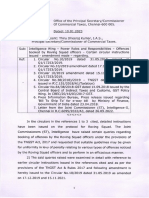

Place of GST Registration For Renting of Immovable Property

Place of GST Registration For Renting of Immovable Property

You might also like

- Genuine Sale Transactions Through Gpa Is Not Barred by Supreme Court Decision For KarnatakaDocument3 pagesGenuine Sale Transactions Through Gpa Is Not Barred by Supreme Court Decision For KarnatakaSridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್100% (1)

- Place of SupplyDocument29 pagesPlace of SupplyShravan NiranjanNo ratings yet

- 14725603564.place of Supply of ServicesDocument12 pages14725603564.place of Supply of ServicesScribbler 414No ratings yet

- By Anandram Sankar GENERALLY, SEZ Entities Export Goods/services or Supply Goods/services To Entities inDocument3 pagesBy Anandram Sankar GENERALLY, SEZ Entities Export Goods/services or Supply Goods/services To Entities inChintan VasaNo ratings yet

- Place of SupplyDocument22 pagesPlace of Supplyanujdas173No ratings yet

- Article - GST On Washout Charges or Liquidated DamagesDocument6 pagesArticle - GST On Washout Charges or Liquidated DamagessupdtconflNo ratings yet

- Power Roles and Responsibilities - Offences Booked by Roving Squad OfficersDocument16 pagesPower Roles and Responsibilities - Offences Booked by Roving Squad OfficersAnandd BabunathNo ratings yet

- Answes: C 1& 2: I, S: Hapter Ntroduction UpplyDocument49 pagesAnswes: C 1& 2: I, S: Hapter Ntroduction UpplyJoseph PrabhuNo ratings yet

- GST Detailed AnalysisDocument10 pagesGST Detailed AnalysisKritibandhu SwainNo ratings yet

- AAR - IGST Is Chargable On Ex-Factory Supplies Where Movement of Goods Terminates in Other StateDocument4 pagesAAR - IGST Is Chargable On Ex-Factory Supplies Where Movement of Goods Terminates in Other StateJigar MakwanaNo ratings yet

- Unit II-Some Basics: Be A Mix of Theory Questions and Numericals/ Situations/ CasesDocument9 pagesUnit II-Some Basics: Be A Mix of Theory Questions and Numericals/ Situations/ CasesArushi GuptaNo ratings yet

- 027 D Dhruv TankDocument26 pages027 D Dhruv TankPrince SoundhNo ratings yet

- Taxation LawDocument16 pagesTaxation Lawsankalp patelNo ratings yet

- Place of SuplyDocument101 pagesPlace of SuplyPremNo ratings yet

- Place of Supply IgstDocument101 pagesPlace of Supply Igsthariom bajpaiNo ratings yet

- GST Manual Sample ChapterDocument6 pagesGST Manual Sample ChapterRishabh vermaNo ratings yet

- Place of Supply: After Studying This Chapter, You Will Be Able ToDocument85 pagesPlace of Supply: After Studying This Chapter, You Will Be Able ToRohit SoniNo ratings yet

- Supplemental Guidelines For Brokers and Salespersons Mc-15-02aDocument13 pagesSupplemental Guidelines For Brokers and Salespersons Mc-15-02aAl MarzolNo ratings yet

- Interstate and Intrastate Transactions Under GSTDocument11 pagesInterstate and Intrastate Transactions Under GSTD.Naga RajuNo ratings yet

- 5b8d6 Liability W.R.T. Jda Entered Prior To GST ArticleDocument3 pages5b8d6 Liability W.R.T. Jda Entered Prior To GST ArticleKunalKumarNo ratings yet

- CH 5 Place of SupplyDocument63 pagesCH 5 Place of SupplyManas Kumar SahooNo ratings yet

- 47321bosfinal p8 Part1 cp5Document61 pages47321bosfinal p8 Part1 cp5doomraoffice2019No ratings yet

