Stock Market Concentration - How Much Is Too Much

Stock Market Concentration - How Much Is Too Much

You might also like

- (English) MEGACITIES of The World (Season 1 - Complete)Document58 pages(English) MEGACITIES of The World (Season 1 - Complete)Sveta EnglishNo ratings yet

- Lululemon Accounting AssignmentDocument20 pagesLululemon Accounting AssignmentBilal AlamNo ratings yet

- Bizhub c3350 Manual PDFDocument81 pagesBizhub c3350 Manual PDFStiven PereiraNo ratings yet

- Tanabe Air Compressor ManualDocument4 pagesTanabe Air Compressor ManualMeta Beta50% (2)

- The Sixty-Year Downward Trend of Economi PDFDocument20 pagesThe Sixty-Year Downward Trend of Economi PDFMarcus WilliamsNo ratings yet

- Why Does Ipo Volume Fluctuate So MuchDocument38 pagesWhy Does Ipo Volume Fluctuate So MuchéricNo ratings yet

- Greenwood - Scharfstein - 2013 - The Growth of FinanceDocument26 pagesGreenwood - Scharfstein - 2013 - The Growth of FinanceBárbara AliagaNo ratings yet

- Lecture 04 - Market EfficiencyDocument34 pagesLecture 04 - Market EfficiencyJingwen YangNo ratings yet

- EMH - Ch6 - Revised LectureDocument60 pagesEMH - Ch6 - Revised Lectureauji amaliaNo ratings yet

- 11311-1087032 CavalloDocument43 pages11311-1087032 CavalloThanekaivel SNo ratings yet

- Measuring The MiddleDocument23 pagesMeasuring The MiddleGabii AmaralNo ratings yet

- AMERCO Investor Presentation 2020Document25 pagesAMERCO Investor Presentation 2020Daniel KwanNo ratings yet

- En Principal Islamic Asia Pacific Dynamic Equity Fund MYR FFSDocument2 pagesEn Principal Islamic Asia Pacific Dynamic Equity Fund MYR FFSsantiyrhNo ratings yet

- Know Your Behavioural BiasesDocument44 pagesKnow Your Behavioural BiasesShreeraj ModiNo ratings yet

- Predicting The Markets Nov2020 - ch4Document29 pagesPredicting The Markets Nov2020 - ch4scribbugNo ratings yet

- Digitalisation On EconomyDocument20 pagesDigitalisation On EconomyMacsim BogdanNo ratings yet

- Developer - 2018 OutlookDocument17 pagesDeveloper - 2018 OutlookFahima Izzatun NisaaNo ratings yet

- The Private Sector Financial Balance As A Predictor of Financial CrisesDocument12 pagesThe Private Sector Financial Balance As A Predictor of Financial CrisesIsaac GoldNo ratings yet

- Hayden Capital Quarterly Letter 2021 Q1Document16 pagesHayden Capital Quarterly Letter 2021 Q1fatih jumongNo ratings yet

- Mansa-X KES Fact Sheet Q1 2023Document1 pageMansa-X KES Fact Sheet Q1 2023KevinNo ratings yet

- Motilal Oswal Value Strategy FundDocument27 pagesMotilal Oswal Value Strategy FundFountainheadNo ratings yet

- ECON F312: Money, Banking and Financial Markets I Semester 2020-21Document23 pagesECON F312: Money, Banking and Financial Markets I Semester 2020-21AKSHIT JAINNo ratings yet

- Navin Agarwal Article Sep 2021Document5 pagesNavin Agarwal Article Sep 2021Smeet GopaniNo ratings yet

- Democratic Legacy of The MRDocument29 pagesDemocratic Legacy of The MRFlacso México CV académicoNo ratings yet

- Predicting The Markets Chapter 4 Charts: Predicting InflationDocument29 pagesPredicting The Markets Chapter 4 Charts: Predicting InflationscribbugNo ratings yet

- MicrosoftWord ReportDebtDocument4 pagesMicrosoftWord ReportDebtCommittee For a Responsible Federal BudgetNo ratings yet

- How The P/E Ratio Can Really Help You: Ordinary Investor's Education Series No. 1Document22 pagesHow The P/E Ratio Can Really Help You: Ordinary Investor's Education Series No. 1Bhakti Bhushan MishraNo ratings yet

