Download as pdf or txt

You might also like

- FIME Korea Bank DetailsDocument1 pageFIME Korea Bank DetailsGgghhhNo ratings yet

- Risk Management: Case Study On AIGDocument8 pagesRisk Management: Case Study On AIGPatrick ChauNo ratings yet

- Goldberg PaperDocument8 pagesGoldberg PaperTony SsenfumaNo ratings yet

- Impact of Microcredit in Rural Areas of Morocco: Evidence From A Randomized EvaluationDocument33 pagesImpact of Microcredit in Rural Areas of Morocco: Evidence From A Randomized EvaluationSedekholie ChadiNo ratings yet

- The Simplified Vision of Microcredit As The Solution To Poverty and Women's EmpowermentDocument4 pagesThe Simplified Vision of Microcredit As The Solution To Poverty and Women's EmpowermentJarlotaNo ratings yet

- Journal - Impact of Microcredit Inrural Areas of Morocco. Evidence From A Randomized EvaluationDocument31 pagesJournal - Impact of Microcredit Inrural Areas of Morocco. Evidence From A Randomized EvaluationAgustina EkaNo ratings yet

- Draft: Alok Misra, PHD Candidate in Development Studies, Victoria University of Wellington, New ZealandDocument20 pagesDraft: Alok Misra, PHD Candidate in Development Studies, Victoria University of Wellington, New ZealandVipul AgarwalNo ratings yet

- Credit Bureuas Peru, Guatemala BoliviaDocument129 pagesCredit Bureuas Peru, Guatemala BoliviaPepe BertocchiNo ratings yet

- Literature Review On MicrofinanceDocument8 pagesLiterature Review On Microfinancenivi_nandu362833% (3)

- Macroeconomics: The Goals of Macroeconomic PolicyDocument13 pagesMacroeconomics: The Goals of Macroeconomic Policyduarif14No ratings yet

- Chapter 8Document15 pagesChapter 8himanshNo ratings yet

- The Definition of MicrofinanceDocument6 pagesThe Definition of MicrofinanceAyush BhavsarNo ratings yet

- A Literature Review of The Impact of Microfinance: by January 18, 2010Document4 pagesA Literature Review of The Impact of Microfinance: by January 18, 2010amma_jayapradha6902No ratings yet

- Effects of Microfinance On Poverty Alleviation.v1Document12 pagesEffects of Microfinance On Poverty Alleviation.v1kyaka herman ceaserNo ratings yet

- Block 89Document60 pagesBlock 89SaurabhNo ratings yet

- Tesema Seminar 2Document29 pagesTesema Seminar 2AssefaTayachewNo ratings yet

- Effect of Micro-Finance On PovertyDocument18 pagesEffect of Micro-Finance On PovertyKarim KhaledNo ratings yet

- ABV Indian Institute of Information Technology and Management, Gwalior - 474 010, IndiaDocument32 pagesABV Indian Institute of Information Technology and Management, Gwalior - 474 010, Indiakushagrabhatnagar10No ratings yet

- IJRFM Volume 1, Issue 5 (September, 2011) (ISSN 2231-5985)Document19 pagesIJRFM Volume 1, Issue 5 (September, 2011) (ISSN 2231-5985)Charu ModiNo ratings yet

- An Appraisal of The Performance of Micro Finance Bank in Economic Development of Delta StateDocument29 pagesAn Appraisal of The Performance of Micro Finance Bank in Economic Development of Delta Statealbertosehi1No ratings yet

- Effect of Microfinance On Poverty Reduction A Critical Scrutiny of Theoretical LiteratureDocument18 pagesEffect of Microfinance On Poverty Reduction A Critical Scrutiny of Theoretical LiteratureLealem tayeworkNo ratings yet

- Print NiDocument35 pagesPrint Nimahinayjake09No ratings yet

- Research Method End of Year Exam ProjectDocument12 pagesResearch Method End of Year Exam ProjectRaissa KoffiNo ratings yet

