Session 2 Reading - Auditing The Auditors

Session 2 Reading - Auditing The Auditors

You might also like

- DUNOD DCG 2 Droit Des SociétésDocument497 pagesDUNOD DCG 2 Droit Des Sociétésbaptiste100% (14)

- Audit and Assurance. ICAEWDocument336 pagesAudit and Assurance. ICAEWMd. Shafiqul IslamNo ratings yet

- Case 1.1 Enron CorporationDocument6 pagesCase 1.1 Enron CorporationZizhang Huang88% (8)

- Eo Organizing BhertDocument2 pagesEo Organizing BhertPonciano Alvero96% (26)

- Accounting Fraud at Worldcom Corporate Governance AssignmentDocument4 pagesAccounting Fraud at Worldcom Corporate Governance AssignmentTarun BansalNo ratings yet

- What Are The Pressures That Lead Executives and Managers To Cook The BooksDocument4 pagesWhat Are The Pressures That Lead Executives and Managers To Cook The Booksarnabdas1122100% (1)

- Case 2Document7 pagesCase 2sulthanhakimNo ratings yet

- 10 - Questions Week 3Document6 pages10 - Questions Week 3Camilo ToroNo ratings yet

- Central Provident Fund Board: Ms Fikriah Binte Samani 767 Woodlands Circle #07 - 338 SINGAPORE 730767Document6 pagesCentral Provident Fund Board: Ms Fikriah Binte Samani 767 Woodlands Circle #07 - 338 SINGAPORE 730767Fikriah SamaniNo ratings yet

- Eg2401A Summary NotesDocument23 pagesEg2401A Summary NotesYangFan AwakeNo ratings yet

- A Change in How Auditors WorkDocument5 pagesA Change in How Auditors WorkMingDynasty11No ratings yet

- Running Head: Auditing & Assurance Services 1Document9 pagesRunning Head: Auditing & Assurance Services 1Fizah aliNo ratings yet

- Auditor Independence Challenges Faced by External Auditors When Auditing Large Firms in ZimbabweDocument7 pagesAuditor Independence Challenges Faced by External Auditors When Auditing Large Firms in ZimbabweInternational Journal of Business Marketing and ManagementNo ratings yet

- Top 5 Accounting Firms in The PhilippinesDocument8 pagesTop 5 Accounting Firms in The PhilippinesRoselle Hernandez100% (3)

- KPMG AnalysisDocument2 pagesKPMG AnalysisElaine YapNo ratings yet

- Enron CaseDocument3 pagesEnron CaseLaya Isabelle SulartaNo ratings yet

- Auditing As An Aid To Accountability in The Public SectorDocument47 pagesAuditing As An Aid To Accountability in The Public SectorDaniel Obasi100% (2)

- Case 2aDocument3 pagesCase 2a侯燕颉100% (1)

- The Perpetrator's DepartmentDocument6 pagesThe Perpetrator's DepartmentMohamadHasriNo ratings yet

- Pribanic WhitepaperDocument9 pagesPribanic WhitepaperCaleb PribanicNo ratings yet

- Dissertation Topics in Internal AuditingDocument6 pagesDissertation Topics in Internal AuditingBuyCheapPapersOnlineUK100% (1)

- Auditing Dissertation IdeasDocument4 pagesAuditing Dissertation IdeasWebsiteThatWillWriteAPaperForYouSavannah100% (1)

- The Chartered Accountant Oct 11Document144 pagesThe Chartered Accountant Oct 11Vikky Vasvani100% (1)

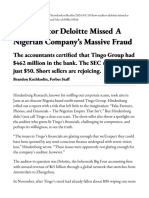

- How Auditor Deloitte Missed A Nigerian Company's Massive FraudDocument8 pagesHow Auditor Deloitte Missed A Nigerian Company's Massive FraudGDoingThings YTNo ratings yet

- 10 Auditing SA 2009 The Audit Expectation Gap in Malaysia Lee Ali Gloeck - 1Document5 pages10 Auditing SA 2009 The Audit Expectation Gap in Malaysia Lee Ali Gloeck - 1T.a. TemesgenNo ratings yet

