Download as pdf or txt

You might also like

- Credit Risk Management at Icici BankDocument128 pagesCredit Risk Management at Icici Bankyash gupta86% (7)

- Ibc ChartsDocument7 pagesIbc Chartspiyush bansalNo ratings yet

- Sanjay Srinivaas, Sadasiv and KishoreDocument43 pagesSanjay Srinivaas, Sadasiv and KishoreSanjay SrinivaasNo ratings yet

- Banking Awareness Topic Wise - Non-Performing Assets and Its ResolutionDocument5 pagesBanking Awareness Topic Wise - Non-Performing Assets and Its Resolutionprekshag17No ratings yet

- Legal Issues in SecuritizationDocument18 pagesLegal Issues in SecuritizationAnisa KhanNo ratings yet

- 731 - 740 Fa-6Document17 pages731 - 740 Fa-6738 Lavanya JadhavNo ratings yet

- Need For Arcs of Rising Bad Loans: Arc Can Help Consolidate AllDocument1 pageNeed For Arcs of Rising Bad Loans: Arc Can Help Consolidate AllRaghav SharmaNo ratings yet

- Mint 12oct2020 PDFDocument16 pagesMint 12oct2020 PDFchintan desaiNo ratings yet

- Dr. Pradiptarathi Panda Lecturer, NismDocument26 pagesDr. Pradiptarathi Panda Lecturer, NismMaunil OzaNo ratings yet

- Sarfaesi ACT, 2002: Project Presentstion BY Smit GandhiDocument16 pagesSarfaesi ACT, 2002: Project Presentstion BY Smit GandhismitNo ratings yet

- NBFCs MAT 3Document23 pagesNBFCs MAT 3Prashant RatnpandeyNo ratings yet

- Banking Law AssignmentDocument11 pagesBanking Law AssignmentTanu Shree SinghNo ratings yet

- Admin Law NotesDocument11 pagesAdmin Law NotesTanu Shree SinghNo ratings yet

- NPA Recovery ManagementDocument31 pagesNPA Recovery ManagementSantoshi AravindNo ratings yet

- Npa'S Under Sarfaesi Act: in Terms of Agriculture / Farm Loans The NPA Is Defined As Under: For ShortDocument6 pagesNpa'S Under Sarfaesi Act: in Terms of Agriculture / Farm Loans The NPA Is Defined As Under: For Short76-Gunika MahindraNo ratings yet

- Credit Risk and Security Documentation For Agri OfficersDocument192 pagesCredit Risk and Security Documentation For Agri OfficersAdnan Adil HussainNo ratings yet

- Risk ManagementDocument15 pagesRisk Managementvaibhav surekaNo ratings yet

- Unit 17 and 19 - BankingDocument14 pagesUnit 17 and 19 - BankingArcha MenonNo ratings yet

- Banking Law AssignmentDocument11 pagesBanking Law AssignmentTanu Shree SinghNo ratings yet

- Literature ReviewDocument21 pagesLiterature ReviewGaurav JaiswalNo ratings yet

- DJ WorkDocument49 pagesDJ WorkPratik GhadeNo ratings yet

- Banking FinalsDocument4 pagesBanking Finalsfxsjhhcc6cNo ratings yet

- Definition of Npas: A NPA Is A Loan or An Advance WhereDocument30 pagesDefinition of Npas: A NPA Is A Loan or An Advance WheremulchandranaNo ratings yet

- NPA Management Policy Revised New - FY 2021-22Document239 pagesNPA Management Policy Revised New - FY 2021-22Abhijit TripathiNo ratings yet

- Income Recognition and Asset ClassificationDocument34 pagesIncome Recognition and Asset ClassificationJ ImamNo ratings yet

- Evolving Landscape of Corporate Stress ResolutionDocument68 pagesEvolving Landscape of Corporate Stress ResolutiongowthampkfNo ratings yet

- CG - DHFL ScamDocument8 pagesCG - DHFL ScamAnushka KeshavNo ratings yet

- 7 Vol 5 No 1Document5 pages7 Vol 5 No 1DevikaNo ratings yet

- Ra 8791 Gen Bank Law of 2000Document60 pagesRa 8791 Gen Bank Law of 2000Joseph MangahasNo ratings yet

- 15 - Asset Reconstruction in BankingDocument16 pages15 - Asset Reconstruction in Bankingcreddie98672No ratings yet

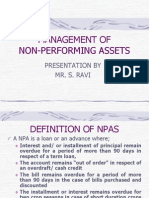

- Management of Non-Performing Assets: Presentation by Mr. S. RaviDocument29 pagesManagement of Non-Performing Assets: Presentation by Mr. S. RaviRajesh MaddiNo ratings yet