- Assignment 1 Research Report On Impact of MicrofinanceDocument17 pagesAssignment 1 Research Report On Impact of MicrofinanceBikash Kumar ShahNo ratings yet

- Dissertation MicrofinanceDocument7 pagesDissertation MicrofinanceWritingServicesForCollegePapersAlbuquerque100% (1)

- Micro Finance in IndiaDocument13 pagesMicro Finance in Indiaashish bansalNo ratings yet

- Services Offered and Sustainable Development Program by The LifeBank Microfinance Foundation, Incorporated: Its Impact On The Branch 220 Members LivesDocument5 pagesServices Offered and Sustainable Development Program by The LifeBank Microfinance Foundation, Incorporated: Its Impact On The Branch 220 Members LivesPoonam KilaniyaNo ratings yet

- Climbing The Economic Ladder The Role of MicrofinaDocument20 pagesClimbing The Economic Ladder The Role of MicrofinaAmmi DonNo ratings yet

- Kapoy Na Jud HuhuhuDocument58 pagesKapoy Na Jud Huhuhumahinayjake09No ratings yet

- Project 2Document5 pagesProject 2Shivaram NayakNo ratings yet

- Does Microfinance Really Help The Poor? Evidence From Rural Households in EthiopiaDocument16 pagesDoes Microfinance Really Help The Poor? Evidence From Rural Households in EthiopiaZewdu EskeziaNo ratings yet

- Demeletal ReturnsDocument41 pagesDemeletal ReturnstanishkaNo ratings yet

- Microfinance and Poverty in The PhilippiDocument12 pagesMicrofinance and Poverty in The PhilippiLiza Laith LizzethNo ratings yet

- Share MicrofinDocument68 pagesShare MicrofinMubeenNo ratings yet

- Micro FinanceDocument32 pagesMicro Financepsychosoul009No ratings yet

- HolaaaDocument31 pagesHolaaaJohnmoni nathNo ratings yet

- Does Micro Finance Benefit The PoorDocument19 pagesDoes Micro Finance Benefit The PoorWamene100% (1)

- Analysis of The Effects of Microfinance PDFDocument13 pagesAnalysis of The Effects of Microfinance PDFxulphikarNo ratings yet

- SSRN Id1284472Document57 pagesSSRN Id1284472K61.FTU NGUYỄN ĐỨC HỒNG NGỌCNo ratings yet

- The Role of Microcredit in Poverty Reduction and Promoting Gender Equity A Discussion PaperDocument37 pagesThe Role of Microcredit in Poverty Reduction and Promoting Gender Equity A Discussion PaperCharu ModiNo ratings yet

- A Production Approach To Performance of Banks With Microfinance OperationsDocument18 pagesA Production Approach To Performance of Banks With Microfinance OperationsShweta workNo ratings yet

- Challenges & Issues of Microfinance in IndiaDocument5 pagesChallenges & Issues of Microfinance in IndiaEdris YawarNo ratings yet

- SKS Impact StudyDocument64 pagesSKS Impact Studypeter235No ratings yet

- Role of Microfinance Institutions in Rural Development B.V.S.S. Subba Rao AbstractDocument13 pagesRole of Microfinance Institutions in Rural Development B.V.S.S. Subba Rao AbstractIndu GuptaNo ratings yet

- Microfinance and Poverty: Evidence Using Panel Data From BangladeshDocument25 pagesMicrofinance and Poverty: Evidence Using Panel Data From BangladeshMvelako StoryNo ratings yet

- The Question of Sustainability For MicroDocument19 pagesThe Question of Sustainability For MicroFel Salazar JapsNo ratings yet

- Micro Finance SpeechDocument4 pagesMicro Finance SpeechJofel HilagaNo ratings yet

- Mitigating Inequality Through Micro-FinancingDocument5 pagesMitigating Inequality Through Micro-FinancingAndrés DelgadoNo ratings yet

