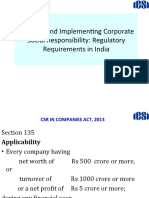

Corporate Social Responsibility Under Section 135 of Companies Act 2013

Corporate Social Responsibility Under Section 135 of Companies Act 2013

You might also like

- INTERMEDIATE ACCOUNTING 2 VALIX (Solution Manual)Document210 pagesINTERMEDIATE ACCOUNTING 2 VALIX (Solution Manual)Shairine Aquino100% (2)

- ch12 - Problems and SolutionsDocument44 pagesch12 - Problems and SolutionsErica Borres0% (1)

- AP4-3A KeyDocument2 pagesAP4-3A KeySindy1121No ratings yet

- My Pure Water Business Plan - Cotonou 25-08-2015Document28 pagesMy Pure Water Business Plan - Cotonou 25-08-2015api-293500234100% (1)

- Chapter 21 Accounting For Non Profit OrganizationsDocument21 pagesChapter 21 Accounting For Non Profit OrganizationsHyewon100% (1)

- Chipboard PlantDocument28 pagesChipboard Plantpradip_kumarNo ratings yet

- CSR - A Panoramic View - DR Bhasker ChatterjiDocument39 pagesCSR - A Panoramic View - DR Bhasker ChatterjicodemakitNo ratings yet

- Sachin Agrawal Batch No. 38Document15 pagesSachin Agrawal Batch No. 38lasix47725No ratings yet

- ApplicabilityDocument4 pagesApplicabilityvasantharaoNo ratings yet

- Chapter 3Document16 pagesChapter 3Mayank SenNo ratings yet

- Warner Bros. Pictures (India) Private LimitedDocument8 pagesWarner Bros. Pictures (India) Private Limitedsaurav singhNo ratings yet

- Companies (Corporate Social Responsibility Policy) Amendment 2021Document22 pagesCompanies (Corporate Social Responsibility Policy) Amendment 2021abhishek pareekNo ratings yet

- CSR NotesDocument14 pagesCSR NotesMallik SVNo ratings yet

- Trust Registration With McaDocument6 pagesTrust Registration With McaCA Amresh VashishtNo ratings yet

- CSR Provisions and Schedule VII of Companies Act, 2013 - Taxguru - inDocument7 pagesCSR Provisions and Schedule VII of Companies Act, 2013 - Taxguru - inPushkarajNo ratings yet

- Law Relating To Corporate Social ResponsibilityDocument12 pagesLaw Relating To Corporate Social ResponsibilityShivam RazorNo ratings yet

- Wa0000.Document14 pagesWa0000.Nikhil KumarNo ratings yet

- Corporate Social ResponsibilityDocument33 pagesCorporate Social ResponsibilitySharma VishnuNo ratings yet

- Section 135 of Companies Act For Corporate Social Responsibility - TDocument3 pagesSection 135 of Companies Act For Corporate Social Responsibility - TVivek ANo ratings yet

- CSR20Final2002022015 Removed RemovedDocument6 pagesCSR20Final2002022015 Removed RemovedNeha MehtaNo ratings yet

- CSR Project MergedDocument7 pagesCSR Project Mergedsyedsabafatima220No ratings yet

- Corporate Social ResponsibilityDocument3 pagesCorporate Social ResponsibilityabcNo ratings yet

- CSR Policy PDFDocument12 pagesCSR Policy PDFAkanksha DhandareNo ratings yet

- India's Mandatory CSR Law: Issues and Challenges: NavjeetDocument15 pagesIndia's Mandatory CSR Law: Issues and Challenges: NavjeetRohit KoulNo ratings yet

- Corporate Social Responsibility RevisedDocument12 pagesCorporate Social Responsibility RevisedVipul NarwalNo ratings yet

- Corporate Social ResponsibiltityDocument75 pagesCorporate Social ResponsibiltityyeshaNo ratings yet

- 0016 Avantika Tijare Assignment 2Document4 pages0016 Avantika Tijare Assignment 2AKSHAT SINGHNo ratings yet

- Corporate Social Responsibility PolicyDocument5 pagesCorporate Social Responsibility PolicyRaaj SinghNo ratings yet

- CSR Laws and GuidelinesDocument4 pagesCSR Laws and Guidelinesanishvijay23No ratings yet

- CSR As Per Companies Act, 2013Document7 pagesCSR As Per Companies Act, 2013Meghna S NedumpurathuNo ratings yet