- Research MaterialDocument2 pagesResearch Materialyogeshshukla.ys14No ratings yet

- IGST Act With Amendments 1Document14 pagesIGST Act With Amendments 1sanjitaNo ratings yet

- Situs of SupplyDocument8 pagesSitus of SupplyManish SachdevaNo ratings yet

- Place of SupplyDocument8 pagesPlace of SupplyIshita YadavNo ratings yet

- Taxation of Intermediary Services Under GSTDocument11 pagesTaxation of Intermediary Services Under GSTShyaam SheoranNo ratings yet

- Place of Supply: After Studying This Chapter, You Will Be Able ToDocument85 pagesPlace of Supply: After Studying This Chapter, You Will Be Able TooverclockthesunNo ratings yet

- Final GST Analysis 2016Document154 pagesFinal GST Analysis 2016Ca Dhruv AgrawalNo ratings yet

- GST AmendmentsDocument15 pagesGST AmendmentsSana KhanNo ratings yet

- Cir 184 16 2022 CGSTDocument4 pagesCir 184 16 2022 CGSTAmritesh RaiNo ratings yet

- Circular No 209 03 2024Document3 pagesCircular No 209 03 2024SSSARMANo ratings yet

- 75915bos61400 cp3Document120 pages75915bos61400 cp3Bhanu RawatNo ratings yet

- Faculty of Law Jamia Millia Islamia: Income From House PropertyDocument21 pagesFaculty of Law Jamia Millia Islamia: Income From House PropertyMohdSaqibNo ratings yet

- Organised By:: National Conference On GSTDocument19 pagesOrganised By:: National Conference On GSTSunil ShahNo ratings yet

- E-Text Unit 2: Concept of SupplyDocument29 pagesE-Text Unit 2: Concept of SupplyrajneeshkarloopiaNo ratings yet

- E-Text Unit 2: Concept of SupplyDocument29 pagesE-Text Unit 2: Concept of SupplyrajneeshkarloopiaNo ratings yet

- Specimen For ITC Denial Against Receipt of GoodsDocument5 pagesSpecimen For ITC Denial Against Receipt of Goodssvasan32453No ratings yet

- Taxsutra All Rights ReservedDocument8 pagesTaxsutra All Rights ReservedAlpa Shah DesaiNo ratings yet

- RERA Order No 38 Non-Negotiable Claues in The AFSDocument8 pagesRERA Order No 38 Non-Negotiable Claues in The AFSSanjeev KumarNo ratings yet

- Conveyancing Project WorkDocument3 pagesConveyancing Project WorkBenjamin Brian NgongaNo ratings yet

- Preliminary Draft Rent Stabilization and Tenant Protection Ordinance (March 26 2024)Document25 pagesPreliminary Draft Rent Stabilization and Tenant Protection Ordinance (March 26 2024)lcNo ratings yet

- Account StandardDocument11 pagesAccount StandardAnuranjan VermaNo ratings yet

- Works Contract of Movable Property - Supply of Service' Under GST?Document2 pagesWorks Contract of Movable Property - Supply of Service' Under GST?Kishor SinghNo ratings yet

- 11 - Chapter 5 PDFDocument97 pages11 - Chapter 5 PDFReshma MallickNo ratings yet

- GST AssignmentDocument16 pagesGST AssignmentAnvesha ChaturvediNo ratings yet

- Section 13 of The Integrated Goods and Services ActDocument3 pagesSection 13 of The Integrated Goods and Services ActNikita BaliNo ratings yet

- CH 2 Supply Under GSTDocument8 pagesCH 2 Supply Under GSTRudra JhaNo ratings yet

- Taxable Event in GST 3.1 Meaning of Taxable EventDocument24 pagesTaxable Event in GST 3.1 Meaning of Taxable Eventhariom bajpaiNo ratings yet

- Import and Export Under GSTDocument50 pagesImport and Export Under GSTSONICK THUKKANINo ratings yet