- Bank Governance, NPA, Debt Recovery, Bank Resolution (Week 7-10)Document47 pagesBank Governance, NPA, Debt Recovery, Bank Resolution (Week 7-10)abhimanyu dharmaNo ratings yet

- Banking Law Final DraftDocument21 pagesBanking Law Final DraftKeerti SinghNo ratings yet

- U Ii NBFCDocument272 pagesU Ii NBFCDeepshi GargNo ratings yet

- Mob NpaDocument44 pagesMob NpaParthNo ratings yet

- Ilovepdf MergedDocument180 pagesIlovepdf MergedIshan vermaNo ratings yet

- Recovery Mechanisms of Non-Performing Assets in Indian Commercial Banks: An Empirical StudyDocument8 pagesRecovery Mechanisms of Non-Performing Assets in Indian Commercial Banks: An Empirical StudyKeya ShahNo ratings yet

- General Banking LawDocument62 pagesGeneral Banking Lawrichard.asentista.22No ratings yet

- Non Performing AssetsDocument11 pagesNon Performing AssetssudheerNo ratings yet

- General Banking LawDocument62 pagesGeneral Banking LawwhatrichNo ratings yet

- A To Z in BankingDocument3 pagesA To Z in Bankingsubhasis123bbsrNo ratings yet

- SBI V Jah Developers PVT LTDDocument26 pagesSBI V Jah Developers PVT LTDShovit BetalNo ratings yet

- Presentation FinalDocument23 pagesPresentation FinalRitu RawatNo ratings yet

- NBFC ChecklistDocument23 pagesNBFC ChecklistSanjeev MaharNo ratings yet

- Non Performing Assets Management in TheDocument10 pagesNon Performing Assets Management in TheAyona AduNo ratings yet

- Rbi Norms For NpaDocument8 pagesRbi Norms For NpaSubashVenkataram89% (9)

- Mid Sem Solution 2Document7 pagesMid Sem Solution 2dipono6356No ratings yet

- CH 8 - MergedDocument30 pagesCH 8 - MergedIshan vermaNo ratings yet

- IBC and BanksDocument23 pagesIBC and BanksAnonymous VFyoCxNo ratings yet

- Bad BanksDocument11 pagesBad BanksYashasvi SNo ratings yet

- Key IssuesDocument7 pagesKey IssuesDhruv MehtaNo ratings yet

- General Banking LawDocument62 pagesGeneral Banking LawKristine FayeNo ratings yet

- BFL End Sem NotesDocument72 pagesBFL End Sem NotesAachman ShekharNo ratings yet

- Basics of Banking - Study NotesDocument13 pagesBasics of Banking - Study NotesTanmoy GhoshNo ratings yet

- Managing NPAsDocument58 pagesManaging NPAsSuranga FernandoNo ratings yet

- Banking Updates - WWW - Bankopedia.co - inDocument5 pagesBanking Updates - WWW - Bankopedia.co - inPrashant SinghNo ratings yet

- NPA Management by Indian Banks-LATEST: Dr. Deepak Tandon IMI New DelhiDocument40 pagesNPA Management by Indian Banks-LATEST: Dr. Deepak Tandon IMI New Delhidev mhaispurkarNo ratings yet

- Banking Law Final DraftDocument21 pagesBanking Law Final DraftKeerti SinghNo ratings yet

- Insolvency Law FinalDocument19 pagesInsolvency Law FinalISHAN SINGHNo ratings yet

- BankingAwarenessLectureEnglish Module25Document18 pagesBankingAwarenessLectureEnglish Module25Sai VaishnavNo ratings yet

- BankingAwarenessLectureEnglish Module23Document22 pagesBankingAwarenessLectureEnglish Module23Sai VaishnavNo ratings yet

- BankingAwarenessLectureEnglish Module19Document12 pagesBankingAwarenessLectureEnglish Module19Sai VaishnavNo ratings yet

- Zones and Divisions of Indian RailwaysDocument5 pagesZones and Divisions of Indian RailwaysSai Vaishnav0% (1)

- Types of Waiting Lists in Indian Railways and Their Confirmation ChancesDocument1 pageTypes of Waiting Lists in Indian Railways and Their Confirmation ChancesSai VaishnavNo ratings yet

- Current Booking in Indian RailwaysDocument1 pageCurrent Booking in Indian RailwaysSai VaishnavNo ratings yet

- Uts in Indian RailwaysDocument2 pagesUts in Indian RailwaysSai VaishnavNo ratings yet

- About Locomotives in Indian RailwaysDocument6 pagesAbout Locomotives in Indian RailwaysSai VaishnavNo ratings yet

- Types of Coaches in Indian RailwaysDocument1 pageTypes of Coaches in Indian RailwaysSai VaishnavNo ratings yet

- About Signaling System in Indian RailwaysDocument3 pagesAbout Signaling System in Indian RailwaysSai VaishnavNo ratings yet

