Cement Report - Aurum

Cement Report - Aurum

You might also like

- Contractors List of USADocument21 pagesContractors List of USAjerry 121100% (2)

- BAYLOR 7040 166-54238 Rev FDocument68 pagesBAYLOR 7040 166-54238 Rev FPablo Galvez Rodriguez100% (4)

- Biomedical Applications of Soft RoboticsDocument11 pagesBiomedical Applications of Soft RoboticsAbdul Rehman100% (2)

- SCM of Tata MotorsDocument14 pagesSCM of Tata MotorsSHARATH JNo ratings yet

- Maruti Suzuki CLSA ConfDocument26 pagesMaruti Suzuki CLSA ConfnishantNo ratings yet

- Ramco Cements Corporate Presentation 2021 1a5936c1eeDocument60 pagesRamco Cements Corporate Presentation 2021 1a5936c1ee21BCH101 AbineshNo ratings yet

- JSW FinalsDocument11 pagesJSW FinalsRahul AgrawalNo ratings yet

- Indian Banking in Next 5 Years - BCG ReportDocument17 pagesIndian Banking in Next 5 Years - BCG ReportNirav ShahNo ratings yet

- Maruti Suzuki India LTDDocument40 pagesMaruti Suzuki India LTDnishantNo ratings yet

- PT Semen Indonesia (Persero) Tbk. and The Prospect of Indonesia Cement IndustryDocument14 pagesPT Semen Indonesia (Persero) Tbk. and The Prospect of Indonesia Cement IndustryJhun NaniNo ratings yet

- ER - BalKrishna Industries - Group 3Document17 pagesER - BalKrishna Industries - Group 3shaaqib mansuriNo ratings yet

- Indian Cement Industry-A Perspective by JVDocument6 pagesIndian Cement Industry-A Perspective by JVKendra TerryNo ratings yet

- Cement: Ranking and Region-Wise CapacityDocument1 pageCement: Ranking and Region-Wise CapacityRANGE VI, CGST & C. Ex RANCHI SOUTH DIVISIONNo ratings yet

- CBRE - Vietnam - Major Report - Vietnam Industrial Real Estate Market - Dec - 2018 - EN PDFDocument24 pagesCBRE - Vietnam - Major Report - Vietnam Industrial Real Estate Market - Dec - 2018 - EN PDFLinh MaiNo ratings yet

- Secondary Pres On MULDocument23 pagesSecondary Pres On MULnishantNo ratings yet

- Kirby Market SegmentationDocument1 pageKirby Market Segmentationsuk1234No ratings yet

- Cement February 2019Document9 pagesCement February 2019Mohammed Aaquib MubeenNo ratings yet

- FSA PresentationDocument44 pagesFSA Presentationarked kediaNo ratings yet

- Company:-Raymond Limited: Submitted By: Laimayum Bikash SharmaDocument35 pagesCompany:-Raymond Limited: Submitted By: Laimayum Bikash SharmasalmanNo ratings yet

- Ambit Capital - Agri Inputs - Diverging Growth Rates (Sector Update) (POSITIVE)Document65 pagesAmbit Capital - Agri Inputs - Diverging Growth Rates (Sector Update) (POSITIVE)Davuluri OmprakashNo ratings yet

- EdgeReport MARUTI CaseStudy 18 02 2022 627Document36 pagesEdgeReport MARUTI CaseStudy 18 02 2022 627Im CandlestickNo ratings yet

- Ecommerce Industry AnalysisDocument14 pagesEcommerce Industry AnalysisJANARTHAN SANKARANNo ratings yet

- EeveindiaDocument32 pagesEeveindiaAditya BhalotiaNo ratings yet

- Motilal Oswal PMS PortfolioDocument25 pagesMotilal Oswal PMS PortfolioHetanshNo ratings yet

- Asahi India Glass Initiation - 210702Document31 pagesAsahi India Glass Initiation - 210702vandit dharamshi100% (1)

- CS Final Assignment Nithya Prashant Raghu ShivaniDocument23 pagesCS Final Assignment Nithya Prashant Raghu ShivanigauravNo ratings yet

- Alpha Invesco Banking Sector Capex CycleDocument28 pagesAlpha Invesco Banking Sector Capex CycleVinay T MNo ratings yet

- Report On Tyres Sector by PACRADocument31 pagesReport On Tyres Sector by PACRAKhuram KhanNo ratings yet

