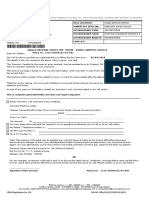

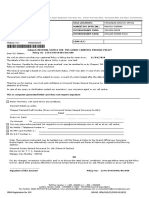

Food Corporation of India Fire Declaration Policy FY 23-24 - 0404011123P102167906

Food Corporation of India Fire Declaration Policy FY 23-24 - 0404011123P102167906

You might also like

- Handbook of Theories of Aging PDFDocument535 pagesHandbook of Theories of Aging PDFYvonne Yap Ying Ying100% (3)

- The Life and Ministry of Apostle PeterDocument113 pagesThe Life and Ministry of Apostle PeterDukejack100% (1)

- Pol 4232643Document3 pagesPol 4232643Ramanuja GanguNo ratings yet

- United India Insurance Company Limited: M/S Kadambri InternationalDocument8 pagesUnited India Insurance Company Limited: M/S Kadambri InternationalReema KhatiNo ratings yet

- Mrs. Shashi Chopra Fire Policy (20-21)Document8 pagesMrs. Shashi Chopra Fire Policy (20-21)Reema KhatiNo ratings yet

- United India Insurance Company LimitedDocument10 pagesUnited India Insurance Company LimitedGOVIND CNo ratings yet

- Standard Fire and Special Perils Policy Schedule Cum Tax Invoice Indian Overseas Bank 200471025418 44 28191102 Healthcare@iobnet - Co.in 271901Document2 pagesStandard Fire and Special Perils Policy Schedule Cum Tax Invoice Indian Overseas Bank 200471025418 44 28191102 Healthcare@iobnet - Co.in 271901Dipak Madhukar KambleNo ratings yet

- United India Insurance Company Limited: Ms Sahasareddy Filling StationDocument3 pagesUnited India Insurance Company Limited: Ms Sahasareddy Filling StationchandraNo ratings yet

- Pravin Lathiya Pragati FabDocument10 pagesPravin Lathiya Pragati FabMilin0606No ratings yet

- GMC Policy 2019-2020Document32 pagesGMC Policy 2019-2020amit_264No ratings yet

- RN02Document10 pagesRN02Adesh yadavNo ratings yet

- United India Insurance Company Limited: Mumbai - 400021 Maharashtra PH: (022) 22822394, (022) 49799210 FAX: EMAILDocument6 pagesUnited India Insurance Company Limited: Mumbai - 400021 Maharashtra PH: (022) 22822394, (022) 49799210 FAX: EMAILtyujvuiyNo ratings yet

- Badhkummed Indane Gramin Vitark-21-22Document9 pagesBadhkummed Indane Gramin Vitark-21-22gera 0734No ratings yet

- Liberty General Insurance Limited: Insured Motor Vehicle Details and Premium ComputationDocument1 pageLiberty General Insurance Limited: Insured Motor Vehicle Details and Premium ComputationSwornamayee SethiNo ratings yet

- We Value Your Relationship With ICICI Lombard General Insurance Company Limited and Thank You For Choosing Us As Your Preferred Insurance ProviderDocument3 pagesWe Value Your Relationship With ICICI Lombard General Insurance Company Limited and Thank You For Choosing Us As Your Preferred Insurance Providersohamnaik649No ratings yet

- All Risk PolicyDocument25 pagesAll Risk PolicyPlanning DAPLNo ratings yet

- United India Insurance Company Limited: POLICY NO.: 0901814220P111699098Document3 pagesUnited India Insurance Company Limited: POLICY NO.: 0901814220P111699098Deepan RajNo ratings yet

- Policy DocumentDocument3 pagesPolicy Documentsunil dhangarNo ratings yet

- Future Generali India Insurance Company Limited, Corporate & Registered Office: 6th Floor, Tower - 3, Indiabulls Finance Center, Senapati Bapat MargDocument6 pagesFuture Generali India Insurance Company Limited, Corporate & Registered Office: 6th Floor, Tower - 3, Indiabulls Finance Center, Senapati Bapat MargKapil SoniNo ratings yet

- Iffco AGSA Springs Final QuoteDocument2 pagesIffco AGSA Springs Final Quoteavi.kadam25No ratings yet

- United India Insurance Company Limited: MR DR Shaina PrasadDocument7 pagesUnited India Insurance Company Limited: MR DR Shaina PrasadKoylanchal i9 Eye & Dental Center DhanbadNo ratings yet