- Summer Internship ProjectDocument31 pagesSummer Internship ProjectAayush PasawalaNo ratings yet

- Mud Executive Order ReportDocument19 pagesMud Executive Order ReportTanasha FlandersNo ratings yet

- MRCI 2023 Market Seasonal Patterns-2Document23 pagesMRCI 2023 Market Seasonal Patterns-2Gkgg100% (1)

- Web 2.0 Weekly - May 11, 2010Document32 pagesWeb 2.0 Weekly - May 11, 2010David ShoreNo ratings yet

- Annual-Letter-To-Shareholders - Terry Smith 2015Document6 pagesAnnual-Letter-To-Shareholders - Terry Smith 2015TotmolNo ratings yet

- Fundsmith Equity Fund +18.3 +449.3 +18.2 1.11 1.06 Equities +12.3 +214.8 +11.9 0.56 0.52 UK Bonds +4.6 +47.5 +3.9 N/a N/a Cash +0.3 +6.3 +0.6 N/a N/aDocument13 pagesFundsmith Equity Fund +18.3 +449.3 +18.2 1.11 1.06 Equities +12.3 +214.8 +11.9 0.56 0.52 UK Bonds +4.6 +47.5 +3.9 N/a N/a Cash +0.3 +6.3 +0.6 N/a N/aGiovanno HermawanNo ratings yet

- SP 220405Document14 pagesSP 220405Ling DylNo ratings yet

- Financiarizacion Empresas UKDocument25 pagesFinanciarizacion Empresas UKArturo Martínez BareaNo ratings yet

- How Does Aid Support Womens Economic Empowerment 2021Document7 pagesHow Does Aid Support Womens Economic Empowerment 2021Glaiza Veluz-SulitNo ratings yet

- Chap 18Document32 pagesChap 18Queen CatastropheNo ratings yet

- Chart Title: 35 Relaxo Footwear Bata Mirza IntlDocument5 pagesChart Title: 35 Relaxo Footwear Bata Mirza Intlsuchita chukkalaNo ratings yet

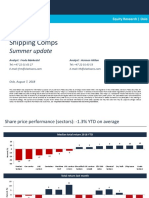

- Shipping Summer Update 2018Document38 pagesShipping Summer Update 2018Samu MenendezNo ratings yet

- Bwa M 03272018Document8 pagesBwa M 03272018asdf100% (1)

- WSO 2022 IB Working Conditions SurveyDocument42 pagesWSO 2022 IB Working Conditions SurveyPhạm Hồng HuếNo ratings yet

- Philippines Market OutlookDocument24 pagesPhilippines Market OutlookJonathan Ian ArinsolNo ratings yet

- BP Statistics Analysis 2015Document19 pagesBP Statistics Analysis 2015Kartik AnejaNo ratings yet

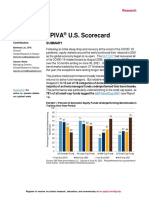

- Spiva Us Mid Year 2021Document36 pagesSpiva Us Mid Year 2021Gábor ZsédelyNo ratings yet

- Web 2.0 Weekly - May 18, 2010 "What Recession? Online Luxury Heats Up"Document32 pagesWeb 2.0 Weekly - May 18, 2010 "What Recession? Online Luxury Heats Up"David ShoreNo ratings yet

- Taking Stock Quarterly Outlook en UsDocument4 pagesTaking Stock Quarterly Outlook en UsjayeshNo ratings yet

- Monthly Meet - April 2017Document43 pagesMonthly Meet - April 2017MukeshSharmaNo ratings yet

- Msci Mis em May 2018Document6 pagesMsci Mis em May 2018Mitesh100% (1)

- GS Global Macro ReportDocument26 pagesGS Global Macro ReportRyanNo ratings yet

- Fourteen: Financial Analysis of Common StocksDocument36 pagesFourteen: Financial Analysis of Common StocksSyed AliNo ratings yet

- Accumulation of Forex and Long Term Economic GrowthDocument52 pagesAccumulation of Forex and Long Term Economic GrowthshaktisahayNo ratings yet

