Download as pdf or txt

You might also like

- The Safe Mortgage Loan Originator National Exam Study Guide Second Edition 2nd Edition Ebook PDFDocument62 pagesThe Safe Mortgage Loan Originator National Exam Study Guide Second Edition 2nd Edition Ebook PDFalec.black13997% (37)

- Whole Loan Book Entry White Paper: A Blueprint For The Future, 1993 Whitepaper - Phyllis K SlesingerDocument3 pagesWhole Loan Book Entry White Paper: A Blueprint For The Future, 1993 Whitepaper - Phyllis K SlesingerTim BryantNo ratings yet

- Cash App - Apps On Google PlayDocument1 pageCash App - Apps On Google PlayMr McMahonNo ratings yet

- 20-Hour MLO Course OutlineDocument34 pages20-Hour MLO Course OutlinethemufiNo ratings yet

- Bankers AcceptancesDocument36 pagesBankers AcceptancesAlexhCreditor100% (1)

- Internship - Report - On - E - Banking - For Merge05Document63 pagesInternship - Report - On - E - Banking - For Merge05ঘুম বাবুNo ratings yet

- Alphabet Soup:: Hmda and Fcra/Fact ActDocument20 pagesAlphabet Soup:: Hmda and Fcra/Fact ActCairo AnubissNo ratings yet

- Fair Credit Reporting Act: Joseph L. Barloon Skadden, Arps, Slate, Meagher & Flom LLPDocument23 pagesFair Credit Reporting Act: Joseph L. Barloon Skadden, Arps, Slate, Meagher & Flom LLPCairo AnubissNo ratings yet

- MBA Regulatory Compliance Conference 2011: Litigation Concerns For The Compliance Professional, Including Fair Lending and Other ClaimsDocument31 pagesMBA Regulatory Compliance Conference 2011: Litigation Concerns For The Compliance Professional, Including Fair Lending and Other ClaimsCairo AnubissNo ratings yet

- MBA Regulatory Compliance Conference 2011 Litigation Forum - Session 4: EnforcementDocument24 pagesMBA Regulatory Compliance Conference 2011 Litigation Forum - Session 4: EnforcementCairo AnubissNo ratings yet

- OCC Feb 2010 Home Mortgage Disclosure HandbookDocument30 pagesOCC Feb 2010 Home Mortgage Disclosure Handbook83jjmackNo ratings yet

- Selected FCRA and Privacy Developments MBA Legal Issues Conference May 5, 2010Document26 pagesSelected FCRA and Privacy Developments MBA Legal Issues Conference May 5, 2010Cairo AnubissNo ratings yet

- Topic 4 Cisa, Dpa and TilaDocument49 pagesTopic 4 Cisa, Dpa and TilaGlaiza Marie CaliseNo ratings yet

- New Credit Card Law: BasicsDocument2 pagesNew Credit Card Law: BasicsJerry419No ratings yet

- Nmls Ce Course - Module 1Document33 pagesNmls Ce Course - Module 1charger1234100% (2)

- National Association of Retail Collection Attorneys (Narca) Comments For Federal Trade Commission Debt Collection WorkshopDocument17 pagesNational Association of Retail Collection Attorneys (Narca) Comments For Federal Trade Commission Debt Collection WorkshopJillian SheridanNo ratings yet

- Consumer IssuesDocument67 pagesConsumer IssuesWarriorpoet100% (2)

- Fair CollectionDocument65 pagesFair CollectionApurva NadkarniNo ratings yet

- CFPB - 2012 Credit Bureaus Reporting SystemDocument48 pagesCFPB - 2012 Credit Bureaus Reporting SystemCP Mario Pérez López100% (1)

- Mortgage Fair Consumer ReportingDocument9 pagesMortgage Fair Consumer ReportingBleak NarrativesNo ratings yet

- WITS Presentation - Avitha Nofal 11 November 2021Document29 pagesWITS Presentation - Avitha Nofal 11 November 2021aviNo ratings yet

- Ra 9510 PDFDocument15 pagesRa 9510 PDFkim tumanganNo ratings yet

- FACT of (2003) Analysis-FactaDocument28 pagesFACT of (2003) Analysis-FactaLaLa BanksNo ratings yet