- gstr2011 d002Document83 pagesgstr2011 d002jndelamora18No ratings yet

- UNIT 2 (3) Place of SupplyDocument25 pagesUNIT 2 (3) Place of SupplySania KhanNo ratings yet

- Circular 14 2021Document8 pagesCircular 14 2021SachinNo ratings yet

- DTC Agreement Between Zambia and SeychellesDocument31 pagesDTC Agreement Between Zambia and SeychellesOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- Where Two Provisions of The Law of The Same Hierarchy Conflicts One Another The...Document9 pagesWhere Two Provisions of The Law of The Same Hierarchy Conflicts One Another The...LDC Online ResourcesNo ratings yet

- White Paper - Isd and Cross Charge Mechanism Under GST RegimeDocument10 pagesWhite Paper - Isd and Cross Charge Mechanism Under GST Regimeprivate completelyNo ratings yet

- Master Circular For Registrars To An Issue and Share Transfer Agents Dated May 17, 2023Document9 pagesMaster Circular For Registrars To An Issue and Share Transfer Agents Dated May 17, 2023kirti sharmaNo ratings yet

- (Pro-Forma) : WHEREAS, The RE Developer Is Authorized To Proceed To The Development Stage of Its RenewableDocument13 pages(Pro-Forma) : WHEREAS, The RE Developer Is Authorized To Proceed To The Development Stage of Its RenewableJoy AlamedaNo ratings yet

- DTC Agreement Between Nepal and AustriaDocument27 pagesDTC Agreement Between Nepal and AustriaOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Eligibility Criteria For FEMA Assistance - FEMA - GovDocument6 pagesEligibility Criteria For FEMA Assistance - FEMA - GovHenry FranksNo ratings yet

- Dr. Cherry Mae L. Limbaco, Ceso VDocument3 pagesDr. Cherry Mae L. Limbaco, Ceso VKatherine DahangNo ratings yet

- Nar 42 SpaDocument14 pagesNar 42 SpaAura Abadi DjayaNo ratings yet

- Condemnation FilesDocument5 pagesCondemnation FilesApril Joy Sumagit HidalgoNo ratings yet

- Bhagat Bolton (2019)Document27 pagesBhagat Bolton (2019)Muhammad Bilal Awan Deputy DirectorNo ratings yet

- Jonbenet RamseyDocument17 pagesJonbenet RamseyRosario Arrieta peralesNo ratings yet

- MEMORIALDocument25 pagesMEMORIALPrerika NarangNo ratings yet

- Case Diary GulabDocument15 pagesCase Diary GulabJai ShreeramNo ratings yet

- S170Document3 pagesS170dssfdNo ratings yet

- Zeldas Lullaby - Ukulele Fingerstyle Tab Easy VersionDocument2 pagesZeldas Lullaby - Ukulele Fingerstyle Tab Easy VersionAlvaro RuizNo ratings yet

- Civil Appeal 146 of 2013Document4 pagesCivil Appeal 146 of 2013Philip MalangaNo ratings yet

- The Universal Declaration of Human Rights (UdhrDocument7 pagesThe Universal Declaration of Human Rights (UdhrSanskruti JagtapNo ratings yet

- Guanio V Makati Shangri-LaDocument10 pagesGuanio V Makati Shangri-LaKathNo ratings yet

- Ano Ang RA 1425?Document2 pagesAno Ang RA 1425?ches g70% (20)

- Motion To Allow Accused To Undergo Medical Examination: Regional Trial Court of BoholDocument2 pagesMotion To Allow Accused To Undergo Medical Examination: Regional Trial Court of BoholralplaguraNo ratings yet

- Melencio-Herrera, J.:: Tax. Until The National Assembly Shall Provide Otherwise, TheDocument2 pagesMelencio-Herrera, J.:: Tax. Until The National Assembly Shall Provide Otherwise, TheIra Francia AlcazarNo ratings yet