- Corporate Social ResponsibilityDocument24 pagesCorporate Social ResponsibilityNaveen MettaNo ratings yet

- CSR-PPT-29 01 2020Document44 pagesCSR-PPT-29 01 2020Acs Kailash TyagiNo ratings yet

- CSR-PPT-29 01 2020Document44 pagesCSR-PPT-29 01 2020Acs Kailash TyagiNo ratings yet

- Policy For Corporate Social Responsibility of The Airports Authority of India-1Document56 pagesPolicy For Corporate Social Responsibility of The Airports Authority of India-1Manohar VennapusaNo ratings yet

- Corporate Social Responsibility Policy: Page 1 of 9Document9 pagesCorporate Social Responsibility Policy: Page 1 of 9Darshan KannurNo ratings yet

- CSR Rules Under Companies ActDocument10 pagesCSR Rules Under Companies ActSuperGuyNo ratings yet

- Corporate Social Responsibility (Section-135) : by Akhil Kodam 20464Document24 pagesCorporate Social Responsibility (Section-135) : by Akhil Kodam 20464Kodam AkhilNo ratings yet

- AzureviewDocument6 pagesAzureviewshubham2904365No ratings yet

- Corporate Social Responsibility (CSR) Policy: Page 1 of 12Document12 pagesCorporate Social Responsibility (CSR) Policy: Page 1 of 12Shubham Jain ModiNo ratings yet

- Chapter 17 - CSR Notes Lyst9419Document8 pagesChapter 17 - CSR Notes Lyst9419beniwalp095No ratings yet

- 1.4 - Annexure IV - CSR Policy Rules 2014Document6 pages1.4 - Annexure IV - CSR Policy Rules 2014Sandip KaleNo ratings yet

- Corporate Social Responsibility 2013Document8 pagesCorporate Social Responsibility 2013sanjeevseshannaNo ratings yet

- Highlights of (Corporate Social Responsibility Policy) Amendment Rules, 2021 - Taxguru - inDocument3 pagesHighlights of (Corporate Social Responsibility Policy) Amendment Rules, 2021 - Taxguru - inPushkarajNo ratings yet

- Spring EnergyDocument6 pagesSpring EnergyShivansh SharmaNo ratings yet

- Company CSR Policy As Per Section 135 (4) - 17012020Document5 pagesCompany CSR Policy As Per Section 135 (4) - 17012020rajesh uluwatuNo ratings yet

- CSR Amendment 1 Lyst3931 110717Document8 pagesCSR Amendment 1 Lyst3931 110717selvakumar2902No ratings yet

- Planning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaDocument23 pagesPlanning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaMuskan ManchandaNo ratings yet

- Concept of CSR in The Indian Context: Section 135 of Companies Act, 2013Document23 pagesConcept of CSR in The Indian Context: Section 135 of Companies Act, 2013Akansha GuptaNo ratings yet

- Corporate Social ResponsibilityDocument12 pagesCorporate Social ResponsibilitySalman MSDNo ratings yet

- CSR PolicyDocument6 pagesCSR PolicyAejaz PatelNo ratings yet

- CORPORATE-SOCIAL-RESPONSIBILITY-AND-SUSTAINABILITY-POLICY-2021 Balmer LawrieDocument13 pagesCORPORATE-SOCIAL-RESPONSIBILITY-AND-SUSTAINABILITY-POLICY-2021 Balmer Lawriekusum2016thadaNo ratings yet

- Unit - 5 Study Material ACGDocument16 pagesUnit - 5 Study Material ACGAbhijeet UpadhyayNo ratings yet

- Introduction To Corporate Social ResponsibilityDocument8 pagesIntroduction To Corporate Social Responsibilityjimmy sewNo ratings yet

- Adctx02 - 21 Paper 4Document7 pagesAdctx02 - 21 Paper 4Soumya swarup MohantyNo ratings yet

- CSR ICAI Guidelines FAQ'sDocument21 pagesCSR ICAI Guidelines FAQ'ssmsuvagiaNo ratings yet

- Hul PPT (CTP)Document31 pagesHul PPT (CTP)vedantNo ratings yet

- Punjab Alkalies and Chemicals LTDDocument4 pagesPunjab Alkalies and Chemicals LTDAshrafNo ratings yet

- Guidance Note On CSR Expenditure (My Notes)Document2 pagesGuidance Note On CSR Expenditure (My Notes)maulesh bhattNo ratings yet