- Request-Jefferies Nantucket FINAL v3Document39 pagesRequest-Jefferies Nantucket FINAL v3guillermoNo ratings yet

- Top Office Markets Report March2023Document136 pagesTop Office Markets Report March2023Pratik BhowmikNo ratings yet

- Spatial Pattern and E Development in China's Urbanization: SustainabilityDocument16 pagesSpatial Pattern and E Development in China's Urbanization: SustainabilityAnjali RaithathaNo ratings yet

- Mankiw8e Chap18Document31 pagesMankiw8e Chap18Sardar AftabNo ratings yet

- Chart PackDocument35 pagesChart Packxyan.zohar7No ratings yet

- Analysis of Marketing Mix Involved in E-Marketing of Outlook MagazinesDocument63 pagesAnalysis of Marketing Mix Involved in E-Marketing of Outlook MagazinesTuhina MistryNo ratings yet

- Theory of Policy Borrowing and Lending I PDFDocument6 pagesTheory of Policy Borrowing and Lending I PDFpagieljcgmailcomNo ratings yet

- Q4 2021 - Investor LetterDocument11 pagesQ4 2021 - Investor LetterRishab WahalNo ratings yet

- Politics of Public Money Second Edition David A Good Online Ebook Texxtbook Full Chapter PDFDocument69 pagesPolitics of Public Money Second Edition David A Good Online Ebook Texxtbook Full Chapter PDFmichael.pleasant621100% (8)

- Trends in Foreign Direct Investment InflowsDocument7 pagesTrends in Foreign Direct Investment InflowsAnnamalai KarthickNo ratings yet

- The Australian Economy and Financial Markets: July 2019Document33 pagesThe Australian Economy and Financial Markets: July 2019Amita SinghNo ratings yet

- Brown Spot of RiceDocument16 pagesBrown Spot of Riceuvmahansar16No ratings yet

- Helix Board 24 FireWire MKIIDocument31 pagesHelix Board 24 FireWire MKIIJeremy MooreNo ratings yet

- Karpagam Academy of Higher Education: Minutes of Class Committee MeetingDocument3 pagesKarpagam Academy of Higher Education: Minutes of Class Committee MeetingDaniel DasNo ratings yet

- Cambridge IGCSE: BIOLOGY 0610/33Document20 pagesCambridge IGCSE: BIOLOGY 0610/33Saleha ShafiqueNo ratings yet

- OM ParticipantGuideDocument52 pagesOM ParticipantGuideGrace RuthNo ratings yet

- Bearing Pad 400 X 400 X 52 MM (Ss400 Yield 235 Mpa)Document3 pagesBearing Pad 400 X 400 X 52 MM (Ss400 Yield 235 Mpa)AlvinbriliantNo ratings yet

- Bending StressDocument9 pagesBending StressUjjal Kalita 19355No ratings yet

- Advanced Cardiac Life Support AsystoleDocument14 pagesAdvanced Cardiac Life Support AsystoleKar TwentyfiveNo ratings yet

- (Ebook) Goodspeed, Edgar J - A History of Early Christian Literature (Christian Library)Document125 pages(Ebook) Goodspeed, Edgar J - A History of Early Christian Literature (Christian Library)Giorgosby17No ratings yet

- Computer Networking A Top Down Approach 7Th Edition PDF Full ChapterDocument41 pagesComputer Networking A Top Down Approach 7Th Edition PDF Full Chapterlawrence.graves202100% (16)

- HP ProLiant ML370 G6 ServerDocument4 pagesHP ProLiant ML370 G6 ServerTrenell Steffan IsraelNo ratings yet

- Voting Preferences in The National Election A Case Among First-Time VotersDocument10 pagesVoting Preferences in The National Election A Case Among First-Time VotersInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Design and Analysis of Water Quality Monitoring and Filtration System For Different Types of Water in MalaysiaDocument12 pagesDesign and Analysis of Water Quality Monitoring and Filtration System For Different Types of Water in MalaysiaMary Anne YadaoNo ratings yet

- MA3003 Standard EU ML Actuador - Electronico de GiroDocument70 pagesMA3003 Standard EU ML Actuador - Electronico de GirojaseriNo ratings yet