- Module 4 - Activity ParaisoDocument2 pagesModule 4 - Activity ParaisoJulian Rose ParaisoNo ratings yet

- Julian Rose V. Paraiso BSAIS-21 Activity For Module 4: TRUTH IN LENDING ACTDocument2 pagesJulian Rose V. Paraiso BSAIS-21 Activity For Module 4: TRUTH IN LENDING ACTJulian Rose ParaisoNo ratings yet

- MBA's Regulatory Compliance Conference 2011: Workshop 1: Quick Guide To The Alphabet Soup - Federal LawsDocument21 pagesMBA's Regulatory Compliance Conference 2011: Workshop 1: Quick Guide To The Alphabet Soup - Federal LawsCairo AnubissNo ratings yet

- MBA Regulatory Compliance Conference: Renaissance Washington DC Downtown Hotel Washington, D.C. September 25, 2011Document15 pagesMBA Regulatory Compliance Conference: Renaissance Washington DC Downtown Hotel Washington, D.C. September 25, 2011Cairo AnubissNo ratings yet

- Gao Fdcpa ReportDocument66 pagesGao Fdcpa ReportMegan McAuleyNo ratings yet

- Contoh PowerpointDocument29 pagesContoh PowerpointNamanyaNo ratings yet

- What Is FCRADocument3 pagesWhat Is FCRAJorge AndrésNo ratings yet

- Summary of Mortgage Related Provisions of The Dodd-Frank Wall Street Reform and Consumer Protection ActDocument16 pagesSummary of Mortgage Related Provisions of The Dodd-Frank Wall Street Reform and Consumer Protection ActPaula HillockNo ratings yet

- Settlement USDOJ FILING News Release1Document3 pagesSettlement USDOJ FILING News Release1Razmik BoghossianNo ratings yet

- US GTM LentraDocument6 pagesUS GTM LentraNabeel MohammadNo ratings yet

- DocuSign PDFDocument7 pagesDocuSign PDFLourdesNo ratings yet

- COVID19 Impact On ConstructionDocument83 pagesCOVID19 Impact On ConstructionVEERKUMAR GNDECNo ratings yet

- MBA's 2010 Legal Issues and Regulatory Compliance Conference Hotel Del Coronado San Diego, CADocument46 pagesMBA's 2010 Legal Issues and Regulatory Compliance Conference Hotel Del Coronado San Diego, CACairo AnubissNo ratings yet

- 11-0015 Report 2Document64 pages11-0015 Report 2RecordTrac - City of OaklandNo ratings yet

- Aug 3 Amor-Bautista Credit Information CorporationDocument60 pagesAug 3 Amor-Bautista Credit Information CorporationJee JeeNo ratings yet

- The Fair Credit Reporting Act of 1970Document8 pagesThe Fair Credit Reporting Act of 1970Mercy LingatingNo ratings yet

- WCG - CRDT RPT 3 11-28-08Document2 pagesWCG - CRDT RPT 3 11-28-08Bill TaylorNo ratings yet

- MBA's Regulatory Compliance Conference 2010: Workshop 1: Quick Guide To The Alphabet SoupDocument19 pagesMBA's Regulatory Compliance Conference 2010: Workshop 1: Quick Guide To The Alphabet SoupCairo AnubissNo ratings yet

- Truth in Lending Act For Mortgage Lending: Presented April 8, 2010 Marjorie A. Corwin, EsquireDocument80 pagesTruth in Lending Act For Mortgage Lending: Presented April 8, 2010 Marjorie A. Corwin, EsquiremzieloNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument8 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledKeepy FamadorNo ratings yet

- Consumer Laws That Protect Your MoneyDocument2 pagesConsumer Laws That Protect Your MoneyDunne Law Offices, P.C.100% (2)

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument10 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledJoan PabloNo ratings yet

- National Settlement Executive SummaryDocument4 pagesNational Settlement Executive SummaryDinSFLANo ratings yet

- Credit Information SharingDocument66 pagesCredit Information SharingKoffi DenaqNo ratings yet

- SAFE Act - Gaps and Disparities Between State Licensing and Federal RegistrationDocument17 pagesSAFE Act - Gaps and Disparities Between State Licensing and Federal RegistrationCairo AnubissNo ratings yet

