: A Tool For ManagementDocument174 pagesTrue/False: Variable Costing: A Tool For ManagementKianneNo ratings yet

- Chapter 20 - Teacher's Manual - Far Part 1BDocument8 pagesChapter 20 - Teacher's Manual - Far Part 1BPacifico HernandezNo ratings yet

- INSTALLMENTDocument3 pagesINSTALLMENTEdison L. ChuNo ratings yet

- First QuizDocument4 pagesFirst QuizArn HicoNo ratings yet

- 4 Property Plant Equipment Classification Acquisition Govt Grant and Borrowing CostDocument11 pages4 Property Plant Equipment Classification Acquisition Govt Grant and Borrowing CostElvie PepitoNo ratings yet

- Fin Acc 2 Review MaterialsDocument17 pagesFin Acc 2 Review Materialsmaria evangelistaNo ratings yet

- FAR-04 Share Based PaymentsDocument3 pagesFAR-04 Share Based PaymentsKim Cristian Maaño0% (1)

- PPE Problem SetDocument18 pagesPPE Problem SetJustz LimNo ratings yet

- Ia3 BSDocument5 pagesIa3 BSMary Joy CabilNo ratings yet

- CL Cup 2018 (AUD, TAX, RFBT)Document4 pagesCL Cup 2018 (AUD, TAX, RFBT)sophiaNo ratings yet

- Unit Vi - Audit of Leases - Final - T11415 PDFDocument4 pagesUnit Vi - Audit of Leases - Final - T11415 PDFSed ReyesNo ratings yet

- Homework On Single Entry PDFDocument2 pagesHomework On Single Entry PDFalyssaNo ratings yet

- ACC 211 Review AssignmentDocument5 pagesACC 211 Review Assignmentglrosaaa cNo ratings yet

- BLT 2012 Final Pre-Board April 21Document17 pagesBLT 2012 Final Pre-Board April 21Lester AguinaldoNo ratings yet

- ACC117-CON09 Module 3 ExamDocument16 pagesACC117-CON09 Module 3 ExamMarlon LadesmaNo ratings yet

- 3rd S.A QuestionsDocument15 pages3rd S.A QuestionsIsaiah John Domenic M. CantaneroNo ratings yet

- MAS 7 Exercises For UploadDocument9 pagesMAS 7 Exercises For UploadChristine Joy Duterte RemorozaNo ratings yet

- Practical Accounting 1 First Pre-Board ExaminationDocument14 pagesPractical Accounting 1 First Pre-Board ExaminationKaren EloisseNo ratings yet

- LiabilitiesDocument2 pagesLiabilitiesFrederick AbellaNo ratings yet

- Module 2 - Assessment ActivitiesDocument3 pagesModule 2 - Assessment Activitiesaj dumpNo ratings yet

- Handouts 04.04 - Part 3Document3 pagesHandouts 04.04 - Part 3John Ray RonaNo ratings yet

- Exercises - Wasting Assets, Borrowing Costs, and Government GrantsDocument3 pagesExercises - Wasting Assets, Borrowing Costs, and Government GrantsMeeka CalimagNo ratings yet

- Dado BpsDocument6 pagesDado BpsmcannielNo ratings yet

- Practical Accounting 1Document6 pagesPractical Accounting 1Myiel AngelNo ratings yet

- IA PPE (Unit Test)Document10 pagesIA PPE (Unit Test)Nina MarieNo ratings yet

- Prelims QuizDocument12 pagesPrelims QuizJanine TupasiNo ratings yet

- Final Exam W MCQDocument12 pagesFinal Exam W MCQPatrick SalvadorNo ratings yet

- 1.2 Factors Impacting International Business OperationsDocument37 pages1.2 Factors Impacting International Business OperationsCharles TuazonNo ratings yet

- Business Report TopicsDocument4 pagesBusiness Report TopicsCharles TuazonNo ratings yet

- 1.1 Overview of International BusinessDocument27 pages1.1 Overview of International BusinessCharles TuazonNo ratings yet

- Dela Cruz - Cloud Computing-1Document4 pagesDela Cruz - Cloud Computing-1Charles TuazonNo ratings yet

- Content ServerDocument26 pagesContent ServerCharles TuazonNo ratings yet

- Updated Annual Per Capita Poverty Threshold Poverty Incidence and Magnitude of Poor FamiDocument32 pagesUpdated Annual Per Capita Poverty Threshold Poverty Incidence and Magnitude of Poor FamiCharles TuazonNo ratings yet

- IAASB Main Agenda (September 2004) Page 2004 1949: Prepared By: Alta Prinsloo (August 2004)Document22 pagesIAASB Main Agenda (September 2004) Page 2004 1949: Prepared By: Alta Prinsloo (August 2004)Charles TuazonNo ratings yet

- PDF h02 Pre TestDocument8 pagesPDF h02 Pre TestCharles TuazonNo ratings yet

- Student-Reports and OpinionDocument44 pagesStudent-Reports and OpinionCharles TuazonNo ratings yet

- 28S32 High Acres LF 2017.2018-03-01.ARDocument144 pages28S32 High Acres LF 2017.2018-03-01.ARCharles TuazonNo ratings yet

- (Final) 11072018 CNPF 17Q Ytd Nine Months 2018Document59 pages(Final) 11072018 CNPF 17Q Ytd Nine Months 2018Charles TuazonNo ratings yet

- AFI Infographics - SignedDocument1 pageAFI Infographics - SignedCharles TuazonNo ratings yet

- Gratittude Manufacturing Company Post-Closing Trial Balance DECEMBER 31, 2017Document3 pagesGratittude Manufacturing Company Post-Closing Trial Balance DECEMBER 31, 2017Charles TuazonNo ratings yet

