Download as pdf or txt

You might also like

- The Red Book of Appin Translated by Scarabaeus - Black Magic and Try From The CollectionDocument26 pagesThe Red Book of Appin Translated by Scarabaeus - Black Magic and Try From The CollectionLukas85% (13)

- Haccp PlanDocument1 pageHaccp PlanFrance Cedrick GarciaNo ratings yet

- 21-Day Mind, Body and Spirit DetoxDocument6 pages21-Day Mind, Body and Spirit DetoxAjay TiwariNo ratings yet

- Session 0Document9 pagesSession 0nhmrajnandgaon22No ratings yet

- Closingrates 202307junDocument19 pagesClosingrates 202307junTabrez IrfanNo ratings yet

- Closingrates 202306junDocument20 pagesClosingrates 202306junTabrez IrfanNo ratings yet

- Closingrates 202316mayDocument18 pagesClosingrates 202316mayrizwanarshad786No ratings yet

- Closing Rate Summary From:: Flu No: Pageno: 1 001/2021 P.Kse100 Ind: C.Kse100 Ind: Net ChangeDocument12 pagesClosing Rate Summary From:: Flu No: Pageno: 1 001/2021 P.Kse100 Ind: C.Kse100 Ind: Net ChangeMuhammad DawoodNo ratings yet

- Top 10 Best Stocks Below Rs 10 - Screener List 2Document3 pagesTop 10 Best Stocks Below Rs 10 - Screener List 2bhavdevgstNo ratings yet

- 1 Pavement Design: 1.1 Subgrade PropertiesDocument31 pages1 Pavement Design: 1.1 Subgrade PropertieshaumbamilNo ratings yet

- RSDPIII - 3 Yrs Plan - FinalDocument15 pagesRSDPIII - 3 Yrs Plan - FinalGenetNo ratings yet

- Letter To Zones Regarding Revised BE Targets 17.05.2024Document2 pagesLetter To Zones Regarding Revised BE Targets 17.05.2024CCM's Office PS BranchNo ratings yet

- CM Meeting Large 11.2.2016Document37 pagesCM Meeting Large 11.2.2016UpendraKumarKakarlaNo ratings yet

- Last One Month DT SummaryDocument13 pagesLast One Month DT SummaryshalukNo ratings yet

- Presentation On Progress On Implementation of Environment Management ActivitiesDocument28 pagesPresentation On Progress On Implementation of Environment Management ActivitiesKhairul IslamNo ratings yet

- National PowerDocument8 pagesNational PowerMELVYN GILBERTGNo ratings yet

- Highdividend PriceDocument11 pagesHighdividend PriceKhalid ButtNo ratings yet

- PBI WC MIS DataDocument26 pagesPBI WC MIS DataMurali MohanNo ratings yet

- Company Analysis KRBL Mayank GargDocument27 pagesCompany Analysis KRBL Mayank GargGaneshTatiNo ratings yet

- Financial Analysis of Power SectorDocument19 pagesFinancial Analysis of Power SectorPKNo ratings yet

- Closingrates 202315junDocument19 pagesClosingrates 202315junTabrez IrfanNo ratings yet

- MOSPI SPB Pg148 Rail Gen StatDocument1 pageMOSPI SPB Pg148 Rail Gen StatishitashuklaNo ratings yet

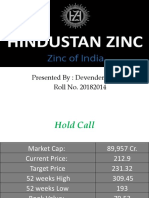

- Hindustan ZincDocument8 pagesHindustan ZincDevender SharmaNo ratings yet

- Closingrates 202309junDocument19 pagesClosingrates 202309junTabrez IrfanNo ratings yet

- Closingrates 202308junDocument19 pagesClosingrates 202308junTabrez IrfanNo ratings yet

- Closingrates 202409aprDocument20 pagesClosingrates 202409aprAbdul AhadNo ratings yet

- Kolkata2 MF & Amfi UpdateDocument1 pageKolkata2 MF & Amfi UpdateAmit SharmaNo ratings yet

- RRB-ALP-Vacancies-Revised-4-July-2024-SarkariExamDocument2 pagesRRB-ALP-Vacancies-Revised-4-July-2024-SarkariExamAzad SinghNo ratings yet

- Annual Report Qa&I/Tlbu/Mbco: L & T Construction PT & DDocument15 pagesAnnual Report Qa&I/Tlbu/Mbco: L & T Construction PT & DKumara SubramanianNo ratings yet

- State Plan AAP 2016-17Document4 pagesState Plan AAP 2016-17Sri KanthNo ratings yet

- Decision ScienceDocument11 pagesDecision ScienceSaksham JainNo ratings yet

- Tabla de Tiempos DanielsDocument13 pagesTabla de Tiempos DanielsSebastian RobaynaNo ratings yet