- United India Insurance Company Limited: POLICY NO.: 0901814220P111699960Document3 pagesUnited India Insurance Company Limited: POLICY NO.: 0901814220P111699960Deepan RajNo ratings yet

- WC Policy SingrauliDocument3 pagesWC Policy Singrauliskaurravneet1No ratings yet

- Sub: Standard Fire and Special Perils Insurance Policy No. 2111202738793400000Document7 pagesSub: Standard Fire and Special Perils Insurance Policy No. 2111202738793400000KrishnaNo ratings yet

- Activa Insurance DocumentDocument6 pagesActiva Insurance DocumentthakuryaNo ratings yet

- Policy - Car Insurance SwiftDocument11 pagesPolicy - Car Insurance Swiftavanthi.surNo ratings yet

- Tata AigDocument3 pagesTata AigAshik IkbalNo ratings yet

- A Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur InvestmentsDocument2 pagesA Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur Investmentscommission sompoNo ratings yet

- A Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur InvestmentsDocument2 pagesA Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur Investmentscommission sompoNo ratings yet

- Agent Name Khivraj Motors Agent Code MIS1000132 Agent Contact No 9108694880Document2 pagesAgent Name Khivraj Motors Agent Code MIS1000132 Agent Contact No 9108694880SanthoshNo ratings yet

- 9616Document2 pages9616Raj KumarNo ratings yet

- United India Insurance Company Limited: M/ Weld Care NDT Inspection ServicesDocument3 pagesUnited India Insurance Company Limited: M/ Weld Care NDT Inspection ServicesDeepan RajNo ratings yet

- Policy 468140003 1899483072595Document1 pagePolicy 468140003 1899483072595Ishan AnandNo ratings yet

- Policy Number:130422223470023187 Proposal/Covernote No:R02072248064Document7 pagesPolicy Number:130422223470023187 Proposal/Covernote No:R02072248064Persflt OpsAINo ratings yet

- InsuranceDocument6 pagesInsurancesourabhNo ratings yet

- HDFC ERGO General Insurance Company Limited: Certificate No. 2045660330000202898400 Certificate of InsuranceDocument2 pagesHDFC ERGO General Insurance Company Limited: Certificate No. 2045660330000202898400 Certificate of InsurancePrateek MondolNo ratings yet

- Policy 578814106 3608578480656Document3 pagesPolicy 578814106 3608578480656uuserhere86No ratings yet

- Versosarichard SindejasDocument1 pageVersosarichard SindejasDorothy NaongNo ratings yet

- 979 PrintersDocument3 pages979 Printerssamidh MorariNo ratings yet

- Policy Number: 110522223080023525 Proposal/Covernote No: R03032239832Document6 pagesPolicy Number: 110522223080023525 Proposal/Covernote No: R03032239832KUMARNo ratings yet

- HDFC ERGO General Insurance Company Limited: Certificate No. 2045660330000201422100 Certificate of InsuranceDocument2 pagesHDFC ERGO General Insurance Company Limited: Certificate No. 2045660330000201422100 Certificate of InsurancePrateek MondolNo ratings yet

- INS 1673863254 PolicydocDocument6 pagesINS 1673863254 Policydocajayparmar015No ratings yet

- Sub: Risk Assumption Letter: Insured & Vehicle DetailsDocument3 pagesSub: Risk Assumption Letter: Insured & Vehicle Detailsl48117733No ratings yet

- A Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur InvestmentsDocument2 pagesA Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur Investmentscommission sompoNo ratings yet

- Group Mediclaim PolicyDocument3 pagesGroup Mediclaim PolicyAman AgrawalNo ratings yet

- United India Insurance Company LimitedDocument9 pagesUnited India Insurance Company LimitedSankar NatarajanNo ratings yet

- Group Mediclaim Tailormade - Endorsement ScheduleDocument2 pagesGroup Mediclaim Tailormade - Endorsement ScheduleSneha SinghNo ratings yet

- Two Wheeler Standalone OD Only: Certificate of Insurance Cum Policy ScheduleDocument3 pagesTwo Wheeler Standalone OD Only: Certificate of Insurance Cum Policy Scheduleprasanth adabalaNo ratings yet

- Strategic ManagementDocument5 pagesStrategic ManagementSubrat SahooNo ratings yet