- AuditingDocument11 pagesAuditingkasoziNo ratings yet

- Research Paper On Auditor IndependenceDocument9 pagesResearch Paper On Auditor Independenceorlfgcvkg100% (1)

- AUDITING AS AN INSTRUMENT FOR ENSURING ACCOUNTABILITY ShettyDocument8 pagesAUDITING AS AN INSTRUMENT FOR ENSURING ACCOUNTABILITY ShettyAnandkumar GuptaNo ratings yet

- 183601fb151b9f5741a7fe66505ccc3dDocument35 pages183601fb151b9f5741a7fe66505ccc3dLeonardo BritoNo ratings yet

- Literature Review On Auditors IndependenceDocument5 pagesLiterature Review On Auditors Independencefuhukuheseg2100% (1)

- Introduction, Conceptual Framework of The Study & Research DesignDocument16 pagesIntroduction, Conceptual Framework of The Study & Research DesignSтυριd・ 3尺ㄖ尺No ratings yet

- Professionalism, Ethics, and Independence in Materiality JudgmentDocument83 pagesProfessionalism, Ethics, and Independence in Materiality JudgmentAlfina Fittrinnisak100% (1)

- Case 1 1 Enron CorporationDocument6 pagesCase 1 1 Enron CorporationMichael Gorby WijayaNo ratings yet

- Acc705 Forensic Accounting and Fraud Investigation Case Study Question (40%) DUE 20 May: Weighting 20% of Final ExamDocument6 pagesAcc705 Forensic Accounting and Fraud Investigation Case Study Question (40%) DUE 20 May: Weighting 20% of Final ExamAkeneta RamNo ratings yet

- The Influence of Auditor - S Professional Skepticism and CompetenceDocument18 pagesThe Influence of Auditor - S Professional Skepticism and Competencedashary.lagiaNo ratings yet

- Paper Auditing 1Document9 pagesPaper Auditing 1ZakyaNo ratings yet

- Resume Chapter Eight (Imma)Document9 pagesResume Chapter Eight (Imma)Maia Nahak100% (1)

- Audit Independence Literature ReviewDocument4 pagesAudit Independence Literature Reviewozbvtcvkg100% (1)

- Internal Auditors Are Business PartnerDocument2 pagesInternal Auditors Are Business PartnerValuers NagpurNo ratings yet

- What Are The Objectives of An Audit?: BSCI CertificationDocument3 pagesWhat Are The Objectives of An Audit?: BSCI CertificationnasamamunNo ratings yet

- Audit and Assurance - Past Papers Question With AnswerDocument153 pagesAudit and Assurance - Past Papers Question With AnswerMuhammad SufyanNo ratings yet

- What Type of Auditor You Want To Be .??: The Primary Goals of This Chapter Are As FollowsDocument7 pagesWhat Type of Auditor You Want To Be .??: The Primary Goals of This Chapter Are As FollowsJhonrey BragaisNo ratings yet

- An Assessment of The Role of Auditing Skills On The Business Performance of Small Business Operators in Thesouth-East of NigeriaDocument4 pagesAn Assessment of The Role of Auditing Skills On The Business Performance of Small Business Operators in Thesouth-East of NigeriaIJAR JOURNALNo ratings yet

- Research Paper On Forensic Accounting in IndiaDocument6 pagesResearch Paper On Forensic Accounting in Indialsfxofrif100% (1)

- Advanced Auditing and EDP: QUEENS College School of Post Graduate Studies Department of ACCOUNTING and FinanceDocument53 pagesAdvanced Auditing and EDP: QUEENS College School of Post Graduate Studies Department of ACCOUNTING and FinanceRas Dawit100% (1)

- Case Study 1Document5 pagesCase Study 1May-AnnJoyRedoñaNo ratings yet

- KPMG Corner Wilfredo Z. PaladDocument2 pagesKPMG Corner Wilfredo Z. PaladSheila Mae AramanNo ratings yet

- Jurnal AkuntansiDocument13 pagesJurnal AkuntansiZAHRAH IBNU SALIM -No ratings yet