- HUBILLADocument11 pagesHUBILLAMarry LooydNo ratings yet

- Crimpro PreliminariesDocument46 pagesCrimpro PreliminariesHarold Saldy CasalemNo ratings yet

- Ocean Builders Construction Corp. vs. Cubacub PDFDocument20 pagesOcean Builders Construction Corp. vs. Cubacub PDFAnonymousNo ratings yet

- Declaration of Security Between A Vessel and A Marine Facility (Canada)Document3 pagesDeclaration of Security Between A Vessel and A Marine Facility (Canada)Steve Yh HuangNo ratings yet

- Airworthiness Directive Cancellation Notice: Design Approval Holder's Name: Type/Model Designation(s)Document2 pagesAirworthiness Directive Cancellation Notice: Design Approval Holder's Name: Type/Model Designation(s)Bob DENARDNo ratings yet

- Chapter 3 - Legal, Ethical, and Professional Issues in Information SecurityDocument7 pagesChapter 3 - Legal, Ethical, and Professional Issues in Information SecurityAshura OsipNo ratings yet

- Executive Order No. 542Document2 pagesExecutive Order No. 542Jey RhyNo ratings yet

- English 9 Q1 1 - Modals Used in Expressing Permission, Obligation, and ProhibitionDocument33 pagesEnglish 9 Q1 1 - Modals Used in Expressing Permission, Obligation, and ProhibitionMarilyn GuillermoNo ratings yet

- Cover Note 8d0a8ac 1Document2 pagesCover Note 8d0a8ac 1fahmie halimNo ratings yet

- Civ1 4SCDE1920 Doctrines PersonsDocument47 pagesCiv1 4SCDE1920 Doctrines PersonsSpartansNo ratings yet

- UntitledDocument1 pageUntitledREZA KURNIAWANNo ratings yet

- Memorandum of Agreement SampleDocument3 pagesMemorandum of Agreement SampleFatMan87No ratings yet

- Contract Unit 1Document10 pagesContract Unit 1SGENo ratings yet

- Estate TaxDocument48 pagesEstate TaxBhosx Kim100% (1)

Download as pdf or txt

You might also like

- Genuine Sale Transactions Through Gpa Is Not Barred by Supreme Court Decision For KarnatakaDocument3 pagesGenuine Sale Transactions Through Gpa Is Not Barred by Supreme Court Decision For KarnatakaSridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್100% (1)

- Place of SupplyDocument29 pagesPlace of SupplyShravan NiranjanNo ratings yet

- 14725603564.place of Supply of ServicesDocument12 pages14725603564.place of Supply of ServicesScribbler 414No ratings yet

- By Anandram Sankar GENERALLY, SEZ Entities Export Goods/services or Supply Goods/services To Entities inDocument3 pagesBy Anandram Sankar GENERALLY, SEZ Entities Export Goods/services or Supply Goods/services To Entities inChintan VasaNo ratings yet

- Place of SupplyDocument22 pagesPlace of Supplyanujdas173No ratings yet

- Article - GST On Washout Charges or Liquidated DamagesDocument6 pagesArticle - GST On Washout Charges or Liquidated DamagessupdtconflNo ratings yet

- Power Roles and Responsibilities - Offences Booked by Roving Squad OfficersDocument16 pagesPower Roles and Responsibilities - Offences Booked by Roving Squad OfficersAnandd BabunathNo ratings yet

- Answes: C 1& 2: I, S: Hapter Ntroduction UpplyDocument49 pagesAnswes: C 1& 2: I, S: Hapter Ntroduction UpplyJoseph PrabhuNo ratings yet

- GST Detailed AnalysisDocument10 pagesGST Detailed AnalysisKritibandhu SwainNo ratings yet

- AAR - IGST Is Chargable On Ex-Factory Supplies Where Movement of Goods Terminates in Other StateDocument4 pagesAAR - IGST Is Chargable On Ex-Factory Supplies Where Movement of Goods Terminates in Other StateJigar MakwanaNo ratings yet