- Genexpert Sars-Cov-2 (Covid-19) Vs Genexpert Mdr/Rif (TB) Test. Keep Moving Forward!Document4 pagesGenexpert Sars-Cov-2 (Covid-19) Vs Genexpert Mdr/Rif (TB) Test. Keep Moving Forward!Bashir MtwaklNo ratings yet

- S.S. Hebberd - Philosophy of HistoryDocument320 pagesS.S. Hebberd - Philosophy of HistorySzoha TomaNo ratings yet

- Granta Selector Installation GuideDocument7 pagesGranta Selector Installation Guidem.junaid143103No ratings yet

- Inductive Deductive QuizDocument1 pageInductive Deductive Quizkimbeerlyn doromasNo ratings yet

- Eurocode 3 Stress Ratio Presentation 5 by Lee CKDocument17 pagesEurocode 3 Stress Ratio Presentation 5 by Lee CKKipodimNo ratings yet

- Greaves Cotton Ar 2018 1 PDFDocument168 pagesGreaves Cotton Ar 2018 1 PDFanand_parchureNo ratings yet

- Camo Paint ManualDocument182 pagesCamo Paint Manualwhsprz100% (1)

- Lecture Notes in Statistics 148Document241 pagesLecture Notes in Statistics 148argha48126No ratings yet

- Horizontal Well Drill String DesignDocument23 pagesHorizontal Well Drill String DesignTarek HassanNo ratings yet

- YuYuYu Bonus Chapter - Sonoko AfterDocument14 pagesYuYuYu Bonus Chapter - Sonoko AfterAaron ParkerNo ratings yet

- Government Engineering College Dahod: Dadhichi HostelDocument5 pagesGovernment Engineering College Dahod: Dadhichi HostelSandip MouryaNo ratings yet

- Psychology and AdvertisingDocument59 pagesPsychology and AdvertisingEMMA SHAFFU EL CHACARNo ratings yet

- 2005 تأثير المعالجة المسبقة للبذور عن طريق المجال المغناطيسي على حساسية شتلات الخيار للأشعة فوق البنفسجيةDocument9 pages2005 تأثير المعالجة المسبقة للبذور عن طريق المجال المغناطيسي على حساسية شتلات الخيار للأشعة فوق البنفسجيةMUHAMMED ALSUVAİDNo ratings yet

Download as pdf or txt

You might also like

- (English) MEGACITIES of The World (Season 1 - Complete)Document58 pages(English) MEGACITIES of The World (Season 1 - Complete)Sveta EnglishNo ratings yet

- Lululemon Accounting AssignmentDocument20 pagesLululemon Accounting AssignmentBilal AlamNo ratings yet

- Bizhub c3350 Manual PDFDocument81 pagesBizhub c3350 Manual PDFStiven PereiraNo ratings yet

- Tanabe Air Compressor ManualDocument4 pagesTanabe Air Compressor ManualMeta Beta50% (2)

- The Sixty-Year Downward Trend of Economi PDFDocument20 pagesThe Sixty-Year Downward Trend of Economi PDFMarcus WilliamsNo ratings yet

- Why Does Ipo Volume Fluctuate So MuchDocument38 pagesWhy Does Ipo Volume Fluctuate So MuchéricNo ratings yet

- Greenwood - Scharfstein - 2013 - The Growth of FinanceDocument26 pagesGreenwood - Scharfstein - 2013 - The Growth of FinanceBárbara AliagaNo ratings yet

- Lecture 04 - Market EfficiencyDocument34 pagesLecture 04 - Market EfficiencyJingwen YangNo ratings yet

- EMH - Ch6 - Revised LectureDocument60 pagesEMH - Ch6 - Revised Lectureauji amaliaNo ratings yet

- 11311-1087032 CavalloDocument43 pages11311-1087032 CavalloThanekaivel SNo ratings yet

- Measuring The MiddleDocument23 pagesMeasuring The MiddleGabii AmaralNo ratings yet

- AMERCO Investor Presentation 2020Document25 pagesAMERCO Investor Presentation 2020Daniel KwanNo ratings yet

- En Principal Islamic Asia Pacific Dynamic Equity Fund MYR FFSDocument2 pagesEn Principal Islamic Asia Pacific Dynamic Equity Fund MYR FFSsantiyrhNo ratings yet