- Opp Risks Chapter1Document4 pagesOpp Risks Chapter1Marius RusNo ratings yet

- Accountability and Audit QualityDocument11 pagesAccountability and Audit QualityNadz AsrulNo ratings yet

- Corporate GovernanceDocument10 pagesCorporate GovernanceBhuwan GulatiNo ratings yet

- Audit Expectation GapDocument10 pagesAudit Expectation GapFaisal MorshedNo ratings yet

- Assignment June 15Document3 pagesAssignment June 15BlackChemistry GuipetacioNo ratings yet

- A Synthesis Essay of Articles Relating Inherent Ethical ChallengesDocument4 pagesA Synthesis Essay of Articles Relating Inherent Ethical ChallengesFaith EstradaNo ratings yet

- Working As A Financial AnalystDocument2 pagesWorking As A Financial AnalystMuhammad Sameer RanaNo ratings yet

- Enron Case StudyDocument3 pagesEnron Case StudyDavid Wijaya100% (1)

- Audit Expectation Gap DissertationDocument8 pagesAudit Expectation Gap DissertationOrderCustomPapersSingapore100% (1)

- Audit Report and Going Concern Assumption in The Face of Corporate Scandals in Nigeria PDFDocument7 pagesAudit Report and Going Concern Assumption in The Face of Corporate Scandals in Nigeria PDFAlexander DeckerNo ratings yet

- Auditing Thesis TopicsDocument6 pagesAuditing Thesis Topicsshannonjoyarvada100% (2)

- To Fiddle or Not To FiddleDocument7 pagesTo Fiddle or Not To FiddleUmmu Atiqah Zainulabid100% (1)

- Aproject Report On Forensic Accounting and AuditingDocument42 pagesAproject Report On Forensic Accounting and AuditingMolineSit100% (1)

- Audit Expectation Gap ThesisDocument4 pagesAudit Expectation Gap Thesisloribowiesiouxfalls100% (2)

- Why Pursue A Career in AccountingDocument5 pagesWhy Pursue A Career in AccountingEunice Albert Dela CruzNo ratings yet

- 473-469 Alberca, Delgado, OcampoDocument5 pages473-469 Alberca, Delgado, OcampoSofia Mae AlbercaNo ratings yet

- Auditing Information Systems and Controls: The Only Thing Worse Than No Control Is the Illusion of ControlFrom EverandAuditing Information Systems and Controls: The Only Thing Worse Than No Control Is the Illusion of ControlNo ratings yet

- 2023.08.25 Reply ISO MSJ (Stamped) Seth Rich CaseDocument16 pages2023.08.25 Reply ISO MSJ (Stamped) Seth Rich CaseJoe HoNo ratings yet

- International Journal of Arts and Humanities (IJAH) EthiopiaDocument10 pagesInternational Journal of Arts and Humanities (IJAH) EthiopiaJohn Michael Barrosa SaturNo ratings yet

- VFP Wake & Health Care FormDocument5 pagesVFP Wake & Health Care FormBohol FSEO AnnexNo ratings yet

- Petitioner vs. vs. Respondents: Second DivisionDocument7 pagesPetitioner vs. vs. Respondents: Second DivisionJuana Dela VegaNo ratings yet

- Unit4 MCQ Labour LawDocument15 pagesUnit4 MCQ Labour Lawvarunendra pandey83% (6)

- Remedial-Law-Review-1-of-3-Parts With NotesDocument15 pagesRemedial-Law-Review-1-of-3-Parts With NotesRussellNo ratings yet

- ITL Slave Trade - SantosDocument8 pagesITL Slave Trade - SantosLee Silver SantosNo ratings yet

- Historical Perspective of Human RightsDocument23 pagesHistorical Perspective of Human RightsMrudula JoshiNo ratings yet

- Cor Bsu18174Document1 pageCor Bsu18174Jessica DiazNo ratings yet

- Case Digests Spec ProDocument15 pagesCase Digests Spec ProLoven Faith GuerreroNo ratings yet

- World Athletics Competition and Technical Rules 20 231003 182425Document259 pagesWorld Athletics Competition and Technical Rules 20 231003 182425Akash KumarNo ratings yet