- Unit II-Some Basics: Be A Mix of Theory Questions and Numericals/ Situations/ CasesDocument9 pagesUnit II-Some Basics: Be A Mix of Theory Questions and Numericals/ Situations/ CasesArushi GuptaNo ratings yet

- 027 D Dhruv TankDocument26 pages027 D Dhruv TankPrince SoundhNo ratings yet

- Taxation LawDocument16 pagesTaxation Lawsankalp patelNo ratings yet

- Place of SuplyDocument101 pagesPlace of SuplyPremNo ratings yet

- Place of Supply IgstDocument101 pagesPlace of Supply Igsthariom bajpaiNo ratings yet

- GST Manual Sample ChapterDocument6 pagesGST Manual Sample ChapterRishabh vermaNo ratings yet

- Place of Supply: After Studying This Chapter, You Will Be Able ToDocument85 pagesPlace of Supply: After Studying This Chapter, You Will Be Able ToRohit SoniNo ratings yet

- Supplemental Guidelines For Brokers and Salespersons Mc-15-02aDocument13 pagesSupplemental Guidelines For Brokers and Salespersons Mc-15-02aAl MarzolNo ratings yet

- Interstate and Intrastate Transactions Under GSTDocument11 pagesInterstate and Intrastate Transactions Under GSTD.Naga RajuNo ratings yet

- 5b8d6 Liability W.R.T. Jda Entered Prior To GST ArticleDocument3 pages5b8d6 Liability W.R.T. Jda Entered Prior To GST ArticleKunalKumarNo ratings yet

- CH 5 Place of SupplyDocument63 pagesCH 5 Place of SupplyManas Kumar SahooNo ratings yet

- 47321bosfinal p8 Part1 cp5Document61 pages47321bosfinal p8 Part1 cp5doomraoffice2019No ratings yet

- Research MaterialDocument2 pagesResearch Materialyogeshshukla.ys14No ratings yet

- IGST Act With Amendments 1Document14 pagesIGST Act With Amendments 1sanjitaNo ratings yet

- Situs of SupplyDocument8 pagesSitus of SupplyManish SachdevaNo ratings yet

- Place of SupplyDocument8 pagesPlace of SupplyIshita YadavNo ratings yet

- Taxation of Intermediary Services Under GSTDocument11 pagesTaxation of Intermediary Services Under GSTShyaam SheoranNo ratings yet

- Place of Supply: After Studying This Chapter, You Will Be Able ToDocument85 pagesPlace of Supply: After Studying This Chapter, You Will Be Able TooverclockthesunNo ratings yet

- Final GST Analysis 2016Document154 pagesFinal GST Analysis 2016Ca Dhruv AgrawalNo ratings yet

- GST AmendmentsDocument15 pagesGST AmendmentsSana KhanNo ratings yet

- Cir 184 16 2022 CGSTDocument4 pagesCir 184 16 2022 CGSTAmritesh RaiNo ratings yet

- Circular No 209 03 2024Document3 pagesCircular No 209 03 2024SSSARMANo ratings yet

- 75915bos61400 cp3Document120 pages75915bos61400 cp3Bhanu RawatNo ratings yet

- Faculty of Law Jamia Millia Islamia: Income From House PropertyDocument21 pagesFaculty of Law Jamia Millia Islamia: Income From House PropertyMohdSaqibNo ratings yet

- Organised By:: National Conference On GSTDocument19 pagesOrganised By:: National Conference On GSTSunil ShahNo ratings yet

- E-Text Unit 2: Concept of SupplyDocument29 pagesE-Text Unit 2: Concept of SupplyrajneeshkarloopiaNo ratings yet

- E-Text Unit 2: Concept of SupplyDocument29 pagesE-Text Unit 2: Concept of SupplyrajneeshkarloopiaNo ratings yet

- Specimen For ITC Denial Against Receipt of GoodsDocument5 pagesSpecimen For ITC Denial Against Receipt of Goodssvasan32453No ratings yet

