Download as pdf or txt

You might also like

- Solutions Manual To Accompany Principles of Corporate Finance 10th Edition 9780073530734Document9 pagesSolutions Manual To Accompany Principles of Corporate Finance 10th Edition 9780073530734BriannaJimenezojmrs99% (83)

- The Billionaire's Apprentice,' by Anita RaghavanDocument7 pagesThe Billionaire's Apprentice,' by Anita Raghavananirudh71100% (2)

- ECMC49F Midterm Solution 2Document13 pagesECMC49F Midterm Solution 2Wissal RiyaniNo ratings yet

- 3 Part1Document23 pages3 Part1arp140102No ratings yet

- Cbse-xii Sqp Economics PDF 2023-24-7Document34 pagesCbse-xii Sqp Economics PDF 2023-24-7pinkyseamnaNo ratings yet

- FIN3009 Financial Management: Topic 5: Bonds and Bond ValuationDocument72 pagesFIN3009 Financial Management: Topic 5: Bonds and Bond Valuationkc103038No ratings yet

- 3 Part2Document19 pages3 Part2arp140102No ratings yet

- Module 9 - Managing Interest Risk Part 2: 9.2 DurationDocument5 pagesModule 9 - Managing Interest Risk Part 2: 9.2 DurationAnna-Clara MansolahtiNo ratings yet

- 2022 Finance Paper & Solution 2022Document21 pages2022 Finance Paper & Solution 2022Brijesh MishraNo ratings yet

- HW 2 ADocument6 pagesHW 2 AhatemNo ratings yet

- Blackwell Publishing American Finance AssociationDocument8 pagesBlackwell Publishing American Finance AssociationhectorNo ratings yet

- Bonds: Dong Lou London School of Economics LSE Summer SchoolDocument45 pagesBonds: Dong Lou London School of Economics LSE Summer SchoolAryan PandeyNo ratings yet

- Iapm 10Document32 pagesIapm 10Rachit BhagatNo ratings yet

- Gap Dur AnalysesDocument8 pagesGap Dur AnalysesmanishapecNo ratings yet

- BMA4106 Investment and Asset Management Lecture 1Document17 pagesBMA4106 Investment and Asset Management Lecture 1Dickson OgendiNo ratings yet

- Chapter 7 (FFM/BH) : Bonds and Their ValuationDocument43 pagesChapter 7 (FFM/BH) : Bonds and Their Valuationsachin_choudhary_5No ratings yet

- FINS3630: UNSW Business SchoolDocument27 pagesFINS3630: UNSW Business SchoolcarolinetsangNo ratings yet

- Interest Rate Derivatives: An Introduction To The Pricing of Caps and FloorsDocument12 pagesInterest Rate Derivatives: An Introduction To The Pricing of Caps and FloorsImranullah KhanNo ratings yet

- Interest Rate Derivatives: An Introduction To The Pricing of Caps and FloorsDocument12 pagesInterest Rate Derivatives: An Introduction To The Pricing of Caps and FloorsnipunNo ratings yet

- CHPT 9Document20 pagesCHPT 9ferahNo ratings yet

- Session 3 Convexity ImmunizationDocument20 pagesSession 3 Convexity ImmunizationRabeya AktarNo ratings yet

- Valuationof Bondsand SharesDocument20 pagesValuationof Bondsand Sharesagarwalsurbhi07No ratings yet

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument50 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing Riskanon_447537688No ratings yet

- Loan On CDSDocument14 pagesLoan On CDSmumsy20No ratings yet

- FINS2624 WEEK 2: y Bond PricesDocument5 pagesFINS2624 WEEK 2: y Bond PricesWahaaj RanaNo ratings yet

- 435x Lecture 3 Duration-Based Strategies VfinalDocument42 pages435x Lecture 3 Duration-Based Strategies Vfinalarjunbusiness7012No ratings yet

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument43 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskMUHAMMAD JAMILNo ratings yet

- AF CHP 9Document27 pagesAF CHP 9Jeffry AshariNo ratings yet

- Lecture 6: Valuation of Bonds and SharesDocument12 pagesLecture 6: Valuation of Bonds and SharesHabibullah SarkerNo ratings yet

