Download as doc, pdf, or txt

You might also like

- Summary: Financial Intelligence: Review and Analysis of Berman and Knight's BookFrom EverandSummary: Financial Intelligence: Review and Analysis of Berman and Knight's BookNo ratings yet

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Basel II and Credit RiskDocument18 pagesBasel II and Credit RiskVasuki BoopathyNo ratings yet

- Principles and CharacteristicsDocument12 pagesPrinciples and CharacteristicsFloyd DaltonNo ratings yet

- Accounting Concepts and ConventionsDocument4 pagesAccounting Concepts and ConventionssrinugudaNo ratings yet

- Accounting Conventions: Monetary MeasurementDocument5 pagesAccounting Conventions: Monetary MeasurementAli HaiderNo ratings yet

- Review Na Sa Conceptual FrameworkDocument5 pagesReview Na Sa Conceptual FrameworkMARY ROSENo ratings yet

- ASPL2 Activity 1n2 DoneDocument4 pagesASPL2 Activity 1n2 DoneConcepcion FamilyNo ratings yet

- Attached With. Q1. What Do You Mean by Accounting'? Explain The Various Concepts of Accounting and The Need For Having Accounting Standards?Document10 pagesAttached With. Q1. What Do You Mean by Accounting'? Explain The Various Concepts of Accounting and The Need For Having Accounting Standards?HozefadahodNo ratings yet

- The Objective of General Purpose Financial ReportingDocument86 pagesThe Objective of General Purpose Financial ReportingAlex liaoNo ratings yet

- Fia Ffa Chapter 3Document8 pagesFia Ffa Chapter 3AngelaNo ratings yet

- IASB Conceptual FrameworkDocument26 pagesIASB Conceptual FrameworkALEXERIK23100% (4)

- Chapter 3 - Conceptual FrameworkDocument2 pagesChapter 3 - Conceptual FrameworkSyed Huzaifa SamiNo ratings yet

- FA - The Qualitative Characteristics of Financial InformationDocument5 pagesFA - The Qualitative Characteristics of Financial InformationOwen GradyNo ratings yet

- AccountsDocument9 pagesAccountsSivaNo ratings yet

- B291 TheoryDocument9 pagesB291 TheoryNajwa Al-khateebNo ratings yet

- 2 Accounting Concepts and ConventionsDocument5 pages2 Accounting Concepts and Conventionsazra khanNo ratings yet

- BKAF 3083 Tutorial 2 Group G-4Document5 pagesBKAF 3083 Tutorial 2 Group G-4Alex YeapNo ratings yet

- Qualitative CharactetisticsDocument9 pagesQualitative CharactetisticsKristina Angelina ReyesNo ratings yet

- Null 2Document9 pagesNull 2Ali nawazNo ratings yet

- Conceptual Framework Module 2Document6 pagesConceptual Framework Module 2Jaime LaronaNo ratings yet

- Merged Fa Cwa NotesDocument799 pagesMerged Fa Cwa NotesAkash VaidNo ratings yet

- Accounting Concepts and ConventionsDocument4 pagesAccounting Concepts and ConventionsSaumitra TripathiNo ratings yet

- Chapter 5 Principls and ConceptsDocument10 pagesChapter 5 Principls and ConceptsawlachewNo ratings yet

- Fundamentals of Accounting 2Document5 pagesFundamentals of Accounting 2Ale EalNo ratings yet

- Chapter 3 Conceptual FrameworkDocument11 pagesChapter 3 Conceptual FrameworkEshe Rae Arquion IINo ratings yet

- Accounting Concepts and ConventionsDocument22 pagesAccounting Concepts and ConventionsMishal SiddiqueNo ratings yet

- Accounting Concepts and ConventionsDocument18 pagesAccounting Concepts and ConventionsDr. Avijit RoychoudhuryNo ratings yet

- Conceptual Framework Underlying Financial ReportingDocument24 pagesConceptual Framework Underlying Financial ReportingLạc LốiNo ratings yet

- Chapter#2 True and Fair View: Assurance EngagementsDocument4 pagesChapter#2 True and Fair View: Assurance EngagementsArham khanNo ratings yet

- Prof Dev 5 (Activity 2)Document7 pagesProf Dev 5 (Activity 2)Arman CabigNo ratings yet

- HBS - Financial AccountingDocument3 pagesHBS - Financial Accountingrahul2014mehtaNo ratings yet

- Conceptual Framework For Financial Reporting Resume Ch. 2Document6 pagesConceptual Framework For Financial Reporting Resume Ch. 2Dhivena JeonNo ratings yet