- Taxsutra All Rights ReservedDocument8 pagesTaxsutra All Rights ReservedAlpa Shah DesaiNo ratings yet

- RERA Order No 38 Non-Negotiable Claues in The AFSDocument8 pagesRERA Order No 38 Non-Negotiable Claues in The AFSSanjeev KumarNo ratings yet

- Conveyancing Project WorkDocument3 pagesConveyancing Project WorkBenjamin Brian NgongaNo ratings yet

- Preliminary Draft Rent Stabilization and Tenant Protection Ordinance (March 26 2024)Document25 pagesPreliminary Draft Rent Stabilization and Tenant Protection Ordinance (March 26 2024)lcNo ratings yet

- Account StandardDocument11 pagesAccount StandardAnuranjan VermaNo ratings yet

- Works Contract of Movable Property - Supply of Service' Under GST?Document2 pagesWorks Contract of Movable Property - Supply of Service' Under GST?Kishor SinghNo ratings yet

- 11 - Chapter 5 PDFDocument97 pages11 - Chapter 5 PDFReshma MallickNo ratings yet

- GST AssignmentDocument16 pagesGST AssignmentAnvesha ChaturvediNo ratings yet

- Section 13 of The Integrated Goods and Services ActDocument3 pagesSection 13 of The Integrated Goods and Services ActNikita BaliNo ratings yet

- CH 2 Supply Under GSTDocument8 pagesCH 2 Supply Under GSTRudra JhaNo ratings yet

- Taxable Event in GST 3.1 Meaning of Taxable EventDocument24 pagesTaxable Event in GST 3.1 Meaning of Taxable Eventhariom bajpaiNo ratings yet

- Import and Export Under GSTDocument50 pagesImport and Export Under GSTSONICK THUKKANINo ratings yet

- gstr2011 d002Document83 pagesgstr2011 d002jndelamora18No ratings yet

- UNIT 2 (3) Place of SupplyDocument25 pagesUNIT 2 (3) Place of SupplySania KhanNo ratings yet

- Circular 14 2021Document8 pagesCircular 14 2021SachinNo ratings yet

- DTC Agreement Between Zambia and SeychellesDocument31 pagesDTC Agreement Between Zambia and SeychellesOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- Where Two Provisions of The Law of The Same Hierarchy Conflicts One Another The...Document9 pagesWhere Two Provisions of The Law of The Same Hierarchy Conflicts One Another The...LDC Online ResourcesNo ratings yet

- White Paper - Isd and Cross Charge Mechanism Under GST RegimeDocument10 pagesWhite Paper - Isd and Cross Charge Mechanism Under GST Regimeprivate completelyNo ratings yet

- Master Circular For Registrars To An Issue and Share Transfer Agents Dated May 17, 2023Document9 pagesMaster Circular For Registrars To An Issue and Share Transfer Agents Dated May 17, 2023kirti sharmaNo ratings yet

- (Pro-Forma) : WHEREAS, The RE Developer Is Authorized To Proceed To The Development Stage of Its RenewableDocument13 pages(Pro-Forma) : WHEREAS, The RE Developer Is Authorized To Proceed To The Development Stage of Its RenewableJoy AlamedaNo ratings yet

- DTC Agreement Between Nepal and AustriaDocument27 pagesDTC Agreement Between Nepal and AustriaOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Eligibility Criteria For FEMA Assistance - FEMA - GovDocument6 pagesEligibility Criteria For FEMA Assistance - FEMA - GovHenry FranksNo ratings yet

- Dr. Cherry Mae L. Limbaco, Ceso VDocument3 pagesDr. Cherry Mae L. Limbaco, Ceso VKatherine DahangNo ratings yet

- Nar 42 SpaDocument14 pagesNar 42 SpaAura Abadi DjayaNo ratings yet

- Condemnation FilesDocument5 pagesCondemnation FilesApril Joy Sumagit HidalgoNo ratings yet