- APS 502 Term Structure SlidesDocument31 pagesAPS 502 Term Structure SlidesHANG ZHANGNo ratings yet

- What Is A Bond (Debenture) ?Document19 pagesWhat Is A Bond (Debenture) ?17roseNo ratings yet

- 03 PS4 FF - SolDocument4 pages03 PS4 FF - SolhatemNo ratings yet

- Bond Valuation & DurationDocument39 pagesBond Valuation & DurationhassanduraniNo ratings yet

- Ch07 BondsDocument44 pagesCh07 BondsRaazia GulNo ratings yet

- What Is Capital Budgeting?Document12 pagesWhat Is Capital Budgeting?Kumaresan RsNo ratings yet

- 20240325 125.364 Week 05Document41 pages20240325 125.364 Week 05jiejialing08No ratings yet

- Stock ValuationDocument85 pagesStock ValuationArun kumar0% (2)

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring YieldDocument34 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring YieldSyed Farzan AzharNo ratings yet

- Chap 007Document67 pagesChap 007ngminhanh216No ratings yet

- CHAPTER 7 Bonds and Their ValuationDocument43 pagesCHAPTER 7 Bonds and Their ValuationAhsan100% (2)

- FM11 CH 10 Mini-Case Old13 Basics of Cap BudgDocument20 pagesFM11 CH 10 Mini-Case Old13 Basics of Cap BudgMZK videos100% (1)

- Interest Rates and Bond Valuation: Mcgraw-Hill/IrwinDocument60 pagesInterest Rates and Bond Valuation: Mcgraw-Hill/IrwinVip ProNo ratings yet

- Chapter 11 PowerPointsDocument48 pagesChapter 11 PowerPointsErik AlvarezNo ratings yet

- 2021 Sept 23 Lec Ch2 Part 4Document27 pages2021 Sept 23 Lec Ch2 Part 4dsfghNo ratings yet

- Session 3 Bond and Interes RateDocument26 pagesSession 3 Bond and Interes RateadamobirkNo ratings yet

- Chap 9 Interest Rate Risk IIDocument123 pagesChap 9 Interest Rate Risk IIAfnan100% (3)

- Capital Budgeting TechniquesDocument21 pagesCapital Budgeting TechniquesMishelNo ratings yet

- CBCSS March 2018 Sixth Sem Accounting For Managerial Decisions QUESTION PAPER Goodwill Tuition Centre 9846710963 9567902805Document4 pagesCBCSS March 2018 Sixth Sem Accounting For Managerial Decisions QUESTION PAPER Goodwill Tuition Centre 9846710963 9567902805Rainy Goodwill75% (4)

- Savings, AmortizationDocument11 pagesSavings, Amortizationtd66jm2gnjNo ratings yet

- Creditrisk 2Document22 pagesCreditrisk 2Sherstobitov SergeiNo ratings yet

- CH 04Document12 pagesCH 04Mai NguyễnNo ratings yet

- Week 2 LectureDocument93 pagesWeek 2 LectureДмитрий КолесниковNo ratings yet

- Chuong 5TVDocument18 pagesChuong 5TVMỹ TâmNo ratings yet

- ch2 SLD DBDDocument23 pagesch2 SLD DBDkamosasakaNo ratings yet

- Chap 009Document123 pagesChap 009ngminhanh216No ratings yet

- Deterministic Cash-Flows: 1 Basic Theory of InterestDocument16 pagesDeterministic Cash-Flows: 1 Basic Theory of InterestNaveen ReddyNo ratings yet

- CH 09 Bonds & ValuationDocument35 pagesCH 09 Bonds & ValuationtyoshinoNo ratings yet

- CH 10Document31 pagesCH 10karlistonsitompulNo ratings yet

- 350i2 Bond Home Work Help DDocument13 pages350i2 Bond Home Work Help Dkarthik sNo ratings yet

