Encl. As Above: Sunil Kumar Bansal

Encl. As Above: Sunil Kumar Bansal

You might also like

- Problem: Andres Adi Putra S 43220110067 AKM2-Forum 6Document17 pagesProblem: Andres Adi Putra S 43220110067 AKM2-Forum 6tes doangNo ratings yet

- Quiz 1Document3 pagesQuiz 1Yong RenNo ratings yet

- BSE Limited National Stock Exchange of India Limited: Madhu R DeoraDocument25 pagesBSE Limited National Stock Exchange of India Limited: Madhu R DeoraLAKHAN TRIVEDINo ratings yet

- Paytm RBI Direction To PPBL 1 Feb 2024Document20 pagesPaytm RBI Direction To PPBL 1 Feb 2024sunmayjioNo ratings yet

- Relations/financial-Results: Encl.: As AboveDocument16 pagesRelations/financial-Results: Encl.: As Abovekrishna PatelNo ratings yet

- Category) On The Board of The Bank, With Effect From April 11, 2024, Who Shall Hold Office As AnDocument3 pagesCategory) On The Board of The Bank, With Effect From April 11, 2024, Who Shall Hold Office As AnBrojo Gopal GhoshNo ratings yet

- Muthoottu NCD PDFDocument244 pagesMuthoottu NCD PDFvivekrajbhilai5850No ratings yet

- BSE 13052024130348 NSEintimationDocument21 pagesBSE 13052024130348 NSEintimationSonu GargNo ratings yet

- IP Sep22Document64 pagesIP Sep22seema202425No ratings yet

- Fed ImpactDocument39 pagesFed Impactpimewip969No ratings yet

- L&T Financi L Services: A e H S e e eDocument53 pagesL&T Financi L Services: A e H S e e eNimesh PatelNo ratings yet

- SOUTHBANK_15062024120027_STTED_SIGNEDDocument2 pagesSOUTHBANK_15062024120027_STTED_SIGNEDVijay VittalNo ratings yet

- Khush HFL - Annual Report March 22Document53 pagesKhush HFL - Annual Report March 22shivabharath.sugaliNo ratings yet

- EarningUpdatesPresentation BBL 30092021 PDFDocument29 pagesEarningUpdatesPresentation BBL 30092021 PDFsuman sheikhNo ratings yet

- Credit Access Grameen After AcquisationDocument63 pagesCredit Access Grameen After AcquisationNihal YnNo ratings yet

- FDH Bank Prospectus Digital PDFDocument152 pagesFDH Bank Prospectus Digital PDFhope mfungwe100% (1)

- PHL PreliminaryinformationmemorandumDocument114 pagesPHL PreliminaryinformationmemorandumVishwas PatilNo ratings yet

- IDFC First Bank Q4 Results UpdateDocument22 pagesIDFC First Bank Q4 Results UpdateRishab WahalNo ratings yet

- Muthoottu Mini Financiers Limited: Debenture Trustee" On Page 33Document241 pagesMuthoottu Mini Financiers Limited: Debenture Trustee" On Page 33Rehab India FoundationNo ratings yet

- M V Srinivasa Murthy: NCC LimitedDocument18 pagesM V Srinivasa Murthy: NCC Limitedkiranvaishnav527No ratings yet

- July 22, 2019: "Kotak Mahindra Bank Q1 FY20 Earnings Conference Call"Document19 pagesJuly 22, 2019: "Kotak Mahindra Bank Q1 FY20 Earnings Conference Call"divya mNo ratings yet

- Happiest Minds Con CallDocument29 pagesHappiest Minds Con Callimran arifNo ratings yet

- Paytm EarningsDocument25 pagesPaytm Earningsjackhack220No ratings yet

- Dina Nath Kumar: Nse Symbol: Indianb BSE Scrip Code-532814Document15 pagesDina Nath Kumar: Nse Symbol: Indianb BSE Scrip Code-532814dipesh.shopNo ratings yet

- Investor Presentation (Company Update)Document59 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Rohan Purshottamda S MittalDocument39 pagesRohan Purshottamda S Mittalgautamkothari2002No ratings yet

- Final PIM and EOI Request - 1 Dec 2022 - NMDC Steel Limited.Document95 pagesFinal PIM and EOI Request - 1 Dec 2022 - NMDC Steel Limited.sabyasachi beheraNo ratings yet

