Download as pdf or txt

You might also like

- Notes For ISTQB Foundation Level CertificationDocument12 pagesNotes For ISTQB Foundation Level CertificationtowidNo ratings yet

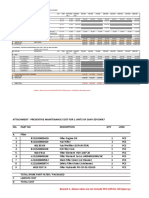

- Quotation Preventive Maintenace Service PT - QuatcontenaDocument4 pagesQuotation Preventive Maintenace Service PT - QuatcontenaDedy patreszNo ratings yet

- 9 Job Costing & Batch Costing PDFDocument7 pages9 Job Costing & Batch Costing PDFgracel angela tolejano100% (1)

- The Cost of Production: Questions For ReviewDocument14 pagesThe Cost of Production: Questions For ReviewVinaNo ratings yet

- Short Run Production FunctionDocument6 pagesShort Run Production FunctionHema Harshitha100% (2)

- Tata Motors ProjectDocument22 pagesTata Motors Projectm19382367% (3)

- ICAP Study Text Chap-4 (Solutions)Document3 pagesICAP Study Text Chap-4 (Solutions)songs 2019 MalikNo ratings yet

- ICAP Study Text Chap-4 (Questions)Document3 pagesICAP Study Text Chap-4 (Questions)songs 2019 MalikNo ratings yet

- 6 Illumination CalculationDocument42 pages6 Illumination CalculationSamant SauravNo ratings yet

- Macchiato Limited - Q-1 Aut-19 - SOLUTIONDocument2 pagesMacchiato Limited - Q-1 Aut-19 - SOLUTIONmichealcorleone1923No ratings yet

- Suggested Answers Certificate in Accounting and Finance - Autumn 2017Document7 pagesSuggested Answers Certificate in Accounting and Finance - Autumn 2017ShehrozSTNo ratings yet

- Advance Management Accounting Test - 3 Suggested Answers / HintsDocument18 pagesAdvance Management Accounting Test - 3 Suggested Answers / HintsSumit AnandNo ratings yet

- SCM Cia 1Document7 pagesSCM Cia 1NANDINI RATHI 1923255No ratings yet

- Production StrategyDocument14 pagesProduction StrategyJD_04100% (3)

- Tutorial - Unit 8 SolutionDocument3 pagesTutorial - Unit 8 Solutionokuhle4002No ratings yet

- Master Question (Mixed With Process Costing) - Q ADocument3 pagesMaster Question (Mixed With Process Costing) - Q AMuaaz NayyarNo ratings yet

- Year 0 1 2 3 4 - Rs. in MillionDocument6 pagesYear 0 1 2 3 4 - Rs. in MillionShehrozSTNo ratings yet

- Standard Costing I SolutionDocument7 pagesStandard Costing I SolutionDheeraj DoliyaNo ratings yet

- Putrajaya OT 30%Document7 pagesPutrajaya OT 30%lokman hakimNo ratings yet

- Service Bulletin: Issued by Canon Europa N.VDocument2 pagesService Bulletin: Issued by Canon Europa N.VokeinfoNo ratings yet

- Perbaikan Zinus Single SheeDocument1 pagePerbaikan Zinus Single Sheedhandy mraNo ratings yet

- Test 8 Sol-1Document2 pagesTest 8 Sol-1Gamerz Den Pes 17No ratings yet

- Tesr 10 Standard Costing and Variance AnalysisDocument1 pageTesr 10 Standard Costing and Variance AnalysisAnmoul ZahraNo ratings yet

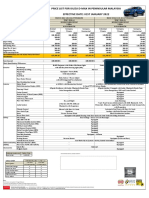

- Harga Toyota YarisDocument1 pageHarga Toyota YarisSTANLEY BIN SULIM MoeNo ratings yet

- Project Plan For VarnishDocument2 pagesProject Plan For Varnishsekhar_jvjNo ratings yet

- Responsibility Accounting and Transfer PricingDocument34 pagesResponsibility Accounting and Transfer PricingJhanna Hall TorrNo ratings yet

- 1.0 PM (IP) Yaris Price List 2024Document2 pages1.0 PM (IP) Yaris Price List 2024as.digibyteNo ratings yet

- Overheads Part 1 SolutionsDocument25 pagesOverheads Part 1 Solutionsdoshiviraj77No ratings yet

- WT - 2016 PDFDocument8 pagesWT - 2016 PDFAbdulAzeemNo ratings yet

- 71694bos57679 Inter P3aDocument12 pages71694bos57679 Inter P3aTECH TeluguNo ratings yet