- 2 PDFDocument5 pages2 PDFSubrat SahooNo ratings yet

- Mr. Amar Shaukat Mujawar A P Palus Maruti Chowk Palus Tal Palus Dist Sangli Palus MAHARASHTRA India - 416310 9113Document8 pagesMr. Amar Shaukat Mujawar A P Palus Maruti Chowk Palus Tal Palus Dist Sangli Palus MAHARASHTRA India - 416310 9113jaibababake880No ratings yet

- Sub: Risk Assumption Letter: Insured & Vehicle DetailsDocument3 pagesSub: Risk Assumption Letter: Insured & Vehicle Detailsl48117733No ratings yet

- Policy No 26020531196210020451 Proposal No. & Date Policy Issued On Period of Insurance Insured Name Previous Policy No. Insured Add Previous InsurerDocument2 pagesPolicy No 26020531196210020451 Proposal No. & Date Policy Issued On Period of Insurance Insured Name Previous Policy No. Insured Add Previous InsurerSanjay SharmaNo ratings yet

- Car Insurance 2017-18Document2 pagesCar Insurance 2017-18Nithin KumarNo ratings yet

- Mgomahinog-06-21-01 SF-4647Document1 pageMgomahinog-06-21-01 SF-4647LGU MAHINOG MTONo ratings yet

- Policy No. Name Address:: 7000054772-02: MR Arbind Kumar Sinha: F-3,202 Shankeshwar Nagar, Manpad RoadDocument18 pagesPolicy No. Name Address:: 7000054772-02: MR Arbind Kumar Sinha: F-3,202 Shankeshwar Nagar, Manpad Roadbinitasinha100No ratings yet

- INS 1697949920 PolicydocDocument8 pagesINS 1697949920 Policydocmukeshsingh870801No ratings yet

- Sub: Risk Assumption Letter: Insured & Vehicle DetailsDocument3 pagesSub: Risk Assumption Letter: Insured & Vehicle Detailssaddam khanNo ratings yet

- Fire-Surya ElectricalDocument6 pagesFire-Surya ElectricalSURAJ PratapNo ratings yet

- Limite D: Reliance Private Car Package Policy-ScheduleDocument9 pagesLimite D: Reliance Private Car Package Policy-Schedulesukhpreet singhNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaNo ratings yet

- Nahuatl Grammar Veracruz 2d Edition WolgemuthDocument169 pagesNahuatl Grammar Veracruz 2d Edition WolgemuthWilfrido Barajas100% (1)

- Learning EvidenceDocument5 pagesLearning EvidenceArtperture Fotografía100% (3)

- Criteria Heritage BuildingsDocument2 pagesCriteria Heritage BuildingsAkilan DhayalanNo ratings yet

- Course Module EL. 107 Week 2Document22 pagesCourse Module EL. 107 Week 2Joevannie AceraNo ratings yet

- 750 GPM - 205 PSI - Dimensiones Bomba 5-1823AF y Motor Clarke JU6H-UF54Document1 page750 GPM - 205 PSI - Dimensiones Bomba 5-1823AF y Motor Clarke JU6H-UF54Carlos_MKTRNo ratings yet

- Cowley Julian - Modern English LiteratureDocument107 pagesCowley Julian - Modern English LiteratureAna M. JingaNo ratings yet

- Syllabus - PAPER 1 - Application of Computer in MediaDocument39 pagesSyllabus - PAPER 1 - Application of Computer in MediaAbubakar shomarNo ratings yet

- Aud679 - Q - S1 Feb 2022Document5 pagesAud679 - Q - S1 Feb 2022NURUL IRA SHAFINAZ ARMENNo ratings yet

- Cps Sca50 60ktl Do Us 480 DatasheetDocument2 pagesCps Sca50 60ktl Do Us 480 Datasheetnelson_grandeNo ratings yet

- Self MonitoringDocument16 pagesSelf MonitoringMaroofa YounusNo ratings yet

- Work Energy PowerDocument47 pagesWork Energy PowerHemant ChaudhariNo ratings yet

- Quantitative DopplerDocument4 pagesQuantitative DopplerBarthélemy HoubenNo ratings yet

- Artificial Intelligence & Machine Learning: Career GuideDocument18 pagesArtificial Intelligence & Machine Learning: Career Guidekallol100% (1)