- Avantel StockDocument18 pagesAvantel StockAjin LeoNo ratings yet

- Investor / Analyst Presentation (Company Update)Document48 pagesInvestor / Analyst Presentation (Company Update)Shyam SunderNo ratings yet

- Earnings Transcript (Q3-FY 21)Document17 pagesEarnings Transcript (Q3-FY 21)beza manojNo ratings yet

- Investor Presentation Q3 FY2012-13 (15-January-2013) PDFDocument33 pagesInvestor Presentation Q3 FY2012-13 (15-January-2013) PDFRohit ShawNo ratings yet

- MoneyBoxx Earning Call Transcript 3Document20 pagesMoneyBoxx Earning Call Transcript 3shashank.keNo ratings yet

- Company Ujjivan Financial Investor PresentationDocument58 pagesCompany Ujjivan Financial Investor Presentationrahul patelNo ratings yet

- Navin Fluorine International LTD 532504 March 2019Document217 pagesNavin Fluorine International LTD 532504 March 2019dwivedishantanuNo ratings yet

- Fy 20Document20 pagesFy 20Guru DarshanNo ratings yet

- G. M. Breweries Limited: 35th Annual Report 2017-2018Document68 pagesG. M. Breweries Limited: 35th Annual Report 2017-2018kishore13No ratings yet

- Investor Presentation - June 2011Document53 pagesInvestor Presentation - June 2011Chhavi JainNo ratings yet

- Pnjdent: Prudent Advisory Services LTDDocument20 pagesPnjdent: Prudent Advisory Services LTDDasari PrabodhNo ratings yet

- Pncal: Pr/ColDocument15 pagesPncal: Pr/ColSanjeev KumarNo ratings yet

- Investor Presentation (Company Update)Document53 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Deshpande Nida Yunus: KPIT Technologies LimitedDocument22 pagesDeshpande Nida Yunus: KPIT Technologies LimitedJ&J ChannelNo ratings yet

- National Stock Exchange of India Limited, BSE Limited,: Geetanjali Santosh VaidyaDocument14 pagesNational Stock Exchange of India Limited, BSE Limited,: Geetanjali Santosh Vaidyanthakur.ntNo ratings yet

- Engagement Letter For VCFO - Hero Electric 2Document3 pagesEngagement Letter For VCFO - Hero Electric 2Amit MNo ratings yet

- Kosamattam Finance Limited Prospectus AprilDocument287 pagesKosamattam Finance Limited Prospectus Aprilmehtarahul999No ratings yet

- Central Depository Services (India) LimitedDocument17 pagesCentral Depository Services (India) Limitedpratik567No ratings yet

- mamaearth_concallDocument18 pagesmamaearth_concallliltity72No ratings yet

- Axis 2Document6 pagesAxis 2srikanthbitra1412No ratings yet

- HDB Annual Report11 12Document49 pagesHDB Annual Report11 12Hariharasudan HariNo ratings yet

- MCF Ar 2019 20Document123 pagesMCF Ar 2019 20Hariprasad bhatNo ratings yet

- IPO Outlook - BLS E-Services LTDDocument2 pagesIPO Outlook - BLS E-Services LTDalkeshkNo ratings yet

- MNCN - Laporan Informasi Dan Fakta Material - 31335204 - Lamp2Document4 pagesMNCN - Laporan Informasi Dan Fakta Material - 31335204 - Lamp2Andri ChandraNo ratings yet

- Intertec Technologies Annual Report - 2012Document85 pagesIntertec Technologies Annual Report - 2012DeepakGarudNo ratings yet

- Secretarial Department: Rajaraman SundaresanDocument14 pagesSecretarial Department: Rajaraman Sundaresanpruthvirajcoc6No ratings yet

- Sub: Earnings Call Transcript: Sanja Y JainDocument24 pagesSub: Earnings Call Transcript: Sanja Y Jainpratik567No ratings yet

- Dhani Loans and Services Limited: Related Information" On Page 199Document506 pagesDhani Loans and Services Limited: Related Information" On Page 199Aman KhanNo ratings yet

- Zentec 09052024173129 CL TDocument13 pagesZentec 09052024173129 CL TaadinaravNo ratings yet

- Corporate Presentation (Company Update)Document35 pagesCorporate Presentation (Company Update)Shyam SunderNo ratings yet

- Sonear Industries Limited - Draft Red Herring ProspectusDocument238 pagesSonear Industries Limited - Draft Red Herring ProspectusManjeet KhannaNo ratings yet