- Caf 3 Cma Spring 2024Document6 pagesCaf 3 Cma Spring 2024rumelrashid_seuNo ratings yet

- Suggested Answers Final Examination - Winter 2015: Management AccounitngDocument7 pagesSuggested Answers Final Examination - Winter 2015: Management AccounitngAbdulAzeemNo ratings yet

- Case ZDocument12 pagesCase ZKshitiz JaiswalNo ratings yet

- Mac S-15 (Solution) (Final)Document10 pagesMac S-15 (Solution) (Final)Ramzan AliNo ratings yet

- Al Ain Distribution Company (Aadc) : JM 0209 SubstationDocument2 pagesAl Ain Distribution Company (Aadc) : JM 0209 SubstationRyo DavisNo ratings yet

- XY Limited - Q-4 Spr-14 - SOLUTIONDocument2 pagesXY Limited - Q-4 Spr-14 - SOLUTIONMuaaz NayyarNo ratings yet

- 26 Os TPJDocument8 pages26 Os TPJIlangovan SubbannaudayarNo ratings yet

- Intoroduction of Sumitomo (121213)Document38 pagesIntoroduction of Sumitomo (121213)Myo Zaw NyuntNo ratings yet

- 3.0 SBH Toyota Yaris MC 20 Price List (IP) ST ExemptionDocument1 page3.0 SBH Toyota Yaris MC 20 Price List (IP) ST ExemptionProAutoNo ratings yet

- Unit Housing Tipe 70Document14 pagesUnit Housing Tipe 70drm4p5ddtnNo ratings yet

- 1.0 PM Toyota Camry Price ListDocument1 page1.0 PM Toyota Camry Price Listdarren.ryan1988No ratings yet

- Kereta 2023 MantapDocument1 pageKereta 2023 MantapSk ChenderiangNo ratings yet

- UMW Toyota Motor SDN BHD (60576-K) Price List For Sabah Effective From 15 December 2020Document1 pageUMW Toyota Motor SDN BHD (60576-K) Price List For Sabah Effective From 15 December 2020ProAutoNo ratings yet

- Assignment Mutiara LimitedDocument5 pagesAssignment Mutiara LimitedjagindasNo ratings yet

- Activity Normal Duration (Days) Normal Cost (RS.) Crash Duration (Days) Crash Cost (RS.)Document7 pagesActivity Normal Duration (Days) Normal Cost (RS.) Crash Duration (Days) Crash Cost (RS.)Nisen ShresthaNo ratings yet

- Surat PPG Paint - PT Badak NGL - Breakdown Material PDFDocument8 pagesSurat PPG Paint - PT Badak NGL - Breakdown Material PDFSujangkung SolikinNo ratings yet

- Standard Costing & Variance AnalysisDocument18 pagesStandard Costing & Variance AnalysisMahesh G VNo ratings yet

- Meguiars Price List PackageDocument3 pagesMeguiars Price List Packagejohnjeric5No ratings yet

- S. No Cable Tag No From To Power Cable Description Item Item Motor Rating KW No. of Runs No. of CoreDocument35 pagesS. No Cable Tag No From To Power Cable Description Item Item Motor Rating KW No. of Runs No. of CorejjspenceNo ratings yet

- Part-A - Strategic Management Accounting: Multiple Choice Questions (MCQS)Document33 pagesPart-A - Strategic Management Accounting: Multiple Choice Questions (MCQS)ARIF HUSSAIN AN ENGLISH LECTURER FOR ALL CLASSESNo ratings yet

- Almoayyed Air Conditioning WLLDocument3 pagesAlmoayyed Air Conditioning WLLSherwin CruzNo ratings yet

- YannDocument1 pageYannnimpamerveille9No ratings yet

- Industrial and Standard Air CurtainDocument2 pagesIndustrial and Standard Air Curtainxen065No ratings yet

- 04 Overheads DistributionDocument15 pages04 Overheads DistributionDevesh BahetyNo ratings yet

- Merton Truck CompanyDocument12 pagesMerton Truck CompanyAbiNo ratings yet

- Cost Accounting 2003Document12 pagesCost Accounting 2003Ok HqNo ratings yet

- Chapter 8 Cost Analysis..rDocument5 pagesChapter 8 Cost Analysis..rAmirul SakibNo ratings yet

- RG01 Price List 1.9at P 1.9at L RS PM PDFDocument1 pageRG01 Price List 1.9at P 1.9at L RS PM PDFShahmi AzmiNo ratings yet