- Know Your Behavioural BiasesDocument44 pagesKnow Your Behavioural BiasesShreeraj ModiNo ratings yet

- Predicting The Markets Nov2020 - ch4Document29 pagesPredicting The Markets Nov2020 - ch4scribbugNo ratings yet

- Digitalisation On EconomyDocument20 pagesDigitalisation On EconomyMacsim BogdanNo ratings yet

- Developer - 2018 OutlookDocument17 pagesDeveloper - 2018 OutlookFahima Izzatun NisaaNo ratings yet

- The Private Sector Financial Balance As A Predictor of Financial CrisesDocument12 pagesThe Private Sector Financial Balance As A Predictor of Financial CrisesIsaac GoldNo ratings yet

- Hayden Capital Quarterly Letter 2021 Q1Document16 pagesHayden Capital Quarterly Letter 2021 Q1fatih jumongNo ratings yet

- Mansa-X KES Fact Sheet Q1 2023Document1 pageMansa-X KES Fact Sheet Q1 2023KevinNo ratings yet

- Motilal Oswal Value Strategy FundDocument27 pagesMotilal Oswal Value Strategy FundFountainheadNo ratings yet

- ECON F312: Money, Banking and Financial Markets I Semester 2020-21Document23 pagesECON F312: Money, Banking and Financial Markets I Semester 2020-21AKSHIT JAINNo ratings yet

- Navin Agarwal Article Sep 2021Document5 pagesNavin Agarwal Article Sep 2021Smeet GopaniNo ratings yet

- Democratic Legacy of The MRDocument29 pagesDemocratic Legacy of The MRFlacso México CV académicoNo ratings yet

- Predicting The Markets Chapter 4 Charts: Predicting InflationDocument29 pagesPredicting The Markets Chapter 4 Charts: Predicting InflationscribbugNo ratings yet

- MicrosoftWord ReportDebtDocument4 pagesMicrosoftWord ReportDebtCommittee For a Responsible Federal BudgetNo ratings yet

- How The P/E Ratio Can Really Help You: Ordinary Investor's Education Series No. 1Document22 pagesHow The P/E Ratio Can Really Help You: Ordinary Investor's Education Series No. 1Bhakti Bhushan MishraNo ratings yet

- Summer Internship ProjectDocument31 pagesSummer Internship ProjectAayush PasawalaNo ratings yet

- Mud Executive Order ReportDocument19 pagesMud Executive Order ReportTanasha FlandersNo ratings yet

- MRCI 2023 Market Seasonal Patterns-2Document23 pagesMRCI 2023 Market Seasonal Patterns-2Gkgg100% (1)

- Web 2.0 Weekly - May 11, 2010Document32 pagesWeb 2.0 Weekly - May 11, 2010David ShoreNo ratings yet

- Annual-Letter-To-Shareholders - Terry Smith 2015Document6 pagesAnnual-Letter-To-Shareholders - Terry Smith 2015TotmolNo ratings yet

- Fundsmith Equity Fund +18.3 +449.3 +18.2 1.11 1.06 Equities +12.3 +214.8 +11.9 0.56 0.52 UK Bonds +4.6 +47.5 +3.9 N/a N/a Cash +0.3 +6.3 +0.6 N/a N/aDocument13 pagesFundsmith Equity Fund +18.3 +449.3 +18.2 1.11 1.06 Equities +12.3 +214.8 +11.9 0.56 0.52 UK Bonds +4.6 +47.5 +3.9 N/a N/a Cash +0.3 +6.3 +0.6 N/a N/aGiovanno HermawanNo ratings yet

- SP 220405Document14 pagesSP 220405Ling DylNo ratings yet

- Financiarizacion Empresas UKDocument25 pagesFinanciarizacion Empresas UKArturo Martínez BareaNo ratings yet

- How Does Aid Support Womens Economic Empowerment 2021Document7 pagesHow Does Aid Support Womens Economic Empowerment 2021Glaiza Veluz-SulitNo ratings yet

- Chap 18Document32 pagesChap 18Queen CatastropheNo ratings yet

- Chart Title: 35 Relaxo Footwear Bata Mirza IntlDocument5 pagesChart Title: 35 Relaxo Footwear Bata Mirza Intlsuchita chukkalaNo ratings yet