- 8thAnnualReport FCL 2010 2011Document38 pages8thAnnualReport FCL 2010 2011Jilesh PabariNo ratings yet

- InvestorPresentation2022 23Document37 pagesInvestorPresentation2022 23Basavaraj GadachintiNo ratings yet

- Financing Handbook for Companies: A Practical Guide by A Banking Executive for Companies Seeking Loans & Financings from BanksFrom EverandFinancing Handbook for Companies: A Practical Guide by A Banking Executive for Companies Seeking Loans & Financings from BanksRating: 5 out of 5 stars5/5 (1)

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- Wise Transaction Invoice Transfer 830772036 1799234782 enDocument2 pagesWise Transaction Invoice Transfer 830772036 1799234782 enfin.tommy.redNo ratings yet

- CORPO LAW 2019 Part 3Document3 pagesCORPO LAW 2019 Part 3Sinetch EteyNo ratings yet

- Thesis Title For Banking and FinanceDocument7 pagesThesis Title For Banking and Financebsqfc4d5100% (2)

- Time Value of MoneyDocument5 pagesTime Value of MoneyJohn Francis IdananNo ratings yet

- Afar Part 1 (2017 Edition) - Sample OnlyDocument58 pagesAfar Part 1 (2017 Edition) - Sample OnlyCM Lance67% (3)

- JP Morgan - Audacity of BitcoinDocument8 pagesJP Morgan - Audacity of Bitcoinarthurnitsopoulos_14No ratings yet

- Project FinancingDocument4 pagesProject FinancingRishabh JainNo ratings yet

- Spouses Eduardo and Lydia Silos Vs Philippine National Bank (PNB)Document6 pagesSpouses Eduardo and Lydia Silos Vs Philippine National Bank (PNB)gregbaccayNo ratings yet

- Financial Instruments Revision YtDocument98 pagesFinancial Instruments Revision YtRaja kumarNo ratings yet

- BhaskarJha, CQF, FRMProfileDocument3 pagesBhaskarJha, CQF, FRMProfileyezdiarwNo ratings yet

- BSF 2112 - Financial Markets and Institutions - August 2022Document6 pagesBSF 2112 - Financial Markets and Institutions - August 2022SaeedNo ratings yet

- Role of Advisors Towards of E-AdvisoryDocument66 pagesRole of Advisors Towards of E-AdvisoryJď SharmaNo ratings yet

- J WF 1 J Lflujq Iaj AnDocument13 pagesJ WF 1 J Lflujq Iaj AnOmprakash JhaNo ratings yet

- N5 Financial Accounting November 2016 MemorandumDocument4 pagesN5 Financial Accounting November 2016 MemorandumTsholofeloNo ratings yet

- Def 3Document48 pagesDef 3Alberto Miguel YuNo ratings yet

- 02Document12 pages02Quang Nguyễn PhúNo ratings yet

- 2010 L 42 Valuation Basis (Health)Document18 pages2010 L 42 Valuation Basis (Health)VivekNo ratings yet

- Submitted By: Vivek SharmaDocument18 pagesSubmitted By: Vivek SharmaVe1kNo ratings yet

- Top 100 Private Equity FirmsDocument20 pagesTop 100 Private Equity FirmssosteniblebusinessNo ratings yet

- The Command Center-Lesson 1Document31 pagesThe Command Center-Lesson 1Dan Marie MorataNo ratings yet

- Pilgram BankDocument9 pagesPilgram BankJasmine ZhuNo ratings yet

- Balance Sheet of Tata MotorsDocument6 pagesBalance Sheet of Tata Motorsnehanayaka25No ratings yet

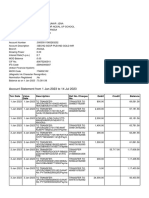

- Account Statement From 1 Jan 2023 To 14 Jul 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Jan 2023 To 14 Jul 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAmit Kumar JenaNo ratings yet

- English For Banking and FinanceDocument28 pagesEnglish For Banking and FinancefathiyarizkiNo ratings yet

- Retirement & Death Assignment NewDocument3 pagesRetirement & Death Assignment Newsakshamagnihotri0No ratings yet

- Insights of Mutual Funds For Retail InvestorsDocument11 pagesInsights of Mutual Funds For Retail InvestorsjayminashahNo ratings yet

- Financial Statement Analysis: Manaac430 - Uno-RDocument10 pagesFinancial Statement Analysis: Manaac430 - Uno-RJulliena BakersNo ratings yet