- Andersons Business Law and The Legal Environment Comprehensive 23rd Edition Twomey Test BankDocument25 pagesAndersons Business Law and The Legal Environment Comprehensive 23rd Edition Twomey Test BankHannahHarrisMDscfep100% (54)

- CITESDocument2 pagesCITESAvram AvramovNo ratings yet

- Manila LET Room Assignment ElementaryDocument300 pagesManila LET Room Assignment ElementaryPhilNewsXYZNo ratings yet

- AkimboNow AkimboNowMCCHA 0719-1Document11 pagesAkimboNow AkimboNowMCCHA 0719-1lindsaysalirah258No ratings yet

- Chavez Vs Romulo 431 SCRA 534Document4 pagesChavez Vs Romulo 431 SCRA 534TineNo ratings yet

- Technological Institute of The Philippines: 938 Aurora Boulevard, Cubao, Quezon CityDocument10 pagesTechnological Institute of The Philippines: 938 Aurora Boulevard, Cubao, Quezon CityJheo TorresNo ratings yet

- PACIIkrarSehatSora PDFDocument2 pagesPACIIkrarSehatSora PDFAbo 3bodiNo ratings yet

- Sleepy Hollow ScriptDocument108 pagesSleepy Hollow ScriptDanilo FoizerNo ratings yet

- Premier Development Bank v. CADocument11 pagesPremier Development Bank v. CArafael.louise.roca2244No ratings yet

- 08 Rap Jazz Notes-Atico-MDADocument2 pages08 Rap Jazz Notes-Atico-MDAhrdirectorNo ratings yet

- CDI 3 Reviewer AbuDocument10 pagesCDI 3 Reviewer AbuDan Lawrence Dela CruzNo ratings yet

- Alimony and Maintenance Under Parsi LawDocument7 pagesAlimony and Maintenance Under Parsi Lawburhanp2600No ratings yet

- Title 34 - Crime Control and Law EnforcementDocument1,191 pagesTitle 34 - Crime Control and Law EnforcementTrevorNo ratings yet

- Extct Bill 905431x 677697Document2 pagesExtct Bill 905431x 677697clinica.sante.resultsNo ratings yet

Download as pdf or txt

You might also like

- DUNOD DCG 2 Droit Des SociétésDocument497 pagesDUNOD DCG 2 Droit Des Sociétésbaptiste100% (14)

- Audit and Assurance. ICAEWDocument336 pagesAudit and Assurance. ICAEWMd. Shafiqul IslamNo ratings yet

- Case 1.1 Enron CorporationDocument6 pagesCase 1.1 Enron CorporationZizhang Huang88% (8)

- Eo Organizing BhertDocument2 pagesEo Organizing BhertPonciano Alvero96% (26)

- Accounting Fraud at Worldcom Corporate Governance AssignmentDocument4 pagesAccounting Fraud at Worldcom Corporate Governance AssignmentTarun BansalNo ratings yet

- What Are The Pressures That Lead Executives and Managers To Cook The BooksDocument4 pagesWhat Are The Pressures That Lead Executives and Managers To Cook The Booksarnabdas1122100% (1)

- Case 2Document7 pagesCase 2sulthanhakimNo ratings yet

- 10 - Questions Week 3Document6 pages10 - Questions Week 3Camilo ToroNo ratings yet

- Central Provident Fund Board: Ms Fikriah Binte Samani 767 Woodlands Circle #07 - 338 SINGAPORE 730767Document6 pagesCentral Provident Fund Board: Ms Fikriah Binte Samani 767 Woodlands Circle #07 - 338 SINGAPORE 730767Fikriah SamaniNo ratings yet

- Eg2401A Summary NotesDocument23 pagesEg2401A Summary NotesYangFan AwakeNo ratings yet

- A Change in How Auditors WorkDocument5 pagesA Change in How Auditors WorkMingDynasty11No ratings yet

- Running Head: Auditing & Assurance Services 1Document9 pagesRunning Head: Auditing & Assurance Services 1Fizah aliNo ratings yet