- Corporate Social Responsibility: An Overview of The Companies Act, 2013Document41 pagesCorporate Social Responsibility: An Overview of The Companies Act, 2013Narender KumarNo ratings yet

- Start-Up: ObjectiveDocument10 pagesStart-Up: ObjectiveAventhikaNo ratings yet

- 2007 Revised Rules in The Availment of Income Tax HolidayDocument23 pages2007 Revised Rules in The Availment of Income Tax HolidayArchie Guevarra100% (1)

- Blackbook PDFDocument43 pagesBlackbook PDFrohitNo ratings yet

- MSL / Note On CSR (Inclusion Provisions of All Amendments Till Date) From: Secretarial & Legal Department / 11 March 2021Document11 pagesMSL / Note On CSR (Inclusion Provisions of All Amendments Till Date) From: Secretarial & Legal Department / 11 March 2021mgsalunke108No ratings yet

- CSR Policy - BilingualDocument15 pagesCSR Policy - BilingualRanjeet DongreNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Theory of AccountsDocument27 pagesTheory of Accountsyatz24No ratings yet

- Công Ty Cổ Phần Vĩnh Hoàn VHC 7.52.36 AmDocument37 pagesCông Ty Cổ Phần Vĩnh Hoàn VHC 7.52.36 AmTammy DaoNo ratings yet

- Joint Venture Management - Sales Positioning - EN20210624Document41 pagesJoint Venture Management - Sales Positioning - EN20210624pramodpatidar2018No ratings yet

- Balance Sheet PDFDocument10 pagesBalance Sheet PDFavinash singhNo ratings yet

- Sample Exit ExamDocument101 pagesSample Exit Examnaolmeseret22No ratings yet

- Hardship: Blake A Brewer 1904 West 75Th Place Davenport Ia 52806Document4 pagesHardship: Blake A Brewer 1904 West 75Th Place Davenport Ia 52806Blake BrewerNo ratings yet

- Risk Management - ITCDocument65 pagesRisk Management - ITCVenugopal VutukuruNo ratings yet

- Paper 7 CmaDocument16 pagesPaper 7 CmaRama KrishnaNo ratings yet

- RTP May 2019 EngDocument162 pagesRTP May 2019 EngVarun SahaniNo ratings yet

- SPADE Analysis Globe Telecom Inc PDFDocument29 pagesSPADE Analysis Globe Telecom Inc PDFLara FloresNo ratings yet

- Midterm Exam (Reviewer)Document84 pagesMidterm Exam (Reviewer)Mj PamintuanNo ratings yet

- What Are Financial Statements?: Financial Statements Represent A Formal Record of The Financial Activities ofDocument6 pagesWhat Are Financial Statements?: Financial Statements Represent A Formal Record of The Financial Activities ofkyrieNo ratings yet

- Khunt Meet ProjectDocument50 pagesKhunt Meet ProjectMeet PrajapatiNo ratings yet

- 02.using Bloomberg Terminals in A Security Analysis and Portfolio Management CourseDocument17 pages02.using Bloomberg Terminals in A Security Analysis and Portfolio Management CourseDarylChanNo ratings yet

- TheTechBlackBoard-AZ-900 - Latest-765Questions - SampleDocument14 pagesTheTechBlackBoard-AZ-900 - Latest-765Questions - SampledivyanshugroverNo ratings yet

- Pt. Ram Lembar Kerja (Sesi 2)Document10 pagesPt. Ram Lembar Kerja (Sesi 2)fannysuwandiNo ratings yet

- SITXFIN004 Student Assessment TasksDocument49 pagesSITXFIN004 Student Assessment Tasksshahriar2k00No ratings yet

- 2013 Unit 7 Tutorial QuestionsDocument4 pages2013 Unit 7 Tutorial QuestionsCkit1990No ratings yet

- Housing Loan of PNBDocument38 pagesHousing Loan of PNBgunpriyaNo ratings yet

- Hair and Beauty Salon Business PlanDocument28 pagesHair and Beauty Salon Business PlanDonNo ratings yet

- A Further Look at Financial StatementsDocument56 pagesA Further Look at Financial StatementsLê Thanh HàNo ratings yet

- Quiz 02 - FAR - UCP - ANS KEYDocument9 pagesQuiz 02 - FAR - UCP - ANS KEYkarim abitagoNo ratings yet

- Bukti TransaktiDocument22 pagesBukti Transakti유리사No ratings yet

- Party Wagon Inc Problem 51a CompressDocument61 pagesParty Wagon Inc Problem 51a CompressMuhammad Salman ImranNo ratings yet