- Equirus PLastic Pipe Sector Report - Initiating Coverage Report - Prince PipesDocument79 pagesEquirus PLastic Pipe Sector Report - Initiating Coverage Report - Prince PipesRees JohnsonNo ratings yet

- Research Note India's Hatchback IndustryDocument11 pagesResearch Note India's Hatchback IndustryVilluri BhargavNo ratings yet

- Zahir AhmedDocument14 pagesZahir AhmedTAPASHNo ratings yet

- Bangladesh Mobile Market - Executive Summary IDC - 2019Q3Document7 pagesBangladesh Mobile Market - Executive Summary IDC - 2019Q3Ayan MitraNo ratings yet

- Pakistan IndustriesDocument20 pagesPakistan IndustriesRehan AliNo ratings yet

- Cement October 2019Document24 pagesCement October 2019KALBHUT RAHUL GAJANANRAO 22No ratings yet

- Enkomatsu 2021 Minexpo Investor RelationsDocument34 pagesEnkomatsu 2021 Minexpo Investor RelationsHugo Victor Huayanca ValverdeNo ratings yet

- Siemens Rotating Machinery GuideDocument191 pagesSiemens Rotating Machinery GuideSathish KumarNo ratings yet

- E Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingDocument10 pagesE Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingredseerNo ratings yet

- A Comprehensive Review of The Bangladesh Cement IndustryDocument12 pagesA Comprehensive Review of The Bangladesh Cement IndustrytasnufaNo ratings yet

- Isme Airtel Case Study Group 07Document18 pagesIsme Airtel Case Study Group 07Bhairavi NagdaNo ratings yet

- AdMob Mobile Metrics Dec 09Document26 pagesAdMob Mobile Metrics Dec 09TechCrunchNo ratings yet

- Black Rose Industries Limited: Global Consumption Share (%) Global Acrylamide Market by End-Use (%)Document6 pagesBlack Rose Industries Limited: Global Consumption Share (%) Global Acrylamide Market by End-Use (%)janmejay26No ratings yet

- Wa0013.Document7 pagesWa0013.Randy ArtawijayaNo ratings yet

- Global Cement Article Cement Demad and Review by JVDocument5 pagesGlobal Cement Article Cement Demad and Review by JVSandeep BhatiaNo ratings yet

- 2022 - 25 March Indocement Public Expose - FinalDocument35 pages2022 - 25 March Indocement Public Expose - FinalDecky PrayogaNo ratings yet

- Auto Components Infographic December 2023Document1 pageAuto Components Infographic December 2023raghunandhan.cvNo ratings yet

- Gabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Document22 pagesGabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Ajinkya YadavNo ratings yet

- The Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureDocument63 pagesThe Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureSharvari ShankarNo ratings yet

- PT Excelcomindo Pratama Tbk. (XL) : Views On IndustryDocument13 pagesPT Excelcomindo Pratama Tbk. (XL) : Views On IndustryEddy SatriyaNo ratings yet

- Rubber Chemicals - Accelarater - Antioxidant and AntiozonentDocument25 pagesRubber Chemicals - Accelarater - Antioxidant and AntiozonentRajdeep MalNo ratings yet

- Opportunity and Investment Potential For Electric Vehicles in Kenya Manufacturing Africa October 2021Document89 pagesOpportunity and Investment Potential For Electric Vehicles in Kenya Manufacturing Africa October 2021Peterson muchiriNo ratings yet

- GCC Telecom Insight - Issued by STC Kuwait - April 2020Document29 pagesGCC Telecom Insight - Issued by STC Kuwait - April 2020AKNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- Mastering The Steel CyclesDocument33 pagesMastering The Steel CyclesSiddharthNo ratings yet

- It Sector ReportDocument25 pagesIt Sector ReportAryan BhageriaNo ratings yet

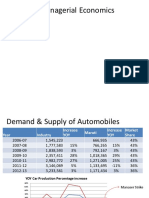

- Managerial Economics-AssignmentDocument9 pagesManagerial Economics-AssignmentSaurabh KaushalNo ratings yet

- GCC - Plastic IndustryDocument44 pagesGCC - Plastic IndustrySeshagiri KalyanasundaramNo ratings yet

- Indian Retail Lube MarketDocument12 pagesIndian Retail Lube MarketsudhanshuNo ratings yet