- SOLUTION MANAC Quiz IV 2019Document1 pageSOLUTION MANAC Quiz IV 2019utsav anandNo ratings yet

- Price List For Peninsular Malaysia Effective From 10: UMW Toyota Motor SDN BHD (60576-K) January 2019Document1 pagePrice List For Peninsular Malaysia Effective From 10: UMW Toyota Motor SDN BHD (60576-K) January 2019نور العصمةNo ratings yet

- 515 AMA Must DO QuestionsDocument217 pages515 AMA Must DO QuestionsVenkataRajuNo ratings yet

- Al Ain Distribution Company (Aadc) : JM 0223 SubstationDocument2 pagesAl Ain Distribution Company (Aadc) : JM 0223 SubstationRyo DavisNo ratings yet

- Cim SyllabusDocument2 pagesCim SyllabusHarish HNo ratings yet

- Inventory Management PDFDocument49 pagesInventory Management PDFVyVyNo ratings yet

- Total Quality Management: SynonymsDocument7 pagesTotal Quality Management: SynonymssabinNo ratings yet

- Powertrain Global Quality RequirementsDocument6 pagesPowertrain Global Quality RequirementsCarlos CarranzaNo ratings yet

- Cost Accounting FinalsDocument4 pagesCost Accounting FinalsJerico Mamaradlo100% (1)

- SAP CO PC Product Costing Q & ADocument14 pagesSAP CO PC Product Costing Q & AJit GhoshNo ratings yet

- PRODUCTIONDocument35 pagesPRODUCTIONSHAWN-PATRICK BERRYNo ratings yet

- Information Technology in A Supply ChainDocument19 pagesInformation Technology in A Supply ChainQadeer KhanNo ratings yet

- Manual de Partes AMMANN Asc100Document4 pagesManual de Partes AMMANN Asc100Jesus Reyes HéroesNo ratings yet

- T-ENG CardDocument14 pagesT-ENG CardViswaChaitanya NandigamNo ratings yet

- Operation Analysis Sheet: Determine and Describe Details of Analysis ActionDocument11 pagesOperation Analysis Sheet: Determine and Describe Details of Analysis Actiontcalhoun1285100% (3)

- Production and Cost AnalysisDocument27 pagesProduction and Cost AnalysisHades RiegoNo ratings yet

- Managerial Accounting: Prepared by Diane Tanner University of North FloridaDocument10 pagesManagerial Accounting: Prepared by Diane Tanner University of North Floridaharshnvicky123No ratings yet

- Chapter 3 - The Fundamental Economic Problem - Scarcity and ChoiceDocument20 pagesChapter 3 - The Fundamental Economic Problem - Scarcity and ChoiceMuhammad FurqanNo ratings yet

- Urban Economics, 9th Edition-73-93Document21 pagesUrban Economics, 9th Edition-73-93sck58866jcNo ratings yet

- Full Chapter Automation Production Systems and Computer Integrated Manufacturing 5E Mikell P Groover PDFDocument53 pagesFull Chapter Automation Production Systems and Computer Integrated Manufacturing 5E Mikell P Groover PDFyulanda.jones166100% (6)

- Tugas Akmen Fadhliya Fauziah CH 8Document18 pagesTugas Akmen Fadhliya Fauziah CH 8FadhliyaFNo ratings yet

- What Is The Highly Optimized Manufacturing ProcessDocument3 pagesWhat Is The Highly Optimized Manufacturing ProcessSharmashDNo ratings yet

- Controlling Material FlowDocument2 pagesControlling Material FlowCharice Anne VillamarinNo ratings yet

- Chap 5 - MRPDocument75 pagesChap 5 - MRPladdooparmarNo ratings yet

- CHAPTER 6 Online QuizDocument12 pagesCHAPTER 6 Online Quizေဟ မိုးဆက္No ratings yet

- MB 044Document380 pagesMB 044Jimmy JhambNo ratings yet

- Entrepreneurship: 4M's of OperationDocument19 pagesEntrepreneurship: 4M's of OperationjmNo ratings yet

- CMCsand GMPsDocument20 pagesCMCsand GMPshamoum100% (1)

- Image Pricelist Aster Chairs PDFDocument5 pagesImage Pricelist Aster Chairs PDFvamseevkNo ratings yet

- Motorola Six Sigma Conversion TableDocument1 pageMotorola Six Sigma Conversion TableMars HNo ratings yet