- Task 1:: Fundamental Accounting ConceptsDocument24 pagesTask 1:: Fundamental Accounting Conceptsisha_fagar008No ratings yet

- Enter Your Search TermsDocument5 pagesEnter Your Search Termskrishna1427No ratings yet

- Pragyani S Maharjan 12/8/15 Accounting 507 - Text Chapter 2 - Conceptual Framework Basic QuestionsDocument6 pagesPragyani S Maharjan 12/8/15 Accounting 507 - Text Chapter 2 - Conceptual Framework Basic QuestionsPragyani ShresthaNo ratings yet

- Kieso15e ContinuingCase Sols Vol1Document41 pagesKieso15e ContinuingCase Sols Vol1HảiAnhInviNo ratings yet

- Meaning and Nature of Accounting Principle: Veena Madaan M.B.A (Finance)Document25 pagesMeaning and Nature of Accounting Principle: Veena Madaan M.B.A (Finance)JenniferNo ratings yet

- Accounting NoteDocument96 pagesAccounting NoteFahomeda Rahman SumoniNo ratings yet

- Conceptual Framwork - Qualitative CharacteristicsDocument11 pagesConceptual Framwork - Qualitative Characteristicsmhel cabigonNo ratings yet

- FrameworkDocument3 pagesFrameworkshayanNo ratings yet

- Financial Accounting AC111Document7 pagesFinancial Accounting AC111sampalukangaNo ratings yet

- Accounting Notes Essential Features of Accounting PrinciplesDocument13 pagesAccounting Notes Essential Features of Accounting PrinciplesGM BalochNo ratings yet

- Introductory Financial Accounting: ACCN104Document28 pagesIntroductory Financial Accounting: ACCN104TinoManhangaNo ratings yet

- Financial Statement Analysis CourseworkDocument8 pagesFinancial Statement Analysis Courseworkpqltufajd100% (2)

- Accounting Concept and Principles - 20160822Document32 pagesAccounting Concept and Principles - 20160822jnyamandeNo ratings yet

- Chapter 2 - Basic Accounting ConceptsDocument29 pagesChapter 2 - Basic Accounting ConceptsDan RyanNo ratings yet

- Chapter 3 Qualitative CharacteristicsDocument15 pagesChapter 3 Qualitative CharacteristicsMicsjadeCastilloNo ratings yet

- Accounting Concepts and ConventionsDocument2 pagesAccounting Concepts and ConventionsBhagya FernandoNo ratings yet

- Chapter 3Document7 pagesChapter 3Tasebe GetachewNo ratings yet

- Bus Fin Topic 3Document18 pagesBus Fin Topic 3Nadjmeah AbdillahNo ratings yet

- Questions - Chapter 2Document3 pagesQuestions - Chapter 2Mohammad Salim HossainNo ratings yet

- CONCEPTUAL FRAMEWORK.docxDocument3 pagesCONCEPTUAL FRAMEWORK.docxCenelyn PajarillaNo ratings yet

- Accounting Concepts Are The Broad Assumptions Which Underline The Periodic Financial Accounts of Business EnterprisesDocument5 pagesAccounting Concepts Are The Broad Assumptions Which Underline The Periodic Financial Accounts of Business EnterprisesHenry MayambuNo ratings yet

- MB41 Ans IDocument14 pagesMB41 Ans IAloke SharmaNo ratings yet

- Accounting ConceptsDocument11 pagesAccounting ConceptssyedasadaligardeziNo ratings yet

- Lesson 2 ACCOUNTING AS THE LANGUAGE OF BUSINESSDocument9 pagesLesson 2 ACCOUNTING AS THE LANGUAGE OF BUSINESSamora elyseNo ratings yet

- F & M AccountingDocument6 pagesF & M AccountingCherry PieNo ratings yet

- MBA-AFM Theory QBDocument18 pagesMBA-AFM Theory QBkanikaNo ratings yet

- Chapter 2 Accounting Concepts and Principles PDFDocument12 pagesChapter 2 Accounting Concepts and Principles PDFAnonymous F9lLWExNNo ratings yet

- Mastering Bookkeeping: Unveiling the Key to Financial SuccessFrom EverandMastering Bookkeeping: Unveiling the Key to Financial SuccessNo ratings yet

- Bank StatementDocument2 pagesBank StatementNicolae DiaconuNo ratings yet

- A Study On Customer Satisfaction at HDFC Bank, VijayapuraDocument70 pagesA Study On Customer Satisfaction at HDFC Bank, Vijayapurapatelhotel786No ratings yet