- Law On Microfinance To PrintDocument10 pagesLaw On Microfinance To PrintHenri KouamNo ratings yet

- National Settlement SummaryDocument4 pagesNational Settlement SummaryalmaurikanosNo ratings yet

- Defense of Collection Cases Edelman, (2007)Document43 pagesDefense of Collection Cases Edelman, (2007)Jillian Sheridan100% (2)

- BSA ManualDocument60 pagesBSA ManualSFLDNo ratings yet

- Brochure (English)Document10 pagesBrochure (English)Florentino-inez FredericksNo ratings yet

- NCA BrochureDocument10 pagesNCA BrochureFlorentino-inez FredericksNo ratings yet

- Letter To OCCDocument4 pagesLetter To OCCGeoffrey RowlandNo ratings yet

- Credit ApprovalDocument5 pagesCredit ApprovalPalaniappan MeenakshisundaramNo ratings yet

- 02 RA 9510 (The Credit Information System Act) - Secs 6, 12Document11 pages02 RA 9510 (The Credit Information System Act) - Secs 6, 12crave_bente03No ratings yet

- Finance Update - August 2003: Financial AssistanceDocument8 pagesFinance Update - August 2003: Financial AssistanceAllen ZhangNo ratings yet

- R.A. 3765 Truth in Lending Act PDFDocument5 pagesR.A. 3765 Truth in Lending Act PDFsunthatburns00No ratings yet

- Adirondack Trust and Dfs Consent OrderDocument13 pagesAdirondack Trust and Dfs Consent OrderrkarlinNo ratings yet

- Credit Information Corporation: How Did The CIC Start Operating in The Philippines?Document4 pagesCredit Information Corporation: How Did The CIC Start Operating in The Philippines?아담No ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument9 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledarvimarieNo ratings yet

- Removal of Corporate TrusteeDocument39 pagesRemoval of Corporate TrusteeCairo AnubissNo ratings yet

- SECURITIZED MORTGAGE TRUSTS (Highly Confedential) (Pandoras Box?)Document148 pagesSECURITIZED MORTGAGE TRUSTS (Highly Confedential) (Pandoras Box?)Cairo Anubiss100% (3)

- The OCC's Asset Management Conflicts of Interest 2015Document96 pagesThe OCC's Asset Management Conflicts of Interest 2015Cairo AnubissNo ratings yet

- A Practitioners Guide To Exchange Offers and Consent SolicitationDocument95 pagesA Practitioners Guide To Exchange Offers and Consent SolicitationCairo AnubissNo ratings yet

- Talush Vs Deutcsh Partial-Summary-JudgmentDocument322 pagesTalush Vs Deutcsh Partial-Summary-JudgmentCairo AnubissNo ratings yet

- UnassignedPending Civil Cases 9-15-05Document540 pagesUnassignedPending Civil Cases 9-15-05Cairo AnubissNo ratings yet

- Unaudited JP Morgan ChaseDocument78 pagesUnaudited JP Morgan ChaseCairo AnubissNo ratings yet

- Fraud Upon The Court (Disqualification of Judges)Document4 pagesFraud Upon The Court (Disqualification of Judges)Cairo Anubiss100% (4)

- Article 9 of The U.C.CDocument20 pagesArticle 9 of The U.C.CCairo Anubiss0% (1)

- Pros & Cons of LitigationDocument8 pagesPros & Cons of LitigationCairo AnubissNo ratings yet

- Securities Litigation Book of WarDocument374 pagesSecurities Litigation Book of WarCairo Anubiss100% (2)

- Commerce Industry OrderDocument10 pagesCommerce Industry OrderCairo AnubissNo ratings yet

- Screw The Note, Show Me The Loan! (The Nuclear Option)Document8 pagesScrew The Note, Show Me The Loan! (The Nuclear Option)Cairo Anubiss0% (1)

- Fed Home Loan Boston vs. BanksDocument378 pagesFed Home Loan Boston vs. BanksCairo AnubissNo ratings yet

- Markets and Interest RateDocument18 pagesMarkets and Interest Rateahmed sakrNo ratings yet

- Chapter 4 Credit Risk PDFDocument53 pagesChapter 4 Credit Risk PDFSyai GenjNo ratings yet