- Unit 5. Payment. L1Document3 pagesUnit 5. Payment. L1halam29051997No ratings yet

Download as pdf or txt

You might also like

- Problem: Andres Adi Putra S 43220110067 AKM2-Forum 6Document17 pagesProblem: Andres Adi Putra S 43220110067 AKM2-Forum 6tes doangNo ratings yet

- Quiz 1Document3 pagesQuiz 1Yong RenNo ratings yet

- BSE Limited National Stock Exchange of India Limited: Madhu R DeoraDocument25 pagesBSE Limited National Stock Exchange of India Limited: Madhu R DeoraLAKHAN TRIVEDINo ratings yet

- Paytm RBI Direction To PPBL 1 Feb 2024Document20 pagesPaytm RBI Direction To PPBL 1 Feb 2024sunmayjioNo ratings yet

- Relations/financial-Results: Encl.: As AboveDocument16 pagesRelations/financial-Results: Encl.: As Abovekrishna PatelNo ratings yet

- Category) On The Board of The Bank, With Effect From April 11, 2024, Who Shall Hold Office As AnDocument3 pagesCategory) On The Board of The Bank, With Effect From April 11, 2024, Who Shall Hold Office As AnBrojo Gopal GhoshNo ratings yet

- Muthoottu NCD PDFDocument244 pagesMuthoottu NCD PDFvivekrajbhilai5850No ratings yet

- BSE 13052024130348 NSEintimationDocument21 pagesBSE 13052024130348 NSEintimationSonu GargNo ratings yet

- IP Sep22Document64 pagesIP Sep22seema202425No ratings yet

- Fed ImpactDocument39 pagesFed Impactpimewip969No ratings yet

- L&T Financi L Services: A e H S e e eDocument53 pagesL&T Financi L Services: A e H S e e eNimesh PatelNo ratings yet

- SOUTHBANK_15062024120027_STTED_SIGNEDDocument2 pagesSOUTHBANK_15062024120027_STTED_SIGNEDVijay VittalNo ratings yet

- Khush HFL - Annual Report March 22Document53 pagesKhush HFL - Annual Report March 22shivabharath.sugaliNo ratings yet

- EarningUpdatesPresentation BBL 30092021 PDFDocument29 pagesEarningUpdatesPresentation BBL 30092021 PDFsuman sheikhNo ratings yet

- Credit Access Grameen After AcquisationDocument63 pagesCredit Access Grameen After AcquisationNihal YnNo ratings yet

- FDH Bank Prospectus Digital PDFDocument152 pagesFDH Bank Prospectus Digital PDFhope mfungwe100% (1)

- PHL PreliminaryinformationmemorandumDocument114 pagesPHL PreliminaryinformationmemorandumVishwas PatilNo ratings yet

- IDFC First Bank Q4 Results UpdateDocument22 pagesIDFC First Bank Q4 Results UpdateRishab WahalNo ratings yet

- Muthoottu Mini Financiers Limited: Debenture Trustee" On Page 33Document241 pagesMuthoottu Mini Financiers Limited: Debenture Trustee" On Page 33Rehab India FoundationNo ratings yet

- M V Srinivasa Murthy: NCC LimitedDocument18 pagesM V Srinivasa Murthy: NCC Limitedkiranvaishnav527No ratings yet

- July 22, 2019: "Kotak Mahindra Bank Q1 FY20 Earnings Conference Call"Document19 pagesJuly 22, 2019: "Kotak Mahindra Bank Q1 FY20 Earnings Conference Call"divya mNo ratings yet

- Happiest Minds Con CallDocument29 pagesHappiest Minds Con Callimran arifNo ratings yet

- Paytm EarningsDocument25 pagesPaytm Earningsjackhack220No ratings yet

- Dina Nath Kumar: Nse Symbol: Indianb BSE Scrip Code-532814Document15 pagesDina Nath Kumar: Nse Symbol: Indianb BSE Scrip Code-532814dipesh.shopNo ratings yet

- Investor Presentation (Company Update)Document59 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Rohan Purshottamda S MittalDocument39 pagesRohan Purshottamda S Mittalgautamkothari2002No ratings yet

- Final PIM and EOI Request - 1 Dec 2022 - NMDC Steel Limited.Document95 pagesFinal PIM and EOI Request - 1 Dec 2022 - NMDC Steel Limited.sabyasachi beheraNo ratings yet