- Auditor Independence Challenges Faced by External Auditors When Auditing Large Firms in ZimbabweDocument7 pagesAuditor Independence Challenges Faced by External Auditors When Auditing Large Firms in ZimbabweInternational Journal of Business Marketing and ManagementNo ratings yet

- Top 5 Accounting Firms in The PhilippinesDocument8 pagesTop 5 Accounting Firms in The PhilippinesRoselle Hernandez100% (3)

- KPMG AnalysisDocument2 pagesKPMG AnalysisElaine YapNo ratings yet

- Enron CaseDocument3 pagesEnron CaseLaya Isabelle SulartaNo ratings yet

- Auditing As An Aid To Accountability in The Public SectorDocument47 pagesAuditing As An Aid To Accountability in The Public SectorDaniel Obasi100% (2)

- Case 2aDocument3 pagesCase 2a侯燕颉100% (1)

- The Perpetrator's DepartmentDocument6 pagesThe Perpetrator's DepartmentMohamadHasriNo ratings yet

- Pribanic WhitepaperDocument9 pagesPribanic WhitepaperCaleb PribanicNo ratings yet

- Dissertation Topics in Internal AuditingDocument6 pagesDissertation Topics in Internal AuditingBuyCheapPapersOnlineUK100% (1)

- Auditing Dissertation IdeasDocument4 pagesAuditing Dissertation IdeasWebsiteThatWillWriteAPaperForYouSavannah100% (1)

- The Chartered Accountant Oct 11Document144 pagesThe Chartered Accountant Oct 11Vikky Vasvani100% (1)

- How Auditor Deloitte Missed A Nigerian Company's Massive FraudDocument8 pagesHow Auditor Deloitte Missed A Nigerian Company's Massive FraudGDoingThings YTNo ratings yet

- 10 Auditing SA 2009 The Audit Expectation Gap in Malaysia Lee Ali Gloeck - 1Document5 pages10 Auditing SA 2009 The Audit Expectation Gap in Malaysia Lee Ali Gloeck - 1T.a. TemesgenNo ratings yet

- AuditingDocument11 pagesAuditingkasoziNo ratings yet

- Research Paper On Auditor IndependenceDocument9 pagesResearch Paper On Auditor Independenceorlfgcvkg100% (1)

- AUDITING AS AN INSTRUMENT FOR ENSURING ACCOUNTABILITY ShettyDocument8 pagesAUDITING AS AN INSTRUMENT FOR ENSURING ACCOUNTABILITY ShettyAnandkumar GuptaNo ratings yet

- 183601fb151b9f5741a7fe66505ccc3dDocument35 pages183601fb151b9f5741a7fe66505ccc3dLeonardo BritoNo ratings yet

- Literature Review On Auditors IndependenceDocument5 pagesLiterature Review On Auditors Independencefuhukuheseg2100% (1)

- Introduction, Conceptual Framework of The Study & Research DesignDocument16 pagesIntroduction, Conceptual Framework of The Study & Research DesignSтυριd・ 3尺ㄖ尺No ratings yet

- Professionalism, Ethics, and Independence in Materiality JudgmentDocument83 pagesProfessionalism, Ethics, and Independence in Materiality JudgmentAlfina Fittrinnisak100% (1)

- Case 1 1 Enron CorporationDocument6 pagesCase 1 1 Enron CorporationMichael Gorby WijayaNo ratings yet

- Acc705 Forensic Accounting and Fraud Investigation Case Study Question (40%) DUE 20 May: Weighting 20% of Final ExamDocument6 pagesAcc705 Forensic Accounting and Fraud Investigation Case Study Question (40%) DUE 20 May: Weighting 20% of Final ExamAkeneta RamNo ratings yet

- The Influence of Auditor - S Professional Skepticism and CompetenceDocument18 pagesThe Influence of Auditor - S Professional Skepticism and Competencedashary.lagiaNo ratings yet

- Paper Auditing 1Document9 pagesPaper Auditing 1ZakyaNo ratings yet

- Resume Chapter Eight (Imma)Document9 pagesResume Chapter Eight (Imma)Maia Nahak100% (1)

- Audit Independence Literature ReviewDocument4 pagesAudit Independence Literature Reviewozbvtcvkg100% (1)