- Seizure Report As On 24.05.2019Document2 pagesSeizure Report As On 24.05.2019Niharika ChoudharyNo ratings yet

- Closingrates 202323novDocument20 pagesClosingrates 202323novsana.mba8120No ratings yet

- NSE Nifty 50 Quarterly Financial Analysis With EPSDocument1 pageNSE Nifty 50 Quarterly Financial Analysis With EPSRajeev NaikNo ratings yet

- Unit 6Document26 pagesUnit 6Amit BrarNo ratings yet

- Top 10 Best Stocks Below Rs 10 - Screener List 1Document3 pagesTop 10 Best Stocks Below Rs 10 - Screener List 1bhavdevgstNo ratings yet

- National PowerDocument8 pagesNational PowerElvishNo ratings yet

- Up 1Document40 pagesUp 1Subash PanthiNo ratings yet

- Closingrates 202317novDocument21 pagesClosingrates 202317novM.Mudasir ChandioNo ratings yet

- Closingrates 202111junDocument13 pagesClosingrates 202111junUzair JatoiNo ratings yet

- Closingrates 202314junDocument19 pagesClosingrates 202314junTabrez IrfanNo ratings yet

- PENNY STOCK - ScreenerDocument3 pagesPENNY STOCK - Screenerdhruvprep16015No ratings yet

- Modle-O eDocument1 pageModle-O eDanish NawazNo ratings yet

- Management Account PPT Vandit Bathla and Shivam JhaDocument4 pagesManagement Account PPT Vandit Bathla and Shivam JhaVandit BatlaNo ratings yet

- Air Ticket ComparisonDocument2 pagesAir Ticket ComparisonKandal Prek EngNo ratings yet

- Closingrates 202319mayDocument19 pagesClosingrates 202319mayrizwanarshad786No ratings yet

- GAS RRAS Despatch 280322 - 100722Document2 pagesGAS RRAS Despatch 280322 - 100722Surajit BanerjeeNo ratings yet

- Closingrates 202431janDocument21 pagesClosingrates 202431janmdcat466No ratings yet

- Closing Rate Summary From:: Flu No: Pageno: 1 150/2021 P.Kse100 Ind: C.Kse100 Ind: Net ChangeDocument16 pagesClosing Rate Summary From:: Flu No: Pageno: 1 150/2021 P.Kse100 Ind: C.Kse100 Ind: Net ChangeirtazaihtiaqgmailcomNo ratings yet

- Power Consumption Report Sept 2022Document1 pagePower Consumption Report Sept 20228269287013No ratings yet

- Consolidated Data On Commission and Expenses Paid To Distributors During FY 2020-21 and Additional DisclosuresDocument16 pagesConsolidated Data On Commission and Expenses Paid To Distributors During FY 2020-21 and Additional DisclosuresChandra PrakashNo ratings yet

- AMRUT Progress MAWS 20.03.2020 REVISED 11.31 Am 19.03.2020Document136 pagesAMRUT Progress MAWS 20.03.2020 REVISED 11.31 Am 19.03.2020JitendraHatwarNo ratings yet

- NHAI Toll Collection 1Document9 pagesNHAI Toll Collection 1prabhu chand alluriNo ratings yet

- Year 2013 2014 2015 2016 2017 Latest: CompetitionDocument3 pagesYear 2013 2014 2015 2016 2017 Latest: CompetitionDahagam SaumithNo ratings yet

- SPSS - Ew AsigesDocument10 pagesSPSS - Ew AsigesBAGAS PUTRA PRATAMANo ratings yet

- MFG Asset Mgtpack June 21Document21 pagesMFG Asset Mgtpack June 21muthum44499335No ratings yet

- Closingrates 202313junDocument19 pagesClosingrates 202313junTabrez IrfanNo ratings yet

- Tarea 3.SFTV.Document28 pagesTarea 3.SFTV.Luis Angel Romero CarrascoNo ratings yet

- HQ - Sr. DCM Meeting 14.11.14Document16 pagesHQ - Sr. DCM Meeting 14.11.14ccm erNo ratings yet

- ClosingDocument13 pagesClosingShujauddin QureshiNo ratings yet

- StatisticsDocument22 pagesStatisticskinzah imranNo ratings yet

- Bluewater Cruisers: A By-The-Numbers Compilation of Seaworthy, Offshore-Capable Fiberglass Monohull Production Sailboats by North American Designers: A Guide to Seaworthy, Offshore-Capable Monohull SailboatsFrom EverandBluewater Cruisers: A By-The-Numbers Compilation of Seaworthy, Offshore-Capable Fiberglass Monohull Production Sailboats by North American Designers: A Guide to Seaworthy, Offshore-Capable Monohull SailboatsRating: 5 out of 5 stars5/5 (2)