- Chart Preparation in Indian RailwaysDocument2 pagesChart Preparation in Indian RailwaysSai VaishnavNo ratings yet

- Auto Upgradation Option in Indian RailwaysDocument1 pageAuto Upgradation Option in Indian RailwaysSai VaishnavNo ratings yet

- Introduction To SAP: Responsibility of A ConsultantDocument20 pagesIntroduction To SAP: Responsibility of A ConsultantSai VaishnavNo ratings yet

- Cancellation Fees in Indian RailwaysDocument2 pagesCancellation Fees in Indian RailwaysSai VaishnavNo ratings yet

- Sap Fico: Fi MaterialDocument150 pagesSap Fico: Fi MaterialSai VaishnavNo ratings yet

- Sap Fico: Co MaterialDocument45 pagesSap Fico: Co MaterialSai VaishnavNo ratings yet

- Banking CompanyDocument5 pagesBanking CompanyPragathi PraNo ratings yet

- Rescue 9Document51 pagesRescue 9abhishek pandeyNo ratings yet

- Unit 19 Factoring, Forfaiting and Bill Discounting: ObjectivesDocument20 pagesUnit 19 Factoring, Forfaiting and Bill Discounting: ObjectivesmanishaNo ratings yet

- Loan Policy 2019Document56 pagesLoan Policy 2019Gourav baruNo ratings yet

- Marginal Cost of Funds Based Lending Rate (MCLR) - ArthapediaDocument3 pagesMarginal Cost of Funds Based Lending Rate (MCLR) - ArthapediasoumyajitroyNo ratings yet

- Vision Ias SeptDocument27 pagesVision Ias SeptAkash SarkarNo ratings yet

- IFS - Chapter 4Document28 pagesIFS - Chapter 4riashahNo ratings yet

- Summary of Union Budget 2019-20Document29 pagesSummary of Union Budget 2019-20SANTHAN KUMARNo ratings yet

- Prudential Norms For Non-Banking Financial (Non-Deposit Accepting or Holding) CompaniesDocument6 pagesPrudential Norms For Non-Banking Financial (Non-Deposit Accepting or Holding) CompaniesGreeshma Babu ShylajaNo ratings yet

- Rbi ActDocument44 pagesRbi Actaneesh arvindhanNo ratings yet

- BC AssignmentDocument19 pagesBC AssignmentSrinath SaravananNo ratings yet

- Impact of Digitalization For Customers of HDFC Bank: Post Graduate Diploma in ManagementDocument42 pagesImpact of Digitalization For Customers of HDFC Bank: Post Graduate Diploma in ManagementJASMEET SINGHNo ratings yet

- Ban103 Syllabus PDFDocument29 pagesBan103 Syllabus PDFkiranNo ratings yet

- MMGS Ii To Iii Model Objective Question Paper 1 PDFDocument16 pagesMMGS Ii To Iii Model Objective Question Paper 1 PDFPRABHU JOTHNo ratings yet

- Liquidity Management in Banks Treasury Risk ManagementDocument11 pagesLiquidity Management in Banks Treasury Risk Managementashoo khoslaNo ratings yet

- BankingDocument50 pagesBankinggopalmeb6368No ratings yet

- Supplementary AgreementDocument2 pagesSupplementary AgreementI CreateNo ratings yet

- Economic Project On RBI PDFDocument20 pagesEconomic Project On RBI PDFDEVENDRA SHARMANo ratings yet

- Pre-Shipment Credit in Foreign CurrencyDocument10 pagesPre-Shipment Credit in Foreign Currencykalik goyalNo ratings yet

- Literature Review of Retail Banking in IndiaDocument5 pagesLiterature Review of Retail Banking in Indiac5qfb5v5100% (1)

- Aditya Birla Finance Limited: U65990GJ1991PLC064603Document11 pagesAditya Birla Finance Limited: U65990GJ1991PLC064603Mohammed JunaidNo ratings yet

- Attachment RBI NABARD SEBI 2019 October 1 To 31 EduTap Docx Lyst1692Document152 pagesAttachment RBI NABARD SEBI 2019 October 1 To 31 EduTap Docx Lyst1692mail mailucNo ratings yet

- Regulations ExportDocument37 pagesRegulations ExportgopalushaNo ratings yet

- 10 Chapter1Document39 pages10 Chapter1Kajal GoswamiNo ratings yet

- RBI State Bankrupcy ReportDocument23 pagesRBI State Bankrupcy ReportChirag RajputNo ratings yet

- Summer Training Project REPORT: "Perception of Investors Towards Investing in Uti Mutual Fund"Document30 pagesSummer Training Project REPORT: "Perception of Investors Towards Investing in Uti Mutual Fund"Pihu SharmaNo ratings yet

- HH HDocument2 pagesHH HPrashant UpadhyayNo ratings yet