- India Bengaluru - Industrial - H2 2022Document2 pagesIndia Bengaluru - Industrial - H2 2022jaiat22No ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- Performance-Based Road Maintenance Contracts in the CAREC RegionFrom EverandPerformance-Based Road Maintenance Contracts in the CAREC RegionNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2021: Volume I—Country and Regional ReviewsFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2021: Volume I—Country and Regional ReviewsNo ratings yet

- Reforms, Opportunities, and Challenges for State-Owned EnterprisesFrom EverandReforms, Opportunities, and Challenges for State-Owned EnterprisesNo ratings yet

- Konsep Pendidikan Religius RasionalDocument14 pagesKonsep Pendidikan Religius RasionalSri ParwatiNo ratings yet

- Clear Choice: TurbomatrixDocument10 pagesClear Choice: TurbomatrixSaleh HamadanyNo ratings yet

- Constitution Research PaperDocument9 pagesConstitution Research PaperSEJAL AGRAWAL BA LLBNo ratings yet

- San Miguel National High School Scuala ST., San Juan, San Miguel, Bulacan Summative Test - Oral Communication in Context S.Y. 2021-2022Document3 pagesSan Miguel National High School Scuala ST., San Juan, San Miguel, Bulacan Summative Test - Oral Communication in Context S.Y. 2021-2022Erica AlbaoNo ratings yet

- EDUCache Simulator For Teaching Computer Architecture and OrganizationDocument8 pagesEDUCache Simulator For Teaching Computer Architecture and OrganizationTenma InazumaNo ratings yet

- SATIP-K-001-08 - Air Filtration Devices and Grease FilterDocument2 pagesSATIP-K-001-08 - Air Filtration Devices and Grease Filterimrankhan22No ratings yet

- Holzer MethodDocument13 pagesHolzer Methodmeadot getachew100% (1)

- EBS Full ReportDocument74 pagesEBS Full ReportEd SalangaNo ratings yet

- Unit 7-Chemical Reactions NotesDocument55 pagesUnit 7-Chemical Reactions Notesapi-182809945No ratings yet

- 1.2c atDocument3 pages1.2c atenyw160309No ratings yet

- Anatomy of A HackDocument43 pagesAnatomy of A Hackczar777No ratings yet

- MSDS Artistri P5910 White Pigment Ink 071808Document10 pagesMSDS Artistri P5910 White Pigment Ink 071808Cisca BebetzNo ratings yet

- Maintenance and Inspection ChecklistDocument1 pageMaintenance and Inspection ChecklistRony NiksonNo ratings yet

- 580M Series 2 Hydraulics 4 PDFDocument3 pages580M Series 2 Hydraulics 4 PDFJESUSNo ratings yet

- Emami Limited: Sales ManagementDocument12 pagesEmami Limited: Sales ManagementSANYUJ ZADGAONKARNo ratings yet

- Quality Assurance of Developed Materials: Heidee F. Ferrer EddDocument60 pagesQuality Assurance of Developed Materials: Heidee F. Ferrer EddHeart SophieNo ratings yet

- Flyer Nutrition For Endurance AthletesDocument1 pageFlyer Nutrition For Endurance AthletesDIAN ADINDANo ratings yet

- Anyone Who Had A Heart - A Case Study in PhysiologyDocument9 pagesAnyone Who Had A Heart - A Case Study in PhysiologyJohnSnow0% (1)

- PurescriptDocument65 pagesPurescriptsolrac1308No ratings yet

- TCCC Handbook Fall 2013Document192 pagesTCCC Handbook Fall 2013AMG_IA100% (4)

- 6 - People vs. VelosoDocument4 pages6 - People vs. Velosogerlie22No ratings yet

- Home - Link - 4.6 PerimeterDocument2 pagesHome - Link - 4.6 Perimetergiselle andalanNo ratings yet

- Analysis of Chemical Plant Heat Exchanger ExplosionDocument1 pageAnalysis of Chemical Plant Heat Exchanger ExplosionArath Leon ReyNo ratings yet

- 216B2, 226B2, 232B2, 236B2, 242B2, Electrical System 247B2 and 257B2 Multi-Terrain Loader and 252B2 Skid Steer LoaderDocument4 pages216B2, 226B2, 232B2, 236B2, 242B2, Electrical System 247B2 and 257B2 Multi-Terrain Loader and 252B2 Skid Steer LoaderAirton SenaNo ratings yet

- SXDocument126 pagesSXpalak32No ratings yet

- PHD Syllabus AMUDocument2 pagesPHD Syllabus AMUMohd ShahidNo ratings yet

- Query Optimization MCQDocument12 pagesQuery Optimization MCQSameer vermaNo ratings yet