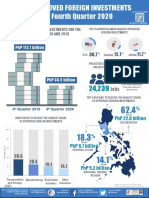

- AFI Infographics - Q4 2020 - SignedDocument1 pageAFI Infographics - Q4 2020 - SignedCharles TuazonNo ratings yet

- Chap 04 Linear RegressionDocument99 pagesChap 04 Linear RegressionCharles TuazonNo ratings yet

- MT Set A PDFDocument6 pagesMT Set A PDFCharles TuazonNo ratings yet

- Tax1 (T31920)Document82 pagesTax1 (T31920)Charles TuazonNo ratings yet

- Q3 WRKSHT Perpetual PDFDocument1 pageQ3 WRKSHT Perpetual PDFCharles TuazonNo ratings yet

- Q1 Set B PDFDocument5 pagesQ1 Set B PDFCharles TuazonNo ratings yet

- LQ2 Set B PDFDocument5 pagesLQ2 Set B PDFCharles TuazonNo ratings yet

- Sample Problem SolvingDocument2 pagesSample Problem SolvingCharles TuazonNo ratings yet

- Partnership Liquidation: Steps Involved in LiquidationDocument13 pagesPartnership Liquidation: Steps Involved in LiquidationCharles TuazonNo ratings yet

- Sir DanteDocument10 pagesSir DanteRhee LigutanNo ratings yet

- CH 2 To CH 6 Beyt Gunniting June21Document49 pagesCH 2 To CH 6 Beyt Gunniting June21Arju SinghNo ratings yet

- Aromânii Din Albania (Cultural Association Aromanians of Albania)Document25 pagesAromânii Din Albania (Cultural Association Aromanians of Albania)valer_crushuveanluNo ratings yet

- Progress Test GD1604Document5 pagesProgress Test GD1604Tran Thi Thuy (K15 HL)No ratings yet

- Macedo 2020Document18 pagesMacedo 2020wahyu indrajayaNo ratings yet

- Letter Request GPPDocument2 pagesLetter Request GPPVoltairNo ratings yet

- Hue As A Traditional City of VietnamDocument18 pagesHue As A Traditional City of VietnamPhi Yen NguyenNo ratings yet

- Criminal Law AssignmentDocument7 pagesCriminal Law AssignmentMusaibNo ratings yet

- Diversity Management: Case One Anthony Byrum Florida State College at Jacksonville April 5, 2020 Antionette RichardsonDocument7 pagesDiversity Management: Case One Anthony Byrum Florida State College at Jacksonville April 5, 2020 Antionette RichardsonSteven AnthonyByrumNo ratings yet

- Reflective EssayDocument8 pagesReflective EssayDiana Elizabeth P. OllerNo ratings yet

- Chapter 26 Section 2 and 3 AnnotatedDocument2 pagesChapter 26 Section 2 and 3 AnnotatedMelody ConklinNo ratings yet

- Jurnal Ilmu SosialDocument11 pagesJurnal Ilmu SosialBudi SetiyoNo ratings yet

- 2 GNLUJLDev Pol 136Document7 pages2 GNLUJLDev Pol 136Sejal LahotiNo ratings yet

- Providence Response To Sen Murray Inquiry - FINALDocument6 pagesProvidence Response To Sen Murray Inquiry - FINALJakob EmersonNo ratings yet

- Pestle AnalysisDocument3 pagesPestle AnalysisATUL AB100% (1)

- Bhaurao Lokhande v. State of MaharashtraDocument2 pagesBhaurao Lokhande v. State of MaharashtraShravan Niranjan100% (1)

- Redcliffe AwardDocument12 pagesRedcliffe AwardNasir AkhtarNo ratings yet

- Sweet Water Stabbing FlyerDocument1 pageSweet Water Stabbing Flyermichael_miller700No ratings yet

- Aprilyn Aquino SOCSCI 2125 Assignment For Reading 01Document2 pagesAprilyn Aquino SOCSCI 2125 Assignment For Reading 01Aprilyn AquinoNo ratings yet

- RAJBHASHA Hindi TrainingDocument3 pagesRAJBHASHA Hindi Trainingengineering controlNo ratings yet

- Potlatch ProductDocument12 pagesPotlatch Productapi-634988536No ratings yet

- Chemical Safety in Your Community:: EPA's New Risk Management ProgramDocument12 pagesChemical Safety in Your Community:: EPA's New Risk Management ProgramFelipe GuioNo ratings yet

- 2014 NEC Electrical Instructor Manual and Student Worksheets Level 1 - PDFDocument352 pages2014 NEC Electrical Instructor Manual and Student Worksheets Level 1 - PDFLimuel Espiritu0% (1)

- 2020-TA-d-ALL (Local 308)Document5 pages2020-TA-d-ALL (Local 308)Chicago Transit Justice CoalitionNo ratings yet

- Chapter 1: Project BackgroundDocument4 pagesChapter 1: Project BackgroundKevin OngjuncoNo ratings yet

- Ligon V City of New York (Stop and Frisk Case)Document3 pagesLigon V City of New York (Stop and Frisk Case)Roger ParloffNo ratings yet

- Property and Modes of Acquiring OwnershipDocument17 pagesProperty and Modes of Acquiring OwnershipLeonor LeonorNo ratings yet

- Writ - C No. - 35475 of 2016 Angel Mercury Apartment Owners Association v. Ghaziabad Development AuthorityDocument1 pageWrit - C No. - 35475 of 2016 Angel Mercury Apartment Owners Association v. Ghaziabad Development AuthorityAdharsh VenkatesanNo ratings yet

- IEC Anti Illegal DrugDocument3 pagesIEC Anti Illegal DrugBarangay CawagNo ratings yet