- Shipping Summer Update 2018Document38 pagesShipping Summer Update 2018Samu MenendezNo ratings yet

- Bwa M 03272018Document8 pagesBwa M 03272018asdf100% (1)

- WSO 2022 IB Working Conditions SurveyDocument42 pagesWSO 2022 IB Working Conditions SurveyPhạm Hồng HuếNo ratings yet

- Philippines Market OutlookDocument24 pagesPhilippines Market OutlookJonathan Ian ArinsolNo ratings yet

- BP Statistics Analysis 2015Document19 pagesBP Statistics Analysis 2015Kartik AnejaNo ratings yet

- Spiva Us Mid Year 2021Document36 pagesSpiva Us Mid Year 2021Gábor ZsédelyNo ratings yet

- Web 2.0 Weekly - May 18, 2010 "What Recession? Online Luxury Heats Up"Document32 pagesWeb 2.0 Weekly - May 18, 2010 "What Recession? Online Luxury Heats Up"David ShoreNo ratings yet

- Taking Stock Quarterly Outlook en UsDocument4 pagesTaking Stock Quarterly Outlook en UsjayeshNo ratings yet

- Monthly Meet - April 2017Document43 pagesMonthly Meet - April 2017MukeshSharmaNo ratings yet

- Msci Mis em May 2018Document6 pagesMsci Mis em May 2018Mitesh100% (1)

- GS Global Macro ReportDocument26 pagesGS Global Macro ReportRyanNo ratings yet

- Fourteen: Financial Analysis of Common StocksDocument36 pagesFourteen: Financial Analysis of Common StocksSyed AliNo ratings yet

- Accumulation of Forex and Long Term Economic GrowthDocument52 pagesAccumulation of Forex and Long Term Economic GrowthshaktisahayNo ratings yet

- Request-Jefferies Nantucket FINAL v3Document39 pagesRequest-Jefferies Nantucket FINAL v3guillermoNo ratings yet

- Top Office Markets Report March2023Document136 pagesTop Office Markets Report March2023Pratik BhowmikNo ratings yet

- Spatial Pattern and E Development in China's Urbanization: SustainabilityDocument16 pagesSpatial Pattern and E Development in China's Urbanization: SustainabilityAnjali RaithathaNo ratings yet

- Mankiw8e Chap18Document31 pagesMankiw8e Chap18Sardar AftabNo ratings yet

- Chart PackDocument35 pagesChart Packxyan.zohar7No ratings yet

- Analysis of Marketing Mix Involved in E-Marketing of Outlook MagazinesDocument63 pagesAnalysis of Marketing Mix Involved in E-Marketing of Outlook MagazinesTuhina MistryNo ratings yet

- Theory of Policy Borrowing and Lending I PDFDocument6 pagesTheory of Policy Borrowing and Lending I PDFpagieljcgmailcomNo ratings yet

- Q4 2021 - Investor LetterDocument11 pagesQ4 2021 - Investor LetterRishab WahalNo ratings yet

- Politics of Public Money Second Edition David A Good Online Ebook Texxtbook Full Chapter PDFDocument69 pagesPolitics of Public Money Second Edition David A Good Online Ebook Texxtbook Full Chapter PDFmichael.pleasant621100% (8)

- Trends in Foreign Direct Investment InflowsDocument7 pagesTrends in Foreign Direct Investment InflowsAnnamalai KarthickNo ratings yet

- The Australian Economy and Financial Markets: July 2019Document33 pagesThe Australian Economy and Financial Markets: July 2019Amita SinghNo ratings yet

- Brown Spot of RiceDocument16 pagesBrown Spot of Riceuvmahansar16No ratings yet

- Helix Board 24 FireWire MKIIDocument31 pagesHelix Board 24 FireWire MKIIJeremy MooreNo ratings yet

- Karpagam Academy of Higher Education: Minutes of Class Committee MeetingDocument3 pagesKarpagam Academy of Higher Education: Minutes of Class Committee MeetingDaniel DasNo ratings yet

- Cambridge IGCSE: BIOLOGY 0610/33Document20 pagesCambridge IGCSE: BIOLOGY 0610/33Saleha ShafiqueNo ratings yet