- Ala-Too International University 2020-2021 Spring Semester Course Timetable of Management Final ExaminationDocument8 pagesAla-Too International University 2020-2021 Spring Semester Course Timetable of Management Final ExaminationKunduz IbraevaNo ratings yet

- Indebted Part 2 The Virgin The Bad Boy Sadie BlackDocument296 pagesIndebted Part 2 The Virgin The Bad Boy Sadie BlackVidhya R100% (2)

- PI Berlin - 2023 PV Module Quality ReportDocument6 pagesPI Berlin - 2023 PV Module Quality ReportIntekhabNo ratings yet

- Adolescent Girls' Nutrition and Prevention of Anaemia: A School Based Multisectoral Collaboration in IndonesiaDocument6 pagesAdolescent Girls' Nutrition and Prevention of Anaemia: A School Based Multisectoral Collaboration in IndonesiamamaazkaNo ratings yet

- What Is An IP AddressDocument4 pagesWhat Is An IP Addresschandvinay_singhNo ratings yet

- Basics of ProgrammingDocument126 pagesBasics of ProgrammingabinayaNo ratings yet

- Collibra Prescriptive Path v2Document4 pagesCollibra Prescriptive Path v2AhamedSharifNo ratings yet

- Unit 1 - Climate and Human ComfortDocument60 pagesUnit 1 - Climate and Human ComfortVamsi KrishnaNo ratings yet

- Ulangan Harian Bab 1Document2 pagesUlangan Harian Bab 1Anwar90% (10)

- Conferencia Project Finance. Juan David González RuizDocument2 pagesConferencia Project Finance. Juan David González RuizErnesto CanoNo ratings yet

- Blood Bank Management System Research PaperDocument8 pagesBlood Bank Management System Research Paperbgmihack4253No ratings yet

- Military Service: The Ministry of Aliyah and Immigrant AbsorptionDocument64 pagesMilitary Service: The Ministry of Aliyah and Immigrant AbsorptionKERVIN6831117No ratings yet

- 545 Znshine PDFDocument2 pages545 Znshine PDFDS INSTALAÇÕES ELÉTRICASNo ratings yet

- Lab 10 Access ListDocument4 pagesLab 10 Access Listanurag sawarnNo ratings yet

- Ranisch Sorgner Posthumanism IntroductionDocument316 pagesRanisch Sorgner Posthumanism IntroductionЕсения КалининаNo ratings yet

Download as pdf or txt

You might also like

- Handbook of Theories of Aging PDFDocument535 pagesHandbook of Theories of Aging PDFYvonne Yap Ying Ying100% (3)

- The Life and Ministry of Apostle PeterDocument113 pagesThe Life and Ministry of Apostle PeterDukejack100% (1)

- Pol 4232643Document3 pagesPol 4232643Ramanuja GanguNo ratings yet

- United India Insurance Company Limited: M/S Kadambri InternationalDocument8 pagesUnited India Insurance Company Limited: M/S Kadambri InternationalReema KhatiNo ratings yet

- Mrs. Shashi Chopra Fire Policy (20-21)Document8 pagesMrs. Shashi Chopra Fire Policy (20-21)Reema KhatiNo ratings yet

- United India Insurance Company LimitedDocument10 pagesUnited India Insurance Company LimitedGOVIND CNo ratings yet

- Standard Fire and Special Perils Policy Schedule Cum Tax Invoice Indian Overseas Bank 200471025418 44 28191102 Healthcare@iobnet - Co.in 271901Document2 pagesStandard Fire and Special Perils Policy Schedule Cum Tax Invoice Indian Overseas Bank 200471025418 44 28191102 Healthcare@iobnet - Co.in 271901Dipak Madhukar KambleNo ratings yet

- United India Insurance Company Limited: Ms Sahasareddy Filling StationDocument3 pagesUnited India Insurance Company Limited: Ms Sahasareddy Filling StationchandraNo ratings yet

- Pravin Lathiya Pragati FabDocument10 pagesPravin Lathiya Pragati FabMilin0606No ratings yet

- GMC Policy 2019-2020Document32 pagesGMC Policy 2019-2020amit_264No ratings yet

- RN02Document10 pagesRN02Adesh yadavNo ratings yet

- United India Insurance Company Limited: Mumbai - 400021 Maharashtra PH: (022) 22822394, (022) 49799210 FAX: EMAILDocument6 pagesUnited India Insurance Company Limited: Mumbai - 400021 Maharashtra PH: (022) 22822394, (022) 49799210 FAX: EMAILtyujvuiyNo ratings yet