Download as pdf or txt

You might also like

- Contractors List of USADocument21 pagesContractors List of USAjerry 121100% (2)

- BAYLOR 7040 166-54238 Rev FDocument68 pagesBAYLOR 7040 166-54238 Rev FPablo Galvez Rodriguez100% (4)

- Biomedical Applications of Soft RoboticsDocument11 pagesBiomedical Applications of Soft RoboticsAbdul Rehman100% (2)

- SCM of Tata MotorsDocument14 pagesSCM of Tata MotorsSHARATH JNo ratings yet

- Maruti Suzuki CLSA ConfDocument26 pagesMaruti Suzuki CLSA ConfnishantNo ratings yet

- Ramco Cements Corporate Presentation 2021 1a5936c1eeDocument60 pagesRamco Cements Corporate Presentation 2021 1a5936c1ee21BCH101 AbineshNo ratings yet

- JSW FinalsDocument11 pagesJSW FinalsRahul AgrawalNo ratings yet

- Indian Banking in Next 5 Years - BCG ReportDocument17 pagesIndian Banking in Next 5 Years - BCG ReportNirav ShahNo ratings yet

- Maruti Suzuki India LTDDocument40 pagesMaruti Suzuki India LTDnishantNo ratings yet

- PT Semen Indonesia (Persero) Tbk. and The Prospect of Indonesia Cement IndustryDocument14 pagesPT Semen Indonesia (Persero) Tbk. and The Prospect of Indonesia Cement IndustryJhun NaniNo ratings yet

- ER - BalKrishna Industries - Group 3Document17 pagesER - BalKrishna Industries - Group 3shaaqib mansuriNo ratings yet

- Indian Cement Industry-A Perspective by JVDocument6 pagesIndian Cement Industry-A Perspective by JVKendra TerryNo ratings yet

- Cement: Ranking and Region-Wise CapacityDocument1 pageCement: Ranking and Region-Wise CapacityRANGE VI, CGST & C. Ex RANCHI SOUTH DIVISIONNo ratings yet

- CBRE - Vietnam - Major Report - Vietnam Industrial Real Estate Market - Dec - 2018 - EN PDFDocument24 pagesCBRE - Vietnam - Major Report - Vietnam Industrial Real Estate Market - Dec - 2018 - EN PDFLinh MaiNo ratings yet

- Secondary Pres On MULDocument23 pagesSecondary Pres On MULnishantNo ratings yet

- Kirby Market SegmentationDocument1 pageKirby Market Segmentationsuk1234No ratings yet

- Cement February 2019Document9 pagesCement February 2019Mohammed Aaquib MubeenNo ratings yet

- FSA PresentationDocument44 pagesFSA Presentationarked kediaNo ratings yet

- Company:-Raymond Limited: Submitted By: Laimayum Bikash SharmaDocument35 pagesCompany:-Raymond Limited: Submitted By: Laimayum Bikash SharmasalmanNo ratings yet

- Ambit Capital - Agri Inputs - Diverging Growth Rates (Sector Update) (POSITIVE)Document65 pagesAmbit Capital - Agri Inputs - Diverging Growth Rates (Sector Update) (POSITIVE)Davuluri OmprakashNo ratings yet

- EdgeReport MARUTI CaseStudy 18 02 2022 627Document36 pagesEdgeReport MARUTI CaseStudy 18 02 2022 627Im CandlestickNo ratings yet

- Ecommerce Industry AnalysisDocument14 pagesEcommerce Industry AnalysisJANARTHAN SANKARANNo ratings yet

- EeveindiaDocument32 pagesEeveindiaAditya BhalotiaNo ratings yet

- Motilal Oswal PMS PortfolioDocument25 pagesMotilal Oswal PMS PortfolioHetanshNo ratings yet

- Asahi India Glass Initiation - 210702Document31 pagesAsahi India Glass Initiation - 210702vandit dharamshi100% (1)

- CS Final Assignment Nithya Prashant Raghu ShivaniDocument23 pagesCS Final Assignment Nithya Prashant Raghu ShivanigauravNo ratings yet

- Alpha Invesco Banking Sector Capex CycleDocument28 pagesAlpha Invesco Banking Sector Capex CycleVinay T MNo ratings yet

- Report On Tyres Sector by PACRADocument31 pagesReport On Tyres Sector by PACRAKhuram KhanNo ratings yet