- 1) KCC IntroductionDocument5 pages1) KCC IntroductionBHANUPRIYANo ratings yet

- Understanding Returns: Absolute Return, CAGR, IRR Etc: What Is Return or Return On Investment?Document13 pagesUnderstanding Returns: Absolute Return, CAGR, IRR Etc: What Is Return or Return On Investment?IndranilGhoshNo ratings yet

- Chapter 14 Non Current Liabilities Test BankDocument36 pagesChapter 14 Non Current Liabilities Test BankSlamet Tri Prastyo100% (2)

- Penyimpanan Barang Ke GudangDocument10 pagesPenyimpanan Barang Ke Gudangajeng.saraswatiNo ratings yet

- Chapter 3 E - CommerceDocument11 pagesChapter 3 E - CommerceAtaklti TekaNo ratings yet

- PayPath Payment Service ReceiptDocument2 pagesPayPath Payment Service Receiptanuragjha19100% (1)

- Audit PlanningDocument15 pagesAudit PlanningJuliana ChengNo ratings yet

- Role of Investment in Indian Economy by Fauzia Shaikh WordDocument73 pagesRole of Investment in Indian Economy by Fauzia Shaikh WordMayur KantariaNo ratings yet

- Chapter 12 LiabilitiesDocument4 pagesChapter 12 Liabilitiesmaria isabella0% (1)

- SBR Examinable Docs 2021-22Document6 pagesSBR Examinable Docs 2021-22Stella YakubuNo ratings yet

- Cambridge O Level: ACCOUNTING 7707/22Document20 pagesCambridge O Level: ACCOUNTING 7707/22shujaitbukhariNo ratings yet

- Cash Advance - Travel, Payroll, PCF, & Operational ExpensesDocument1 pageCash Advance - Travel, Payroll, PCF, & Operational ExpensesPgas PaccoNo ratings yet

- Axis Bank: Management Information SystemDocument13 pagesAxis Bank: Management Information SystemAnurag RanaNo ratings yet

- Assignment Money MarketsDocument17 pagesAssignment Money Marketsrobinkapoor80% (5)

- CEILLI New Edition Questions English Set 1 PDFDocument19 pagesCEILLI New Edition Questions English Set 1 PDFTillie LeongNo ratings yet

- Audit Chalisa - FULL - CA Ravi AgarwalDocument19 pagesAudit Chalisa - FULL - CA Ravi AgarwalSri PavanNo ratings yet

- Current & Saving Account Statement: Jithu George S/O George Kanipayoor House Mannampetta Varakkara P O ThrissurDocument7 pagesCurrent & Saving Account Statement: Jithu George S/O George Kanipayoor House Mannampetta Varakkara P O ThrissurJithu GeorgeNo ratings yet

- What Is The Monetary Policy?Document20 pagesWhat Is The Monetary Policy?thisisnitin86No ratings yet

- Understanding Title Insurance: About FSCODocument10 pagesUnderstanding Title Insurance: About FSCOsanjNo ratings yet

- Financial and Managerial Accounting 4Th Edition Wild Solutions Manual Full Chapter PDFDocument60 pagesFinancial and Managerial Accounting 4Th Edition Wild Solutions Manual Full Chapter PDFClaudiaAdamsfowp100% (12)

- Virtual Wallet Fine PrintDocument34 pagesVirtual Wallet Fine PrintDeanthony WilliamsNo ratings yet

- Invoice 788560 PDFDocument1 pageInvoice 788560 PDFAadil KhanNo ratings yet

- Project Report On Kotak Mahindra Bank CompressDocument55 pagesProject Report On Kotak Mahindra Bank CompressShaikh ShamaNo ratings yet

- Bs NewDocument7 pagesBs NewDevendra RawoolNo ratings yet

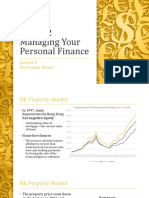

- GE1202 Managing Your Personal Finance: Purchasing HomesDocument33 pagesGE1202 Managing Your Personal Finance: Purchasing HomesAiden LANNo ratings yet

- PST Fundamentals of Finance 2015 2022Document58 pagesPST Fundamentals of Finance 2015 2022benard owinoNo ratings yet