- Badhkummed Indane Gramin Vitark-21-22Document9 pagesBadhkummed Indane Gramin Vitark-21-22gera 0734No ratings yet

- Liberty General Insurance Limited: Insured Motor Vehicle Details and Premium ComputationDocument1 pageLiberty General Insurance Limited: Insured Motor Vehicle Details and Premium ComputationSwornamayee SethiNo ratings yet

- We Value Your Relationship With ICICI Lombard General Insurance Company Limited and Thank You For Choosing Us As Your Preferred Insurance ProviderDocument3 pagesWe Value Your Relationship With ICICI Lombard General Insurance Company Limited and Thank You For Choosing Us As Your Preferred Insurance Providersohamnaik649No ratings yet

- All Risk PolicyDocument25 pagesAll Risk PolicyPlanning DAPLNo ratings yet

- United India Insurance Company Limited: POLICY NO.: 0901814220P111699098Document3 pagesUnited India Insurance Company Limited: POLICY NO.: 0901814220P111699098Deepan RajNo ratings yet

- Policy DocumentDocument3 pagesPolicy Documentsunil dhangarNo ratings yet

- Future Generali India Insurance Company Limited, Corporate & Registered Office: 6th Floor, Tower - 3, Indiabulls Finance Center, Senapati Bapat MargDocument6 pagesFuture Generali India Insurance Company Limited, Corporate & Registered Office: 6th Floor, Tower - 3, Indiabulls Finance Center, Senapati Bapat MargKapil SoniNo ratings yet

- Iffco AGSA Springs Final QuoteDocument2 pagesIffco AGSA Springs Final Quoteavi.kadam25No ratings yet

- United India Insurance Company Limited: MR DR Shaina PrasadDocument7 pagesUnited India Insurance Company Limited: MR DR Shaina PrasadKoylanchal i9 Eye & Dental Center DhanbadNo ratings yet

- United India Insurance Company Limited: POLICY NO.: 0901814220P111699960Document3 pagesUnited India Insurance Company Limited: POLICY NO.: 0901814220P111699960Deepan RajNo ratings yet

- WC Policy SingrauliDocument3 pagesWC Policy Singrauliskaurravneet1No ratings yet

- Sub: Standard Fire and Special Perils Insurance Policy No. 2111202738793400000Document7 pagesSub: Standard Fire and Special Perils Insurance Policy No. 2111202738793400000KrishnaNo ratings yet

- Activa Insurance DocumentDocument6 pagesActiva Insurance DocumentthakuryaNo ratings yet

- Policy - Car Insurance SwiftDocument11 pagesPolicy - Car Insurance Swiftavanthi.surNo ratings yet

- Tata AigDocument3 pagesTata AigAshik IkbalNo ratings yet

- A Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur InvestmentsDocument2 pagesA Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur Investmentscommission sompoNo ratings yet

- A Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur InvestmentsDocument2 pagesA Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur Investmentscommission sompoNo ratings yet

- Agent Name Khivraj Motors Agent Code MIS1000132 Agent Contact No 9108694880Document2 pagesAgent Name Khivraj Motors Agent Code MIS1000132 Agent Contact No 9108694880SanthoshNo ratings yet

- 9616Document2 pages9616Raj KumarNo ratings yet

- United India Insurance Company Limited: M/ Weld Care NDT Inspection ServicesDocument3 pagesUnited India Insurance Company Limited: M/ Weld Care NDT Inspection ServicesDeepan RajNo ratings yet

- Policy 468140003 1899483072595Document1 pagePolicy 468140003 1899483072595Ishan AnandNo ratings yet

- Policy Number:130422223470023187 Proposal/Covernote No:R02072248064Document7 pagesPolicy Number:130422223470023187 Proposal/Covernote No:R02072248064Persflt OpsAINo ratings yet

- InsuranceDocument6 pagesInsurancesourabhNo ratings yet

- HDFC ERGO General Insurance Company Limited: Certificate No. 2045660330000202898400 Certificate of InsuranceDocument2 pagesHDFC ERGO General Insurance Company Limited: Certificate No. 2045660330000202898400 Certificate of InsurancePrateek MondolNo ratings yet

- Policy 578814106 3608578480656Document3 pagesPolicy 578814106 3608578480656uuserhere86No ratings yet