- Morningstarreport 20240205111609Document1 pageMorningstarreport 20240205111609rishabhsethiaNo ratings yet

- Ew 201016 C&P PDFDocument55 pagesEw 201016 C&P PDFrishabhsethiaNo ratings yet

- Nat ZuraDocument88 pagesNat ZurarishabhsethiaNo ratings yet

- Flow Chart Solvent Extraction 2Document4 pagesFlow Chart Solvent Extraction 2rishabhsethiaNo ratings yet

- Flow Chart Solvent Extraction 2Document4 pagesFlow Chart Solvent Extraction 2rishabhsethiaNo ratings yet

- Negotiation ProcessDocument6 pagesNegotiation ProcessAkshay NashineNo ratings yet

- Module 1Document17 pagesModule 1Richilien Teneso43% (14)

- UMRAH Supplications DUADocument10 pagesUMRAH Supplications DUAsamNo ratings yet

- Studies On Soil Structure Interaction of Multi Storeyed Buildings With Rigid and Flexible FoundationDocument8 pagesStudies On Soil Structure Interaction of Multi Storeyed Buildings With Rigid and Flexible FoundationAayush jhaNo ratings yet

- Lecture 5 Theory of AccidentDocument14 pagesLecture 5 Theory of Accidenthayelom100% (1)

- Global Clothing ZaraDocument19 pagesGlobal Clothing ZaraDaniel ArroyaveNo ratings yet

- Full Download 2014 Psychiatric Mental Health Nursing Revised Reprint 5e Test Bank PDF Full ChapterDocument36 pagesFull Download 2014 Psychiatric Mental Health Nursing Revised Reprint 5e Test Bank PDF Full Chapterpassim.pluvialg5ty6100% (17)

- DOMINODocument16 pagesDOMINOBerat DalyabrakNo ratings yet

- Campaign For Tobacco Free KidsDocument1 pageCampaign For Tobacco Free KidsNurses For Tobacco ControlNo ratings yet

- TELECONFERENCINGDocument5 pagesTELECONFERENCINGAbhinav SharmaNo ratings yet

- Dell's Working CapitalDocument17 pagesDell's Working CapitalJo Ryl100% (2)

- The Return of JesusDocument5 pagesThe Return of JesusMick AlexanderNo ratings yet

- Karur Vysya Bank Employees' Union: 11th Bipartite Arrears Calculation Package - ClerkDocument10 pagesKarur Vysya Bank Employees' Union: 11th Bipartite Arrears Calculation Package - ClerkDeepa ManianNo ratings yet

- Accounting Standards - Handwritten Notes - Udesh Regular - Group 1Document24 pagesAccounting Standards - Handwritten Notes - Udesh Regular - Group 1Uday TomarNo ratings yet

- Gilbert Clayton PapersDocument37 pagesGilbert Clayton PapersbosLooKiNo ratings yet

- Conceptual Design of An Automotive Composite Brake Pedal: Mohd Sapuan Salit, Mohd Syed Ali Molla and MD Liakot AliDocument5 pagesConceptual Design of An Automotive Composite Brake Pedal: Mohd Sapuan Salit, Mohd Syed Ali Molla and MD Liakot Aliseran ünalNo ratings yet

- Petition For Writ of Kalikasan (Marj)Document4 pagesPetition For Writ of Kalikasan (Marj)Myka FloresNo ratings yet

- D13. Physical AppearanceDocument2 pagesD13. Physical AppearanceNguyen Bao LIenNo ratings yet

- # Pembagian Kelas Alkes Per KategoriDocument41 pages# Pembagian Kelas Alkes Per KategoriR.A.R TVNo ratings yet

- Disaster Recovery Best PracticesDocument8 pagesDisaster Recovery Best PracticesJose RosarioNo ratings yet

- Break Even AnalysisDocument18 pagesBreak Even AnalysisSMHE100% (10)

- Santiago City, Isabela: University of La Salette, IncDocument1 pageSantiago City, Isabela: University of La Salette, IncLUCAS, PATRICK JOHNNo ratings yet

- Chords Like Jeff BuckleyDocument5 pagesChords Like Jeff BuckleyTDROCKNo ratings yet

- Organisational BehaviourDocument279 pagesOrganisational BehaviourSumitha SelvarajNo ratings yet

- GenEd - Lumabas Jan 2022Document4 pagesGenEd - Lumabas Jan 2022angelo mabulaNo ratings yet

- Lab 6 Shouq PDFDocument10 pagesLab 6 Shouq PDFreemy100% (1)

- Ms. Rossana Hoyos DíazDocument19 pagesMs. Rossana Hoyos DíazMaryNo ratings yet