- Bhagat Bolton (2019)Document27 pagesBhagat Bolton (2019)Muhammad Bilal Awan Deputy DirectorNo ratings yet

- Jonbenet RamseyDocument17 pagesJonbenet RamseyRosario Arrieta peralesNo ratings yet

- MEMORIALDocument25 pagesMEMORIALPrerika NarangNo ratings yet

- Case Diary GulabDocument15 pagesCase Diary GulabJai ShreeramNo ratings yet

- S170Document3 pagesS170dssfdNo ratings yet

- Zeldas Lullaby - Ukulele Fingerstyle Tab Easy VersionDocument2 pagesZeldas Lullaby - Ukulele Fingerstyle Tab Easy VersionAlvaro RuizNo ratings yet

- Civil Appeal 146 of 2013Document4 pagesCivil Appeal 146 of 2013Philip MalangaNo ratings yet

- The Universal Declaration of Human Rights (UdhrDocument7 pagesThe Universal Declaration of Human Rights (UdhrSanskruti JagtapNo ratings yet

- Guanio V Makati Shangri-LaDocument10 pagesGuanio V Makati Shangri-LaKathNo ratings yet

- Ano Ang RA 1425?Document2 pagesAno Ang RA 1425?ches g70% (20)

- Motion To Allow Accused To Undergo Medical Examination: Regional Trial Court of BoholDocument2 pagesMotion To Allow Accused To Undergo Medical Examination: Regional Trial Court of BoholralplaguraNo ratings yet

- Melencio-Herrera, J.:: Tax. Until The National Assembly Shall Provide Otherwise, TheDocument2 pagesMelencio-Herrera, J.:: Tax. Until The National Assembly Shall Provide Otherwise, TheIra Francia AlcazarNo ratings yet

- HUBILLADocument11 pagesHUBILLAMarry LooydNo ratings yet

- Crimpro PreliminariesDocument46 pagesCrimpro PreliminariesHarold Saldy CasalemNo ratings yet

- Ocean Builders Construction Corp. vs. Cubacub PDFDocument20 pagesOcean Builders Construction Corp. vs. Cubacub PDFAnonymousNo ratings yet

- Declaration of Security Between A Vessel and A Marine Facility (Canada)Document3 pagesDeclaration of Security Between A Vessel and A Marine Facility (Canada)Steve Yh HuangNo ratings yet

- Airworthiness Directive Cancellation Notice: Design Approval Holder's Name: Type/Model Designation(s)Document2 pagesAirworthiness Directive Cancellation Notice: Design Approval Holder's Name: Type/Model Designation(s)Bob DENARDNo ratings yet

- Chapter 3 - Legal, Ethical, and Professional Issues in Information SecurityDocument7 pagesChapter 3 - Legal, Ethical, and Professional Issues in Information SecurityAshura OsipNo ratings yet

- Executive Order No. 542Document2 pagesExecutive Order No. 542Jey RhyNo ratings yet

- English 9 Q1 1 - Modals Used in Expressing Permission, Obligation, and ProhibitionDocument33 pagesEnglish 9 Q1 1 - Modals Used in Expressing Permission, Obligation, and ProhibitionMarilyn GuillermoNo ratings yet

- Cover Note 8d0a8ac 1Document2 pagesCover Note 8d0a8ac 1fahmie halimNo ratings yet

- Civ1 4SCDE1920 Doctrines PersonsDocument47 pagesCiv1 4SCDE1920 Doctrines PersonsSpartansNo ratings yet

- UntitledDocument1 pageUntitledREZA KURNIAWANNo ratings yet

- Memorandum of Agreement SampleDocument3 pagesMemorandum of Agreement SampleFatMan87No ratings yet

- Contract Unit 1Document10 pagesContract Unit 1SGENo ratings yet

- Estate TaxDocument48 pagesEstate TaxBhosx Kim100% (1)