- Versosarichard SindejasDocument1 pageVersosarichard SindejasDorothy NaongNo ratings yet

- 979 PrintersDocument3 pages979 Printerssamidh MorariNo ratings yet

- Policy Number: 110522223080023525 Proposal/Covernote No: R03032239832Document6 pagesPolicy Number: 110522223080023525 Proposal/Covernote No: R03032239832KUMARNo ratings yet

- HDFC ERGO General Insurance Company Limited: Certificate No. 2045660330000201422100 Certificate of InsuranceDocument2 pagesHDFC ERGO General Insurance Company Limited: Certificate No. 2045660330000201422100 Certificate of InsurancePrateek MondolNo ratings yet

- INS 1673863254 PolicydocDocument6 pagesINS 1673863254 Policydocajayparmar015No ratings yet

- Sub: Risk Assumption Letter: Insured & Vehicle DetailsDocument3 pagesSub: Risk Assumption Letter: Insured & Vehicle Detailsl48117733No ratings yet

- A Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur InvestmentsDocument2 pagesA Joint Venture Between Allahabad Bank, Sompo Japan Nipponkoa Insurance Inc., Indian Overseas Bank, Karnataka Bank and Dabur Investmentscommission sompoNo ratings yet

- Group Mediclaim PolicyDocument3 pagesGroup Mediclaim PolicyAman AgrawalNo ratings yet

- United India Insurance Company LimitedDocument9 pagesUnited India Insurance Company LimitedSankar NatarajanNo ratings yet

- Group Mediclaim Tailormade - Endorsement ScheduleDocument2 pagesGroup Mediclaim Tailormade - Endorsement ScheduleSneha SinghNo ratings yet

- Two Wheeler Standalone OD Only: Certificate of Insurance Cum Policy ScheduleDocument3 pagesTwo Wheeler Standalone OD Only: Certificate of Insurance Cum Policy Scheduleprasanth adabalaNo ratings yet

- Strategic ManagementDocument5 pagesStrategic ManagementSubrat SahooNo ratings yet

- 2 PDFDocument5 pages2 PDFSubrat SahooNo ratings yet

- Mr. Amar Shaukat Mujawar A P Palus Maruti Chowk Palus Tal Palus Dist Sangli Palus MAHARASHTRA India - 416310 9113Document8 pagesMr. Amar Shaukat Mujawar A P Palus Maruti Chowk Palus Tal Palus Dist Sangli Palus MAHARASHTRA India - 416310 9113jaibababake880No ratings yet

- Sub: Risk Assumption Letter: Insured & Vehicle DetailsDocument3 pagesSub: Risk Assumption Letter: Insured & Vehicle Detailsl48117733No ratings yet

- Policy No 26020531196210020451 Proposal No. & Date Policy Issued On Period of Insurance Insured Name Previous Policy No. Insured Add Previous InsurerDocument2 pagesPolicy No 26020531196210020451 Proposal No. & Date Policy Issued On Period of Insurance Insured Name Previous Policy No. Insured Add Previous InsurerSanjay SharmaNo ratings yet

- Car Insurance 2017-18Document2 pagesCar Insurance 2017-18Nithin KumarNo ratings yet

- Mgomahinog-06-21-01 SF-4647Document1 pageMgomahinog-06-21-01 SF-4647LGU MAHINOG MTONo ratings yet

- Policy No. Name Address:: 7000054772-02: MR Arbind Kumar Sinha: F-3,202 Shankeshwar Nagar, Manpad RoadDocument18 pagesPolicy No. Name Address:: 7000054772-02: MR Arbind Kumar Sinha: F-3,202 Shankeshwar Nagar, Manpad Roadbinitasinha100No ratings yet

- INS 1697949920 PolicydocDocument8 pagesINS 1697949920 Policydocmukeshsingh870801No ratings yet

- Sub: Risk Assumption Letter: Insured & Vehicle DetailsDocument3 pagesSub: Risk Assumption Letter: Insured & Vehicle Detailssaddam khanNo ratings yet

- Fire-Surya ElectricalDocument6 pagesFire-Surya ElectricalSURAJ PratapNo ratings yet

- Limite D: Reliance Private Car Package Policy-ScheduleDocument9 pagesLimite D: Reliance Private Car Package Policy-Schedulesukhpreet singhNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaNo ratings yet