- Internal Auditors Are Business PartnerDocument2 pagesInternal Auditors Are Business PartnerValuers NagpurNo ratings yet

- What Are The Objectives of An Audit?: BSCI CertificationDocument3 pagesWhat Are The Objectives of An Audit?: BSCI CertificationnasamamunNo ratings yet

- Audit and Assurance - Past Papers Question With AnswerDocument153 pagesAudit and Assurance - Past Papers Question With AnswerMuhammad SufyanNo ratings yet

- What Type of Auditor You Want To Be .??: The Primary Goals of This Chapter Are As FollowsDocument7 pagesWhat Type of Auditor You Want To Be .??: The Primary Goals of This Chapter Are As FollowsJhonrey BragaisNo ratings yet

- An Assessment of The Role of Auditing Skills On The Business Performance of Small Business Operators in Thesouth-East of NigeriaDocument4 pagesAn Assessment of The Role of Auditing Skills On The Business Performance of Small Business Operators in Thesouth-East of NigeriaIJAR JOURNALNo ratings yet

- Research Paper On Forensic Accounting in IndiaDocument6 pagesResearch Paper On Forensic Accounting in Indialsfxofrif100% (1)

- Advanced Auditing and EDP: QUEENS College School of Post Graduate Studies Department of ACCOUNTING and FinanceDocument53 pagesAdvanced Auditing and EDP: QUEENS College School of Post Graduate Studies Department of ACCOUNTING and FinanceRas Dawit100% (1)

- Case Study 1Document5 pagesCase Study 1May-AnnJoyRedoñaNo ratings yet

- KPMG Corner Wilfredo Z. PaladDocument2 pagesKPMG Corner Wilfredo Z. PaladSheila Mae AramanNo ratings yet

- Jurnal AkuntansiDocument13 pagesJurnal AkuntansiZAHRAH IBNU SALIM -No ratings yet

- Opp Risks Chapter1Document4 pagesOpp Risks Chapter1Marius RusNo ratings yet

- Accountability and Audit QualityDocument11 pagesAccountability and Audit QualityNadz AsrulNo ratings yet

- Corporate GovernanceDocument10 pagesCorporate GovernanceBhuwan GulatiNo ratings yet

- Audit Expectation GapDocument10 pagesAudit Expectation GapFaisal MorshedNo ratings yet

- Assignment June 15Document3 pagesAssignment June 15BlackChemistry GuipetacioNo ratings yet

- A Synthesis Essay of Articles Relating Inherent Ethical ChallengesDocument4 pagesA Synthesis Essay of Articles Relating Inherent Ethical ChallengesFaith EstradaNo ratings yet

- Working As A Financial AnalystDocument2 pagesWorking As A Financial AnalystMuhammad Sameer RanaNo ratings yet

- Enron Case StudyDocument3 pagesEnron Case StudyDavid Wijaya100% (1)

- Audit Expectation Gap DissertationDocument8 pagesAudit Expectation Gap DissertationOrderCustomPapersSingapore100% (1)

- Audit Report and Going Concern Assumption in The Face of Corporate Scandals in Nigeria PDFDocument7 pagesAudit Report and Going Concern Assumption in The Face of Corporate Scandals in Nigeria PDFAlexander DeckerNo ratings yet

- Auditing Thesis TopicsDocument6 pagesAuditing Thesis Topicsshannonjoyarvada100% (2)

- To Fiddle or Not To FiddleDocument7 pagesTo Fiddle or Not To FiddleUmmu Atiqah Zainulabid100% (1)

- Aproject Report On Forensic Accounting and AuditingDocument42 pagesAproject Report On Forensic Accounting and AuditingMolineSit100% (1)

- Audit Expectation Gap ThesisDocument4 pagesAudit Expectation Gap Thesisloribowiesiouxfalls100% (2)

- Why Pursue A Career in AccountingDocument5 pagesWhy Pursue A Career in AccountingEunice Albert Dela CruzNo ratings yet

- 473-469 Alberca, Delgado, OcampoDocument5 pages473-469 Alberca, Delgado, OcampoSofia Mae AlbercaNo ratings yet