- OM ParticipantGuideDocument52 pagesOM ParticipantGuideGrace RuthNo ratings yet

- Bearing Pad 400 X 400 X 52 MM (Ss400 Yield 235 Mpa)Document3 pagesBearing Pad 400 X 400 X 52 MM (Ss400 Yield 235 Mpa)AlvinbriliantNo ratings yet

- Bending StressDocument9 pagesBending StressUjjal Kalita 19355No ratings yet

- Advanced Cardiac Life Support AsystoleDocument14 pagesAdvanced Cardiac Life Support AsystoleKar TwentyfiveNo ratings yet

- (Ebook) Goodspeed, Edgar J - A History of Early Christian Literature (Christian Library)Document125 pages(Ebook) Goodspeed, Edgar J - A History of Early Christian Literature (Christian Library)Giorgosby17No ratings yet

- Computer Networking A Top Down Approach 7Th Edition PDF Full ChapterDocument41 pagesComputer Networking A Top Down Approach 7Th Edition PDF Full Chapterlawrence.graves202100% (16)

- HP ProLiant ML370 G6 ServerDocument4 pagesHP ProLiant ML370 G6 ServerTrenell Steffan IsraelNo ratings yet

- Voting Preferences in The National Election A Case Among First-Time VotersDocument10 pagesVoting Preferences in The National Election A Case Among First-Time VotersInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Design and Analysis of Water Quality Monitoring and Filtration System For Different Types of Water in MalaysiaDocument12 pagesDesign and Analysis of Water Quality Monitoring and Filtration System For Different Types of Water in MalaysiaMary Anne YadaoNo ratings yet

- MA3003 Standard EU ML Actuador - Electronico de GiroDocument70 pagesMA3003 Standard EU ML Actuador - Electronico de GirojaseriNo ratings yet

- Genexpert Sars-Cov-2 (Covid-19) Vs Genexpert Mdr/Rif (TB) Test. Keep Moving Forward!Document4 pagesGenexpert Sars-Cov-2 (Covid-19) Vs Genexpert Mdr/Rif (TB) Test. Keep Moving Forward!Bashir MtwaklNo ratings yet

- S.S. Hebberd - Philosophy of HistoryDocument320 pagesS.S. Hebberd - Philosophy of HistorySzoha TomaNo ratings yet

- Granta Selector Installation GuideDocument7 pagesGranta Selector Installation Guidem.junaid143103No ratings yet

- Inductive Deductive QuizDocument1 pageInductive Deductive Quizkimbeerlyn doromasNo ratings yet

- Eurocode 3 Stress Ratio Presentation 5 by Lee CKDocument17 pagesEurocode 3 Stress Ratio Presentation 5 by Lee CKKipodimNo ratings yet

- Greaves Cotton Ar 2018 1 PDFDocument168 pagesGreaves Cotton Ar 2018 1 PDFanand_parchureNo ratings yet

- Camo Paint ManualDocument182 pagesCamo Paint Manualwhsprz100% (1)

- Lecture Notes in Statistics 148Document241 pagesLecture Notes in Statistics 148argha48126No ratings yet

- Horizontal Well Drill String DesignDocument23 pagesHorizontal Well Drill String DesignTarek HassanNo ratings yet

- YuYuYu Bonus Chapter - Sonoko AfterDocument14 pagesYuYuYu Bonus Chapter - Sonoko AfterAaron ParkerNo ratings yet

- Government Engineering College Dahod: Dadhichi HostelDocument5 pagesGovernment Engineering College Dahod: Dadhichi HostelSandip MouryaNo ratings yet

- Psychology and AdvertisingDocument59 pagesPsychology and AdvertisingEMMA SHAFFU EL CHACARNo ratings yet

- 2005 تأثير المعالجة المسبقة للبذور عن طريق المجال المغناطيسي على حساسية شتلات الخيار للأشعة فوق البنفسجيةDocument9 pages2005 تأثير المعالجة المسبقة للبذور عن طريق المجال المغناطيسي على حساسية شتلات الخيار للأشعة فوق البنفسجيةMUHAMMED ALSUVAİDNo ratings yet