- Nahuatl Grammar Veracruz 2d Edition WolgemuthDocument169 pagesNahuatl Grammar Veracruz 2d Edition WolgemuthWilfrido Barajas100% (1)

- Learning EvidenceDocument5 pagesLearning EvidenceArtperture Fotografía100% (3)

- Criteria Heritage BuildingsDocument2 pagesCriteria Heritage BuildingsAkilan DhayalanNo ratings yet

- Course Module EL. 107 Week 2Document22 pagesCourse Module EL. 107 Week 2Joevannie AceraNo ratings yet

- 750 GPM - 205 PSI - Dimensiones Bomba 5-1823AF y Motor Clarke JU6H-UF54Document1 page750 GPM - 205 PSI - Dimensiones Bomba 5-1823AF y Motor Clarke JU6H-UF54Carlos_MKTRNo ratings yet

- Cowley Julian - Modern English LiteratureDocument107 pagesCowley Julian - Modern English LiteratureAna M. JingaNo ratings yet

- Syllabus - PAPER 1 - Application of Computer in MediaDocument39 pagesSyllabus - PAPER 1 - Application of Computer in MediaAbubakar shomarNo ratings yet

- Aud679 - Q - S1 Feb 2022Document5 pagesAud679 - Q - S1 Feb 2022NURUL IRA SHAFINAZ ARMENNo ratings yet

- Cps Sca50 60ktl Do Us 480 DatasheetDocument2 pagesCps Sca50 60ktl Do Us 480 Datasheetnelson_grandeNo ratings yet

- Self MonitoringDocument16 pagesSelf MonitoringMaroofa YounusNo ratings yet

- Work Energy PowerDocument47 pagesWork Energy PowerHemant ChaudhariNo ratings yet

- Quantitative DopplerDocument4 pagesQuantitative DopplerBarthélemy HoubenNo ratings yet

- Artificial Intelligence & Machine Learning: Career GuideDocument18 pagesArtificial Intelligence & Machine Learning: Career Guidekallol100% (1)

- Ala-Too International University 2020-2021 Spring Semester Course Timetable of Management Final ExaminationDocument8 pagesAla-Too International University 2020-2021 Spring Semester Course Timetable of Management Final ExaminationKunduz IbraevaNo ratings yet

- Indebted Part 2 The Virgin The Bad Boy Sadie BlackDocument296 pagesIndebted Part 2 The Virgin The Bad Boy Sadie BlackVidhya R100% (2)

- PI Berlin - 2023 PV Module Quality ReportDocument6 pagesPI Berlin - 2023 PV Module Quality ReportIntekhabNo ratings yet

- Adolescent Girls' Nutrition and Prevention of Anaemia: A School Based Multisectoral Collaboration in IndonesiaDocument6 pagesAdolescent Girls' Nutrition and Prevention of Anaemia: A School Based Multisectoral Collaboration in IndonesiamamaazkaNo ratings yet

- What Is An IP AddressDocument4 pagesWhat Is An IP Addresschandvinay_singhNo ratings yet

- Basics of ProgrammingDocument126 pagesBasics of ProgrammingabinayaNo ratings yet

- Collibra Prescriptive Path v2Document4 pagesCollibra Prescriptive Path v2AhamedSharifNo ratings yet

- Unit 1 - Climate and Human ComfortDocument60 pagesUnit 1 - Climate and Human ComfortVamsi KrishnaNo ratings yet

- Ulangan Harian Bab 1Document2 pagesUlangan Harian Bab 1Anwar90% (10)

- Conferencia Project Finance. Juan David González RuizDocument2 pagesConferencia Project Finance. Juan David González RuizErnesto CanoNo ratings yet

- Blood Bank Management System Research PaperDocument8 pagesBlood Bank Management System Research Paperbgmihack4253No ratings yet

- Military Service: The Ministry of Aliyah and Immigrant AbsorptionDocument64 pagesMilitary Service: The Ministry of Aliyah and Immigrant AbsorptionKERVIN6831117No ratings yet

- 545 Znshine PDFDocument2 pages545 Znshine PDFDS INSTALAÇÕES ELÉTRICASNo ratings yet

- Lab 10 Access ListDocument4 pagesLab 10 Access Listanurag sawarnNo ratings yet

- Ranisch Sorgner Posthumanism IntroductionDocument316 pagesRanisch Sorgner Posthumanism IntroductionЕсения КалининаNo ratings yet