- Equirus PLastic Pipe Sector Report - Initiating Coverage Report - Prince PipesDocument79 pagesEquirus PLastic Pipe Sector Report - Initiating Coverage Report - Prince PipesRees JohnsonNo ratings yet

- Research Note India's Hatchback IndustryDocument11 pagesResearch Note India's Hatchback IndustryVilluri BhargavNo ratings yet

- Zahir AhmedDocument14 pagesZahir AhmedTAPASHNo ratings yet

- Bangladesh Mobile Market - Executive Summary IDC - 2019Q3Document7 pagesBangladesh Mobile Market - Executive Summary IDC - 2019Q3Ayan MitraNo ratings yet

- Pakistan IndustriesDocument20 pagesPakistan IndustriesRehan AliNo ratings yet

- Cement October 2019Document24 pagesCement October 2019KALBHUT RAHUL GAJANANRAO 22No ratings yet

- Enkomatsu 2021 Minexpo Investor RelationsDocument34 pagesEnkomatsu 2021 Minexpo Investor RelationsHugo Victor Huayanca ValverdeNo ratings yet

- Siemens Rotating Machinery GuideDocument191 pagesSiemens Rotating Machinery GuideSathish KumarNo ratings yet

- E Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingDocument10 pagesE Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingredseerNo ratings yet

- A Comprehensive Review of The Bangladesh Cement IndustryDocument12 pagesA Comprehensive Review of The Bangladesh Cement IndustrytasnufaNo ratings yet

- Isme Airtel Case Study Group 07Document18 pagesIsme Airtel Case Study Group 07Bhairavi NagdaNo ratings yet

- AdMob Mobile Metrics Dec 09Document26 pagesAdMob Mobile Metrics Dec 09TechCrunchNo ratings yet

- Black Rose Industries Limited: Global Consumption Share (%) Global Acrylamide Market by End-Use (%)Document6 pagesBlack Rose Industries Limited: Global Consumption Share (%) Global Acrylamide Market by End-Use (%)janmejay26No ratings yet

- Wa0013.Document7 pagesWa0013.Randy ArtawijayaNo ratings yet

- Global Cement Article Cement Demad and Review by JVDocument5 pagesGlobal Cement Article Cement Demad and Review by JVSandeep BhatiaNo ratings yet

- 2022 - 25 March Indocement Public Expose - FinalDocument35 pages2022 - 25 March Indocement Public Expose - FinalDecky PrayogaNo ratings yet

- Auto Components Infographic December 2023Document1 pageAuto Components Infographic December 2023raghunandhan.cvNo ratings yet

- Gabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Document22 pagesGabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Ajinkya YadavNo ratings yet

- The Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureDocument63 pagesThe Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureSharvari ShankarNo ratings yet

- PT Excelcomindo Pratama Tbk. (XL) : Views On IndustryDocument13 pagesPT Excelcomindo Pratama Tbk. (XL) : Views On IndustryEddy SatriyaNo ratings yet

- Rubber Chemicals - Accelarater - Antioxidant and AntiozonentDocument25 pagesRubber Chemicals - Accelarater - Antioxidant and AntiozonentRajdeep MalNo ratings yet

- Opportunity and Investment Potential For Electric Vehicles in Kenya Manufacturing Africa October 2021Document89 pagesOpportunity and Investment Potential For Electric Vehicles in Kenya Manufacturing Africa October 2021Peterson muchiriNo ratings yet

- GCC Telecom Insight - Issued by STC Kuwait - April 2020Document29 pagesGCC Telecom Insight - Issued by STC Kuwait - April 2020AKNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- Mastering The Steel CyclesDocument33 pagesMastering The Steel CyclesSiddharthNo ratings yet

- It Sector ReportDocument25 pagesIt Sector ReportAryan BhageriaNo ratings yet

- Managerial Economics-AssignmentDocument9 pagesManagerial Economics-AssignmentSaurabh KaushalNo ratings yet

- GCC - Plastic IndustryDocument44 pagesGCC - Plastic IndustrySeshagiri KalyanasundaramNo ratings yet

- Indian Retail Lube MarketDocument12 pagesIndian Retail Lube MarketsudhanshuNo ratings yet

- India Bengaluru - Industrial - H2 2022Document2 pagesIndia Bengaluru - Industrial - H2 2022jaiat22No ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- Performance-Based Road Maintenance Contracts in the CAREC RegionFrom EverandPerformance-Based Road Maintenance Contracts in the CAREC RegionNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2021: Volume I—Country and Regional ReviewsFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2021: Volume I—Country and Regional ReviewsNo ratings yet