- Avantel StockDocument18 pagesAvantel StockAjin LeoNo ratings yet

- Investor / Analyst Presentation (Company Update)Document48 pagesInvestor / Analyst Presentation (Company Update)Shyam SunderNo ratings yet

- Earnings Transcript (Q3-FY 21)Document17 pagesEarnings Transcript (Q3-FY 21)beza manojNo ratings yet

- Investor Presentation Q3 FY2012-13 (15-January-2013) PDFDocument33 pagesInvestor Presentation Q3 FY2012-13 (15-January-2013) PDFRohit ShawNo ratings yet

- MoneyBoxx Earning Call Transcript 3Document20 pagesMoneyBoxx Earning Call Transcript 3shashank.keNo ratings yet

- Company Ujjivan Financial Investor PresentationDocument58 pagesCompany Ujjivan Financial Investor Presentationrahul patelNo ratings yet

- Navin Fluorine International LTD 532504 March 2019Document217 pagesNavin Fluorine International LTD 532504 March 2019dwivedishantanuNo ratings yet

- Fy 20Document20 pagesFy 20Guru DarshanNo ratings yet

- G. M. Breweries Limited: 35th Annual Report 2017-2018Document68 pagesG. M. Breweries Limited: 35th Annual Report 2017-2018kishore13No ratings yet

- Investor Presentation - June 2011Document53 pagesInvestor Presentation - June 2011Chhavi JainNo ratings yet

- Pnjdent: Prudent Advisory Services LTDDocument20 pagesPnjdent: Prudent Advisory Services LTDDasari PrabodhNo ratings yet

- Pncal: Pr/ColDocument15 pagesPncal: Pr/ColSanjeev KumarNo ratings yet

- Investor Presentation (Company Update)Document53 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Deshpande Nida Yunus: KPIT Technologies LimitedDocument22 pagesDeshpande Nida Yunus: KPIT Technologies LimitedJ&J ChannelNo ratings yet

- National Stock Exchange of India Limited, BSE Limited,: Geetanjali Santosh VaidyaDocument14 pagesNational Stock Exchange of India Limited, BSE Limited,: Geetanjali Santosh Vaidyanthakur.ntNo ratings yet

- Engagement Letter For VCFO - Hero Electric 2Document3 pagesEngagement Letter For VCFO - Hero Electric 2Amit MNo ratings yet

- Kosamattam Finance Limited Prospectus AprilDocument287 pagesKosamattam Finance Limited Prospectus Aprilmehtarahul999No ratings yet

- Central Depository Services (India) LimitedDocument17 pagesCentral Depository Services (India) Limitedpratik567No ratings yet

- mamaearth_concallDocument18 pagesmamaearth_concallliltity72No ratings yet

- Axis 2Document6 pagesAxis 2srikanthbitra1412No ratings yet

- HDB Annual Report11 12Document49 pagesHDB Annual Report11 12Hariharasudan HariNo ratings yet

- MCF Ar 2019 20Document123 pagesMCF Ar 2019 20Hariprasad bhatNo ratings yet

- IPO Outlook - BLS E-Services LTDDocument2 pagesIPO Outlook - BLS E-Services LTDalkeshkNo ratings yet

- MNCN - Laporan Informasi Dan Fakta Material - 31335204 - Lamp2Document4 pagesMNCN - Laporan Informasi Dan Fakta Material - 31335204 - Lamp2Andri ChandraNo ratings yet

- Intertec Technologies Annual Report - 2012Document85 pagesIntertec Technologies Annual Report - 2012DeepakGarudNo ratings yet

- Secretarial Department: Rajaraman SundaresanDocument14 pagesSecretarial Department: Rajaraman Sundaresanpruthvirajcoc6No ratings yet

- Sub: Earnings Call Transcript: Sanja Y JainDocument24 pagesSub: Earnings Call Transcript: Sanja Y Jainpratik567No ratings yet

- Dhani Loans and Services Limited: Related Information" On Page 199Document506 pagesDhani Loans and Services Limited: Related Information" On Page 199Aman KhanNo ratings yet

- Zentec 09052024173129 CL TDocument13 pagesZentec 09052024173129 CL TaadinaravNo ratings yet

- Corporate Presentation (Company Update)Document35 pagesCorporate Presentation (Company Update)Shyam SunderNo ratings yet

- Sonear Industries Limited - Draft Red Herring ProspectusDocument238 pagesSonear Industries Limited - Draft Red Herring ProspectusManjeet KhannaNo ratings yet