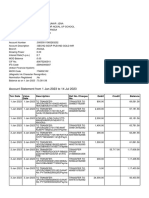

- Account Statement From 1 Jan 2023 To 14 Jul 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Jan 2023 To 14 Jul 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAmit Kumar JenaNo ratings yet

- O F F E R 2 B MT 103 2way Swift 10+4 Etf 1302 KulDocument2 pagesO F F E R 2 B MT 103 2way Swift 10+4 Etf 1302 KulPool AtalayaNo ratings yet

- Trade and Cash Discount MAT112Document2 pagesTrade and Cash Discount MAT112syafiqahNo ratings yet

- What Is Sap Fico An Introduction of Fi and Co ModuleDocument4 pagesWhat Is Sap Fico An Introduction of Fi and Co ModuleFahim JanNo ratings yet

- Frequently Asked Questions - Maybank Visa DebitDocument4 pagesFrequently Asked Questions - Maybank Visa DebitholaNo ratings yet

- Bisbull 38Document9 pagesBisbull 38readerNo ratings yet

- Audit of Receivables and Sales SolutionsDocument16 pagesAudit of Receivables and Sales SolutionsNICELLE TAGLENo ratings yet

- Risk and InsuranceDocument63 pagesRisk and InsuranceGuruKPO100% (2)

- Audit and Tax AssignmentDocument3 pagesAudit and Tax AssignmentPrathamesh WaghNo ratings yet

- CHAPTER 25 - Borrowing CostsDocument6 pagesCHAPTER 25 - Borrowing CostsRosee D.No ratings yet

- Preodic Class TestDocument5 pagesPreodic Class TestMOHAMMAD SYED AEJAZNo ratings yet

- Current & Saving Account Statement: Vishnu Gupta S/O Jagdish Gupta HNO 417 Mo Arya Nagar Shiv Ganj EtahDocument6 pagesCurrent & Saving Account Statement: Vishnu Gupta S/O Jagdish Gupta HNO 417 Mo Arya Nagar Shiv Ganj Etahvishnu guptaNo ratings yet

- Account Statement From 1 Jun 2020 To 17 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Jun 2020 To 17 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRathnakar ReddyNo ratings yet

- PT MSM TBK 30 Sept 2022 KONSOL - Q3 PDFDocument67 pagesPT MSM TBK 30 Sept 2022 KONSOL - Q3 PDFandry4jcNo ratings yet

- Home Office, Branch and Agency Accounting - QuizDocument6 pagesHome Office, Branch and Agency Accounting - QuizJohn Mark VerarNo ratings yet

- CERSAI Search Report 200287459334 For Debtor Based Search 21 11 2023 13 13 21 601Document4 pagesCERSAI Search Report 200287459334 For Debtor Based Search 21 11 2023 13 13 21 601advocatemayankvijNo ratings yet

- Contoh Tugasan AccountDocument20 pagesContoh Tugasan AccountMuhammad IddinNo ratings yet

- Auditing II AssignmentDocument9 pagesAuditing II AssignmentAnwarNo ratings yet

- Salma Barkah - Dasar Akuntansi - Latihan E2-9 & E2-10Document6 pagesSalma Barkah - Dasar Akuntansi - Latihan E2-9 & E2-10Salma BarkahNo ratings yet

- Tugas I Pengantar Akuntansi IDocument6 pagesTugas I Pengantar Akuntansi IWiedya fitrianaNo ratings yet

- Associated Bank v. CADocument19 pagesAssociated Bank v. CAGia DimayugaNo ratings yet

- Research Report On Loans and Advance SystemDocument16 pagesResearch Report On Loans and Advance SystemRavi DhudiyaNo ratings yet

- Exhibit A Generic - Bank Readiness Notification (UBS To La Caixa) 7-3-13Document2 pagesExhibit A Generic - Bank Readiness Notification (UBS To La Caixa) 7-3-13lion100_saadNo ratings yet

- Total Retail Bond Trading 1511Document307 pagesTotal Retail Bond Trading 1511Sorken75No ratings yet

- How Hedge Funds Are StructuredDocument17 pagesHow Hedge Funds Are Structuredvarun khajuriaNo ratings yet

- FINANCIAL REPORTING 2.1nov 2016Document31 pagesFINANCIAL REPORTING 2.1nov 2016Seli KemNo ratings yet

- 11 Accountancy TP Ch03 01 Journal EntriesDocument2 pages11 Accountancy TP Ch03 01 Journal EntriesBhavi ChaudharyNo ratings yet