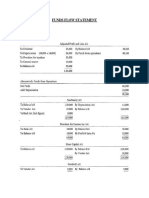

- Funds Flow Statement: Numerical 1Document4 pagesFunds Flow Statement: Numerical 1Neelu AhluwaliaNo ratings yet

- Types of Dividend PolicyDocument7 pagesTypes of Dividend PolicyRakibul Islam JonyNo ratings yet

- 4.aug Ijmte - 830Document16 pages4.aug Ijmte - 830BasappaSarkarNo ratings yet

- The Gox InitiativeDocument53 pagesThe Gox InitiativeDaniel Kelman100% (1)

- #2 - What Do You Think This Company Does Right? What Do You Think We Do Wrong?Document8 pages#2 - What Do You Think This Company Does Right? What Do You Think We Do Wrong?helloNo ratings yet

- Adhoc Exemption Order NoDocument4 pagesAdhoc Exemption Order NoSourav Banerjee100% (1)

- TD Ameritrade Free Etf List PDFDocument6 pagesTD Ameritrade Free Etf List PDFjjy1234No ratings yet

- Dell Working Capital Management Write UpDocument1 pageDell Working Capital Management Write UpSalil AggarwalNo ratings yet

- Residual Income ValuationDocument39 pagesResidual Income ValuationImashi100% (1)

- Abf303 BQ2Document4 pagesAbf303 BQ2Jay PatelNo ratings yet

- Chapter 4-6 Advanced Accounting 5009: Roger Mayer 7:00 PM & 8:30 PMDocument43 pagesChapter 4-6 Advanced Accounting 5009: Roger Mayer 7:00 PM & 8:30 PMalejandra_giraldo_3No ratings yet

- Prospectus Amazon Store Selling Survival and Sports Gear PDFDocument11 pagesProspectus Amazon Store Selling Survival and Sports Gear PDFAliciaNo ratings yet

- CreditDocument8 pagesCreditmiranaismNo ratings yet

- Commodity Derivative Market in IndiaDocument16 pagesCommodity Derivative Market in IndiaNaveen K. JindalNo ratings yet

- LECTURE-03c Source of CapitalsDocument55 pagesLECTURE-03c Source of CapitalsNurhayati Faiszah IsmailNo ratings yet

- Bolsa de MadridDocument17 pagesBolsa de MadridMihaelaNo ratings yet

- Statement of Cash Flows: Optional Assignment Characteristics TableDocument11 pagesStatement of Cash Flows: Optional Assignment Characteristics Table'Steffan Tanzil'No ratings yet

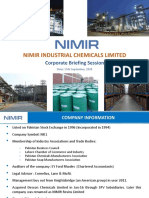

- Nimir Industrial Chemicals Limited: Corporate Briefing SessionDocument14 pagesNimir Industrial Chemicals Limited: Corporate Briefing SessionIlyas FaizNo ratings yet

- BrokerDocument40 pagesBrokerMotiram paudelNo ratings yet

- 2018 John Deere Proxy StatementDocument104 pages2018 John Deere Proxy StatementMichelle O'NeillNo ratings yet

- DeriDocument8 pagesDerisyedsubzposhNo ratings yet

- 2016 ORION Consolidated Audit ReportDocument112 pages2016 ORION Consolidated Audit ReportJoachim VIALLONNo ratings yet

- Calculator Workshop - TI BA IIDocument57 pagesCalculator Workshop - TI BA IIkabirakhan2007No ratings yet

- Initial Information Report (IIR) : Summer Internship ProgramDocument2 pagesInitial Information Report (IIR) : Summer Internship ProgramSupriya TholeteNo ratings yet

- Credit Transactions (Pledge)Document5 pagesCredit Transactions (Pledge)Aishan SuarezNo ratings yet

- JPM - Cap and FloorDocument7 pagesJPM - Cap and FloorRR BakshNo ratings yet

- TaxationDocument10 pagesTaxationhotjuristNo ratings yet

- Aptitude Test 4Document12 pagesAptitude Test 4ankit0076No ratings yet

- FS XcolcsgDocument1 pageFS Xcolcsggreengrin3No ratings yet