Download as pdf or txt

You might also like

- INTERMEDIATE ACCOUNTING 2 VALIX (Solution Manual)Document210 pagesINTERMEDIATE ACCOUNTING 2 VALIX (Solution Manual)Shairine Aquino100% (2)

- ch12 - Problems and SolutionsDocument44 pagesch12 - Problems and SolutionsErica Borres0% (1)

- AP4-3A KeyDocument2 pagesAP4-3A KeySindy1121No ratings yet

- My Pure Water Business Plan - Cotonou 25-08-2015Document28 pagesMy Pure Water Business Plan - Cotonou 25-08-2015api-293500234100% (1)

- Chapter 21 Accounting For Non Profit OrganizationsDocument21 pagesChapter 21 Accounting For Non Profit OrganizationsHyewon100% (1)

- Chipboard PlantDocument28 pagesChipboard Plantpradip_kumarNo ratings yet

- CSR - A Panoramic View - DR Bhasker ChatterjiDocument39 pagesCSR - A Panoramic View - DR Bhasker ChatterjicodemakitNo ratings yet

- Sachin Agrawal Batch No. 38Document15 pagesSachin Agrawal Batch No. 38lasix47725No ratings yet

- ApplicabilityDocument4 pagesApplicabilityvasantharaoNo ratings yet

- Chapter 3Document16 pagesChapter 3Mayank SenNo ratings yet

- Warner Bros. Pictures (India) Private LimitedDocument8 pagesWarner Bros. Pictures (India) Private Limitedsaurav singhNo ratings yet

- Companies (Corporate Social Responsibility Policy) Amendment 2021Document22 pagesCompanies (Corporate Social Responsibility Policy) Amendment 2021abhishek pareekNo ratings yet

- CSR NotesDocument14 pagesCSR NotesMallik SVNo ratings yet

- Trust Registration With McaDocument6 pagesTrust Registration With McaCA Amresh VashishtNo ratings yet

- CSR Provisions and Schedule VII of Companies Act, 2013 - Taxguru - inDocument7 pagesCSR Provisions and Schedule VII of Companies Act, 2013 - Taxguru - inPushkarajNo ratings yet

- Law Relating To Corporate Social ResponsibilityDocument12 pagesLaw Relating To Corporate Social ResponsibilityShivam RazorNo ratings yet

- Wa0000.Document14 pagesWa0000.Nikhil KumarNo ratings yet

- Corporate Social ResponsibilityDocument33 pagesCorporate Social ResponsibilitySharma VishnuNo ratings yet

- Section 135 of Companies Act For Corporate Social Responsibility - TDocument3 pagesSection 135 of Companies Act For Corporate Social Responsibility - TVivek ANo ratings yet

- CSR20Final2002022015 Removed RemovedDocument6 pagesCSR20Final2002022015 Removed RemovedNeha MehtaNo ratings yet

- CSR Project MergedDocument7 pagesCSR Project Mergedsyedsabafatima220No ratings yet

- Corporate Social ResponsibilityDocument3 pagesCorporate Social ResponsibilityabcNo ratings yet

- CSR Policy PDFDocument12 pagesCSR Policy PDFAkanksha DhandareNo ratings yet

- India's Mandatory CSR Law: Issues and Challenges: NavjeetDocument15 pagesIndia's Mandatory CSR Law: Issues and Challenges: NavjeetRohit KoulNo ratings yet

- Corporate Social Responsibility RevisedDocument12 pagesCorporate Social Responsibility RevisedVipul NarwalNo ratings yet

- Corporate Social ResponsibiltityDocument75 pagesCorporate Social ResponsibiltityyeshaNo ratings yet

- 0016 Avantika Tijare Assignment 2Document4 pages0016 Avantika Tijare Assignment 2AKSHAT SINGHNo ratings yet

- Corporate Social Responsibility PolicyDocument5 pagesCorporate Social Responsibility PolicyRaaj SinghNo ratings yet

- CSR Laws and GuidelinesDocument4 pagesCSR Laws and Guidelinesanishvijay23No ratings yet

- CSR As Per Companies Act, 2013Document7 pagesCSR As Per Companies Act, 2013Meghna S NedumpurathuNo ratings yet

- Corporate Social ResponsibilityDocument24 pagesCorporate Social ResponsibilityNaveen MettaNo ratings yet