- ReductionDocument17 pagesReductionedvinabregu08No ratings yet

- Xia Li 2011Document8 pagesXia Li 2011Feryanto W. Karo-KaroNo ratings yet

- Impact of Microfinance On Poverty Alleviation: The Study of District Bahawal Nagar, Punjab, PakistanDocument17 pagesImpact of Microfinance On Poverty Alleviation: The Study of District Bahawal Nagar, Punjab, PakistanMiss ZoobiNo ratings yet

- Microfinance Poverty and Food InsecurityDocument29 pagesMicrofinance Poverty and Food InsecurityzamaldudeNo ratings yet

- DeMel ReturnToCapitalSriLankaDocument44 pagesDeMel ReturnToCapitalSriLankaaseNo ratings yet

- Empowering Women Through Micro Finance RanchiDocument5 pagesEmpowering Women Through Micro Finance RanchiApoorva GuptaNo ratings yet

- 1.1 MicrocreditDocument18 pages1.1 MicrocreditMahbub SkyNo ratings yet

- Chapter 1-5 Kakapoy Na JudDocument47 pagesChapter 1-5 Kakapoy Na JudCarla Jane Maitom TagoyNo ratings yet

- Group 9 - EE - Role of Microfinance - CompressedDocument31 pagesGroup 9 - EE - Role of Microfinance - CompressedSwati PorwalNo ratings yet

- 4. Magartu BirbirsoDocument7 pages4. Magartu BirbirsoAsfaw BelayNo ratings yet

- Poverty Alleviation Through Micro Finance in India: Empirical EvidencesDocument8 pagesPoverty Alleviation Through Micro Finance in India: Empirical EvidencesRia MakkarNo ratings yet

- Building Financial Resilience: Do Credit and Finance Schemes Serve or Impoverish Vulnerable People?From EverandBuilding Financial Resilience: Do Credit and Finance Schemes Serve or Impoverish Vulnerable People?No ratings yet

- Micro-Financing and the Economic Health of a NationFrom EverandMicro-Financing and the Economic Health of a NationNo ratings yet

- Connecting the Disconnected: Coping Strategies of the Financially Excluded in BhutanFrom EverandConnecting the Disconnected: Coping Strategies of the Financially Excluded in BhutanNo ratings yet

- Mayne17 RobustToCCJPEDocument20 pagesMayne17 RobustToCCJPEkbhNo ratings yet

- IMIST ArticleDoctorat1Document14 pagesIMIST ArticleDoctorat1kbhNo ratings yet

- Teaching English For Specific Purposes (ESP) To The Students in English Language Teaching (ELT)Document13 pagesTeaching English For Specific Purposes (ESP) To The Students in English Language Teaching (ELT)kbhNo ratings yet

- SSRN Id3076781Document39 pagesSSRN Id3076781kbhNo ratings yet

- Economic Analysis and Policy: Cuong Viet NguyenDocument24 pagesEconomic Analysis and Policy: Cuong Viet NguyenkbhNo ratings yet

- Social Science & Medicine: Su Hyun Shin, Hyunjung JiDocument11 pagesSocial Science & Medicine: Su Hyun Shin, Hyunjung JikbhNo ratings yet

- Economic Shocks and Their Effect On The Schooling and Labor Participation of Youth: Evidence From The Metal Mining Price Boom in Chilean CountiesDocument29 pagesEconomic Shocks and Their Effect On The Schooling and Labor Participation of Youth: Evidence From The Metal Mining Price Boom in Chilean CountieskbhNo ratings yet

- Adr Vol40no1 9 Shocks Constraints Child Schooling ThailandDocument29 pagesAdr Vol40no1 9 Shocks Constraints Child Schooling ThailandkbhNo ratings yet

- Ingenico 5100 Paymark Merchant Quick Guide (Standard)Document2 pagesIngenico 5100 Paymark Merchant Quick Guide (Standard)Synjon ElderNo ratings yet