- 8thAnnualReport FCL 2010 2011Document38 pages8thAnnualReport FCL 2010 2011Jilesh PabariNo ratings yet

- InvestorPresentation2022 23Document37 pagesInvestorPresentation2022 23Basavaraj GadachintiNo ratings yet

- Financing Handbook for Companies: A Practical Guide by A Banking Executive for Companies Seeking Loans & Financings from BanksFrom EverandFinancing Handbook for Companies: A Practical Guide by A Banking Executive for Companies Seeking Loans & Financings from BanksRating: 5 out of 5 stars5/5 (1)

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- Wise Transaction Invoice Transfer 830772036 1799234782 enDocument2 pagesWise Transaction Invoice Transfer 830772036 1799234782 enfin.tommy.redNo ratings yet

- CORPO LAW 2019 Part 3Document3 pagesCORPO LAW 2019 Part 3Sinetch EteyNo ratings yet

- Thesis Title For Banking and FinanceDocument7 pagesThesis Title For Banking and Financebsqfc4d5100% (2)

- Time Value of MoneyDocument5 pagesTime Value of MoneyJohn Francis IdananNo ratings yet

- Afar Part 1 (2017 Edition) - Sample OnlyDocument58 pagesAfar Part 1 (2017 Edition) - Sample OnlyCM Lance67% (3)

- JP Morgan - Audacity of BitcoinDocument8 pagesJP Morgan - Audacity of Bitcoinarthurnitsopoulos_14No ratings yet

- Project FinancingDocument4 pagesProject FinancingRishabh JainNo ratings yet

- Spouses Eduardo and Lydia Silos Vs Philippine National Bank (PNB)Document6 pagesSpouses Eduardo and Lydia Silos Vs Philippine National Bank (PNB)gregbaccayNo ratings yet

- Financial Instruments Revision YtDocument98 pagesFinancial Instruments Revision YtRaja kumarNo ratings yet

- BhaskarJha, CQF, FRMProfileDocument3 pagesBhaskarJha, CQF, FRMProfileyezdiarwNo ratings yet

- BSF 2112 - Financial Markets and Institutions - August 2022Document6 pagesBSF 2112 - Financial Markets and Institutions - August 2022SaeedNo ratings yet

- Role of Advisors Towards of E-AdvisoryDocument66 pagesRole of Advisors Towards of E-AdvisoryJď SharmaNo ratings yet

- J WF 1 J Lflujq Iaj AnDocument13 pagesJ WF 1 J Lflujq Iaj AnOmprakash JhaNo ratings yet

- N5 Financial Accounting November 2016 MemorandumDocument4 pagesN5 Financial Accounting November 2016 MemorandumTsholofeloNo ratings yet

- Def 3Document48 pagesDef 3Alberto Miguel YuNo ratings yet

- 02Document12 pages02Quang Nguyễn PhúNo ratings yet

- 2010 L 42 Valuation Basis (Health)Document18 pages2010 L 42 Valuation Basis (Health)VivekNo ratings yet

- Submitted By: Vivek SharmaDocument18 pagesSubmitted By: Vivek SharmaVe1kNo ratings yet

- Top 100 Private Equity FirmsDocument20 pagesTop 100 Private Equity FirmssosteniblebusinessNo ratings yet

- The Command Center-Lesson 1Document31 pagesThe Command Center-Lesson 1Dan Marie MorataNo ratings yet

- Pilgram BankDocument9 pagesPilgram BankJasmine ZhuNo ratings yet

- Balance Sheet of Tata MotorsDocument6 pagesBalance Sheet of Tata Motorsnehanayaka25No ratings yet

- Account Statement From 1 Jan 2023 To 14 Jul 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Jan 2023 To 14 Jul 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAmit Kumar JenaNo ratings yet

- English For Banking and FinanceDocument28 pagesEnglish For Banking and FinancefathiyarizkiNo ratings yet

- Retirement & Death Assignment NewDocument3 pagesRetirement & Death Assignment Newsakshamagnihotri0No ratings yet

- Insights of Mutual Funds For Retail InvestorsDocument11 pagesInsights of Mutual Funds For Retail InvestorsjayminashahNo ratings yet

- Financial Statement Analysis: Manaac430 - Uno-RDocument10 pagesFinancial Statement Analysis: Manaac430 - Uno-RJulliena BakersNo ratings yet

- Unit 5. Payment. L1Document3 pagesUnit 5. Payment. L1halam29051997No ratings yet