- CSR-PPT-29 01 2020Document44 pagesCSR-PPT-29 01 2020Acs Kailash TyagiNo ratings yet

- CSR-PPT-29 01 2020Document44 pagesCSR-PPT-29 01 2020Acs Kailash TyagiNo ratings yet

- Policy For Corporate Social Responsibility of The Airports Authority of India-1Document56 pagesPolicy For Corporate Social Responsibility of The Airports Authority of India-1Manohar VennapusaNo ratings yet

- Corporate Social Responsibility Policy: Page 1 of 9Document9 pagesCorporate Social Responsibility Policy: Page 1 of 9Darshan KannurNo ratings yet

- CSR Rules Under Companies ActDocument10 pagesCSR Rules Under Companies ActSuperGuyNo ratings yet

- Corporate Social Responsibility (Section-135) : by Akhil Kodam 20464Document24 pagesCorporate Social Responsibility (Section-135) : by Akhil Kodam 20464Kodam AkhilNo ratings yet

- AzureviewDocument6 pagesAzureviewshubham2904365No ratings yet

- Corporate Social Responsibility (CSR) Policy: Page 1 of 12Document12 pagesCorporate Social Responsibility (CSR) Policy: Page 1 of 12Shubham Jain ModiNo ratings yet

- Chapter 17 - CSR Notes Lyst9419Document8 pagesChapter 17 - CSR Notes Lyst9419beniwalp095No ratings yet

- 1.4 - Annexure IV - CSR Policy Rules 2014Document6 pages1.4 - Annexure IV - CSR Policy Rules 2014Sandip KaleNo ratings yet

- Corporate Social Responsibility 2013Document8 pagesCorporate Social Responsibility 2013sanjeevseshannaNo ratings yet

- Highlights of (Corporate Social Responsibility Policy) Amendment Rules, 2021 - Taxguru - inDocument3 pagesHighlights of (Corporate Social Responsibility Policy) Amendment Rules, 2021 - Taxguru - inPushkarajNo ratings yet

- Spring EnergyDocument6 pagesSpring EnergyShivansh SharmaNo ratings yet

- Company CSR Policy As Per Section 135 (4) - 17012020Document5 pagesCompany CSR Policy As Per Section 135 (4) - 17012020rajesh uluwatuNo ratings yet

- CSR Amendment 1 Lyst3931 110717Document8 pagesCSR Amendment 1 Lyst3931 110717selvakumar2902No ratings yet

- Planning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaDocument23 pagesPlanning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaMuskan ManchandaNo ratings yet

- Concept of CSR in The Indian Context: Section 135 of Companies Act, 2013Document23 pagesConcept of CSR in The Indian Context: Section 135 of Companies Act, 2013Akansha GuptaNo ratings yet

- Corporate Social ResponsibilityDocument12 pagesCorporate Social ResponsibilitySalman MSDNo ratings yet

- CSR PolicyDocument6 pagesCSR PolicyAejaz PatelNo ratings yet

- CORPORATE-SOCIAL-RESPONSIBILITY-AND-SUSTAINABILITY-POLICY-2021 Balmer LawrieDocument13 pagesCORPORATE-SOCIAL-RESPONSIBILITY-AND-SUSTAINABILITY-POLICY-2021 Balmer Lawriekusum2016thadaNo ratings yet

- Unit - 5 Study Material ACGDocument16 pagesUnit - 5 Study Material ACGAbhijeet UpadhyayNo ratings yet

- Introduction To Corporate Social ResponsibilityDocument8 pagesIntroduction To Corporate Social Responsibilityjimmy sewNo ratings yet

- Adctx02 - 21 Paper 4Document7 pagesAdctx02 - 21 Paper 4Soumya swarup MohantyNo ratings yet

- CSR ICAI Guidelines FAQ'sDocument21 pagesCSR ICAI Guidelines FAQ'ssmsuvagiaNo ratings yet

- Hul PPT (CTP)Document31 pagesHul PPT (CTP)vedantNo ratings yet

- Punjab Alkalies and Chemicals LTDDocument4 pagesPunjab Alkalies and Chemicals LTDAshrafNo ratings yet

- Guidance Note On CSR Expenditure (My Notes)Document2 pagesGuidance Note On CSR Expenditure (My Notes)maulesh bhattNo ratings yet

- Corporate Social Responsibility: An Overview of The Companies Act, 2013Document41 pagesCorporate Social Responsibility: An Overview of The Companies Act, 2013Narender KumarNo ratings yet