- NBP Gomal Uni InternshipDocument94 pagesNBP Gomal Uni InternshipahmadNo ratings yet

- Deposit SlipDocument2 pagesDeposit Slipsoly2k12No ratings yet

- Receipt Voucher: Jaipuria Institute of Management, LucknowDocument1 pageReceipt Voucher: Jaipuria Institute of Management, LucknowSanjeev Kumar Suman Student, Jaipuria LucknowNo ratings yet

- Indian Bank: Profile of The BankDocument16 pagesIndian Bank: Profile of The BankJagan NathanNo ratings yet

- 2980 Daf1206 LendingDocument118 pages2980 Daf1206 Lendingmargaret kurgatNo ratings yet

- Examination About Investment 15Document3 pagesExamination About Investment 15BLACKPINKLisaRoseJisooJennieNo ratings yet

- Chapter 3 Notes Money Class 12Document6 pagesChapter 3 Notes Money Class 12Ankush JiiNo ratings yet

- Global Exam I Fall 2012Document4 pagesGlobal Exam I Fall 2012mauricio0327No ratings yet

- Financial MarketDocument14 pagesFinancial MarketDavid DavidNo ratings yet

- PDF DocumentDocument12 pagesPDF Documentksa966ikNo ratings yet

- 31-12-20 To Till DateDocument3 pages31-12-20 To Till DatePDRK BABIUNo ratings yet

- Gmail - Raj Musicals - Order #6161Document2 pagesGmail - Raj Musicals - Order #6161DevakumarNo ratings yet

- RRBDocument13 pagesRRBNeelam DeshpandeNo ratings yet

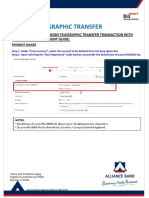

- How To Perform Foreign Telegraphic TransferDocument33 pagesHow To Perform Foreign Telegraphic TransferBerney RyxlerNo ratings yet

- Ancient India: Vedas Usury Sutras Jatakas Vasishtha Brahmin Kshatriya Varnas ManusmritiDocument7 pagesAncient India: Vedas Usury Sutras Jatakas Vasishtha Brahmin Kshatriya Varnas ManusmritiKamal Kiran BhanjaNo ratings yet

- Metrobank Vs PBComDocument2 pagesMetrobank Vs PBComRaiden DalusagNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument8 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancedilNo ratings yet

- Fin103 LT2 2004 - JTA-1Document4 pagesFin103 LT2 2004 - JTA-1JARED DARREN ONGNo ratings yet

- Paper Manajemen Risiko: Disusun Oleh: DAMA AZIIZ PRAYOGO (1805056014) Kelas Manajemen A7Document8 pagesPaper Manajemen Risiko: Disusun Oleh: DAMA AZIIZ PRAYOGO (1805056014) Kelas Manajemen A7blazerpria kerenNo ratings yet

- Steps To Private Placement Programs (PPP) DeskDocument7 pagesSteps To Private Placement Programs (PPP) DeskPattasan U100% (1)

- Real vs. Nominal Interest Rates: What's The Difference?Document5 pagesReal vs. Nominal Interest Rates: What's The Difference?Samantha EstilongNo ratings yet

- Expense Bill: Habib Bank LTD, Bangladesh OperationsDocument4 pagesExpense Bill: Habib Bank LTD, Bangladesh Operations2rmjNo ratings yet

- List of Empanelled Architects Under All Zones - Punjab & Sind Bank PDFDocument6 pagesList of Empanelled Architects Under All Zones - Punjab & Sind Bank PDFParvez KhanNo ratings yet

- Class 5 - JournalDocument17 pagesClass 5 - Journal04shubhgoelNo ratings yet

- The TransfersDocument3 pagesThe TransfersYahya Al-AmeriNo ratings yet

- Project Report On NPADocument24 pagesProject Report On NPANavkiran Kinni90% (30)