- Reforms, Opportunities, and Challenges for State-Owned EnterprisesFrom EverandReforms, Opportunities, and Challenges for State-Owned EnterprisesNo ratings yet

- Konsep Pendidikan Religius RasionalDocument14 pagesKonsep Pendidikan Religius RasionalSri ParwatiNo ratings yet

- Clear Choice: TurbomatrixDocument10 pagesClear Choice: TurbomatrixSaleh HamadanyNo ratings yet

- Constitution Research PaperDocument9 pagesConstitution Research PaperSEJAL AGRAWAL BA LLBNo ratings yet

- San Miguel National High School Scuala ST., San Juan, San Miguel, Bulacan Summative Test - Oral Communication in Context S.Y. 2021-2022Document3 pagesSan Miguel National High School Scuala ST., San Juan, San Miguel, Bulacan Summative Test - Oral Communication in Context S.Y. 2021-2022Erica AlbaoNo ratings yet

- EDUCache Simulator For Teaching Computer Architecture and OrganizationDocument8 pagesEDUCache Simulator For Teaching Computer Architecture and OrganizationTenma InazumaNo ratings yet

- SATIP-K-001-08 - Air Filtration Devices and Grease FilterDocument2 pagesSATIP-K-001-08 - Air Filtration Devices and Grease Filterimrankhan22No ratings yet

- Holzer MethodDocument13 pagesHolzer Methodmeadot getachew100% (1)

- EBS Full ReportDocument74 pagesEBS Full ReportEd SalangaNo ratings yet

- Unit 7-Chemical Reactions NotesDocument55 pagesUnit 7-Chemical Reactions Notesapi-182809945No ratings yet

- 1.2c atDocument3 pages1.2c atenyw160309No ratings yet

- Anatomy of A HackDocument43 pagesAnatomy of A Hackczar777No ratings yet

- MSDS Artistri P5910 White Pigment Ink 071808Document10 pagesMSDS Artistri P5910 White Pigment Ink 071808Cisca BebetzNo ratings yet

- Maintenance and Inspection ChecklistDocument1 pageMaintenance and Inspection ChecklistRony NiksonNo ratings yet

- 580M Series 2 Hydraulics 4 PDFDocument3 pages580M Series 2 Hydraulics 4 PDFJESUSNo ratings yet

- Emami Limited: Sales ManagementDocument12 pagesEmami Limited: Sales ManagementSANYUJ ZADGAONKARNo ratings yet

- Quality Assurance of Developed Materials: Heidee F. Ferrer EddDocument60 pagesQuality Assurance of Developed Materials: Heidee F. Ferrer EddHeart SophieNo ratings yet

- Flyer Nutrition For Endurance AthletesDocument1 pageFlyer Nutrition For Endurance AthletesDIAN ADINDANo ratings yet

- Anyone Who Had A Heart - A Case Study in PhysiologyDocument9 pagesAnyone Who Had A Heart - A Case Study in PhysiologyJohnSnow0% (1)

- PurescriptDocument65 pagesPurescriptsolrac1308No ratings yet

- TCCC Handbook Fall 2013Document192 pagesTCCC Handbook Fall 2013AMG_IA100% (4)

- 6 - People vs. VelosoDocument4 pages6 - People vs. Velosogerlie22No ratings yet

- Home - Link - 4.6 PerimeterDocument2 pagesHome - Link - 4.6 Perimetergiselle andalanNo ratings yet

- Analysis of Chemical Plant Heat Exchanger ExplosionDocument1 pageAnalysis of Chemical Plant Heat Exchanger ExplosionArath Leon ReyNo ratings yet

- 216B2, 226B2, 232B2, 236B2, 242B2, Electrical System 247B2 and 257B2 Multi-Terrain Loader and 252B2 Skid Steer LoaderDocument4 pages216B2, 226B2, 232B2, 236B2, 242B2, Electrical System 247B2 and 257B2 Multi-Terrain Loader and 252B2 Skid Steer LoaderAirton SenaNo ratings yet

- SXDocument126 pagesSXpalak32No ratings yet

- PHD Syllabus AMUDocument2 pagesPHD Syllabus AMUMohd ShahidNo ratings yet

- Query Optimization MCQDocument12 pagesQuery Optimization MCQSameer vermaNo ratings yet