- Auditing Information Systems and Controls: The Only Thing Worse Than No Control Is the Illusion of ControlFrom EverandAuditing Information Systems and Controls: The Only Thing Worse Than No Control Is the Illusion of ControlNo ratings yet

- 2023.08.25 Reply ISO MSJ (Stamped) Seth Rich CaseDocument16 pages2023.08.25 Reply ISO MSJ (Stamped) Seth Rich CaseJoe HoNo ratings yet

- International Journal of Arts and Humanities (IJAH) EthiopiaDocument10 pagesInternational Journal of Arts and Humanities (IJAH) EthiopiaJohn Michael Barrosa SaturNo ratings yet

- VFP Wake & Health Care FormDocument5 pagesVFP Wake & Health Care FormBohol FSEO AnnexNo ratings yet

- Petitioner vs. vs. Respondents: Second DivisionDocument7 pagesPetitioner vs. vs. Respondents: Second DivisionJuana Dela VegaNo ratings yet

- Unit4 MCQ Labour LawDocument15 pagesUnit4 MCQ Labour Lawvarunendra pandey83% (6)

- Remedial-Law-Review-1-of-3-Parts With NotesDocument15 pagesRemedial-Law-Review-1-of-3-Parts With NotesRussellNo ratings yet

- ITL Slave Trade - SantosDocument8 pagesITL Slave Trade - SantosLee Silver SantosNo ratings yet

- Historical Perspective of Human RightsDocument23 pagesHistorical Perspective of Human RightsMrudula JoshiNo ratings yet

- Cor Bsu18174Document1 pageCor Bsu18174Jessica DiazNo ratings yet

- Case Digests Spec ProDocument15 pagesCase Digests Spec ProLoven Faith GuerreroNo ratings yet

- World Athletics Competition and Technical Rules 20 231003 182425Document259 pagesWorld Athletics Competition and Technical Rules 20 231003 182425Akash KumarNo ratings yet

- Andersons Business Law and The Legal Environment Comprehensive 23rd Edition Twomey Test BankDocument25 pagesAndersons Business Law and The Legal Environment Comprehensive 23rd Edition Twomey Test BankHannahHarrisMDscfep100% (54)

- CITESDocument2 pagesCITESAvram AvramovNo ratings yet

- Manila LET Room Assignment ElementaryDocument300 pagesManila LET Room Assignment ElementaryPhilNewsXYZNo ratings yet

- AkimboNow AkimboNowMCCHA 0719-1Document11 pagesAkimboNow AkimboNowMCCHA 0719-1lindsaysalirah258No ratings yet

- Chavez Vs Romulo 431 SCRA 534Document4 pagesChavez Vs Romulo 431 SCRA 534TineNo ratings yet

- Technological Institute of The Philippines: 938 Aurora Boulevard, Cubao, Quezon CityDocument10 pagesTechnological Institute of The Philippines: 938 Aurora Boulevard, Cubao, Quezon CityJheo TorresNo ratings yet

- PACIIkrarSehatSora PDFDocument2 pagesPACIIkrarSehatSora PDFAbo 3bodiNo ratings yet

- Sleepy Hollow ScriptDocument108 pagesSleepy Hollow ScriptDanilo FoizerNo ratings yet

- Premier Development Bank v. CADocument11 pagesPremier Development Bank v. CArafael.louise.roca2244No ratings yet

- 08 Rap Jazz Notes-Atico-MDADocument2 pages08 Rap Jazz Notes-Atico-MDAhrdirectorNo ratings yet

- CDI 3 Reviewer AbuDocument10 pagesCDI 3 Reviewer AbuDan Lawrence Dela CruzNo ratings yet

- Alimony and Maintenance Under Parsi LawDocument7 pagesAlimony and Maintenance Under Parsi Lawburhanp2600No ratings yet

- Title 34 - Crime Control and Law EnforcementDocument1,191 pagesTitle 34 - Crime Control and Law EnforcementTrevorNo ratings yet

- Extct Bill 905431x 677697Document2 pagesExtct Bill 905431x 677697clinica.sante.resultsNo ratings yet