- Start-Up: ObjectiveDocument10 pagesStart-Up: ObjectiveAventhikaNo ratings yet

- 2007 Revised Rules in The Availment of Income Tax HolidayDocument23 pages2007 Revised Rules in The Availment of Income Tax HolidayArchie Guevarra100% (1)

- Blackbook PDFDocument43 pagesBlackbook PDFrohitNo ratings yet

- MSL / Note On CSR (Inclusion Provisions of All Amendments Till Date) From: Secretarial & Legal Department / 11 March 2021Document11 pagesMSL / Note On CSR (Inclusion Provisions of All Amendments Till Date) From: Secretarial & Legal Department / 11 March 2021mgsalunke108No ratings yet

- CSR Policy - BilingualDocument15 pagesCSR Policy - BilingualRanjeet DongreNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Theory of AccountsDocument27 pagesTheory of Accountsyatz24No ratings yet

- Công Ty Cổ Phần Vĩnh Hoàn VHC 7.52.36 AmDocument37 pagesCông Ty Cổ Phần Vĩnh Hoàn VHC 7.52.36 AmTammy DaoNo ratings yet

- Joint Venture Management - Sales Positioning - EN20210624Document41 pagesJoint Venture Management - Sales Positioning - EN20210624pramodpatidar2018No ratings yet

- Balance Sheet PDFDocument10 pagesBalance Sheet PDFavinash singhNo ratings yet

- Sample Exit ExamDocument101 pagesSample Exit Examnaolmeseret22No ratings yet

- Hardship: Blake A Brewer 1904 West 75Th Place Davenport Ia 52806Document4 pagesHardship: Blake A Brewer 1904 West 75Th Place Davenport Ia 52806Blake BrewerNo ratings yet

- Risk Management - ITCDocument65 pagesRisk Management - ITCVenugopal VutukuruNo ratings yet

- Paper 7 CmaDocument16 pagesPaper 7 CmaRama KrishnaNo ratings yet

- RTP May 2019 EngDocument162 pagesRTP May 2019 EngVarun SahaniNo ratings yet

- SPADE Analysis Globe Telecom Inc PDFDocument29 pagesSPADE Analysis Globe Telecom Inc PDFLara FloresNo ratings yet

- Midterm Exam (Reviewer)Document84 pagesMidterm Exam (Reviewer)Mj PamintuanNo ratings yet

- What Are Financial Statements?: Financial Statements Represent A Formal Record of The Financial Activities ofDocument6 pagesWhat Are Financial Statements?: Financial Statements Represent A Formal Record of The Financial Activities ofkyrieNo ratings yet

- Khunt Meet ProjectDocument50 pagesKhunt Meet ProjectMeet PrajapatiNo ratings yet

- 02.using Bloomberg Terminals in A Security Analysis and Portfolio Management CourseDocument17 pages02.using Bloomberg Terminals in A Security Analysis and Portfolio Management CourseDarylChanNo ratings yet

- TheTechBlackBoard-AZ-900 - Latest-765Questions - SampleDocument14 pagesTheTechBlackBoard-AZ-900 - Latest-765Questions - SampledivyanshugroverNo ratings yet

- Pt. Ram Lembar Kerja (Sesi 2)Document10 pagesPt. Ram Lembar Kerja (Sesi 2)fannysuwandiNo ratings yet

- SITXFIN004 Student Assessment TasksDocument49 pagesSITXFIN004 Student Assessment Tasksshahriar2k00No ratings yet

- 2013 Unit 7 Tutorial QuestionsDocument4 pages2013 Unit 7 Tutorial QuestionsCkit1990No ratings yet

- Housing Loan of PNBDocument38 pagesHousing Loan of PNBgunpriyaNo ratings yet

- Hair and Beauty Salon Business PlanDocument28 pagesHair and Beauty Salon Business PlanDonNo ratings yet

- A Further Look at Financial StatementsDocument56 pagesA Further Look at Financial StatementsLê Thanh HàNo ratings yet

- Quiz 02 - FAR - UCP - ANS KEYDocument9 pagesQuiz 02 - FAR - UCP - ANS KEYkarim abitagoNo ratings yet

- Bukti TransaktiDocument22 pagesBukti Transakti유리사No ratings yet

- Party Wagon Inc Problem 51a CompressDocument61 pagesParty Wagon Inc Problem 51a CompressMuhammad Salman ImranNo ratings yet